by Adam Hartung | Mar 6, 2018 | In the Swamp, Investing, Retail, Scenario Planning

On February 20, 2018 Walmart’s stock had its biggest price drop ever. And the second biggest percentage decline ever. Even though same store sales improved, investors sold off the stock in droves. And after a pretty healthy recent valuation run-up.

What happened? Simply put, Walmart said its on-line sales slowed and its cost of operations rose, slowing growth and cramping margins. In other words, even though it bought Jet.com Walmart is still a long, long way from coming close to matching the customer relationship and growth of Amazon.com. And (surprise, surprise) margins in on-line aren’t an easy thing — as Amazon’s thin margins for 15 years have demonstrated.

In other words, this was completely to be expected. Walmart is a behemoth with no adaptability. For decades the company has been focused on how to operate its warehouses and stores, and beat up its suppliers. Management had to be drug, kicking and screaming, into e-commerce. And failing regularly it finally made an acquisition. But to think that Jet.com was going to change WalMart’s business model into a growing, high profit operation any time soon was foolish. Management still wants people in the store, first and foremost, and really doesn’t understand how to do anything else.

All the way back in 2005, I wrote that Walmart was too big to learn, and was unwilling to create white space teams to really explore growing e-commerce (hence the belated Jet-com acquisition.) In 2007, I wrote that calling Walmart a “mature” competitor with huge advantages was the wrong way to view the company already under attack by all the e-commerce players. In July, 2015 Amazon’s market cap exceeded Walmart’s, showing the importance of retail transformation on investor expectations. By February, 2016 there were 10 telltale signs Walmart was in big trouble by a changing retail market. And by October, 2017 it was clear the Waltons were cashing out of Walmart, questioning why any investor should remain holding the stock.

It really is possible to watch trends and predict future markets. And that can lead to good predictions about the fates of companies. The signs were all there that Walmart shouldn’t be going up in value. Hope had too many investors thinking that Walmart was too big to stumble – or fail. But hope is not how you should invest. Not for your portfolio, and not for your business. Walmart should have dedicated huge sums to e-commerce 15 years ago, now it is playing catch up with Amazon.com, and that’s a race it simply won’t win. Are you making the right investment decisions for your business early enough? Or will you stumble like Walmart?

by Adam Hartung | Feb 27, 2018 | Growth Stall, Innovation, Investing, Software

This February, Warren Buffett admitted he had no faith in IBM. After accumulating a huge position, by 4th quarter of 2017 he sold out almost the entire Berkshire Hathaway position. He lost faith in the IBM CEO Virginia (Ginni) Rometty, who talked big about a turnaround, but it never happened.

Mr. Buffett would have been wise to stopped having “faith” long ago. All the way back in May, 2014 I wrote that IBM was not going to be a turnaround. CEO Rommetty was spending ALL its money on share buybacks, rather than growing its business. The Washington Post made IBM the “poster child” for stupid share buybacks, pointing out that spending over $8B on repurchases had maintained earnings-per-share, and propped up the stock price, but giving IBM the largest debt-to-equity ratio of comparable companies.

IBM was already in a Growth Stall, something about which I’ve written often. Once a company stalls, its odds  of growing at 2%/year fall to a mere 7%. But it was clear then that the CEO was more interested in financial machinations, borrowing money to repurchase shares and prop up the stock, rather than actually investing in growing the company. The once great IBM was out of step with the tech market, and had no programs in place to make it an industry leader in the future.

of growing at 2%/year fall to a mere 7%. But it was clear then that the CEO was more interested in financial machinations, borrowing money to repurchase shares and prop up the stock, rather than actually investing in growing the company. The once great IBM was out of step with the tech market, and had no programs in place to make it an industry leader in the future.

By April, 2017 it was clear IBM was a disaster. By then we had 20 consecutive quarters of declining revenue. Amazing. How Rometty kept her job was completely unclear. Five years of shrinkage, while all investments were in buying the stock of its shrinking enterprise – intended to hide the shrink! CEO Rometty continued promising a turnaround, with vague references to the “wonderful” Watson program. But it was clear, Buffett (and everyone else) needed to get out in 2014. So Berkshire ate its losses, took the money and ran.

Have you learned your lesson? As an investor are you holding onto stocks long after leadership has shown they have no idea how to grow revenues? If so, why? Hope is not a strategy.

As a leader, are you still forecasting hockey stick turnarounds, while continuing to invest in outdated products and businesses? Are you hoping your past will somehow create your future, even though competitors and markets have moved on? Are you leading like Rometty, hoping you can hide your failures with financial machinations and Powerpoint presentations about how things will turn your way in the future – even though those assumptions are made out of hole cloth?

It’s time to get real about your investments, and your business. When revenues are challenged, something bad is happening. It’s time to do something. Fast. Before a bad quarter becomes 20, and everyone is giving up.

by Adam Hartung | Feb 13, 2018 | Entertainment, Innovation, Investing, Television, Web/Tech

On January 23 Netflix’ value rose to $100B. The stock is now trading north of $250/share. A year ago it was $139/share. An 80% increase in just 12 months. And long-term investors have done very well. Five years ago (January, 2013) the stock was trading at $24/share – so the valuation has increased 10-fold in 5 years! A decade ago it was trading for $3/share – so if you got in early (NFLX went public in June, 2002) you are up 83X your initial investment (meaning $1,000 would be worth $83,000.)

Back in 2004 I wrote that Blockbuster was dead meat – because by going after streaming Netflix would make Blockbuster obsolete. Netflix was using external data to project its future, and thus its strategy was not to defend & extend its DVD rental business but to spend strongly to grow the replacement. In 2010 I wrote that Netflix had projected the complete demise of DVDs by 2013, and was thus investing all its resources into streaming in order to be the market leader. At the time NFLX was $15.68. Over the next year it took off, tripling in value to $42.16. By cannibalizing DVDs it’s strategy was to leave its competition in a dying marketplace.

But, investors weren’t as sure of the Netflix strategy as I was. They feared cannibalizing DVDs would cut out the “core” of Netflix and kill the company. By October, 2011 the stock had tumbled to $12 (a drop of over 70%.) But, with the stock at new lows after a year of declines I optimistically wrote “The Case for Buying Netflix. Really.” I told readers the stock analysts were wrong, and the Netflix strategy was spot-on.

Netflix went nowhere for the next year, trading between $9 and $12. But then in December, 2012 investors started seeing the results of Netflix strategy, with fast growing streaming subscriber rates. By January, 2014 the stock was trading north of $52, so those who bought when my article published made a 400% return in just over 2 years! By March, 2015 NFLX was up another 23%, to $62 when I told readers “Netflix Valuation Was Not a House of Cards.” The Netflix strategy to dominate streaming by offering its own content may have shocked a lot of people, due to the investment size, but it was the strategy that would allow Netflix to grow subscribers globally. That has driven the last jump, to $250 in just under 3 years – another 400%+ return!

Strategy matters- to company performance, and thus long-term investor returns. Netflix has been a volatile stock, and it has had plenty of naysayers. These were people looking only short-term, and fearful of strategic pivots that have proven highly valuable. If you want your company, and your investment portfolio, to succeed it is imperative you understand external trends and use them to develop the right strategy. And heed my forecasts.

by Adam Hartung | Feb 6, 2018 | Innovation, Mobile, Software, Web/Tech

InvestorPlace.com declared Snap stock will be a big disappointment in 2018. Bad news for investors, because SNAP was an enormous disappointment in 2017. After going public at $27/share in early March, the stock dropped to $20 by mid-March, then just kept dropping until it bottomed at just under $12 in August. Since then the stock has largely gone sideways at $15.

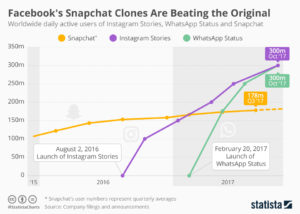

This was not unexpected. As I wrote in April, Snapchat was not without competition and was unlikely to be a long-term winner. Even though Snapchat and its Stories feature grew popular with teenagers 14 to 19, in August, 2016 Facebook launched Instagram Stories as a direct competitor. In just 7 months – just as SNAP went public – Instagram Stories had more users than Snapchat. It was clear then if you wanted to make money on the photo and video sharing trends, investors were better off to own Facebook stock and avoid the newly available SNAP shares (stock, not pix!)

Now the situation is far worse. Facebook launched WhatsApp Status as another competitive product in February, 2017 and it took less than 3 months for its user base to exceed Snapchat. As the chart below shows, by October, 2017 Stories and Status each had 300 million users, while Snapchat was mired at 180 million users. With only 30% the users of Facebook, Snapchat has little chance to succeed against the social media powerhouse.

Statista

Facebook is now a very large company. But, it has shown it is adaptable. Rather than sticking to its original market, Facebook went mobile and has launched new products as fast as competitors tried to carve out niches. The question is, are you constantly scanning the horizon for new products and adapting – fast – to keep your customers and grow? Or are you stuck trying to defending your old business while upstarts carve up your market?”

by Adam Hartung | Jan 23, 2018 | Disruptions, Investing, Retail, Trends

Business Insider is projecting a “tsunami” of retail store closings in 2018 — 12,000 (up from 9,000 in 2017.) Also, the expect several more retailers will file bankruptcy, including Sears.

Duh. Nothing surprising about those projections. In mid-2016, Wharton Radio interviewed me about Sears, and I made sure everyone clearly understood I expect it to fail. Soon. In December, 2016 I overviewed Sears’ demise, predicted its inevitable failure, and warned everyone that all traditional retail was going to get a lot smaller. I again recommended dis-investing your portfolio of retail. By March, 2017 the handwriting was so clear I made sure investors knew that there were NO traditional retailers worthy of owning, including Walmart. By October, 2017 I wrote about the Waltons cashing out their Walmart ownership, indicating nobody should be in the stock – or any other retailer.

The trend is unmistakable, and undeniable. The question is – what are you going to do about it? In July, 2015 Amazon became more valuable than Walmart, even though much smaller. I explained why that made sense – because the former is growing and the latter is shrinking. Companies that leverage trends are always worth more. And that fact impacts YOU! As I wrote in February, 2017 the “Amazon Effect” will change not only your investments, but how you shop, the value of retail real estate (and thus all commercial real estate,) employment opportunities for low-skilled workers, property and sales tax revenues for all cities impacting school and infrastructure funding, and all supply chain logistics. These trends are far-reaching, and no business will be untouched.

Don’t just say “oh my, retailers are crumbling” and go to the next web page. You need to make sure your strategy is leveraging the “Amazon Effect” in ways that will help you grow revenues and profits. Because your competition is making plans to use these trends to hurt your business if you don’t make the first move. Need help?

by Adam Hartung | Dec 22, 2017 | Advertising, Film, Innovation, Marketing, Trends

Here in late 2017, the biggest trends are: the 24 hour news cycle, animosity in broadcast and online media, fatigue from constant connection and interaction, international threats and our political climate. The holiday season is in the background struggling for attention.

How are people tuning out of this cacophony to get in the mood for the holidays?

The answer: Christmas movies! And which channel has 75% share of the new movies in 2017? If you have watched any TV since October, you’d know that it’s The Hallmark Channel. THC has produced over 20 original movies for the 2017 Christmas season and has seen viewership grow by 6.7% per year since 2013. THC is on track to surpass the 2016 season in viewership and its brand image is solidly wholesome.

Starting in October, THC runs seasonal programming with its successful “The Good Witch” series (no vampires!) and continues with “Countdown to Christmas” featuring original Hallmark-produced content.

Hallmark spent decades preparing to capture the benefits of these trends. It had become a source of family oriented, holiday-themed programming especially popular in recent years. Once only an ink and paper company, Hallmark expanded strategically in the 1970s with ornaments and cultural greeting cards and again in 1984 with its acquisition of Crayola drawing products. The company moved into direct retail in 1986 and ecommerce in the mid-1990s. Hallmark eCards was launched in 2005.

Hallmark capitalized on branded media content originally to support the core business and it now generates profits as a standalone business. In 2001, the Hallmark Channel was launched. The Hallmark Movie Channel was developed in 2004 which became Hallmark Movies and Mysteries in 2014. This year, the Hallmark Drama channel was launched further leveraging the brand.

Many companies sponsored radio shows in the 1920s through the war years. Serials featuring one company’s products appeared in 1928 on radio. In 1952, Proctor and Gamble sponsored the first TV soap opera featuring one company (“The Guiding Light”). But The Hallmark Hall of Fame was there first on Christmas Eve in 1951 sponsoring a made-for-TV opera, “Amahl and the Night Visitors.”

Written by Gian Carlo Menotti in less than two months and timed for a one hour TV slot, “Amahl” has become, probably, the most performed opera in history.

Hallmark wasn’t the first mover in sponsored media content, but it had learned to experiment with new media. The company was positioned to take advantage of the trend toward family friendly broadcast content and this year was ready to give the nation a place to rest and escape from the chaos. A bit like the story of Amahl and Christmas itself.

Once just a card company, Hallmark followed market trends to expand its business and become a leader in content marketing which is now one of the hottest areas in all marketing. And both the new video content and large library were ready for the current trend- streaming video!

by Adam Hartung | Dec 9, 2017 | Advertising, Investing, Television, Trends, Web/Tech

Facebook shareholders should be cheering. And if you don’t own FB, you should be asking yourself why not. The company’s platform investments continue to draw users, and advertisers, in unprecedented numbers.

With permission: Statista

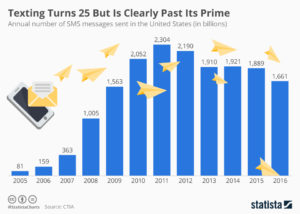

People over 40 still might text. But for most younger people, messaging happens via FB Messenger or WhatsApp. Text messages have thus been declining in the USA. Internationally, where carriers still frequently charge for text messages, the use of both Facebook products dominates over texting. Both Facebook products now are leaders in internet usage.

And as their use grows, so do the ad dollars.

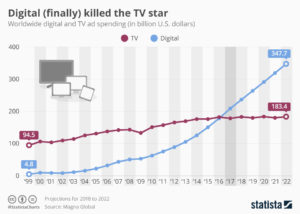

With permission: Statista

As this chart shows, in 2017 ad spending on digital outpaced money spent on TV ads. And TV spending, like print and radio, is flat to declining. While digital spending accelerates. And the big winner here is the platform getting the most eyeballs – which would be Facebook (and Google.)

Looking at the trends, Facebook investors should feel really good about future returns. And if you don’t own Facebook shares, why not?

by Adam Hartung | Nov 17, 2017 | Finance, Investing, Leadership, Web/Tech

What Business Leaders Can Learn From Bitcoin Fanatics

On August 15, Bitcoin rose to $4,000, I wrote a column about the crypto-currency. At the time, I thought Bitcoin was reasonably obscure, and I doubted there would be many readers. I was amazed when the column went semi-viral, and it has had almost 350,000 reads. But even more amazing was that the column generated an enormous amount of feedback. From email responses to Facebook remarks and Tweets I was inundated with people who, largely, wanted my head.

I found this confounding and fascinating. Why would an article that simply said a crypto-currency was speculative draw such an enormous response? And why such hostility? Just as I had not anticipated much readership, I certainly did not anticipate the reaction. These factors led me to research Bitcoin owners, and develop some theories on why Bitcoin is such a big deal to its enthusiasts.

1 – Bitcoin owners want the value to increase

I made the mistake of thinking of Bitcoins as a form of cash. Something to be spent. But I discovered most owners are holding Bitcoins as an asset. Because there are technical limits on how many Bitcoins can be created, and how quickly, these owners see the possibility of Bitcoin value increasing. As “investors” in Bitcoins, they don’t want anything (like a negative column) to put a damper on Bitcoin’s ability to rise.

Such speculation is not uncommon. Many people buy land, gold, silver and diamonds because they expect limited supply, and growing demand, to cause the value to rise. Other people buy Andy Warhol prints, vintage automobiles, signatures of historical people or baseball cards for the same reason. I prefer to call this speculation, but these people refer to themselves as investors in rare assets. Bitcoin investors see themselves in this camp, only they think Bitcoins are less risky than the other assets.

Regardless the nomenclature, anyone who is buying and holding Bitcoins would be unhappy to hear that the asset is risky, or potentially a bad holding. But unlike all those other items I mentioned, Bitcoins are not physical. To some extent merely owning the other assets has a certain amount of its own reward. One can enjoy a diamond ring, or a Warhol print on the wall while waiting to learn if its value goes up or down. But Bitcoins are just computer 1s and 0s, and really a new kind of asset (crypto-currency.) These investors are considerably younger on average, a bit more skittish, and considerably more outspoken regarding the future of their investment – and those who would be negative on Bitcoins.

While wanting their asset value to rise makes sense, it is rare that speculators have been as passionate as those who responded on Bitcoin. I’ve written about many companies I feared would lose value, and thus were speculative, but those columns did not create the fervor with responses like those regarding Bitcoin

2 – Confusion between Bitcoin and Blockchain technology

Blockchain is the underlying technology upon which Bitcoins are created. I have now read a few hundred articles on Bitcoins and Blockchain.

I was struck at just how confusing authors on these topics can be. They will say the two are very different, but then go on at great length that if you believe in Blockchain you should believe in Bitcoins. Few columns on Blockchain don’t talk about Bitcoins. And all Bitcoin authors talk about the wonders of Blockchain.

There is no doubt that Blockchain technology is new to the scene, and shows dramatic promise. Many large organizations are investigating using Blockchain for uses from financial transaction clearing to medical record retention. This is serious technology, and as it matures there are a great many people working to make it as trustworthy as (no, more trustworthy than) the internet. Just as the web requires some rules about URLs, domain naming, page serving, data accumulation, site direction, etc. there are serious people thinking about how to make Blockchain consistent in its application and use – which could open the door for many opportunities to streamline the digital world and make our lives better, and possibly more secure.

There were many, many people who disliked my skeptical view of Bitcoins, and based their entire argument for Bitcoinvalue on their belief in Blockchain. I was schooled over and again on the strength of Blockchain and its many future applications. And I was told that Blockchain technology inherently meant that Bitcoins have to go up in value. Buying Bitcoins was frequently referred to as investing in “Internet 2.0” due to the Blockchain technology.

It is clear that without Blockchain you could not have Bitcoins. But the case demanding one owns Bitcoin because it is built on Blockchain (“the technology of the future” as it is referred to by many) is still being developed. To them I was the one who was confused, unable to see the future they saw built on Blockchain. There were hoards of people who were almost religious in their Bitcoin faith, indicating that there was yet still more underlying their passion.

3 – As trust in government declines, there is growing trust in technology

More than ever in modern history, people have little faith in their government. In the USA, favorable opinions of Congress and its leaders are nearly non-existent. And favorable opinions for the current President started out below normal, and have gotten considerably worse. It is reported now with some regularity that Americans have little trust in the President, Congress, Courts – and the Federal Reserve.

There were, literally, hundreds of people who sent messages talking about the failure of government based currencies. Most of these examples were South American, but still these people made the point, loudly and clearly, that governments can affect the value of their currency. Thus, these Bitcoin investors had lost faith in all government backed securities, including the U.S. dollar, euro, yen, etc. They believed, fervently, that only a currency based on technology, without any government involvement, could ever maintain its value.

Today if someone is asked to give personal information for a census on their city, county, state or country they will often refuse. They want nothing to do with giving additional information to their government.

But these same people allow Facebook, Google and Amazon to watch their most private communications. Facebook records their emotions, their personal interactions, friends, complaints and a million other things going on in users’ lives to develop profiles of what is interesting to them in order to send along newsfeeds, information and ads. Google has recorded every search everyone has ever done, and analyzes those to develop profiles of each person’s interests, concerns, desires and hundreds of other categories to match each with the right ad. Amazon watches every product search made, and everything purchased to profile each person in order to push them the right products, entertainment, news and ads. And they all sell these profiles, and a lot of other personal information, to a host of other companies who do credit ratings, develop credit card offerings and push their own items for sale.

People who have no faith at all in government, and don’t believe government entities can make their lives better, leave their cookies on because they trust these tech companies to use technology to make their lives better. They believe in technology. Are these folks losing privacy? Maybe, but they see a direct benefit to what the technology operated by these tech companies can do for their lives.

For them, Bitcoin represents a future without government. And that clearly drives passion. Blockchain is a bias free, regulator free technology platform. Bitcoin is a government free form of currency, unable to be manipulated by the Federal Reserve, Exchequer of the currency, European Central Bank, Congress, Presidents, the G7, or anyone else. For the vocal Bitcoin owners, they see in Bitcoin a new future with far less government involvement, based on Blockchain technology. And they trust technology far more than they trust the current systems. They claim to not be anarchists, but rather believers in technology over human government, and in some instances even religion.

Leadership lessons from my Bitcoin journey

Often we try to explain away feedback, especially negative feedback or feedback that is hard to interpret, with easy answers. Such as, “they just want their asset to go up in value.” That is a big mistake. If the feedback is strong, it is really worth digging harder to understand why there is passion. Never forget that every piece of negative feedback is a chance to learn and grow. It is almost always worth taking the time to really understand not only what is being said, but why it is being said. There could be a lot more to the issue than face value.

If things are confusing, it is important to sort out the source of the confusion. If I’m talking about a currency, why do they keep talking about the technology? Saying “they don’t get it” misses the point that maybe “you don’t get it.” It is worth digging into the confusion to try and really understand what motivates someone. Only by listening again and again and again, and trying to really see their point of view, can you come to understand that what you think is confusing, to them is not. They aren’t confused, they see you as confused. Until you resolve this issue, both parties will keep talking right past each other.

You cannot lead if you do not understand what other people value. Their belief system may not match yours, and thus they are reaching very different conclusions when looking at the same “facts.” While I may trust the Fed and the ECB, and even banks, if others don’t then they may well have a very different view of the future.

When leaders lose the faith of those they are supposedly leading, unexpected outcomes will occur. Leaders cannot lead people who don’t trust them. Using the power of their office to force their will on others, and forcing conformance to existing processes, methods and systems can often lead to strong negative reactions. People may have no choice short-term but to do as instructed, but they may well be plotting (investing) longer term in a very different future. Failing to see the passion with which they are seeking that different future will only cause the leadership gap to widen, and shorten the time to a disruptive event.

Adam's book reveals the truth about how to use strategy to outpace the competition.

Follow Adam's coverage in the press and in other media.

Follow Adam's column in Forbes.

by Adam Hartung | Oct 30, 2017 | Food and Drink, Growth Stall, Investing, Leadership, Retail

Understand Growth Stalls So You Can Avoid GM, JCPenney and Chipotle

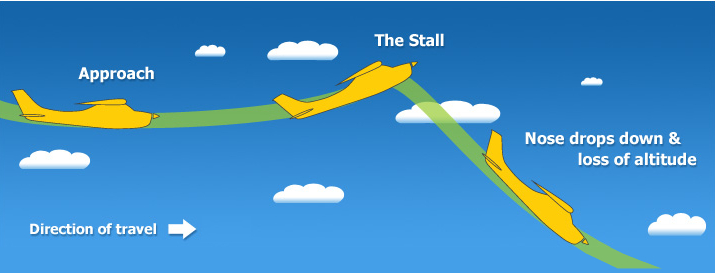

Companies, like aircraft, stall when they don’t have enough “power” to continue to climb.

Everybody wants to be part of a winning company. As investors, winners maximize portfolio returns. As employees winners offer job stability and career growth. As communities winners create real estate value growth and money to maintain infrastructure. So if we can understand how to avoid the losers, we can be better at picking winners.

It has been 20 years since we recognized the predictive power of Growth Stalls. Growth Stalls are very easy to identify. A company enters a Growth Stall when it has 2 consecutive quarters, or 2 successive quarters vs the prior year, of lower revenues or profits. What’s powerful is how this simple measure indicates the inability of a company to ever grow again.

Only 7% of the time will a company that has a Growth Stall ever grow at greater than 2%/year. 93% of these companies will never achieve even this minimal growth rate. 38% will trudge along with -2% to 2% growth, losing relevancy as it develops no growth opportunities. But worse, 55% of companies will go into decline, with sales dropping at 2% or more per year. In fact 20% will see sales drop at 6% or more per year. In other words, 93% of companies that have a Growth Stall simply will not grow, and 55% will go into immediate decline.

Growth Stalls happen because the company is somehow “out of step” with its marketplace. Often this is a problem with the product line becoming less desirable. Or it can be an increase in new competitors. Or a change in technology either within the products or in how they are manufactured. The point is, something has changed making the company less competitive, thus losing sales and/or profits.

Unfortunately, leadership of most companies react to a Growth Stall by doubling down on what they already do. They vow to cut costs in order to regain lost margin, but this rarely works because the market has shifted. They also vow to make better products, but this rarely matters because the market is moving toward a more competitive product. So the company in a Growth Stall keeps doing more of the same, and fortunes worsen.

But, inevitably, this means someone else, some company who is better aligned with market forces, starts doing considerably better.

This week analysts at Goldman Sachs lowered GM to a sell rating. This killed a recent rally, and the stock is headed back to $40/share, or lower, values it has not maintained since recovering from bankruptcy after the Great Recession. GM is an example of a company that had a Growth Stall, was saved by a government bailout, and now just trudges along, doing little for employees, investors or the communities where it has plants in Michigan.

Tesla- enough market power to gain share “uphill”?

By understanding that GM, Ford and Chrysler (now owned by Fiat) all hit Growth Stalls we can start to understand why they have simply been a poor place to invest one’s resources. They have tried to make cars cheaper, and marginally better. But who has seen their fortunes skyrocket? Tesla. While GM keeps trying to make a lot of cars using outdated processes and technologies Tesla has connected with the customer desire for a different auto experience, selling out its capacity of Model S sedans and creating an enormous backlog for Model 3. Understanding GM’s Growth Stall would have encouraged you to put your money, career, or community resources into the newer competitor far earlier, rather than the no growth General Motors.

This week, JCPenney’s stock fell to under $3/share. As JCPenney keeps selling real estate and clearing out inventory to generate cash, analysts now say JCPenney is the next Sears, expecting it to eventually run out of assets and fail. Since 2012 JCP has lost 93% of its market value amidst closing stores, laying off people and leaving more retail real estate empty in its communities.

In 2010 JCPenney entered a Growth Stall. Hoping to turn around the board hired Ron Johnson, leader of Apple’s retail stores, as CEO. But Mr. Johnson cut his teeth at Target, and he set out to cut costs and restructure JCPenney in traditional retail fashion. This met great fanfare at first, but within months the turnaround wasn’t happening, Johnson was ousted and the returning CEO dramatically upped the cost cutting.

The problem was that retail had already started changing dramatically, due to the rapid growth of e-commerce. Looking around one could see Growth Stalls not only at JCPenney, but at Sears and Radio Shack. The smart thing to do was exit those traditional brick-and-mortar retailers and move one’s career, or investment, to the huge leader in on-line sales, Amazon.com. Understanding Growth Stalls would have helped you make a good decision much earlier.

This recent quarter Chipotle Mexican Grill saw analysts downgrade the company, and the stock took another hit, now trading at a value not seen since the end of 2012. Chipotle leadership blamed bad results on higher avocado prices, temporary store closings due to hurricanes, paying out damages due to a “one time event” of hacking, and public relations nightmares from rats falling out of a store ceiling in Texas and a norovirus outbreak in Virginia. But this is the typical “things will all be OK soon” sorts of explanations from a leadership team that failed to recognize Chipotle’s Growth Stall.

Prior to 2015, Chipotle was on a hot streak. It poured all its cash into new store openings, and the share price went from $50 from the 2006 IPO to over $700 by end of 2015; a 14x improvement in 9 years. But when it was discovered that ecoli was in Chipotle’s food the company’s sales dropped like a stone. It turned out that runaway growth had not been supported by effective food safety processes, nor effective store operations processes that would meet the demands of a very large national chain.

Prior to 2015, Chipotle was on a hot streak. It poured all its cash into new store openings, and the share price went from $50 from the 2006 IPO to over $700 by end of 2015; a 14x improvement in 9 years. But when it was discovered that ecoli was in Chipotle’s food the company’s sales dropped like a stone. It turned out that runaway growth had not been supported by effective food safety processes, nor effective store operations processes that would meet the demands of a very large national chain.

But ever since that problem was discovered, management has failed to recognize its Growth Stall required a significant set of changes at Chipotle. They have attacked each problem like it was something needing individualized attention, and could be rectified quickly so they could “get back to normal.” And they hoped to turn around public opinion by launching nationwide a new cheese dip product in 2017, despite less than good social media feedback on the product from early customers. They kept attempting piecemeal solutions when the Growth Stall indicated something much bigger was engulfing the company.

What’s needed at Chipotle is a recognition of the wholesale change required to meet customer demands amidst a shift to more growth in independent restaurants, and changing millennial tastes. From the menu options, to app ordering and immediate delivery, to the importance of social media branding programs and customer testimonials as well as demonstrating commitment to social causes and healthier food Chipotle has fallen out-of-step with its marketplace. The stock has now lost 66% of its value in just 2 years amidst sales declines and growth stagnation.

We don’t like to study losers. But understanding the importance of Growth Stalls can be very helpful for your career and investments. If you identify who is likely to do poorly you can avoid big negatives. And understanding why the market shifted can lead you to finding a job, or investing, where leadership is headed in the right direction.

Adam's book reveals the truth about how to use strategy to outpace the competition.

Follow Adam's coverage in the press and in other media.

Follow Adam's column in Forbes.

by Adam Hartung | Oct 27, 2017 | Food and Drink, Growth Stall, Investing, Leadership, Retail

The Three Steps GE Should Take Now – And The Lessons For Your Business

Monitor displays General Electric Co. (GE) at the New York Stock Exchange (NYSE) October, 2017. Photographer: Michael Nagle/Bloomberg

For years I have been negative on GE’s leadership. CEO Immelt led the dismantling of the once-great GE, making it a smaller company and one worth quite a bit less. The process has been devastating to many employees who lost their jobs, pensioners who have seen their benefits shrivel, communities with GE facilities that have suffered from investment atrophy, suppliers that have been squeezed out or displaced and investors that have seen the value of GE shares plummet.

But now there is a new CEO, a new leadership team and even some new faces on the Board of Directors. Some readers have informed me that it is easier to attack a weak leader than recommend a solution, and they have inquired as to what I think GE should do now. I do not see the GE situation as hopeless. The company still has an enormous revenue base, and vast assets it can use to fund a directional shift. And that’s what GE must do – make a serious shift in how it allocates resources.

Step 1 – Apply the First Rule of Holes

The first rule of holes is “when you find yourself in a hole, stop digging.” (Will Rogers, 1911) This seems simple. But far too many companies have their resourcing process on auto-pilot. Businesses that have not been growing, and often are not producing good returns on investment, continue to receive funding. Possibly because they are a legacy business that nobody wants to stop. Or possibly because leadership remains ever hopeful that tomorrow will somehow look like yesterday and the next round of money, or hiring, will change things to the way they were.

In fact, these businesses are in a hole, and spending more on them is continuing to dig. The investment hole just keeps getting bigger. The smart thing to do is just stop. Quit adding resources to a business that’s not adding value to the market capitalization. Just stop investing.

When Steve Jobs took over Apple he discontinued several Macintosh models, and cut funding for Macintosh development. The Mac was not going to save Apple’s declining fortunes. Apple needed new products for new markets, and the only way to make that happen was to stop putting so much money into the Mac business.

When streaming emerged CEO Reed Hastings of Netflix quit spending money on the traditional DVD/Video distribution business even though Netflix dominated it. He even raised the price. Only by stopping investments in traditional distribution could he turn the company toward streaming.

Step 2 – Identify the Trend that will Guide Your Strategy

All growth strategies build on trends. After receiving funding from Microsoft to avoid bankruptcy in 2000, Apple spent a year deciding its future lied in building on the trend to mobile. Once the trend was identified, all product development, and new product introductions, were targeted at being a leader in the mobile trend.

When the internet emerged GE CEO Jack Welch required all business units to create “DestroyYourBusiness.com” teams. This forced every business to look at the impact the internet would have on their business, including business model changes and emergence of new competitors. By focusing on the internet trend GE kept growing even in businesses not inherently thought of as “internet” businesses.

GE has to decide what trend it will leverage to guide all new growth projects. Given its large positions in manufacturing and health care it would make sense to at least start with IoT opportunities, and new opportunities to restructure America’s health care system. But even if not these trends, GE needs to identify the trend that it can build upon to guide its investments and grow.

Step 3 – Place Your Bets and Monetize

When Facebook CEO Mark Zuckerberg realized the trend in communications was toward pictures and video he took action to keep users on the company platform. First he bought Instagram for $1 billion, even though it had no revenues. Two years later he paid $19 billion for WhatsApp, gaining many new users as well as significant OTT technology. Both seemed very expensive acquisitions, but Facebook rapidly moved to increase their growth

and monetize their markets. Leaders of the acquired companies were given important roles in Facebook to help guide growth in users, revenues and profits.

Netflix leads the streaming war, but it has tough competition. So Netflix has committed spending over $6billion on new original content to keep customers from going to Amazon Prime, Hulu and others. This large expenditure is intended to allow ongoing subscriber growth domestically and internationally, as well as raise subscription prices.

This week CVS announced it is planning to acquire Aetna Health for $66 billion. On the surface it is easy to ask “why?” But quickly analysts offered support for the deal, ranging from fighting off Amazon in prescription sales to restructuring how health care costs are paid and how care is delivered. The fact that analysts see this acquisition as building on industry trends gives support to the deal and expectations for better future returns for CVS.

During the Immelt era, there were attempts to grow, such as in the “water business.” But the investments were not consistent, and there was insufficient effort placed on understanding how to monetize the business short- and long-term. Leadership did not offer a compelling vision for how the trends would turn into revenues and profits. Acquisitions were made, but lacking a strong vision of how to grow revenues, and an outsider’s perspective on how to lead the trend, very quickly short-term financial metrics built into GE’s review process led to bad decisions crippling these opportunities for growth. And today the consensus is that GE will likely sell its healthcare businessrather than make the necessary investments to grow it as CVS is doing.

Successful leadership means moving beyond traditional financial management to invest for growth

In the Welch era, GE made dozens of acquisitions. These were driven by a desire to build on trends. Welch did not fear investing in growth businesses, and he held leaders’ feet to the fire to produce successful results. If they didn’t achieve goals he let the people and/or the business go. Hence his nickname “Neutron Jack.”

For example, although GE had no background in entertainment, GE bought NBC at a time when viewership was growing and ad prices were growing even faster. This led to higher revenues and market cap for GE. On the other hand, when leaders at CALMA did not anticipate the shift in CAD/CAM from dedicated workstations to PCs, Welch saw them overly tied to old technology and unable to recognize the trend, so he immediately sold the business. He invested in businesses that added to valuation, and sold businesses that lacked a clear path to building on trends for higher value.

Being a caretaker, or steward, is no longer sufficient for business leadership. Competitors, and markets, shift too quickly. Leaders must anticipate trends, reduce investments in products, services and projects that are off the trend, and put resources to work where growth can create higher returns.

This is all possible at GE – if the new leadership has a vision for the future and starts allocating resources effectively. For now, all we can do is wait and see……

Adam's book reveals the truth about how to use strategy to outpace the competition.

Follow Adam's coverage in the press and in other media.

Follow Adam's column in Forbes.