Chart courtesy of Felix Richter, Statista.com https://www.statista.com/chart/9454/retail-space-per-1000-people/

Take for example Netflix. Netflix won the war in video distribution, annihilating Blockbuster. But then, when it seemed Netflix owned video distribution, CEO Reed Hastings pivoted from distribution to streaming. He cut investment in distribution assets, and raised prices. Then he spent the money learning how to become a tech company that could lead the world in streaming services. It was a big bet that cannibalized the old business in order to position Netflix for future success.

Analysts hated the idea, and the stock price sank. But CEO Hastings was proven right. By investing heavily in the next wave of technology and market growth Netflix soared toward far greater success than had it kept spending money in lower cost distribution of cassettes and DVDs.

Simply put, CEO Sadoun announced at the largest ad agency awards conference, the Cannes International Festival of Creativity, that Publicis would no longer participate in Cannes. Nor would it participate in several other conferences including the very large South by Southwest (SXSW) and Consumer Electronics Show (CES.) Instead, he would save those costs to invest in AR (artificial or augmented reality.)

In an industry long dominated by highly creative people who love mixing with other agency folks and clients, this was an enormous shock. These conferences were where award winners marketed their creative capability, showing off how much they were admired by peers. And they wined and dined clients seeking to build on awards to gain new business. No one would expect any major agency to drop out, and most especially not an agency as large as Publicis.

In changing markets strategic pivots make sense.

And strategically this pivot makes a lot of sense. The ad industry was once dominated by ads placed in newspaper, magazines and on TV. But today print journalism is almost dead. The demand for print ads is a fraction of 20 years ago. And TV is no longer as prevalent as before. Today, people spend more time looking at their smartphone than they do their TV. The days of thinking high creativity would lead to high sales are in the past. Fewer and fewer big advertisers care about who wins awards, and fewer are going to these conferences to decide who they would like to hire.

Today advertising is going “programmatic.” Increasingly ads are placed by computers, on web and mobile sites. Advertising is about finding the right eyeballs, at the right time, next to the right content in order to find a buyer. Advertisers no longer spend money lavishly on mass media hoping for good results. Instead ads are targeted, measured for response and evaluated for ROI based on media, location, user and a raft of other metrics.

And the industry has changed. There still is an advertising agency business. But it is under attack from tech companies like Google, Facebook, Twitter and Snap that promote to advertisers their ability to target the right clients for high returns on money spent. The content is important, but today almost everyone in the industry will tell you success depends on your budget and how you spend it, not the creative. And that is a lot more about understanding how we’re all interconnected, knowing how to measure device usage, profiling user behavior and programming the computers to put those ads in the right place, at the right time.

To pivot you must stop doing the old to start doing the new

Publicis has something like $10B in revenue. Thus, dropping $20M on filing award applications at events like Cannes, and sending a contingent of employees to receive awards, meet people and have fun doesn’t sound like a lot. But multiple that across the year and the total amount could well come to $100M-$200M. That’s still only 2% of revenues – at most. It would seem like not that much money given what has been a core part of historical marketing.

But, if Publicis is to compete in the future with the tech leaders, and emerging digital-oriented agencies, it has to develop technology that will make it a leader. Publicis can’t invent money out of thin air, so it has to stop doing something to create the funds for investing in what’s coming next. And stopping investing in something as “old school” as Cannes actually sounds really smart. As boomer ad execs retire the newer generation is not going to conventions to find agencies, they are looking under the hood at the technology engines these companies provide.

In new strategic areas a little money can go a long way

And while $100M to $200M may not sound like a lot, it is enough money to make a difference in creating a tech team that can work on future-oriented technology like AI. If spent wisely, that could truly move the needle. If Publicis could demonstrate an ability to use proprietary AI technology to better place ads and manage the budget for higher returns it can survive, and perhaps thrive, in a digitally dominated ad industry future. At the very least it can find its place next to Facebook and Google.

WPP, Omnicom and Interpublic should take serious notice. Will they succeed in 2025 if they keep marketing the way they did in 1985? Will this spending grow revenues if customers really don’t care about creative awards? Will they remain relevant if they lack their own technology to develop ads, campaigns and demonstrate positive rates of return on ad dollars spent?

It’s a lot smarter to try what you don’t know than hope everything will stay the same.

Whole Food flagship store in Austin, Texas.

Amazon announced it was paying $13.7B to buy Whole Foods. While not without risks, there are a lot of reasons this is a great idea:

Building any retail chain takes a long time. Due to the intensity of competition, and low margins, building a grocery chain takes even longer. Amazon would have spent decades trying to create its own chain. Now it won’t lose all that time, and it won’t give competitors more time to figure out their strategies.

Few people realize that no grocer makes money selling groceries. Revenues do not cover the costs of inventory, buildings and labor. On its own, selling groceries loses money. Grocers survive on manufacturer “deal dollars.”

Companies like P&G, Nabisco, etc. pay grocers slotting fees to obtain shelf space, they pay premiums for eye level shelves and end caps, they pay new product fees to have grocers stock new items, they pay inventory fees to have grocers keep inventory on shelf and in back, they pay advertising fees to have signs in the stores and products in circulars, and they pay volume rebates for meeting, and exceeding, volume goals. It is these manufacturer “deal dollars” that cover the losses on the store operations and create a profit for investors.

One reason Whole Foods prices are so high is they stock less of the mass market goods and thus receive fewer deal dollars. Now Amazon can use Whole Foods to increase its volume in all products and dramatically increase its deal dollar inflow. Something that Amazon sorely missed as a “delivery only” grocer.

Grocery distribution is unique. For decades grocers have worked with manufacturers, cooperatives, growers and other suppliers to create the shortest, most efficient distribution of food with the lowest inventory. In many instances replenishment quantities are shipped based on manufacturer access to real grocer sales data. Amazon is the best at what it does, but to compete in groceries it needed a grocery distribution system – and with Whole Foods it obtains one at scale without having to create it.

Additionally Amazon will obtain the corporate infrastructure of a grocer, without having to build one on its own. All those buyers, merchandisers, real estate professionals, local ad buyers, etc. are there and ready to execute – something building would be very hard to do.

Whole Foods has 460 stores, and almost all are in great locations. Whole Foods focused on upscale, growing and often urban or suburban locations – all great for Amazon to grow its distribution footprint. And hard sites to find.

These can be used to sell other products, such as other grocery items, or some selection of Amazon products if that makes sense. Or these can be used to augment Amazon’s distribution system for local delivery – or as neighborhood drop-off locations for people who don’t want at-home delivery to pick up Amazon-purchased products. Or they can be sold/leased at very attractive prices.

“Whole Paycheck” has long been the knock on Whole Foods. As mentioned before, the lack of mass market items meant their products lacked deal dollars and thus had to be priced higher. And their stores are large, and not the best use of space. The result has been a lot of trouble keeping customers, and one of the lowest sales per square foot in the grocery industry.

Amazon can easily use its low-price position to alter the Whole Foods brand concept to include things like Pepsi, Coke, Bounty, Gain – a slew of branded consumer goods previously eschewed by Whole Foods. Adding these products could make the stores more useful to more customers, and greatly lower the average cost of a cart full of goods. On its own, this brand transition has been impossible for Whole Foods. As part of Amazon remaking the brand will be vastly easier.

If you shopped Amazon you know they really figure out your needs, and help you find what you want. Amazon keeps track of your searches and purchases, and makes recommendations that often help the shopping experience and delight us as customers.

But today all that information on grocery shopping is un-mined. Despite using a loyalty card, traditional grocers (and WalMart) have been unable to actually mine that information for better marketing. Now Whole Foods will be able to use Amazon’s incredible technology skills, including big data mining and artificial (or augmented) intelligence to actually help us make the grocery shopping experience better – less time intensive, and most likely less costly while still allowing us to fill our carts with what we need and what makes us happy.

$13.7B is only 65% of the cash Amazon had on hand end of last quarter. And Amazon has only $7.7B in long-term debt. With a $460B market cap Amazon could easily take on more debt without adding significant financial risk.

But even more important, Amazon has the amazingly cheap currency that is Amazon stock. Even at the offering price, Whole Foods trades at 34x earnings. Amazon trades at 185x earnings. Thus by swapping Amazon shares for Whole Foods shares Amazon lowers the price 80%! Amazon isn’t spending real dollars, it is using its stock – which is an incredibly valuable move for its shareholders.

For the last several years WalMart’s general merchandise sales have been declining due to the Amazon Effect and growing on-line competitor sales. For the last 3 years overall revenues have not grown at all. To maintain revenue Walmart has shifted increasingly to groceries – which account for well over half of all WalMart revenues. By purchasing Whole Foods, Amazon takes direct aim at the only part of WalMart’s “core” business that it has not attacked.

Walmart’s net profit before taxes is ~4%. If Amazon can use Whole Foods to combine stores and on-line sales to take just 3% of WalMart’s grocery business away it could remove from Walmart ($485B revenues * 60% grocery * 3% market share loss) a net revenue decline of ~$9B. Given that the cost of grocery goods sold is about 50% – that would mean a net loss in contribution of $4.5B – which would cut almost 25% out of Amazon’s $20B pre-tax income. Raise the share taken to 5% and Amazon could cut WalMart’s pre-tax income by $7.25B, or ~35%.

The negative impact of declining store sales on the fixed costs of WalMart is atrocious. Even small revenue drops mean cutting staff, cutting inventory, cutting store size and eventually closing stores. Look at how fast Sears and Kmart fell apart when sales started declining. Like dominoes falling, declining sales sets off a series of bad events that dooms almost all retailers – as the quickened pace of retail bankruptcy filings has proven.

The above analysis, taking 3-5% out of Walmart’s grocery sales, say over 3 years, would be a huge gain attributed to the creation of a new Whole Foods combined with Amazon’s e-commerce. Growing grocery revenues by $9-$14B would mean practically a doubling of Whole Foods. Which sounds enormous – and most likely impossible for Whole Foods to do on its own, even if it did launch some kind of e-commerce initiative.

But this is not so unlikely given Amazon’s track record. Amazon has been growing at over 25%/year, adding between $20-$25B of new revenues annually. In 3 years between 2013 and 2016 Amazon doubled its revenues. So it is not that unlikely to expect Amazon puts forward an extremely ambitious push to turn around Whole Foods, increase store sales and use the combined entities to grow delivery sales of groceries and other general merchandise.

Is there risk in this acquisition? Of course. Combining any two companies is fraught with peril – combining IT systems, distribution systems, customer systems and cultures leaves enormous opportunities for missteps and disaster. But the upsides are enormous. Overall, this is a bet Amazon investors should be glad leadership is making – and it is a great benefit for Whole Foods investors.

GE Chairman and CEO Jeff Immelt walks off stage after being interviewed during the Washington Ideas Forum at the Harmon Center for the Arts September 28, 2016 in Washington, DC. A proud Republican, Immelt said it would hurt the United States and cripple President Barack Obama — and the next president of the U.S. — not to agree to trade deals like theTrans Pacific Partnership (Photo by Chip Somodevilla/Getty Images)

Readers of this column know I’m not a fan of General Electric’s CEO, Jeffrey Immelt. In May, 2012 I listed CEO Immelt as the 4th worst CEO of a large publicly traded American company. Unfortunately, his continued tenure since then did nothing to help make GE a stronger, or more valuable company. GE’s lead director says this is the culmination of a transition plan first developed in 2011. One can only wonder why it took the board so incredibly long to replace the feckless CEO, and why they allowed GE’s leadership to continue destroying shareholder value.

The longer back you look, the worse Immelt’s performance appears.

Few company analysts can say they’ve followed a company for 3 years. Fewer yet can say 5 years. Nearly none can say a decade. Yet, CEO Immelt was in his job for 16 years – much longer than almost all business analysts or writers have followed GE. Therefore, their lack of long-term memory often leaves them unable to give a proper overview of the company’s fortunes under the long-lived CEO.

I have followed GE closely for almost 35 years. Ever since I graduated from HBS class of 1982 along with Mr. Immelt. Several fellow alumni worked at GE, and a large number of my BCG (Boston Consulting Group) colleagues joined GE in senior positions during the mid-1980s as GE grew exponentially. I have followed several of these alumni as the years passed allowing me to take the “long view” on GE’s performance, during Welch’s leadership and more recently since Mr. Immelt took the top job.

I was very pleased to include a positive case study of GE’s business practices in my book “Create Marketplace Distruption – How to Stay Ahead of the Competition” (Financial Times Press, 2007.) CEO Welch used a number of internal processes to help GE leaders identify disruptive opportunities to change industries – whether markets where GE already competed or new markets. He relentlessly encouraged entering new businesses where GE could bring something new to the game, and he put GE’s money to good use growing revenues, and market cap, enormously. No other CEO in American history made as much value for shareholders as Jack Welch. His leadership pushed GE to the top position in most industries, and his relentless focus on growth helped even rank-and-file employees build million dollar IRAs to go with well funded pension and retiree benefit plans.

GE’s performance could not have changed more dramatically than it has under Mr. Immelt. But there are now a number of apologists who would say GE’s smaller size, and lower valuation, are due to market conditions which were out of Mr. Immelt’s control. They contend CEO Immelt was a good steward of the company during difficult market conditions, and the results of his tenure – notably lower revenues, lower valuation, fewer markets, fewer employees and lower community involvement – are not his fault. They argue he did a good job, all things considered.

Balderdash. Immelt was a terrible CEO

There is an overall reluctance to say bad things about any huge American icon, and its CEO. After all, columnists and analysts who are non-congratulatory don’t usually get called by the company to be consultants, or advisors. Or to be on the board. And publishers of columnists who say negative things about big companies and their execs risk having ad dollars moved to more favorable journals, and often unfriendly relationships with their ad departments and agencies. So it is far easier, and more acceptable, to sugar coat bad strategy, bad leadership and bad results.

But we should move beyond that bias. Mr. Immelt was the CEO of the ONLY company on the Dow Jones Industrial Average (DJIA) to have been on that list since it was created. He inherited the most successful company at creating shareholder value during the 1980s and 1990s. He surely should be held to the highest of comparative bars.

Those who say CEO Immelt was “set up to fail” are somehow making the case that Immelt would have been more successful if he had inherited a company with a bad brand image, weak history, and inadequate performance. They are rewriting history to say Jack Welch was not a good CEO, and his outsized gains destined GE to do poorly under his successor. That simply defies the facts – and logic.

Looking at the last 16 years of “difficult times,” when GE has struggled under Immelt’s leadership, one should ask “why did so many other companies do so well?” After all, the DJIA has more than doubled. The S&P 500 has almost doubled. The Russell 2000 has almost tripled. Overall, far more companies have gone up in value than down. Why were Immelt’s circumstances so difficult that all of those CEOs did so much better? They dealt with the same financial meltdown, same Great Recession, same increase in regulations, same federal reserve, same government administration – yet they were able to adapt their companies, grow and increase value.

Yes, GE was huge in financial services when Immelt took the reigns, and financial services saw a major crash. But look at the performance of JPMorganChase under CEO Jamie Dimon (also a classmate of Mr. Immelt.) JPM is stronger today than ever, growing and gaining market share and increasing its value to shareholders. Prior to the crash, in spring 2007, GE was trading at $41/share, and now it is $29 – a decline of ~30%. Back then JPM was trading at $53, and now it is $93 – a gain of ~75%. There obviously was a strategy to adapt to market conditions and do well. Just not at GE.

Immelt reacted to market events, poorly, rather than having a prepared, proactive strategy

Let’s not rewrite history. Prior to the banking crash CEO Immelt was more than happy for GE to be in the “easy money” world of finance. Welch had created GE Capital, and Immelt had furthered its growth when lending was easy and profitable. And he supported the enormous growth in GE’s real estate division. When this industry faced the crash, GE faced a near-bankruptcy not because of Welch, but because of Immelt’s leadership during the over 6 years he had been CEO. If there were risks in the system CEO Immelt had ample time to re-arrange the portfolio, reduce lending, offload financial assets and reduce exposure to real estate and mortgages. But Immelt did not do those things. He did not prepare for a reversal in the markets, and he did not prepare the balance sheet for a significant change of events. It was his leadership that left GE exposed.

As GE shares fell to $7 Immelt made a famous deal with Berkshire Hathaway’s CEO Warren Buffet to increase GE’s capital base in order to stave off demise. And this deal saved GE. But this was an extremely sweet deal for Buffett, giving Berkshire very good interest (10%) on the preferred shares and warrants allowing Buffett to buy future shares of GE at a fixed price. Berkshire made a profit, over and above the interest, of $260M on the deal, and overall at least $1.2B. By being prepared Buffett saved GE and made a lot of money. GE’s investors paid the price for a CEO that was unprepared.

But the changes brought about by the crash, and Dodd-Frank, were more than CEO Immelt could manage. Thus GE exited the business selling many assets at fire sale prices. This “turn tale and run” strategy was sold to the public as a way for GE to “focus” on its “core manufacturing business.” Rather, it was a failure of leadership to understand how to manage this business to future success in changed markets. Where Welch’s GE had grasped for disruption as opportunity, Immelt’s GE gasped at disruption and fled, destroying billions in GE value.

Immelt could not grow GE’s businesses, so he divested GE of many.

GE was to be the “industrial internet giant.” GE was to be a leader in the internet-of-things (IoT) where sensors, the cloud and remote devices created greater productivity. And, to be sure, companies like Apple, Google and Samsung have made huge gains in this market. Even small companies, like Nest, were able to jump on this technology shift with new products for the residential market. But name one market where GE is the dominant IoT player. During 16 years the internet and remote services markets have exploded, yet GE is not the market leader. Rather it is barely recognized.

Rather than growing GE with disruptive innovations and visionary products in emerging technology markets, Immelt’s GE was primarily shrinking via divestitures. In dismantling GE Capital he eliminated the lending and real estate operations. After decades as a leader in appliances, that division was sold. Welch built the extremely successful entertainment division around NBC/Universal, which Immelt sold.

The water business that was to be a world leader under Immelt’s vision, likewise sold – and largely to make sure GE could close the deal on selling its oil & gas unit. Even the famed electrical distribution business, going back to the start of GE, is now close to being sold.

And what happened to all this money? Well, about $50B went into share buybacks – which ostensibly would help shareholders. Only it didn’t, because GE is still worth less than when buybacks started. So the money just disappeared. At least Immelt could have paid it to shareholders as a dividend – but then that would not have boosted his bonuses.

GE’s website says Mr. Immelt wanted to create a “simpler, more valuable industrial company.” Mr. Immelt is definitely leaving behind a simpler, much smaller and weaker company. The brand is gone from consumer products, and severely tarnished in commercial products. GE lacks a great product pipeline, and even a strong development pipeline due to the rampant divestitures. When Mr. Flannery takes over as CEO he will not inherit a powerhouse company. He will inherit a company that is shrinking and rudderless, and disconnected from most growth markets with almost no product, technology or brand advantages. And he will report to the Chairman that created this mess, Mr. Immelt.

The most likely outcome is that Mr. Peltz and his firm, Trian Partners, will buy more GE shares and seek directorships on the board. Then, in a move not unlike the deaths of DuPont and Dow, there will be a massive cost cutting effort to bring expenses in-line with the shrunken GE business. R&D will be discontinued, as will product development. Support groups will be shredded. Customer service will be downsized. Then the remaining pieces will be sold off to buyers, or taken public, leaving GE a dismantled piece of history.

While that may work for the capital markets, and some short-term investors will share in the higher valuation, what about the people? People who dedicated their careers to GE, and are pensioners or current employees? What about cities and counties where GE has been a major employer, and civic contributor? What about customers that bought GE industrial products, only to see those products dropped due to low profitability, or little growth opportunity? What about suppliers that invested in developing new technologies or products for GE to take to market? What will happen to the people who once relied on GE as America’s largest diversified industrial company?

These people all have an ax to grind with the very wealthy, and now departing, CEO Immelt. He inherited what may well have been the most successful company on earth. He leaves behind a far weaker company that may not survive.

On the day after Memorial Day Amazon stock hit $1,000/share — a new record high. Amazon is up about 40% the last year. It’s market capitalization doubles Wal-mart. And the vast majority of investment analysts expect Amazon to rise further.

Amazon competes in dozens of international markets, as do many on-line retailers, yet the ‘Amazon Effect’ is far greater in the USA than anywhere else. And there’s a good reason — America is vastly over-served when it comes to traditional retail.

Chart courtesy of Felix Richter, Statista.com https://www.statista.com/chart/9454/retail-space-per-1000-people/

America is enormously over-built with retail space

Looking at square feet of retail space per 1,000 people, this infographic shows that, adjusted for population size, the USA has 8x the retail of Spain, 9x the retail of Italy, 11x the retail of Germany, 22x the retail of Mexico, 51x the retail of China and 400x the retail of India! Overall, this is remarkable. I’ve been to all of these countries, and in none did I feel that I was unable to buy things I needed. Clearly, the USA has had such a robust retail sector that it has dramatically over-expanded – with individual stores, suburban strip malls, elaborate horizontal malls, vertical urban malls and multi-floor urban retail complexes far outpacing the needs of American shoppers.

All these stores created a very competitive retail environment. This competition, and the lack of any sort of national value added tax (VAT,) kept prices for most things in America among the lowest in the world. Simultaneously according to the Department of Labor, Retail is the third largest employer in America. Couple that with the enormous wholesale distribution networks of warehouses and truck fleets — and selling things becomes the country’s largest employer — even bigger than the sum total of all federal, state and local government employees .

Additionally, retail has produced the largest local taxes of any industry, combining local sales taxes with property taxes, which has funded schools and public works projects for decades. And this retail space has helped drive demand for all kinds of support services from utilities to maintenance.

U.S. retail consumers are tremendously over-served, and the market is set to collapse

But now retail is wildly overbuilt. Organic demand for all retail grows about equal to population growth, so about 3%/year. But retail real estate grew far faster since World War II as developers kept building more malls, and large retailers like Sears, KMart, Walmart, Target, Lowe’s and Home Depot built more stores. Now demand for products through traditional retail is declining. People are simply ordering on-line.

Net/net, America’s consumers are now over-served by retailers. There is too much space, and inventory. And now that store-to-home distribution has faded as a problem, with multiple carriers offering overnight service, people are increasingly happy to avoid stores altogether, greatly exacerbating the overcapacity problem. Thus, the ‘Amazon Effect’ has emerged, where stores are closing at a rapid rate and many retailers are failing altogether leaving vast amounts of empty retail space.

Foreign markets are under-served, and benefit from Amazon’s entry

Contrarily, in other countries consumers were to some extent under-served. They actually dealt with local stock-outs on desirable items. And frequently lived in a world with a lot less product choice. And, generally, international consumers expected to travel farther to shop at the few larger stores, malls and urban shopping centers with greater selections.

In those countries local economies became far less dependent on retail real estate for jobs — and for taxes. Most have little or no property taxes as deployed in the USA. Additionally, rather than adding a local sales tax to the price of goods, most countries use some sort of national VAT to collect the tax during distribution. When Amazon starts distributing in these markets it is seen as a good thing! Consumers have more choice, less hassle and often better service. Also, Amazon collects the VAT so no taxes are lost.

Contrarily, American communities could never stop adding retail space. Whenever Walmart or Best Buy wanted a new store, no community leaders turned down the potential local economic gains. But it led to too much space being built for a healthy sector, and certainly far too much given the market shift to on-line retail. Now retail is a classic over-served market, sort of like the need for stagecoaches and livery barns after the railroads were built.

Expect 50-67% of retail space to go vacant within a decade

How much retail space could go vacant in the USA? Just invert the multiples from above. For the USA to have the same retail space as Spain implies an 87.5% reduction, Italy -89%, Germany -91%, Mexico -95.5%. Thus it is not hard to imagine a full 50-67% of America’s retail space to be empty in just 5 or 10 years. Americans would still have 2-3 times the retail space of other developed markets.

There is no doubt Amazon is a good employer, and on-line sales growth will employ hundreds of thousands at Amazon, and millions across the marketplace. Further, most of those jobs will pay a lot better than traditional retail jobs. But there is no sugar-coating the huge impact the ‘Amazon Effect’ will have on local economies and jobs. America is vastly overbuilt and over-supplied by retailers. There will be a huge shake-out, with dozens of retail failures. And there will be enormous amounts of vacant property sitting around, looking for some kind of alternative use. And local communities will find it difficult to meet constituent needs as sales tax and property tax receipts fall dramatically.

As I wrote in my column on February 28, this is going to be an enormous shift. Far bigger than the offshoring of manufacturing. The ‘Amazon Effect’ is automating retailing in ways never imagined by those who built all that retail space. As people keep buying on-line there will be a collapse of retail space pricing, and a collapse of industry participants. Industry players always greatly under-estimate these shifts, so they aren’t projecting retail armaggedon. But in short order the need for retail will be like the need for dedicated, raised-floor computer centers to house mainframes, and later network hubs. It’s just going to go away.

The words “search” and “Google” are practically synonymous. We’ve even turned the name of the ubiquitous web application into a verb by telling people to “Google it.” And that’s good, because Alphabet’s revenue (that’s Google’s parent company) soared more than 25% in the last quarter, and over 90% of Alphabet’s revenue comes from Google AdWords. The more people search using Google, the more money Alphabet makes.

Chart courtesy of Martin Armstrong at Statista.com

But ever since Facebook came along, a new trend has started emerging. People often want answers to their questions within the context of their community. So “searches” are changing. People are going back to what they did before Google existed – they are asking for information from their friends. But online. And primarily using Facebook.

There is no doubt Google dominates keyword searching. But that type of searching has its shortcomings. How often have you found yourself doing multiple searches — adding words, adding phrases, dropping words, etc. trying to find what you were seeking? It’s a common problem, and we all know people who are better “Googlers” than others because of their skill at putting together key words to actually find what we want. And how often do we find ourselves lost in the initial batch of ads, but not finding the link we want? Or going through several pages of links in search of what we seek?

Context often matters. Take the classic problem of finding a place to eat. Googling an answer requires we enter the location, type of food, price point, and other info — which often doesn’t lead us to the desired information, but instead puts us into some kind of web site, or article, with restaurant review. What seems an easy question can be hard to answer when relying on key words.

But, we know how incredibly easy it is for a friend to answer this question. So when seeking a place to eat we use Facebook to ask our friends “hey, any ideas on where I should eat dinner?” Because they know us, and where we are, they fire back specific answers like “the Mexican place two blocks north is just for you,” or “spend the money to eat at that place across the street – pricey but worth it.” Your friends are loaded with context about you, your habits, your favorites and they can give great answers much faster than Google.

Think of these kind of referrals – for food, entertainment, directions, quick facts, local info — as “context based searches” rather than referrals. Instead of making a query with a string of key words, we use context to derive the answer — and our friends. Most people undertake far more of these kind of “searches” than keywords every day.

Even though Google is still growing incredibly fast, context searching — or referrals — pose a threat. People will use their network to answer questions. The web birthed on-line data, and we all quickly wanted engines to help us find that data. We were excited to use Excite, Lycos, InfoSeek, AltaVista and Ask Jeeves to name just a few of the early search engines. We gravitated toward Google because it was simply better. But with the growth of Facebook today we can ask our friends a question faster, and easier, than Google — and often we obtain better results.

Both Google and Facebook rely on ads for most of their revenue. But if consumer goods companies, event promoters, apparel manufacturers and other “core advertisers” realize that people are using Facebook to ask for information, rather than searching Google, where do you think they will spend their on-line ad dollars? Isn’t it better to have an ad for diapers on the screen when someone asks “what diapers do you like best?” than relying on someone to search for diaper reviews?

This is why Google+ with its Groups and Google Hangouts was such a big deal. Google+ allows users to come together in discussions much like Facebook. But Plus, Groups and Hangouts never really caught on, and Plus isn’t nearly as popular as Facebook discussions, or Instagram picture sharing or WhatsApp messaging. Today, when it comes to referral traffic Facebook has eclipsed Google. Five years ago most people would have guessed this would never happen.

I’m not saying that Google searches will decline, nor am I saying Google will stop growing, nor am I saying that Google’s other revenue generators, like YouTube, won’t grow. I am saying that Facebook as a platform is growing incredibly fast, and becoming an ever more powerful tool for users and advertisers. Possibly a lot more powerful than Google as people use it for more and more information gathering — and referrals. The more people make referrals on Facebook, the more it will attract advertisers, and potentially take searches away from Google.

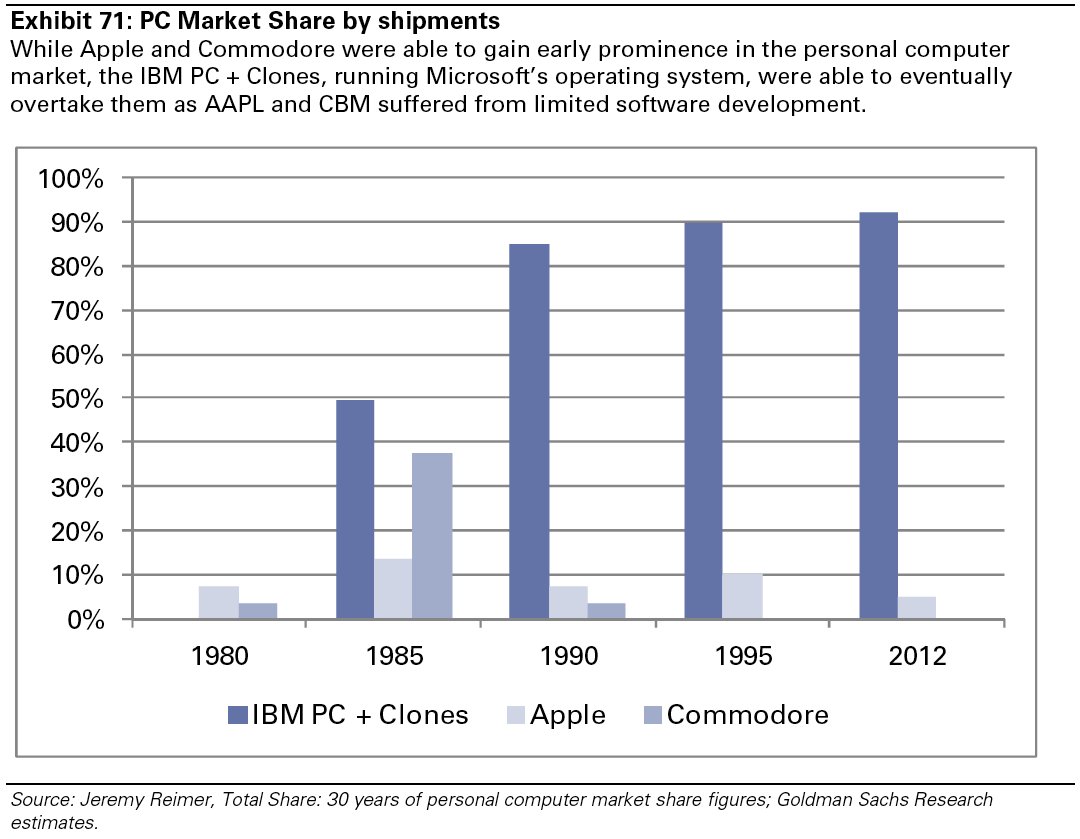

By comparison, this moment may be like the late 1980s when PC sales finally edged ahead of Apple Mac sales. At the time it didn’t look deadly for Apple. But it didn’t take long for the Wintel platform to dominate the market, and the Mac began its slide toward being a submarket favorite.

(Photo: CEO of Amazon.com, Inc. Jeff Bezos, TOMMASO BODDI/AFP/Getty Images)

Amazon.com is now worth about the same as Berkshire Hathaway. Amazon has had an amazing run-up in value. The stock is up 17% year to date, and 46% over the last 12 months. By comparison, Berkshire has risen 3.1% this year and Microsoft has risen 5.6% —while the S&P 500 is up 5.8%. Due to this greater value increase, Jeff Bezos has become the second richest man in the world, jumping past Warren Buffett while Bill Gates remains No. 1.

Obviously, it wouldn’t take much of a slip in Amazon, or a jump in Berkshire, to reverse the positions of the companies and their CEOs. But it is important to recognize what is happening when a barely profitable company that sells general merchandise, technology products (Kindles, Fires and Echos) and technology services (AWS) eclipses one of the most revered financial minds and successful investment managers of all time.

Warren Buffett (Photo by Paul Morigi/Getty Images for Fortune/Time Inc)

When Buffett started his magical machine he realized that capital was often in short supply. Companies had to ration capital, unable to build the means of production they desired. Banks were unwilling to lend when they perceived any risk, even when the risk was not that great. Simultaneously investment banks were highly inefficient. The industry was unwilling to support companies prior to going public, often uninterested in taking companies public, and poor at allocating additional capital to the highest return opportunities. By the time you were big enough to use an investment bank you really didn’t need them to raise capital – they just organized the transactions.

Berkshire Hathaway was a big winner at mastering finance during the industrial era. By putting money in the right place, at the right time, tremendous gains could be made. Berkshire didn’t have to be a manufacturer, it could make a higher rate of return by understanding how to deploy capital to industrial companies in a marketplace where capital was rationed. In other words, give people money when they need it and Berkshire could generate outsized returns.

It was a great strategy for supporting companies in the Industrial Age. And a great way to make money when capital was hard to come by.

But the world has changed. Two important things happened First, capital became a lot easier to acquire. Deregulation and a vast expansion of financial services led to a greater willingness to lend by banks, larger secondary markets for bank-originated products that carried risk, the creation of venture capital and private equity firms willing to invest in riskier opportunities, and a dramatic growth in investment banking globally making it far easier to go public and raise equity. Capital became vastly more available, and the cost of capital dropped dramatically.

This made finding opportunities for outsized returns just based on investing considerably more difficult. And thus every year it has become harder for Berkshire Hathaway to find investment opportunities that exceed market rates of return. Berkshire isn’t doing poorly, but it now competes in a world of many competitors who have driven down returns for everyone. Thus, Berkshire’s returns increasingly move toward the market norm.

The Industrial Era is dead — usher in the Information Era. Second, we are no longer in the Industrial Age. Sometime in the 1990s (economic historians will pin it to a specific date eventually) the world transitioned into the Information Age. In the Information Age assets are no longer worth as much as they previously were. Instead, information has become much more valuable. What a business knows about customers, markets and supply chains is worth more than the buildings, machines and trucks that actually make up the physical economy. The value from having information has become much higher than the value of things — or of providing capital to purchase things.

In the Information Era, few companies have mastered the art of information management better than Amazon.com. Amazon doesn’t succeed because it has great retail stores, or great product inventory or even great computers. Amazon’s success is based on knowing things about markets and its customers. Amazon has piles and piles of data, and Amazon monetizes that information into sales.

By studying customer habits, every time they buy something, Amazon has been able to make the company more valuable to customers. Often Amazon is able to tell a customer what they need before they realize they need it. And Amazon is able to predict the flow of new product introductions, and predict sales for manufacturers with great accuracy. Amazon is able to understand what media customers want, and when they’ll want it. Amazon is able to predict a business’ “cloud needs” before that business knows – and predict the customer’s likely future services needs long before the customer knows.

In the Information Age, Amazon is one of the very, very best information companies out there. It knows how to obtain information, analyze those mounds of “big data” to determine and predict needs, then connect customers with things they want to buy. Being great at information means that Amazon, even with its relatively poor current profits, is positioned to capitalize on its intellectual property for years to come. Not without competition. But with a tremendous competitive lead.

So, how is your portfolio allocated? Are you invested in assets, or information? Accumulating assets is a very hard way to make high rates of return. But creating sales, and profits, out of information is far easier today. The relative change in the value of Amazon and Berkshire is telling investors that it is now smarter to be long information rich companies than asset rich companies.

If you’re long GE, GM, 3M and Walmart how well will you do in an economy where information is more valuable than assets? If you don’t own data rich, analytically intensive companies like Amazon, Facebook, Alphabet/Google and Netflix how would you expect to make above-average rates of return?

And where is your business investing? Are you still putting most of your attention on how you allocate capital, in a world where capital is abundant and cheap? Are you focusing your attention on getting the most out of what you know about markets, customers and suppliers, or just making and selling more stuff? Do you invest in projects to give you insights competitors don’t have, or in making more of the products you have — or launching product version X?

And are you being smart about how you manage your most important information tool — your talented employees? Information is worthless without insight. It is critical companies today do all they can to help employees develop insights, and then rapidly deploy those insights to grow sales. If you spend a few hours pouring over expenses to find dimes, consider letting that activity go in order to spend hours brainstorming how to find new markets and new product opportunities that can generate a lot more revenue dollars.

Harvard Business Review Press just published an insightful new book by two senior partners at Bain & Company, one of the world’s three leading strategy consulting firms, entitled Time Talent Energy. The book’s great insight is that companies utilize a plethora of tools to manage money and financials to the nth degree, but that approach is less successful than putting a greater focus on managing employee time, talent and energy.

Harvard Business Review Press

Harvard Business Review PressTime Talent Energy jacket cover

While managing financials is required in the modern organization, it is insufficient for success. Mankins and Garton discovered that organizations which focus more heavily on managing how employees spend their time and how they thoughtfully place people in their roles, create companies where employees are inspired and 40% more productive than their competition. And this pays off, with profit margins which are 30-50% higher than their industry average. The improvement is so great from focusing on employees that in today’s low cost and easily accessible capital world it is better to waste some cash in the process of better managing time and talent.

In most companies 25% of all productive time is wasted and can reach as high as 40% in complex organizations. Think of all the emails, texts, voice mails and meetings that absorb vast amounts of time. Yet, as the authors are fond of pointing out, nobody can create a 25 hour day. So if you can recapture that time, productivity will soar. The results are far greater than squeezing another 1% (or even 10%) out of your cost structure. If instead of spending so much time managing costs we spent more time eliminating complexity and unneeded tasks, competitiveness will soar.

But in most organizations the focus still remains on finance. The CFO is frequently the second most powerful individual, behind only the CEO. The head of Human Resources (Chief Human Resources Officer — CHRO) rarely has the clout of a CFO. And the CFO job is seen as the route to CEO — far more CFOs than CHROs become CEOs. Simultaneously, organizations spend exorbitantly on financial control tools, such as ERP (Enterprise Resource Planning) from companies like Oracle and SAP — while very few have any kind of tool set for effectively managing employee time or talent deployment. The authors conclude it is apparent business leaders have significantly overshot on managing financial resources, while allowing their organization to be woefully incapable of managing its human resources.

Adam Hartung: Do businesses need to lessen the CFO role, and heighten the CHRO role?

Michael Mankins: The reality is that most human resource decisions, those that determine how people spend their time, and how talent is deployed, are made by line managers. Made within the bowels of the organization, with little more than senior leadership guidelines. There needs to be significantly more involvement by senior leadership in collecting and reviewing data on critical skills for the organization, “A” player performance and leadership development. If as much time was spent by senior leadership teams discussing human resources as spent on budgets there would be a tremendous improvement in productivity.

The CFO and CHRO should definitely be peers. To do that requires a cultural change from being an organization focused on preserving the status quo, reducing mistakes and keeping leadership out of jail to one that is far more future oriented. This can be done and in the book we highlight companies such as ABInBev, Ford, Nordstrom, Starbucks, IKEA, Netflix and others who have accomplished this.

Hartung: Companies spent enormous sums installing ERP systems and they spend a lot to maintain them. Yet, from reading your book it seems like this may have been misguided.

Mankins: All companies need to be able to change their business model as markets shift. ERP frequently creates a wiring that makes it hard to change with the competitive landscape, or as changes in capability are required. ERP locks in the business model at a point in time — but great performers develop ways to adapt.

All companies need a great general ledger. ERP goes far beyond the general ledger and in doing so can make a company too inflexible for today’s rate of change. There needs to be a flexible ERP system —which just doesn’t seem to exist right now. The ERP market seems ripe for a marketplace disrupter!

Simultaneously there aren’t any great tools out there for collecting data that can help a company reduce complexity and eliminate time wasters. Nor are there great tools for managing the performance of “A” players. The top performing companies do create a discipline around these tasks, collecting and analyzing data. Many companies would be helped by a tool that would do for time and talent management what we’ve done for financial management.

Hartung: You demonstrate that clustering “A” players creates dramatic improvement in productivity and company performance. Do great companies focus these clusters on improving the company as it is, or looking for the next “big thing?”

Mankins: We discovered that by and large the greatest gains come from focusing on the latter. Almost all MBA programs are maniacal about training managers to improve the existing business. For many years corporate planning systems have focused almost entirely on improving the operating model. The result is that in many, many industries leadership has almost no hope of improving operating margins by even 1%. There simply is nothing left to improve which can achieve significant results.

Simultaneously, 1% growth has a far, far greater return on investment than 1% operating margin improvement. So if companies focus their best talent on breakthroughs, in whole new ways of running the business, or creating new markets, the results are significantly greater.

Hartung: Many companies have clustered their top performers into “all star teams.” But this has been met by demotivation of employees not on these teams – feeling like “also rans” or “bench warmers.” And often there is a compensation difference between the all-star team members and others that is demotivating. How do leaders manage this conundrum?

Mankins: If this demotivation is driven by internal competitiveness — by ambition to move up the organization — there is a culture problem. Everyone is not on the same page about company needs and the talent to address those needs. Internal competitiveness should be addressed so everyone wants the company to succeed, so everyone individually can succeed. Rewards, compensation and non-compensation, need to be geared for groups to be motivated, not just individuals.

In the organization, leadership should work hard to make sure everyone knows they are important. There should be an effort to reward the “supporting cast” and not just the main characters. It is true that in today’s world many people have an exaggerated view of their own performance. We address this in the book with recommendations for how to give people feedback so they know the reality of their role and their performance in order to grow and do better. Today most companies have a very poorly performing review and training process, because they tie it to the compensation cycle thus limiting feedback to once per year and, unfortunately, doing feedback at the same time (often the same meeting) as compensation and bonus decisions. Addressing the performance feedback process can go a long way to avoid the demotivation problem.

Hartung: How do companies find “A” players?

Mankins: Search firms are the antithesis of finding “A” players. Their approach, their process, is not designed to deliver “A” candidates. To build a good group of “A” players requires the CEO, CHRO and senior leadership team understand what constitutes an “A” player in their organization. Then they can use the entire organization to seek out people with this behavioral signature in order to recruit them.

It is unfortunate that most company HR processes would not recognize an “A” player if one submitted a resume and would not hire one if they arrived for an interview. Most current processes focus too much on relationships (who candidates know,) narrow skills and prior specific experiences and not enough on what is needed for future success. And hiring decisions are often made by the wrong people; people too low in the organization and people who don’t know the desired behavioral signature. Google is one role model for knowing how to find and develop “A” players.

Unfortunately there is enormous ageism in hiring today. Especially in technology. Employers lack awareness of the value of generalizable experience they can bring into their company. The search for very specific experiences often leads to a very limited list of candidates with narrow experience and too often they do not perform at the “A” level when placed in the context of the new company and new competitive market requirements. Looking more broadly at candidates with great experience, even if not seemingly directly applicable (including candidates in their 50s and 60s) could lead to far greater success.

Sears recently announced it is closing another big batch of stores. Yawn. Who cares? Sears losses since 2010 are nearly $10 billion, with a $.75 billion loss in just the third quarter. As revenue fell another 13% overall and comparable store sales declined 7.4% investors have fled the stock for years.

Five years ago Sears had 3,510 stores. Now it has 1,687. It has 750 with leases expiring in the next five years and CFO Jason Hollar has said 550 of those are short-term enough they will let those close.

What’s striking about this statement is that Sears is a perfect candidate to file bankruptcy, renegotiate those leases, and start with a new plan for the future. Unless it has no plan. Lacking a plan to make its business successful and return those stores to profitability, the CFO is admitting the company has no choice but to keep shrinking assets as Sears simply disappears. Investors should view Sears as a microcosm of trends in traditional brick-and-mortar retailing across the industry. The business is shrinking. Fast

A closed retail store is viewed in Manhattan. (Photo by Spencer Platt/Getty Images)

A closed retail store is viewed in Manhattan. (Photo by Spencer Platt/Getty Images)

Just look at retail employment. Amidst another strong jobs report for November, retail employment actually shrank. This previously only happened in recessions – and 2016 is definitely not a recession year. And all the losses were in traditional store retailing. Kohl’s said it is hiring almost 13% fewer seasonal workers, and Macy’s says it is hiring 2.4% fewer.

In January, 2015 I wrote how the trend to e-commerce had taken hold, and traditional retailing would never again be the same. For the 2014 holiday season online retail grew 17%, but brick-and-mortar sales actually declined. This was a pivotal event. It clearly indicated a sea change in the marketplace, and it was clear valuations would be shifting accordingly. Surprising many, but not those who really understood the trends and market shifts, six months later (July, 2015) Amazon’s market cap exceeded that of much larger Wal-Mart.

ALL trends (including mobile use) reinforce on-line growth, brick and mortar decline.

The 2016 holiday season is further reinforcing this trend. The National Retail Federation reported that on black Friday 99 million people went to stores. 108.5million shopped online. Black Friday online sales jumped 21.6%.

And this trend is going to continue amplifying as more people do more shopping from mobile devices, which they all have in their hands most of the day, every day . E-commerce apps are making the on-line experience constantly better. On Thanksgiving day 70% of all on-line retail traffic was mobile, and for the first time ever 53% of on-line orders were from mobile devices – exceeding the orders placed on PCs. With this kind of access, and easy shopping, the need to travel to physical stores accelerates their decline.

Sears is beyond rescue. Unfortunately, there are a number of retailers already so challenged by the on-line competition that they are “the walking dead.” They will falter, and fail, just like the former Dow Jones Industrial retailing giant. They will not make the shift to on-line effectively. They are unwilling to dramatically change their business model, unwilling to cannibalize store sales to create an aggressively competitive on-line business. Expect bad things at JCPenney, Kohl’s, Pier 1 – and weakness at giants Wal-Mart and even Target.

Christmas used to be the time when investors in traditional retail cheered. Results for the quarter could create great gains in stock values. But that time is long gone – passed during the 2014 inflection when traditional started declining while e-commerce continued double digit growth. One can understand the Scrooge-like mentality of those investors, who dread seeing the shift in customers, and valuation, away from their companies and toward the Amazon’s who embrace trends and market shifts.

(Photo by Spencer Platt/Getty Images)

Howard Schultz is one of those CEO legends. Like Steve Jobs, Larry Ellison, Jeff Bezos and Mark Zuckerberg, he turned a startup into a huge, mega-billion dollar company – and in the process created an entirely new market. This isn’t easy to do, and that’s why business acolytes and the media turn these people into heroes.

But, is it right to hand-wring over Schultz’s departure as CEO? After all, things have not been pretty for investors since Mr. Jobs turned over Apple to his hand-picked successor Tim Cook. However, could this change mean something better is in store for shareholders?

First, let’s address the very popular myth that when Mr. Schultz left Starbucks in 2000 his successors nearly destroyed the company – and Starbucks was saved only by Mr. Schultz returning with his tremendous creativity and servant leadership. While it is great propaganda for making the Schultz as hero story more appealing, it isn’t exactly accurate.

His successor, Orin Smith, far outperformed Mr. Schultz, more than tripling the chain to over 9,000 stores and expanding revenue to over $5 billion in just four years! He expanded the original model internationally, began adding many new varieties of coffee and other drinks, and even added food. These enhancements were tremendously successful at bringing in additional revenue, even if the average store revenue fell as smaller stores were added in places like airports, hotels and entertainment venues.

In 2007 Starbucks fourth quarter saw 22% revenue increase, and for the year 21% growth. Comparable store sales grew 5%. International margins expanded, and net earnings grew over 19% from $564 million to $673 million.

Starbucks’ stock, from 2000 when Mr. Schultz departed into 2006 rose 375%, from $4 to just under $19 per share. Not the ruination that some seem to think was happening.

But Mr. Schultz did not like the diversification, even if it produced more revenue and profit. He joined the chorus of analysts that beat down the P/E ratio, and the stock price, as the company expanded beyond its “core” coffee store business.

When the Great Recession hit, and people realized they could live without $4 per cup of coffee and a $50 per day habit, revenues plummeted, as they did for many restaurants and retailers. Mr. Schultz seized the opportunity to return to his old job as CEO. That the downturn in Starbucks had far more to do with the greatest economic debacle since the 1930s was overlooked as Mr. Schultz blamed everything on the previous CEO and his leadership team – firing them all.

What returning CEO Schultz did was far from creative. He simply stopped all the projects that didn’t fit his definition of the “core” Starbucks he created. And he closed 600 stores in 2009 then 300 more in 2010 – making the chain smaller as new store openings stopped. Although the popular myth is that Starbucks stagnated under Mr. Schultz successors, the opposite was true. The chain expanded both its “core” and new incremental revenues from 2000 though 2008. But as Mr. Schultz returned as CEO from 2008 through 2011 Starbucks actually did stagnate , with virtually no growth.

Since 2012 Starbucks has returned to doing what it did prior to 2000 – opening more stores. Growing from 17,000 to 25,000 stores. Refocused on its very easy to understand, if dated, business model analysts loved the simpler company and bid up the P/E to over 30 – creating a trough (2008) to peak (2016) increase in adjusted stock price from $4 to $60 – an incredible 15 times!

But, more realistically one should compare the price today to that of 2006, before the entire market crashed and analysts turned negative on the profitable Starbucks diversification and business model expansion. That gain is a more modest 300% – basically a tripling over a decade – far less a gain for investors than happened under the 2000-2006 era of Mr. Schultz’s successors.

Mr. Schultz succeeded in returning Starbucks to its “core.” But now he’s leaving a much more vulnerable company. As my fellow Forbes contributor Richard Kestenbaum has noted, retail success requires innovation. Starbucks is now almost everywhere, leaving little room for new store expansion. Yet it has abandoned other revenue opportunities pioneered under Messrs. Smith and Donald. And competition has expanded dramatically – both via direct coffee store competitors and the emergence of new gathering spots like smoothie stores, tech stores and fast casual restaurants that are attracting people away from a coffee addiction.

At some point Starbucks and its competition will saturate the market. And tastes will change. And when that happens, growth will be a lot harder to find. As McDonald’s and WalMart have learned, business models grow tired and customers switch . Exciting new competitors emerge, like Starbucks once was, and Amazon.com is increasingly today.

Mr. Schultz has said he is vastly more confident in this change of leadership than he was the last time he left – largely because he feels this hand-picked team (as if he didn’t pick the last team, by the way) will continue to remain tightly focused on defending and extending Starbucks “core” business. This approach sounds all too familiar – like Jobs selection of Cook – and the risks for investors are great.

A focus on the core has real limits. Diminishing returns do apply. And P/E compression (from the very high 30+ today) could cause Starbucks to lose any investor upside, possibly even cause the stock to decline. If Mr. Schultz’s departure was opening the door for more innovation, new business expansion and a change to new trends that sparked growth one could possibly be excited. But there is real reason for concern – just as happened at Apple.

As I write this in 2016, Hurricane Matthew is crashing into Daytona Beach. It is a monster storm, and far from over. But there already is a great lesson we can learn.

Shockingly, after passing nearly half of Florida, including densely populated areas like Miami, Fort Lauderdale and Palm Beach, only one person has died. Even as northeastern Florida awaits Matthew’s fury, damage assessments are underway in south Florida. Even though 600,000 homes are without power, utility companies are already restoring power to over 50,000 homes, and that number is growing. The Florida highway system is open, with all roads passable and people are able to reach safety, while realistically expecting they may soon be able to return to their homes. By all accounts, damage is considerable. Yet, few lives were lost and repair is already underway – long before the storm is ending.

Photo by Drew Angerer/Getty Images

The lesson here is that scenario planning is incredibly valuable. Florida’s leaders have been preparing for this storm for years. The many agencies, federal, state, county and municipal, built their scenarios, and prepared action plans. They talked about “what if” various things happened, and thought through the impacts – and actions they would take.

Then, there’s Brexit. The British currency has fallen to 30-plus year lows. This morning a “flash crash” happened with the currency falling 10% in minutes. Even though the pound recovered much of that loss, the crash left traders and those who do international business shaken. This was just the latest reaction to the British vote to exit the EU.

JUSTIN TALLIS/AFP/Getty Images

This week people in all parts of the international business community were trying to figure out how to react to Prime Minister May’s speech saying Britain would seek a “hard exit.” This seems to imply a faster, more drastic break from Europe. But as David Buik, market commentator at Panmure Gordon & Co. said, “The media decided very quickly what interpretation to put on the term ‘hard Brexit,’ when most of us are none the wiser as to what Brexit means yet.”

The key word here is “reacting.” It is clear that almost nobody had any plans for undertaking Britain’s departure from the EU, even as the effort to create a vote, and implement a vote, occurred. While there was a lot of talk, nobody in government or business had a plan for what to do if the vote to leave actually passed. Now everyone is reacting, and the consequences are significant fear, uncertainty and doubt (FUD), and wild swings in everything from currency values to equity values and even real estate.

Proper scenario planning separates leaders from wanna-bes, and winners from losers. Those who consider what might happen, and prepare for events, inevitably do far, far better than those who react. Lacking a preparedness plan, based on careful consideration of “what-ifs,” it is impossible to implement good decision-making, because you have no idea what markers, or metrics, to watch – and no idea of what actions to take as those metrics vary.

I observed a scenario-planning meeting where the head of planning was asking questions – “what-if…regulations go in this direction…technology accomplishes this level of performance…customer adoption of a substitute increase.” After a series of these propositions were discussed, the CEO said “This seems to be a waste of time. We don’t know what will happen. What if pigs could fly?” Given a lack of facts about the future, he proposed building a future plan based upon the market as it existed at the time, and reacting to changes only after they occurred.

The planning lead responded, “Whether or not pigs will fly has very little to do with the future performance of our company. And that is why we aren’t discussing flying pigs. These variables in the scenarios could have a major impact on future performance, and if we prepare for them we most likely will improve competitiveness, sales and profits.”

Scenario planning is not a wild exercise of imaginary happenings. Scenario planning uses known trends to identify key variables which can be measured. By looking forward on the trend, it is possible to predict possible outcomes – and prepare.

For example, famously, the leadership of Apple in 2000 looked at the trend toward high-speed internet implementation, including WiFi. They started tracking high-speed implementation, and realized that as bandwidth expanded and improved the desire to work on-line would grow as well. They began preparing products for much greater on-line use (iMac) and products based on widely available, low cost internet access. The result was a shift from near bankruptcy to the most valuable traded equity in America in just one decade.

Planning systems are biased toward using historical data, and do not consider big changes. Leadership must constantly fight the urge to assume the future will look like the past, and invest time building scenario plans. Building the skill to predict the future, using trends to build scenarios and plans, is a hallmark of the most successful companies.

Florida’s leaders could have assumed another big hurricane would not hit their state, and simply waited to react when it happened. By thinking through possible outcomes, they have shown an amazing level of preparedness. In contrast, Britain’s leaders did not think through the impact of a British exit, pushed for a vote prematurely, and now are lurching from point to point, reacting to events, unprepared for any outcome – and trying to create and implement a plan “on the fly.”

How prepared is your company? How often do you discuss future scenarios, and actually plan for them? Or do you plan based on history, hoping the future will look like the past? Are you going to use scenarios to be effective in future markets?

Or are you going to wait for events to unfold, react and hope you don’t drown?