by Adam Hartung | Jul 11, 2018 | Computing, Growth Stall, Innovation, Investing, Software

The last few quarters sales growth has not been as good for Apple as it once was. The iPhone X didn’t sell as fast as they hoped, and while the Apple Watch outsells the entire Swiss watch industry it does not generate the volumes of an iPhone. And other new products like Apple Pay and iBeacon just have not taken off.

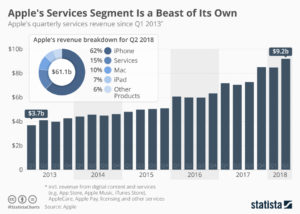

Amidst this slowness, the big winner has been “Apple Services” revenue. This is largely sales of music, videos and apps from iTunes and the App store. In Q2, 2018 revenues reached $9.2B, 15% of total revenues and second only to iPhone sales. Although Apple does not have a majority of smartphone users, the user base it has spends a lot of money on things for Apple devices. A lot of money.

In a bit of “get them the razor so they will buy the razor blades” CEO Tim Cook’s Apple is increasingly relying upon farming the “installed base” of users to drive additional revenues. Leveraging the “installed base” of users is now THE primary theme for growing Apple sales. And even old-tech guys like Warren Buffett at Berkshire Hathaway love it, as they gobble up Apple shares. As do many analysts, and investors. Apple has paid out over $100B to developers for its services, and generated over $40B in revenues for itself – and with such a large base willing to buy things developers are likely to keep providing more products and working to grow sales.

In a bit of “get them the razor so they will buy the razor blades” CEO Tim Cook’s Apple is increasingly relying upon farming the “installed base” of users to drive additional revenues. Leveraging the “installed base” of users is now THE primary theme for growing Apple sales. And even old-tech guys like Warren Buffett at Berkshire Hathaway love it, as they gobble up Apple shares. As do many analysts, and investors. Apple has paid out over $100B to developers for its services, and generated over $40B in revenues for itself – and with such a large base willing to buy things developers are likely to keep providing more products and working to grow sales.

But the risks here should not be taken lightly. At one time Apple’s Macintosh was the #1 selling PC. But it was “closed” and required users buy their applications from Apple. Microsoft offered its “open architecture” and suddenly lots of new applications were available for PCs, which were also cheaper than Macs. Over a few years that “installed base” strategy backfired for Apple as PC sales exploded and Mac sales shrank until it became a niche product with under 10% market share.

Today, Android phones are the #1 smartphone market share platform, and Android devices (like the PC) are much cheaper. Even cheaper are Chinese made products. Although there are problems, the risk exists that someday apps, etc for Android and/or other platforms could become more standard and the larger Android base could “flip” the market.

The history of companies relying on an installed base to grow their company has not gone well. Going back 30 years, AM Multigraphics an ABDick sold small printing presses to schools, government agencies and businesses. After the equipment sale these companies made most of their growth on the printing supplies these presses used. But competitors whacked away at those sales, and eventually new technologies displaced the small presses. The installed base shrank, and both companies disappeared.

Xerox would literally give companies a copier if they would just pay a “per click” charge for service on the machine, and use Xerox toner. Xerox grew like the proverbial weed. Their service and toner revenue built the company. But then people started using much cheaper copiers they could buy, and supply with cheaper consumables. And desktop publishing solutions caused copier use to decline. So much for Xerox growth – and the company rapidly lost relevance. Now Xerox is on the verge of disappearing into Fuji.

HP loved to sell customers cheap ink-jet printer so they bought the ink. But now images are mostly transferred as .jpg, .png or .pdf files and not printed at all. The installed base of HP printers drove growth, until the need for any printing started disappearing.

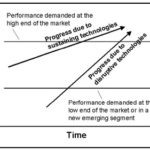

The point? It is very risky to rely on your installed platform base for your growth. Why? Because competitors with cheaper platforms can come along and offer cheaper consumables, making your expensive platform hard to keep forefront in the market. That’s the classic “innovator’s dilemma” – someone comes along with a less-good solution but it’s cheaper and people say “that’s good enough” thus switching to the cheaper platform. This leaves the innovator stuck trying to defend their expensive platform and aftermarket sales as the market switches to ever better, cheaper solutions.

It’s great that Apple is milking its installed base. That’s smart. But it is not a viable long-term strategy. That base will, someday, be overtaken by a competitor or a new technology. Like, maybe, smart speakers. They are becoming ubiquitous. Yes, today Siri is the #1 voice assistant. But as Echo and Google speaker sales proliferate, can they do to smartphones what smartphones did to PCs? What if one of these companies cooperates with Microsoft to incorporate Cortana, and link everything on the network into the Windows infrastructure? If these scenarios prevail, Apple could/will be in big trouble.

I pointed out in October, 2016 that Apple hit a Growth Stall. When that happens, maintaining 2% growth long-term happens only 7% of the time. I warned investors to be wary of Apple. Why? Because a Growth Stall is an early indicator of an innovation gap developing between the company’s products and emerging products. In this case, it could be a gap between ever enhanced (beyond user needs) mobile devices and really cheap voice activated assistant devices in homes, cars, offices, everywhere. Apple can milk that installed base for a goodly while, but eventually it needs “the next big thing” if it is going to continue being a long-term winner.

by Adam Hartung | Apr 3, 2018 | Computing, Growth Stall, Innovation, Investing, Mobile, Music

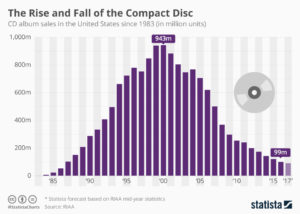

Do you still have a pile of compact discs? If so, why? When was the last time you listened to one? Like almost everyone else, you probably stream your music today. If you are just outdated, you listen to music you bought from iTunes or GooglePlay and store on your mobile device. But it would be considered prehistoric to tell people you carry around CDs for listening in your car – because you surely don’t own a portable CD player.

As the chart shows, CD sales exploded from nothing in 1983 to nearly 1B units in 2000. Now sales are less than 1/10th that number, due to the market shift expanded bandwidth allowed.

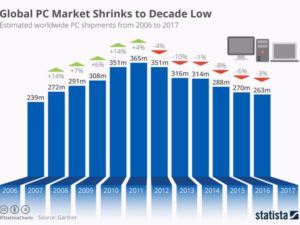

Do you still carry a laptop? If so, you are a dying minority. As PCs became more portable they became indispensable. Nobody left the office, or attended a meeting, without their laptop. That trend exploded until 2011, when PC sales peaked at 365M units. As the chart shows, in the 6 years since, PC sales have dropped by over 100M units, a 30% decline. The advent of mobile devices (smartphones and tablets) coupled with expanded connectivity and growing cloud services allowed mobility to reach entirely new levels – and people stopped carrying their PCs. And just like CDs are disappearing, so will PCs.

These charts dramatically show how quickly a new technology, or package of technologies, can change the way we behave. Simultaneously, they change the competitive landscape. Sony dominated the music industry, as a producer and supplier of hardware, when CDs dominated. But, as I wrote in 2012, the shift to more portable music caused Sony to fall into a rapid decline, and the company suffered 6 consecutive years (24 quarters) of falling sales and losses. The one-time giant was crippled by a technology shift they did not adopt. And they weren’t alone, as big box retailers such as Best Buy and Circuit City also faltered when these sales disappeared.

Once, Microsoft was synonymous with personal technology. Nobody maximized the value in PC growth more than Microsoft. But changing technology altered the competitive landscape, with Apple, Google, Samsung and Amazon emerging as the leaders. Microsoft, as the almost unnoticed launch of Windows 10 demonstrated, is struggling to maintain relevancy.

Too often we discount trends. Like Sony and Microsoft we think historical growth will continue, unabated. We find ways to discount market shifts, saying the products are “niche” and denigrating their quality. We will express our view that the market has “hiccuped” and will return to growth again. By the time we admit the shift is permanent new competitors have overtaken the lead, and we risk becoming totally obsolete. Like Toys-R-Us, Radio Shack, Sears and Motorola.

Aircraft stalls when not enough power to climb

The time for action is when the very first signs of shift happened. I’ve written a lot about “Growth Stalls” and they occur in just 2 quarters. 93% of the time a stalled company never again grows at a mere 2%/year. Look at how fast GE went from the best company in America to the worst. It is incredibly important that leadership react FAST when trends push customers toward new solutions, because it often takes very little time for the trend to make dying markets completely untenable.

by Adam Hartung | Mar 13, 2018 | Defend & Extend, Growth Stall, Innovation, Investing, Software

In February, Berkshire Hathaway revealed it had dumped its IBM position. Good riddance to a stock that has gone down for 5 years while the S&P went up! What did Buffett do with the money? He loaded up on Apple – making that high-flyer Berkshire’s #1 holding. So, isn’t the smart thing now to buy Apple?

First, don’t confuse your investing goals with Berkshire Hathaway’s. It may seem that everyone has the same objective, to buy stocks that go up. But Berkshire is a very special case. As I pointed out in 2014, we mere mortals can’t invest like Buffett, and shouldn’t try. Berkshire Hathaway has the opportunity to make investments in special situations with tremendous return potential that we don’t have. Berkshire’s investment strategy is to invest where it can create cash to prepare for special situations, or to park money where it can make a decent return, and hopefully generate cash while it waits.

Apple is the #1 most cash-rich company on the planet, and with the new tax laws it can repatriate that cash. This is an opportunity for a “special dividend” to investors, and that is the kind of thing that Buffett loves. He isn’t a venture capitalist looking for a 10x price appreciation. He wants a decent 5% rate of return, and hopefully dividends, so he can grow cash for his special situation opportunities. Apple, the most valuable company on any exchange, is exactly the kind of company where he can place a few billion dollars without driving up the price and let it sit making a solid 5-6%, collect dividends and maybe get a few kickers from things like the cash repatriation.

Second, let’s not forget that Buffett’s IBM buying spree lost money. If he was a great tech investor, he never would have bought IBM. He bought it for the same reason he’s buying Apple, only he was wrong about what was going to happen to IBM as it continued to lose relevancy.

I pointed out in May, 2016 that Apple was showing us all a lot of sustaining innovations, with new rev levels of existing products, but almost no new disruptive innovations. The company that once gave us iPods, iTunes, iPhones and iPads was increasingly relying on the next version of everything to drive sales. Lots of incremental improvement. But little discussion about any breakthrough products, like iBeacon, ApplePay or even the Apple Watch. In a real way, Apple was looking a lot more like the old Microsoft with its Windows and Office fascination than the old Apple.

By October, 2016 Apple hit a Growth Stall. While this may have seemed like “no big deal,” recall that only 7% of the time do companies maintain a 2% growth rate after stalling. Is Apple going to be in that 7%? With the launch of the less-than-overwhelming iPhone X, and the actual drop in iPhone sales in Q4, 2017 it looks increasingly like Apple is on the same road as all other stalled companies.

In the short term Apple has said it is milking its installed base. By constantly bringing out new apps it has raised iTunes sales to over $30B/quarter. And it has a dedicated cadre of developers making over $25B/year creating new apps. So Apple is doing its best to get as much revenue out of that installed base of iPhones as it can, even if device sales slow (or decline.) For Buffett, this is no big deal. After all, he’s parking cash and hoping to get dividends. Milking the base is a cash generation strategy he would love – like a railroad, or Coca-Cola.

But if you’re interested in maintaining high returns in your portfolio, be aware of what’s happening. Apple is changing. It’s not going to falter and fail any time soon. But don’t be lulled by Berkshire’s big purchases into thinking Apple in 2018 is anything like it was in 2012 – or through 2014. Instead, keep your eyes on game changers like Netflix, Tesla and Amazon.

by Adam Hartung | Oct 21, 2017 | In the Swamp, Investing, Leadership

In other words, CEO Flannery continues the strategy of making GE smaller, and a less hospitable workplace, that his predecessor Immelt started implementing 16 years ago. That’s the strategy that has seen GE lose ~45% of its value since Immelt took the top job, and lose over 60% of its value since peaking at $60 in 2000. So far, GE just keeps shrinking in size, and value, and leadership gives no indication it has a plan to grow GE revenues and profits in future markets building on major market trends.

What’s most surprising is that people seem surprised by the horrible current performance, and surprised that GE is in such terrible condition. All the way back in

December, 2010 this column highlighted selections for CEO of the year, and CEO of the decade, and in doing so pointed out that GE’s Immelt was on nobody’s list. Even though his predecessor, Jack Welch, was widely lauded.

Immelt inherited one of America’s strongest, fastest growing and most valuable companies. But in the first few years of his leadership the company completely failed to maintain Welch’s gains, and under Immelt’s mismanagement nearly went bankrupt by not preparing for the near-collapse of financial services in the Great Recession. It was obvious then that Immelt was trying to be a “caretaker” of GE, a “steward” of its history. But he was not an effective leader with plans for a growing future, and competitors were beating up GE in all markets. Even upstarts like Facebook, and its CEO Mark Zuckerberg, were far outperforming the stagnating, declining GE.

By May, 2012 it was impossible to miss the mismanagement at GE.

This column selected CEO Immelt as the 4th worst CEO of all publicly traded American companies (beaten in badness by Mike Duke of WalMart who was pushed out during allegations of international bribery and fraud, Ed Lampert of Sears who has now completely destroyed the once great retailer, and Steve Ballmer of Microsoft who over-invested in Windows and Office while missing every major tech development of the last 15 years before being forced out by the board.) By 2012 it was time for the Board of Directors to take action and replace Immelt. But few investors amplified this column’s cries for change, and quiet complacency set in as people simply expected GE to perform better. Just because it was GE, it appeared, as there were no signs the company understood market trends and how to ignite growth.

Of course, performance did not improve at GE. By April, 2015 GE was the victim of a total leadership failure. The company was not developing any major new trends, and Immelt’s focus was on unraveling old businesses, mostly via sales to external parties, in order to increase cash. And the cash was used for share buybacks and dividends, rather than investing in growth. A slow, and badly implemented, liquidation of one of America’s oldest, and greatest, companies was underway.

Which made GE a target for activist investors, and Trian Funds took up the challenge, investing $1.5B in GE stock and taking a seat on the GE board. Finally, it was time for action. Immelt was pushed out and Flannery was put in, and dramatic cuts and re-organizations led the discussions. Current appearances indicate GE will be significantly dismantled, assets will be sold, and in short order GE will look nothing like the great company it once was.

But, the question remains, why did things have to become so bad before the board took action? Why were people surprised? Why didn’t Jim Cramer scream for a leadership housecleaning 7, 5 or 3 years ago? Why didn’t shareholders vote against CEO compensation plans on the “say-on-pay” measures, exerting their voice to change a lackluster board that was allowing an incompetent CEO to remain in the job? Why wasn’t the pension fund, constantly whittling away at retiree benefits, forcing change? Why were so many people, so many leaders, so quiet about what was an obvious business failure? A failure that needed to be addressed, first and foremost, by replacing the CEO?

So GE’s stock value has taken a big hit of late. And now people seem surprised by the admission of how bad things really are. What’s really surprising is that people are surprised. This was not hard to see coming.

Adam's book reveals the truth about how to use strategy to outpace the competition.

Follow Adam's coverage in the press and in other media.

Follow Adam's column in Forbes.

by Adam Hartung | Jul 14, 2017 | In the Rapids, Innovation, Marketing

Amazon just had another record Prime Day, with sales up 60%. And the #1 product sold was Amazon’s Echo Dot speaker. At $34.99 it surpassed last year’s unit sales by seven-fold. And the traditional Echo speaker, marked down 50% to $90, broke all previous sales records.

Amazon just took a commanding lead in the voice assistant platform market

These Echo sales most likely sealed Amazon’s long-term leadership in the war to be the #1 voice assistant. Amazon already has 70% market share in voice activated speakers, nearly 3 times #2 provider Google. And all other vendors in total barely have 5% share.

While it may seem like digital speakers are no big deal, speaker sales are analogous to iPhone sales when evaluating the emergence of smartphones and apps. The iPhone seemed like a small segment until it became clear smartphones were the new personal technology platform. Apple’s early lead allowed iOS to dominate the growth cycle, making the company intensely profitable.

Echo and Echo Dot aren’t just speakers, but interfaces to voice activated virtual assistants. For Echo the platform is Amazon’s Alexa. Alexa is to voice activated devices and applications what iOS was to Smartphones. By talking to Alexa customers are able to do many things, such as shopping, altering their thermostats, opening and closing doors, raising and lowering blinds, recording people in their homes — the list is endless. And as that list grows customers are buying more Alexa devices to gain greater productivity and enhanced lifestyle. Echos are entering more homes, and multiplying across rooms in these homes.

Do you remember when early iPhone ads touted “there’s an app for that?” That tagline told customers if they changed from a standard mobile phone to a smartphone there were a lot of advantages, measured by the number of available apps. Just like iOS apps gave an advantage to owning an iPhone, Alexa skills give an advantage to owning Echo products. In the last year the number of skills available for Alexa has exploded, growing from 135 to 15,000. Quite obviously developers are building on Alexa much faster than any other voice assistant.

By radically cutting the price of both Echo Dot and Echo, and promoting sales, Amazon is creating an installed base of units which encourages developers to write even more skills/apps.

The more Alexa devices are installed, the more likely developers will write additional skills for Alexa. As more devices lead to more skills, skills leads to more Alexa/Echo capability, which encourages more people to buy Alexa activated devices, which further encourages even more skills development. It’s a virtuous circle of goodness, all leading to more Amazon growth.

For marketers it is important to realize that success really doesn’t correlate with how “good” Alexa works. Google’s Assistant and Microsoft’s Cortana perform better at voice recognition and providing appropriate responses than Alexa and Siri. But there are relatively few (almost no) devices in the marketplace built with Assistant or Cortana as the interface. Developers need their skills/apps to be on platforms customers use. If customers are buying speakers, thermostats and televisions that are embedded with Alexa, then developers will write for Alexa. Even if it has shortcomings. It’s not the product quality that determines the winner, but rather the ability to create a base of users.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

This is a horrible problem for Google, #2 in this market, because Google does not have the retail clout to place millions of their speakers (and other devices) in the market. Google is not a device company, nor a powerful retailer of Android devices. The Android device makers need to profit from their devices, so they cannot afford to sell devices unprofitably in order to build an installed base for Google. And because Android’s platform is not applied consistently across device manufacturers, Google Assistant skills cannot be assured of operating on every Android phone. All of which makes the decision to build Google Assistant skills problematic for developers.

Can Apple Stop the Alexa juggernaut?

The game is not over. Apple would like customers to use Siri on their iPhones to accomplish what Amazon and Alexa do with Echo. Apple has an enormous iPhone base, and all have Siri embedded. Perhaps Apple can encourage developers to create Siri-integrated apps which will beat back the Amazon onslaught?

Today, Apple customers still cannot use Siri to control their Apple TV (Though as of August, 2017, it’s been improved.), or make payments with ApplePay, for example. Nor can iPhone users tell Siri to execute commands for remote systems which are controlled by apps, like unlocking doors, turning on appliances, shooting remote security video or placing an on-line order. Apple has a lot of devices, and apps, but so far Siri is not integrated in a way that allows voice activation like can be done with Alexa.

Additionally, as big as the iPhone installed base has become, when comparing markets the actual raw number of speakers could catch up with iPhones. Echo Dot is $35. The cheapest iPhone is the SE, at $399 (on the Apple site although available from Best Buy at $160.) And an iPhone 7 starts at $650. The huge untapped Apple markets, such as China and India, will find it a lot easier to purchase low cost speakers than iPhones, especially if their focus is to use some of those 15,000 skills. And because of the low pricing ($35 to $90) it is easy to buy multiple devices for multiple locations in one’s home or office.

Will we look back and call Echo a Disruptive Innovation?

Innovator’s Dilemma

Recall the wisdom of Clayton Christensen‘s “Innovator’s Dilemma.” The incumbent keeps improving their product, hoping to maintain a capability lead over the competition. But eventually the incumbent far overshoots customer needs, developing a product that is overly enhanced. The disruptive innovator enters the market with a considerably “less good” product, but it meets customer needs at a much lower price. People buy the cheaper product to meet their limited goal, and bypass the more capable but more expensive early market leader.

Doesn’t this sound remarkably similar to the development of iPhones (now on version 8 and expected to sell at over $1,000) compared with a $35 speaker that is far less capable, but still does 15,000 interesting things?

The biggest loser in this new market is Microsoft

This week Microsoft announced another 1,500 layoffs in what has become an annual bloodletting ritual for the PC software giant. But even worse was the announcement that Microsoft would no longer support any version of Windows Phone OS version 8.1 or older – which is 80% of the Windows Phone market. Given that Microsoft has less than 2% market share, and that less than .4% of the installed smartphone base operates on Windows Phone, killing support for these phones will lead to sales declines. This action, along with gutting the internal developer team last year, clearly indicates Microsoft has given up on the phone business for good. This means that now Microsoft has no device platform for Cortana, Microsoft’s voice assistant, to use.

Microsoft ignored smartphones, allowing Apple’s iOS to become the early standard. Apple rapidly grew its installed base. Microsoft could not convince developers to write for Windows Phone because there weren’t enough devices in the market. Without a phone base, with tablet and hybrid sales flat to declining, and with PC sales in the gutter Cortana enters the market DOA (Dead On Arrival.) Even if it were the best voice assistant on the planet developers will not create skills for Cortana because there are no devices out there using Cortana as the interface.

So Microsoft completely missed yet another market. This time the market for voice activated devices in the smart phone, smart car or any other smart device in the IoT marketplace. It missed mobile, and now it has missed voice assist. As PC sales decline, Microsoft’s only hope is to somehow emerge a big winner in cloud storage and services (IaaS or Infrastructure as a Service) with Azure. But, Azure was a late-comer to the cloud market and is far behind Amazon’s AWS (Amazon Web Services.) Amazon has +40% market share, which is 40% more than the share of Microsoft, Google and IBM combined.

Build the base and developers will come…