by Adam Hartung | Feb 11, 2016 | Current Affairs, In the Whirlpool, Leadership, Lock-in

USAToday alerted investors that when Sears Holdings reports results 2/25/16 they will be horrible. Revenues down another 8.7% vs. last year. Same store sales down 7.1%. To deal with ongoing losses the company plans to close another 50 stores, and sell another $300million of assets. For most investors, employees and suppliers this report could easily be confused with many others the last few years, as the story is always the same. Back in January, 2014 CNBC headlined “Tracking the Slow Death of an Icon” as it listed all the things that went wrong for Sears in 2013 – and they have not changed two years later. The brand is now so tarnished that Sears Holdings is writing down the value of the Sears name by another $200million – reducing intangible value from the $4B at origination in 2004 to under $2B.

This has been quite the fall for Sears. When Chairman Ed Lampert fashioned the deal that had formerly bankrupt Kmart buying Sears in November, 2004 the company was valued at $11billion and 3,500 stores. Today the company is valued at $1.6billion (a decline of over 85%) and according to Reuters has just under 1,700 stores (a decline of 51%.) According to Bloomberg almost no analysts cover SHLD these days, but one who does (Greg Melich at Evercore ISI) says the company is no longer a viable business, and expects bankruptcy. Long-term Sears investors have suffered a horrible loss.

When I started business school in 1980 finance Professor Bill Fruhan introduced me to a concept that had never before occurred to me. Value Destruction. Through case analysis the good professor taught us that leadership could make decisions that increased company valuation. Or, they could make decisions that destroyed shareholder value. As obvious as this seems, at the time I could not imagine CEOs and their teams destroying shareholder value. It seemed anathema to the entire concept of business education. Yet, he quickly made it clear how easily misguided leaders could create really bad outcomes that seriously damaged investors.

As a case study in bad leadership, Sears under Chairman Lampert offers great lessons in Value Destruction that would serve Professor Fruhan’s teachings well:

As a case study in bad leadership, Sears under Chairman Lampert offers great lessons in Value Destruction that would serve Professor Fruhan’s teachings well:

1 – Micro-management in lieu of strategy. Mr. Lampert has been merciless in his tenacity to manage every detail at Sears. Daily morning phone calls with staff, and ridiculously tight controls that eliminate decision making by anyone other than the top officers. Additionally, every decision by the officers was questioned again and again. Explanations took precedent over action as micro-management ate up management’s time, rather than trying to run a successful company. While store employees and low- to mid-level managers could see competition – both traditional and on-line – eating away at Sears customers and core sales, they were helpless to do anything about it. Instead they were forced to follow orders given by people completely out of touch with retail trends and customer needs. Whatever chance Sears and Kmart had to grow the chain against intense competition it was lost by the Chairman’s need to micro-manage.

2 – Manage-by-the-numbers rather than trends. Mr. Lampert was a finance expert and former analyst turned hedge fund manager and investor. He truly believed that if he had enough numbers, and he studied them long enough, company success would ensue. Unfortunately, trends often are not reflected in “the numbers” until it is far, far too late to react. The trend to stores that were cleaner, and more hip with classier goods goes back before Lampert’s era, but he completely missed the trend that drove up sales at Target, H&M and even Kohl’s because he could not see that trend reflected in category sales or cost ratios. Merchandising – from buying to store layout and shelf positioning – are skills that go beyond numerical analysis but are critical to retail success. Additionally, the trend to on-line shopping goes back 20 years, but the direct impact on store sales was not obvious until customers had long ago converted. By focusing on numbers, rather than trends, Sears was constantly reacting rather than being proactive, and thus constantly retreating, cutting stores and cutting product lines.

3 – Seeking confirmation rather than disagreement. Mr. Lampert had no time for staff who did not see things his way. Mr. Lampert wanted his management team to agree with him – to confirm his Beliefs, Interpretations, Assumptions and Strategies — to believe his BIAS. By seeking managers who would confirm his views, and execute, rather than disagree Mr. Lampert had no one offering alternative data, interpretations, strategies or tactics. And, as Mr. Lampert’s plans kept faltering it led to a revolving door of managers. Leaders came and went in a year or two, blamed for failures that originated at the Chairman’s doorstep. By forcing agreement, rather than disagreement and dialogue, Sears lacked options or alternatives, and the company had no chance of turning around.

4 – Holding assets too long. In 2004 Sears had a LOT of assets. Many that could likely be redeployed at a gain for shareholders. Sears had many owned and leased store locations that were highly valuable with real estate prices climbing from then through 2008. But Mr. Lampert did not spin out that real estate in a REIT, capturing the value for SHLD shareholders while the timing was good. Instead he held those assets as real estate in general plummeted, and as retail real estate fell even further as more revenue shifted to e-commerce. By the time he was ready to sell his REIT much of the value was depleted.

Additionally, Sears had great brands in 2004. DieHard batteries, Craftsman tools, Kenmore appliances and Lands End apparel were just 4 household brands that still had high customer appeal and tremendous value. Mr. Lampert could have sold those brands to another retailer (such as selling DieHard to WalMart, for example) as their house brands, capturing that value. Or he could have mass marketd the brand beyond the Sears store to increase sales and value. Or he could have taken one or more brands on-line as a product leader and “category killer” for ecommerce customers. But he did not act on those options, and as Sears and Kmart stores faded, so did these brands – which largely no longer have any value. Had he sold when value was high there were profits to be made for investors.

5 – Hubris – unfailingly believing in oneself regardless the outcomes. In May, 2012 I wrote that Mr. Lampert was the 2nd worst CEO in America and should fire himself. This was not a comment made in jest. His initial plans had all panned out very badly, and he had no strategy for a turnaround. All results, from all programs implemented during his reign as Chairman had ended badly. Yet, despite these terrible numbers Mr. Lampert refused to recognize he was the wrong person in the wrong job. While it wasn’t clear if anyone could turn around the problems at Sears at such a late date, it was clear Mr. Lampert was not the person to do it. If Mr. Lampert had been as self-analytical as he was critical of others he would have long before replaced himself as the leader at Sears. But hubris would not allow him to do this, he remained blind to his own failings and the terrible outcome of a failed company was pretty much sealed.

From $11B valuation and a $92/share stock price at time of merging KMart and Sears, to a $1.6B valuation and a $15/share stock price. A loss of $9.4B (that’s BILLION DOLLARS). That is amazing value destruction. In a world where employees are fired every day for making mistakes that cost $1,000, $100 or even $10 it is a staggering loss created by Mr. Lampert. At the very least we should learn from his mistakes in order to educate better, value creating leaders.

by Adam Hartung | Feb 9, 2016 | Current Affairs, In the Swamp, Leadership, Web/Tech

Verizon tipped its hand that it would be interested to buy Yahoo back in December. In the last few days this possibility drew more attention as Verizon’s CFO confirmed interest on CNBC, and Bloomberg reported that AOL’s CEO Tim Armstrong is investigating a potential acquisition. There are some very good reasons this deal makes sense:

First, this acquisition has the opportunity to make Verizon distinctive. Think about all those ads you see for mobile phone service. Pretty much alike. All of them trying to say that their service is better than competitors, in a world where customers don’t see any real difference. 3G, 4G – pretty soon it feels like they’ll be talking about 10G – but users mostly don’t care. The service is usually good enough, and all competitors seem the same.

So, that leads to the second element they advertise – price. How many different price programs can anyone invent? And how many phone or tablet give-aways. What is clear is that the competition is about price. And that means the product has become generic. And when products are generic, and price is the #1 discussion, it leads to low margins and lousy investor returns.

But a Yahoo acquisition would make Verizon differentiated. Verizon could offer its own unique programming, at a meaningful level, and make it available only on their network. And this could offer price advantages. Like with Go90 streaming, Verizon customers could have free downloads of Verizon content, while having to pay data fees for downloads from other sites like YouTube, Facebook, Vine, Instagram, Amazon Prime, etc. The Verizon customer could have a unique experience, and this could allow Verizon to move away from generic selling and potentially capture higher margins as a differentiated competitor.

Second, Yahoo will never be a lead competitor and has more value as a supporting player. Yahoo has lost its lead in every major competitive market, and it will never catch up. Google is #1 in search, and always will be. Google is #1 in video, with Facebook #2, and Yahoo will never catch either. Ad sales are now dominated by adwords and social media ads – and Yahoo is increasingly an afterthought. Yahoo’s relevance in digital advertising is at risk, and as a weak competitor it could easily disappear.

But, Verizon doesn’t need the #1 player to put together a bundled solution where the #2 is a big improvement from nothing. By integrating Yahoo services and capabilities into its unique platform Verizon could take something that will never be #1 and make it important as part of a new bundle to users and advertisers. As supporting technology and products Yahoo is worth quite a bit more to Verizon than it will ever be as an independent competitor to investors – who likely cannot keep up the investment rates necessary to keep Yahoo alive.

Third, Yahoo is incredibly cheap. For about a year Yahoo investors have put no value on the independent Yahoo. The company’s value has been only its stake in Alibaba. So investors inherently have said they would take nothing for the traditional “core” Yahoo assets.

Additionally, Yahoo investors are stuck trying to capture the Alibaba value currently locked-up in Yahoo. If they try to spin out or sell the stake then a $10-12Billion tax bill likely kicks in. By getting rid of Yahoo’s outdated business what’s left is “YaBaba” as a tracking stock on the NASDAQ for the Chinese Alibaba shares. Or, possibly Alibaba buys the remaining “YaBaba” shares, putting cash into the shareholder pockets — or giving them Alibaba shares which they may prefer. Etiher way, the tax bill is avoided and the Alibaba value is unlocked. And that is worth considerably more than Yahoo’s “core” business.

So it is highly unlikely a deal is made for free. But lacking another likely buyer Verizon is in a good position to buy these assets for a pretty low value. And that gives them the opportunity to turn those assets into something worth quite a lot more without the overhang of huge goodwill charges left over from buying an overpriced asset – as usually happens in tech.

Fourth, Yahoo finally gets rid of an ineffectual Board and leadership team. The company’s Board has been trying to find a successful leader since the day it hired Carol Bartz. A string of CEOs have been unable to define a competitive positioning that works for Yahoo, leading to the current lack of investor enthusiasm.

The current CEO Mayer and her team, after months of accomplishing nothing to improve Yahoo’s competitiveness and growth prospects, is now out of ideas. Management consulting firm McKinsey & Company has been brought in to engineer yet another turnaround effort. Last week we learned there will be more layoffs and business closings as Yahoo again cannot find any growth prospects. This was the turnaround that didn’t, and now additional value destruction is brought on by weak leadership.

Most of the time when leaders fail the company fails. Yahoo is interesting because there is a way to capture value from what is currently a failing situation. Due to dramatic value declines over the last few years, most long-term investors have thrown in the towel. Now the remaining owners are very short-term, oriented on capturing the most they can from the Alibaba holdings. They are happy to be rid of what the company once was. Additionally, there is a possible buyer who is uniquely positioned to actually take those second-tier assets and create value out of them, and has the resources to acquire the assets and make something of them. A real “win/win” is now possible.

by Adam Hartung | Feb 3, 2016 | Current Affairs, Leadership, Lifecycle, Web/Tech

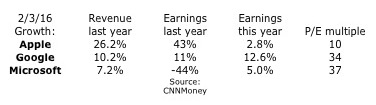

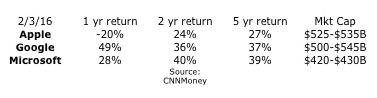

The three highest valued publicly traded companies today (2/3/16) are Google/Alphabet, Apple and Microsoft. All 3 are tech companies, and they compete – although with different business models – in multiple markets. However, investor views as to their futures are wildly different. And that has everything to do with how the leadership teams of these 3 companies have explained their recent results, and described their futures.

Looking at the financial performance of these companies, it is impossible to understand the price/earnings multiple assigned to each. Apple clearly had better revenue and earnings performance in all but the most recent year. Yet, both Alphabet and Microsoft have price to earnings (P/E) multiples that are 3-4 times that of Apple.

Much was made this week about Alphabet’s valuation exceeding that of Apple’s. But the really big story is the difference in multiples. If Apple had a multiple even half that of Alphabet or Microsoft it’s value would be much, much higher.

But, as we can see, investors did the best over both 2 years and 5 years by investing in Microsoft. And Apple investors have fared the poorest of all 3 companies regardless of time frame. Looking at investment performance, one would think that the revenue and earnings performance of these companies would be the reverse of what’s seen in the first chart.

The missing piece, of course, is future expectations. In this column a few days ago, I pointed out that Apple has done a terrible job explaining its future. In that column I pointed out how Facebook and Amazon both had stratospheric P/E multiples because they were able to keep investors focused on their future growth story, even more than their historical financial performance.

Alphabet stole the show, and at least briefly the #1 valuation spot, from Apple by convincing investors they will see significant, profitable growth. Starting even before earnings announcements the company was making sure investors knew that revenues and profits would be up. But even more they touted the notion that Alphabet has a lot of growth in non-monetized assets. For example, vastly greater ad sales should be expected from YouTube and Google Maps, as well as app sales for Android phones through Google Play. And someday on the short horizon profits will emerge from Fiber transmission revenues, smart home revenues via Nest, and even auto market sales now that the company has logged over 1million driverless miles.

This messaging clearly worked, as Alphabet’s value shot up. Even though 99% of the company’s growth was in “core” products that have been around for a decade! Yes, ad revenue was up 15%, but most of that was actually on the company’s own web sites. And most was driven by further price erosion. The number of paid clicks were up 30%, but price/click was actually down yet another 15% – a negative price trend that has been happening for years. Eventually prices will erode enough that volume will not make up the difference – and what will investors do then? Rely on the “moonshot” projects which still have almost no revenue, and no proven market performance!

But, the best performer has been Microsoft. Investors know that PC sales have been eroding for years, that PC sales will continue eroding as users go mobile, and that PC’s are the core of Microsoft’s revenue. Investors also knows that Microsoft missed the move to mobile, and has practically no market share in the war between Apple’s iOS and Google’s Android. Further, investors have known forever that gaming (xBox,) search and entertainment products have always been a money-loser for Microsoft. Yet, Microsoft investors have done far better than Apple investors, and long-term better than Google investors!

Microsoft has done an absolutely terrific job of constantly trumpeting itself as a company with a huge installed base of users that it can leverage into the future. Even when investors don’t know how that eroding base will be leveraged, Microsoft continually makes the case that the base is there, that Microsoft is the “enterprise” brand and that those users will stay loyal to Microsoft products.

Forget that Windows 8 was a failure, that despite the billions spent on development Win8 never reached even 10% of the installed base and the company is even dropping support for the product. Forget that Windows 10 is a free upgrade (meaning no revenue.) Just believe in that installed base.

Microsoft trumpeted that its Surface tablet sales rose 22% in the last quarter! Yay! Of course there was no mention that in just the last 6 weeks of the quarter Apple’s newly released iPad Pro actually sold more units than all Surface tablets did for the entire quarter! Or that Microsoft’s tablet market share is barely registerable, not even close to a top 5 player, while Apple still maintains 25% share. And investors are so used to the Microsoft failure in mobile phones that the 49% further decline in sales was considered acceptable.

Instead Microsoft kept investors focused on improvements to Windows 10 (that’s the one you can upgrade to for free.) And they made sure investors knew that Office 365 revenue was up 70%, as 20million consumers now use the product. Of course, that is a cumulative 20million – compared to the 75million iPhones Apple sold in just one quarter. And Azure revenue was up 140% – to something that is almost a drop in the bucket that is AWS which is over 10 times the size of all its competitors combined.

To many, this author included, the “growth story” at Microsoft is more than a little implausible. Sales of its core products are declining, and the company has missed the wave to mobile. Developers are writing for iOS first and foremost, because it has the really important installed base for today and tomorrow. And they are working secondarily on Android, because it is in some flavor the rest of the market. Windows 10 is a very, very distant third and largely overlooked. xBox still loses money, and the new businesses are all relatively quite small. Yet, investors in Microsoft have been richly rewarded the last 5 years.

Meanwhile, investors remain fearful of Apple. Too many recall the 1980s when Apple Macs were in a share war with Wintel (Microsoft Windows on Intel processors) PCs. Apple lost that war as business customers traded off the Macs ease of use for the lower purchase cost of Windows-based machines. Will Apple make the same mistake? Will iPad sales keep declining, as they have for 2 years now? Will the market shift to mobile favor lower-priced Android-based products? Will app purchases swing from iTunes to Google Play as people buy lower cost Android-based tablets? Have iPhone sales really peaked, and are they preparing to fall? What’s going to happen with Apple now? Will the huge Apple mobile share be eroded to nothing, causing Apple’s revenues, profits and share price to collapse?

This would be an interesting academic discussion were the stakes not so incredibly high. As I said in the opening paragraph, these are the 3 highest valued public companies in America. Small share price changes have huge impacts on the wealth of individual and institutional investors. It is rather quite important that companies tell their stories as good as possible (which Apple clearly has not, and Microsoft has done extremely well.) And likewise it is crucial that investors do their homework, to understand not only what companies say, but what they don’t say.

by Adam Hartung | Jan 30, 2016 | Current Affairs, In the Rapids, Leadership, Web/Tech

Apple announced earnings for the 4th quarter this week, and the company was creamed. Almost universally industry analysts and stock analysts had nothing good to say about the company’s reports, and forecast. The stock ended the week down about 5%, and down a whopping 27.8% from its 52 week high.

Wow, how could the world’s #1 mobile device company be so hammered? After all, sales and earnings were both up – again! Apple’s brand is still one of the top worldwide brands, and Apple stores are full of customers. It’s PC sales are doing better than the overall market, as are its tablet sales. And it is the big leader in wearable devices with Apple Watch.

Yet, let’s compare the stock price to earnings (P/E) multiple of some well known companies (according to CNN Money 1/29/16 end of day):

- Apple – 10.3

- Used car dealer AutoNation – 10.7

- Food company Archer Daniel Midland (ADM) – 12.2

- Industrial equipment maker Caterpillar Tractor – 12.9

- Farm equipment maker John Deere – 13.3

- Defense equipment maker General Dynamics – 15.1

- Utility American Electric Power – 16.9

- Industrial product company Illinois Tool Works (ITW) – 17.7

- Industrial product company 3M – 19.5

What’s wrong with this picture? It all goes to future expectations. Investors watched Apple’s meteoric rise, and many wonder if it will have a similar, meteoric fall. Remember the rise and fall of Digital Equipment? Wang? Sun Microsystems? Palm? Blackberry (Research in Motion)? Investors don’t like companies where they fear growth has stalled.

And Apple’s presentation created growth stall fears. While iPhone sales are enormous (75million units/quarter,) there was little percentage growth in Q4. And CEO Tim Cook actually predicted a sales decline next quarter! iPod sales took off like a rocket years ago, but they have now declined for 6 straight quarters and there was no prediction of a return to higher sales volumes. And as for future products, the company seems only capable of talking about Apple Watch, and so far few people have seen any reason to buy one. Amidst this gloom, Apple presented an unclear story about a future based on services – a market that is at the very least vague, where Apple has no market presence, little experience and no brand position. And wasn’t that IBM’s story some 2.5 decades ago?

In other words, Apple fed investor’s worst fears. That growth had stopped. And usually, like in the examples above, when growth stops – especially in tech companies – it presages a dramatic reversal in sales and profits. Sales have been known to fall far, far faster than management predicts. Although Apple has not yet entered a Growth Stall (which is 2 consecutive quarters of declining sales and/or profits, or 2 consecutive quarters than the previous year’s sales or profits) investors are now worried that one is just around the corner.

Contrast this with Facebook. P/E – 113.3. Facebook said ad revenues rose 57%, and net income was up 2.2x the previous year’s quarter. But what was really important was Facebook’s story about its future:

- Facebook is now a “must buy” for advertisers

- Mobile is the #1 ad trend, and 80% of revenues are from mobile

- Revenue/user is up 33%, and growing

- There are multiple unmonetized new markets that Facebook is just developing – Instagram, WhatsApp, FB Messenger and Oculus

In other words, the past was great – but the future will be even better. The short-term result? FB stock rose 7.4% for the week, and intraday hit a new 52 week high. Facebook might have seemed like a fad 3 years ago, especially to older folks. But now the company’s story is all about market trends, and how Facebook is offering products on those trends that will drive future revenue and profit growth.

Amazon may be an even better example of smart communications. As everyone knows, Amazon makes no profit. So it sells for an astonishing P/E of 846.9. Amazon sales increased 22% in Q4, and Amazon continued gaining share of the fast growing, #1 trend in retail — ecommerce. While WalMart and Macy’s are closing stores, Amazon is expanding and even creating its own logistics system.

Profits were up, but only 2/3 of expectations – ouch! Anticipating higher sales and earnings announcements the stock had run up $40/share. But the earnings miss took all that away and more as the stock crashed about $70/share! A wild 12.5% peak-to-trough swing was capped at end of week down a mere 2.5%.

But, Amazon did a great job, once again, of selling its future. In addition to the good news on retail sales, there was ongoing spectacular growth in cloud services – meaning Amazon Web Services (AWS.) JPMorganChase, Wells Fargo, Raymond James and Benchmark all raised their future price forecasts after the announcement, based on future performance expectations. Even analysts who cut their price targets still kept price targets higher than where Amazon actually ended the week. And almost all analysts expect Amazon one year from now to be worth more than its historical 52 week high, which is 19% higher than current pricing.

So, despite bad earnings news, Amazon continued to sell its growth story. Growth can heal all wounds, if investors continue to believe. We’ll see how it plays out, but for now things appear at least stable.

Steve Jobs was, by most accounts, an excellent showman. But what he did particularly well was tell a great growth story. No matter Apple’s past results, or concerns about the company, when Steve Jobs took the stage his team had crafted a story about Apple’s future growth. It wasn’t about cash flow, cash in the bank, assets in place, market share or historical success – boring, boring. There was an Apple growth story. There was always a reason for investor’s to believe that competitors will falter, markets will turn to Apple, and growth will increase!

Should investors think Apple is without future growth? Unfortunately, the communications team at Apple last week let investors think so. It is impossible to believe this is true, but the communicators this week simply blew it. Because what they said led to nothing but headlines questioning the company’s future.

What should Apple have said?

- Give investors a great news story about wearables. Show applications in health care, retail, etc. that really makes investors think all those people with a Timex or Rolex will wear an AppleWatch in the future. Apple sold investors the future of iPhone apps long before most of people used anything other than maps and weather – and the story led investors to believe if people didn’t have an iPhone they would miss out on something important, so they were bound to go buy one. Where’s that story when it comes to wearables?

- ApplePay is going to change the world. While ApplePay is #1, investors are wondering if mobile payments is ever going to be big. What will make it big, when, and what is Apple doing to make this a multi-billion dollar business? ApplePay launched to a lot of hype, but very little has been said since. Is this going to be the Apple version of Microsoft’s Zune? Make investors believers in ApplePay. Convince them this is worth a lot of future value.

- iBeacons are one of the most important technology products in retail and inventory control. iBeacons were launched as a great tool for local businesses, but since then Apple has said almost nothing. B2B may not be as sexy as consumer markets, but Microsoft made investors believers in the value of enterprise products. Demonstrate that Apple’s technology is the best, and give investors some stories about how companies are winning. Most investors have forgotten about beacons and thus they no longer plan for substantial revenues.

- Apple has the #1 mobile developer community, and the best products are yet to come – so sales are far from stalling. Honestly, the developer war is critical. The platform with the most developers wins the most customers. Microsoft taught investors that. But Apple never talks about its developer community. IBM has made a huge commitment to develop iOS enterprise apps that should drive substantial future sales, but Apple isn’t exciting investors about that opportunity. Tell investors more stories about how Apple is king of the developer world, and will remain in the top spot – better than Android or anyone – for years. Tell investors this will turn users toward tablets from PCs faster, and iPod sales will start growing again as smartphone and wearable sales join suit.

- Apple will win big revenues in auto markets. There was lots of rumors about hiring people to design a car, and now firing the lead guy. What is going on? Google has been pretty clear about its plans, but Apple offers investors no encouragement to think the company will succeed at even winning the war to be in other manufacturer’s cars, much less build its own. Given that the story sounds limited for Apple’s “core” products, investors need some stories about Apple’s own “moonshot” projects.

- Apple is not a 1-pony, iPhone story. Make investors believe it.

Tim Cook and the rest of Apple leadership are obviously competent. But when it comes to storytelling, this week their messaging looked like it was created as a high school communications project. Growth is what matters, and Apple completely missed the target. And investors are moving on to better stories – fast.

by Adam Hartung | Jan 17, 2016 | Current Affairs, In the Rapids, Innovation, Leadership, Web/Tech

Stocks are starting 2016 horribly. To put it mildly. From a Dow (DJIA or Dow Jones Industrial Average) at 18,000 in early November values of leading companies have fallen to under 16,000 – a decline of over 11%. Worse, in many regards, has been the free-fall of 2016, with the Dow falling from end-of-year close 17,425 to Friday’s 15,988 – almost 8.5% – in just 10 trading days!

With the bottom apparently disappearing, it is easy to be fearful and not buy stocks. After all, we’re clearly seeing that one can easily lose value in a short time owning equities.

But if you are a long-term investor, then none of this should really make any difference. Because if you are a long-term investor you do not need to turn those equities into cash today – and thus their value today really isn’t important. Instead, what care about is the value in the future when you do plan to sell those equities.

Investors, as opposed to traders, buy only equities of companies they think will go up in value, and thus don’t need to worry about short-term volatility created by headline news, short-term politics or rumors. For investors the most important issue is the major trends which drive the revenues of those companies in which they invest. If those trends have not changed, then there is no reason to sell, and every reason to keep buying.

(1) Buy Amazon

Take for example Amazon. Amazon has fallen from its high of about $700/share to Friday’s close of $570/share in just a few weeks – an astonishing drop of over 18.5%. Yet, there is really no change in the fundamental market situation facing Amazon. Either (a) something dramatic has changed in the world of retail, or (b) investors are over-reacting to some largely irrelevant news and dumping Amazon shares.

Everyone knows that the #1 retail trend is sales moving from brick-and-mortar stores to on-line. And that trend is still clearly in place. Black Friday sales in traditional retail stores declined in 2013, 2014 and 2015 – down 10.4% over the Thanksgiving Holiday weekend. For all December, 2015 retail sales actually declined from 2014. Due to this trend, mega-retailer Wal-Mart announced last week it is closing 269 stores. Beleaguered KMart also announced more store closings as it, and parent Sears, continues the march to non-existence. Nothing in traditional retail is on a growth trend.

However, on-line sales are on a serious growth trend. In what might well be the retail inflection point, the National Retail Federation reported that more people shopped on line Black Friday weekend than those who went to physical stores (and that counts shoppers in categories like autos and groceries which are almost entirely physical store based.) In direct opposition to physical stores, on-line sales jumped 10.4% Black Friday.

And Amazon thoroughly dominated on-line retail sales this holiday season. On Black Friday Amazon sales tripled versus 2014. Amazon scored an amazing 35% market share in e-commerce, wildly outperforming number 2 Best Buy (8%) and ten-fold numbers 3 and 4 Macy’s and WalMart that accomplished just over 3% market share each.

Clearly the market trend toward on-line sales is intact. Perhaps accelerating. And Amazon is the huge leader. Despite the recent route in value, had you bought Amazon one year ago you would still be up 97% (almost double your money.) Reflecting market trends, Wal-Mart has declined 28.5% over the last year, while the Dow dropped 8.7%.

Amazon may not have bottomed in this recent swoon. But, if you are a long-term investor, this drop is not important. And, as a long-term investor you should be gratified that these prices offer an opportunity to buy Amazon at a valuation not available since October – before all that holiday good news happened. If you have money to invest, the case is still quite clear to keep buying Amazon.

(2) Buy Facebook

The trend toward using social media has not abated, and Facebook continues to be the gorilla in the room. Nobody comes close to matching the user base size, or marketing/advertising opportunities Facebook offers. Facebook is down 13.5% from November highs, but is up 24.5% from where it was one year ago. With the trend toward internet usage, and social media usage, growing at a phenomenal clip, the case to hold what you have – and add to your position – remains strong. There is ample opportunity for Facebook to go up dramatically over the next few years for patient investors.

(3) Buy Netflix

When was the last time you bought a DVD? Rented a DVD? Streamed a movie? How many movies or TV programs did you stream in 2015? In 2013? Do you see any signs that the trend to streaming will revert? Or even decelerate as more people in more countries have access to devices and high bandwidth?

Last week Netflix announced it is adding 130 new countries to its network in 2016, taking the total to 190 overall. By 2017, about the only place in the world you won’t be able to access Netflix is China. Go anywhere else, and you’ve got it. Additionally, in 2016 Netflix will double the number of its original programs, to 31 from 16. Simultaneously keeping current customers in its network, while luring ever more demographics to the Netflix platform.

Netflix stock is known for its wild volatility, and that remains in force with the value down a whopping 21.8% from its November high. Yet, had you bought 1 year ago even Friday’s close provided you a 109% gain, more than doubling your investment. With all the trends continuing to go its way, and as Netflix holds onto its dominant position, investors should sleep well, and add to their position if funds are available.

(4) Buy Google

Ever since Google/Alphabet overwhelmed Yahoo, taking the lead in search and on-line advertising the company has never looked back. Despite all attempts by competitors to catch up, Google continues to keep 2/3 of the search market. Until the market for search starts declining, trends continue to support owning Google – which has amassed an enormous cash hoard it can use for dividends, share buybacks or growing new markets such as smart home electronics, expanded fiber-optic internet availability, sensing devices and analytics for public health, or autonomous cars (to name just a few.)

The Dow decline of 8.7% would be meaningless to a shareholder who bought one year ago, as GOOG is up 37% year-over year. Given its knowledge of trends and its investment in new products, that Google is down 12% from its recent highs only presents the opportunity to buy more cheaply than one could 2 months ago. There is no trend information that would warrant selling Google now.

(5) Buy Apple

Despite spending most of the last year outperforming the Dow, a one-year investor would today be down 10.7% in Apple vs. 8.7% for the Dow. Apple is off 27.6% from its 52 week high. With a P/E (price divided by earnings) ratio of 10.6 on historical earnings, and 9.3 based on forecasted earnings, Apple is selling at a lower valuation than WalMart (P/E – 13). That is simply astounding given the discussion above about Wal-mart’s operations related to trends, and a difference in business model that has Apple producing revenues of over $2.1M/employee/year while Walmart only achieve $220K/employee/year. Apple has a dividend yield of 2.3%, higher than Dow companies Home Depot, Goldman Sachs, American Express and Disney!

Apple has over $200B cash. That is $34.50/share. Meaning the whole of Apple as an operating company is valued at only $62.50/share – for a remarkable 6 times earnings. These are the kind of multiples historically reserved for “value companies” not expected to grow – like autos! Even though Apple grew revenues by 26% in fyscal 2015, and at the compounded rate of 22%/year from 2011- 2015.

Apple has a very strong base market, as the world leader today in smartphones, tablets and wearables. Additionally, while the PC market declined by over 10% in 2015, Apple’s Mac sales rose 3% – making Apple the only company to grow PC sales. And Apple continues to move forward with new enterprise products for retail such as iBeacon and ApplePay. Meanwhile, in 2016 there will be ongoing demand growth via new development partnerships with large companies such as IBM.

Unfortunately, Apple is now valued as if all bad news imaginable could occur, causing the company to dramatically lose revenues, sustain an enormous downfall in earnings and have its cash dissipated. Yet, Apple rose to become America’s most valuable publicly traded company by not only understanding trends, but creating them, along with entirely new markets. Apple’s ability to understand trends and generate profitable revenues from that ability seems to be completely discounted, making it a good long-term investment.

In August, 2015 I recommended FANG investing. This remains the best opportunity for investors in 2016 – with the addition of Apple. These companies are well positioned on long-term trends to grow revenues and create value for several additional years, thereby creating above-market returns for investors that overlook short-term market turbulence and invest for long-term gains.

by Adam Hartung | Dec 30, 2015 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership

2015 was not short on bad decisions, nor bad outcomes. But there are 5 major leadership themes from 2015 that can help companies be better in 2016:

1 – Cost cutting, restructurings and stock buybacks do not increase company value – Dow/DuPont

There was no shortage of financial engineering experiments in 2015 intended to increase short-term shareholder returns at the expense of long-term value creation. Companies continued borrowing money to buy back their own stock – spending more on repurchases than they made in profits.

Unfortunately, too many companies continue to increase earnings per share (EPS) via financial machinations rather than creating and introducing new products, or creating new markets.

In a grand show of value reducing financial re-engineering, 2015 is ending with the massive merger between Dow and DuPont. There is no intent of introducing new products or entering new markets via this merger. Rather, to the contrary, the plan is to merge these beasts, lay off tens of thousands of employees, cut the R&D staff, cut new product introductions and “rationalize” the company into 3 new businesses intended to be relaunched as new companies, with fewer products, less business development and less competition.

Massive cost cutting will weaken both companies, put thousands out of work and leave the marketplace with fewer new products. All just to create 3 new, different profit and loss statements in the hopes of improving the EPS and price to earnings (P/E) multiple. This story has become all too familiar the last few years, and the only winners are the bankers, who will make massive fees, and hedge fund managers that rapidly dump the stock in the terrible companies they leave behind.

2 – Doing more of the same is not innovative and does not create value – McDonald’s

McDonald’s has been losing market share to fast casual restaurants for over a decade. Yet, leadership insists on constantly maintaining its undying focus on the fast food success formula upon which the company was launched some 60 years ago.

As the number of customers continued declining, McDonalds kept closing more stores. Yet, sales per store remained weak even as the denominator grew smaller. Unwilling to actually update McDonald’s to make it fit modern trends, in 2015 leadership decided the path to growth was serving breakfast all-day. Really. It is still hard to believe. No new products, just the same McMuffins and sausage biscuits, but now offered for more hours.

Because of McDonald’s size and legacy the media covered this story heavily in 2015. Yet, as 2016 starts we all can look back and see that this was no story at all. Doing more of the same is not in any way innovative or revolutionary. Defending and extending an outdated success formula does not fix a company strategy that is out of date and rapidly losing relevancy.

3 – Hiring the wrong CEO is a BIG problem – Yahoo

We would like to think that Boards are really good at hiring CEOs. Unfortunately, we are regularly reminded they are not. The Board at Yahoo has spent a decade making bad CEO selections, and now the company’s core business is valueless.

In 2015 we saw that the decision by Yahoo’s board to hire a CEO based on political correctness (gender advantages), and limited experience with a well known company (a short Google career) rather than leadership capability could be deadly. Although Marissa Mayer was hired in 2012 amid much fanfare, we learned in 2015 that Yahoo is worth only the value of its Alibaba shareholdings, and no more. Yahoo as it was founded is now worth – nothing.

After 3 years of Mayer leadership it became clear that “there was no there, there” at Yahoo (to quote Gertrude Stein.) The value of the company’s “core” search and content accumulation businesses dropped to zero. Although 3 years have passed, practically no progress has been made toward developing a new business able to compete in the market shifted to social media and instant communications. Investors now realize Ms. Mayer has failed to grow future revenue and profits for the historical internet leader. Following a decade of incompetent CEOs, Yahoo has been left almost wholly irrelevant.

What was once Yahoo will soon be Alibaba USA, as the company gets rid of its old businesses – in some fashion, although who would want them is unclear – in order to allow shareholders to preserve their value in Alibaba stock purchased by Jerry Yang in 2005.

Yahoo has become irrelevant, replaced by its minority stake in Alibaba, largely due to a Board unable to identify and hire a competent CEO – ending with the wholly unqualified selection of Ms. Mayer, who will achieve at least a footnote in history for the outsized compensation package she received and the huge severance that will come her way, wildly out of proportion to her poor performance, when leaving Yahoo.

4 – Even 1 dumb leadership decision can devastate a company — Turing Pharmaceuticals and CEO Shkreli

In 2015 former hedge fund manager Martin Shkreli raised a lot of money, and obtained control of an anit-parasitic pharmaceutical product. Recognizing that his customers either paid up or died, and being young, naïve, enormously greedy and without much oversight he decided to raise product pricing 70-fold. This would leave his customers either dead, bankrupt or bankrupting the insurance companies paying for his product – but he infamously said he did not care.

Thumbing your nose at customers, and regulators, is never a good idea. And even if they could not roll back the price quickly, they could target the CEO and his company for further investigation. It didn’t take long until Mr. Shrkeli was indicted for stock manipulation, leaving Turing Pharmaceuticals in disrepair as it rapidly cut staff and tried to determine what it will do next. Now KaloBios Pharma, controlled by Turing, is forced to file bankruptcy.

Never forget that Al Capone did not go to prison for stealing, bribing police, bootlegging, number running, murder or other gangster behavior. He went to prison for tax evasion. The simple lesson is, when you think you are smarter than everyone else, can do whatever you want and thumb your nose at those with government powers you’ll soon find yourself under the microscope of investigation, and most likely in really big trouble. And in the desire to take down the unwise CEO corporations become mere fodder.

The pharma industry is a regular target of consumers and politicians. Now not only are the investors in Turing damaged by this foolishly incompetent CEO, but the entire industry will once again be under close scrutiny for its pricing practices. Arrogantly making brash decisions, based on ill-formed thinking and juvenile egotism, without careful, thoughtful consideration can create enormous damage.

5 – Putting short-term results above good business practice will hurt you very badly long-term – Volkswagen and Takata

VW cheated on its emissions tests. Takata sold deadly, exploding airbags. Both companies are large organizations with layers of management. How could judgemenetal errors so big, so costly and so deadly happen?

These outcomes did not happen because of just “one bad apple.” Cultural acceptance of lying takes years of leadership focused on short-term results, even when it means operating unethically or illegally, to be inculcated. It took years for layers of management to learn how to turn away from problems, falsify test results, fake outcomes, lie to customers and even lie to regulators. It took years to create a culture of tolerated deception and willful misrepresentation.

Unfortunately, the auto industry is a tough place to make money. There is a lot of regulation, and a lot of competition. When it becomes too hard to make money honestly, cheating can become far too easily accepted. Rather than trying to revolutionize the auto making process, or the product itself, it can be a lot easier to push managers all the way down to the front-line of procurement, manufacturing or sales to simply cheat.

“Make your numbers” becomes a mantra. If you want to keep your job, or even more importantly if you want to move up, do whatever it takes to tell those above you what they want to hear. And those above don’t ask too many questions, don’t try to figure out how results happen – just keep applying pressure to those below to do what’s necessary to make the numbers.

As VW and Takata showed us, eventually the company will be caught. And the consequences are severe. Now those companies, their customers, their employees and their shareholders are suffering. And industry regulations will tighten further to make it harder to cheat. Everyone loses when short-term results are the top goal, rather than building a sustainable long-term business.

Let’s hope for better leadership in 2016.

by Adam Hartung | Dec 19, 2015 | Books, Current Affairs, Ethics, Lifecycle

America’s middle class has been decimated. Ever since Ronald Reagan rewrote the tax code, dramatically lowering marginal rates on wealthy people and slashing capital gains taxes, America’s wealthy have been amassing even greater wealth, while the middle class has gone backward and the poor have remained poor. Losing 30% of their wealth, and for many most of their home equity, has left what were once middle class families actually closer to definitions of working poor than a 1950s-1960s middle class.

When Charles Dickens wrote “A Christmas Carole” he brought to life for readers the striking difference between those who “have” from those who “have not” in early England. If you had money England was a great place to be. If you relied on your labors then you were struggling to make ends meet, and regularly disappointing yourself and your family.

For a great many American’s that is the situation in 2015 USA.

At the book’s outset, Mr. Ebenezer Scrooge felt that his wealth was all due to his own great skill. He gave himself 100% of the credit for amassing a fortune, and he felt that it was wrong of laborers, such as his bookkeeper Mr. Cratchit, to expect to pay when seeking a day off for Christmas.

Unfortunately, this sounds far too often like the wealthy and 1%ers. They feel as if their wealth is 100% due to their great intelligence, skill, hard work or conniving. And they don’t think they owe anyone anything as they work to keep unions at bay as they campaign to derail all employee bargaining. Nor do they think they should pay taxes on their wealth as many actively seek to destroy the role of government.

Meanwhile, there are employers today who have taken a page right out of Mr. Scrooge’s book of worklife desolation. Ever since President Reagan fired the Air Traffic Controllers Union employee rights have been on the downhill. Employers increasingly do not allow employees to have any say in their work hours or workplace conditions – such as Marissa Mayer eliminating work from home at Yahoo, yet expecting 3 year commitments from all managers.

Just as Mr. Scrooge refused to put more coal in the office stove as Mr. Cratchit’s fingers froze, employers like WalMart rigidly control the workplace environment – right down to the temperature in every single building and office – in order to save cost regardless of employee satisfaction. Workplace comfort has little voice when implementing the CEOs latest cost-saving regimen.

Just as Mr. Scrooge objected to giving the 25th December as a paid holiday (picking his pocket once a year was his viewpoint,) many employers keep cutting sick leave and holidays – or, worse, they allow days off but expect employees to respond to texts, voice mails, emails and social media 24x7x365. “Take all the holiday you want, just respond within minutes to the company’s every need, regardless of day or time.”

Increasingly, those who “go to work” have less and less voice about their work. How many of you readers will check your work voice mail and/or email on Christmas Day? Is this not the modern equivalent of your employer, like Scrooge, treating you like a filcher if you don’t work on the 25th December? But, do you dare leave the smartphone, tablet or laptop alone on this day? Do you risk falling behind on your job, or angering your boss on the 26th if something happened and you failed to respond?

Like many with struggling economic uncertainty, Bob Cratchit had a very ill son. But Mr. Scrooge could not be bothered by such concerns. Mr. Scrooge had a business to run, and if an employee’s family was suffering then it was up to social services to take care of such things. If those social services weren’t up to standards, well it simply was not his problem. He wasn’t the government – although he did object to any and all taxes. And he had no value for the government offering decent prisons, or medical care to everyone.

Today, employers right and left have dropped employee health insurance, recommending employees go on the exchanges; even though these same employers do not offer any incremental income to cover the cost of exchange-based employee insurance. And many employers are cutting employee hours to make sure they are not able to demand health care coverage. And the majority of employers, and employer associations such as the Chamber of Commerce, want to eliminate the Affordable Care Act entirely, leaving their employees with no health care at all – as was the case for many prior to ACA passage.

Even worse, there are employers (especially in retail, fast food and other minimum wage environments) with employees earning so little pay that as employers they recommend their employees file for government based Medicaid in order to receive the bottom basics of healthcare. Employees are a necessity, but not if they are sick or if the employer has to help their families maintain good health.

But things changed for Mr. Scrooge, and we can hope they do for a lot more of America’s employers and wealthy elite.

Mr. Scrooge’s former partner, Mr. Jakob Marley, visits Mr. Scrooge in a dream and reminds him that, in fact, there was a lot more to his life, and wealth creation, than just Ebenezer’s toils. Those around him helped him become successful, and others in his life were actually very important to his happiness. He reminds Mr Scrooge that as he isolated himself in the search for ever greater wealth he gained money, but lost a lot of happiness.

Today we have some business leaders taking the cue from Mr. Marley, and speaking out to the Scrooges. In particular, we can be thankful for folks like Warren Buffet who consistently points out the great luck he had to be born with certain skills at this specific point in time. Mr. Buffett regularly credits his wealth creation with the luck to receive a good education, learning from academics such as Ben Graham, and having a great network of colleagues to help him invest.

Further, amplifying his role as a modern day Jacob Marley, Mr. Buffett recognizes the vast difference between his situation and those around him. He has pointed out that his secretary pays a higher percent of her income in taxes than himself, and he points out this is a remarkably unfair situation. Additionally, he makes it clear that for many wealth is a gift of birth – and “winning the ovarian lottery” does not make that wealthy person smarter, harder working or more valuable to society. Rather, just lucky.

What we need is for more wealthy Americans to have a vision of Christmas future – as it appeared to Mr. Scrooge. He saw how wealth inequality would worsen young Tiny Tim’s health, leaving him crippled and dying. He saw his employee Mr. Cratchet struggle and become ill. These visions scared him. Scared him so much, he offered a bounty upon his community, sharing his wealth.

Mr. Scrooge realized that great wealth, preserved just for him, was without merit. He was doomed to a future of being rich, but without friends, without a great world of colleagues and without the sharing of riches among everyone in order that all in society could be healthy and grow. Many would suffer, and die, if society overall did not take actions to share success.

These days we do have a few of these visionary 1%ers, such as Bill Gates, Warren Buffett and recently Mark Zuckerberg, who are either currently, or in the future, planning to disseminate their vast wealth for the good of mankind.

Yet, middle class Americans have been watching their dreams evaporate. Over the last 50 years America has changed, and they have been left behind. Hard work, well…….. it just doesn’t give people what it once did. Policy changes that favored the wealthy with Ayn Rand style tax programs have made the rich ever richer, supported the legal rights of big corporations and left the middle class with a lot less money and power. Incomes that did not come close to matching inflation, and home values that too often are more anchors than balloons have beset 2015’s strivers.

It will take more than philanthropic foundations and a few standout generous donors to rebuild America’s middle class. It will take policies that provide more (more safety nets, more health care, more education, more pension protection, more job protections and more political power) for those in the middle, and give them economic advantages today offered only wealthier Americans.

Let us hope that in 2016 we see a re-awakening of the need to undertake such rebuilding by policymakers, corporate leaders and the 1%. Let us hope this Christmas for a stronger, more robust, healthier and disparate, shared economy “for each and every one.”

by Adam Hartung | Dec 13, 2015 | In the Whirlpool, Innovation, Leadership

DuPont is one of America’s oldest corporations. Founded by Eleuthere Irenee duPont as a gunpowder manufacturer for the Revolutionary War, the company has long been one of America’s leading business institutions. From humble beginnings, DuPont became well known as a leader in Research & Development, a consistent leader in patent applications, and the inventor of products that proliferate in our lives from nylon to Teflon pans plastic bottles to Kevlar vests.

But in a series of fast actions during 2015, DuPont as it has been known is going away. And it is too bad the leadership wasn’t in place to save it. Now there will be a short-term bump to investors, but long-term cost cutting will decimate a once great innovation leader. When the bankers take over, it’s never pretty for employees, suppliers, customers or the local community.

But in a series of fast actions during 2015, DuPont as it has been known is going away. And it is too bad the leadership wasn’t in place to save it. Now there will be a short-term bump to investors, but long-term cost cutting will decimate a once great innovation leader. When the bankers take over, it’s never pretty for employees, suppliers, customers or the local community.

It has been a long time since DuPont was the kind of business leader that gathered attention like, say, Apple or Google. From dynamic roots, the company had become quite stodgy and unexciting. Many felt leadership was over-spending on overhead costs like R&D,product development and headquarters personnel.

Thus Trian Fund, led by activist investor Nelson Peltz, set its sites on DuPont, buying 2.7% of the shares and launching a proxy campaign to place its slate of directors on the Board. The objective? Slash R&D and other costs, sell some divisions, raise cash in a hurry and dress up the P&L for a higher short-term valuation.

These sort of attacks almost always work. But DuPont’s CEO, Ellen Kullman, dug in her heels and fought back. She aligned her Board, spent $15M making her case to shareholders, and in a surprising victory beat back Mr. Peltz keeping the board and management intact. In a great rarity, this May DuPont’s management convinced enough shareholders to back their efforts for improving the P&L via their own restructuring and cost improvements, planned divestitures and organic growth that existing leadership remained intact.

But this victory was quite short-lived. By October, Ms. Kullman was forced out as CEO. A few days later the CFO reported quarterly profits that were only half the previous year. Sales had continued a history of declining in almost all divisions and across almost all geographic segments – with total revenue down to $5B from $7.5B a year ago. As it had done in July and previous quarters end-of-year projections were again lowered.

Net/net – CEO Kullman and management may have won the Trian battle, but they clearly lost the business war. Unable to actually profitably grow the company, the Board lost patience. They were willing to support management, but when that team could not produce the innovations to keep growing they were willing to accelerate cost cutting ($1B in 2015 alone) in order to prop up short-term stock valuation.

Now the newly placed transaction-oriented CEO of Dupont has cooked up a deal the bankers simply love. Merge DuPont with Saran Wrap and Ziploc inventor Dow Chemical, which itself has been the target of Third Point’s activist leader Dan Loeb (which Dow settled by giving Third Point 2 board seats rather than risk a proxy battle.) Then whack even more costs – some $3B – and lay off some 20,000 of the combined companies’ 110,000 employees. Then split the remaining operations into 3 new companies and spin those out publicly.

Sounds so good on paper. So simple. And think of the size of the investment banking and legal fees!!!! That will create some great partner bonuses in 2016!

Theoretically, this will create 3 companies that are more profitable, even though sales are not improving at all. Improved P&L’s will be projected into the future, and higher P/E (price to earnings) multiples on the stock should yield investors a very nice short-term gain. A one-time investor “Christmas present.”

But what will investors actually own? The lower cost companies will now be largely without R&D, new product development, internal patent departments, university research grant management programs, and many of the finance, marketing and sales personnel. Exactly how will future growth be assured? What will happen to these once-great sources of invention and innovation?

Nothing about this mega-transaction actually makes business better for anyone:

- The companies are no closer aligned with market trends than before. In fact, lacking people in innovation positions (product development, R&D and marketing) they are very likely to become even further removed from the leading trends that could create breakthrough products.

- Competition will be reduced short-term, so there will be less price pressure. But longer-term innovation will shift to smaller companies like Monsanto and Syngenta, or even companies currently not on the industry radar – as well as universities. These big companies will be removed from the leading edge of competition, the innovation edge, and will much more likely miss the next wave of products in all markets as new competitors emerge.

- There will be no resources to develop or manage new innovations that emerge internally, or externally. The much smaller staffs will have no bandwidth to explore new technologies, new products, new go-to-market channels or new ways of doing business. There will be no resources for white space teams to explore market shifts, consider major threats to their “core,” or develop potentially disruptive businesses that will generate future growth.

A very smart CFO once told me “when the finance guys are figuring out how to make money, rather than the business guys, you need to be very worried.” Clever transactions, like the one proposed between DuPont and Dow, do not replace great leadership. These are one-time events, and almost always leave the remaining assets weaker and less competitive than before.

Leadership requires understanding markets, managing innovation, creating new solutions, disrupting old businesses by launching new ones, and generating recurring profitable sales growth. Unfortunately, DuPont suffered from a lack of great leadership for several years, which left it vulnerable. Now the bankers are in charge, busy managing spreadsheets rather than products, customers and sales.

Don’t be confused. In no way does this merger and reorganization improve the competitiveness of these businesses. And for that reason, it will not offer a long-term value enhancement for shareholders. But even more obvious is the outcome negative outcome we can expect for employees, suppliers, customers and the communities in which these companies have operated. Bad leadership let the hyenas in, and they will pick the best meat off the bone for themselves first – leaving seriously damaged carcasses for everyone else.

by Adam Hartung | Dec 6, 2015 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Web/Tech

Marissa Mayer’s reign as head of Yahoo looks to be ending like her predecessors. With a serious flop. Only this may well be the last flop – and the end of the internet pioneer.

It didn’t have to happen this way, but an inability to manage Status Quo Risk doomed Ms. Mayer’s leadership – as it has too many others. And once again bad leadership will see a lot of people – investors, employees and even customers – pay the price.

Yahoo was in big trouble when Ms. Mayer arrived. Growth had stalled, and its market was being chopped up by Google and Facebook. It’s very relevancy was questionable as people no longer needed news consolidation sites – which had ended AOL, for example – and search had long gone to Google. The intense internet users were already clearly mobile social media fans, and Yahoo simply did not compete in that space.

In other words, Yahoo desperately needed a change of direction and an entirely new strategy the day Ms. Mayer showed up. Only, unfortunately, she didn’t provide either. Instead Ms. Meyer offered, at best, a series of fairly meaningless tactical actions. Changing Yahoo’s home page layout, cancelling the company’s work-from-home policy and hiring Katie Couric, amidst a string of small and meaningless acquisitions, were the business equivalent of fiddling while Rome burned. Tinkering with the tactics of an outdated success formula simply ignored the fact that Yahoo was already well on the road to irrelevancy and needed to change, dramatically, quickly.

The saving grace for Yahoo was when Alibaba went public. Suddenly a long-ago decision to invest in the Chinese company created a vast valuation increase for Yahoo. This was the opportunity of a lifetime to shift the business fast and hard into something new, different and much more relevant than the worn out Yahoo strategy. But, unfortunately, Ms. Mayer used this as a curtain to hide the crumbling former internet leader. She did nothing to make Yahoo relevant, as fights erupted over how to carve up the Alibaba windfall.

When it became public that Ms. Mayer had hired famed strategy firm McKinsey & Co. to decide what businesses to close in its next “restructuring” it lit up the internet with cries to possibly just get rid of the whole thing! After 3 years, and more than one layoff, it now appears that Ms. Mayer has no better idea for creating value out of Yahoo than doing another big layoff to, once again, improve “focus on core offerings.” Additional layoffs, after 3 years of declining sales, is not the way to grow and increase shareholder value.

Analysts are pointing out that Yahoo’s core business today is valueless. The company is valued at less than its remaining Alibaba stake. And this is not outrageous, since in the ad world Yahoo has become close to irrelevant. Nobody would build an on-line ad campaign ignoring Google or Facebook, and several other internet leaders. But ignoring Yahoo as a media option is increasingly common.

Investors are rightly worried that the IRS will take much of the remaining Alibaba value as taxes in any spinoff, leaving them with far less money. Giving up on the CEO, and its increasingly irrelevant “core business” they are asking if it wouldn’t be smarter to sell what we think of as Yahoo to Softbank so the Japanese company can obtain the rest of Yahoo Japan it does not already own. Ostensibly then Yahoo as it is known in the USA could simply start to disappear – like AOL and all the other on-line news consolidators.

It really did not have to happen this way. Yahoo’s troubles were clearly visible, and addressable. But CEO Mayer simply chose to keep doing more of the same, making small improvements to Yahoo’s site and search tool. By keeping Yahoo aligned with its historical Status Quo risk of irrelevance, obsolescence and failure grew quarter-by-quarter.

Now Status Quo Risk (the risk created by not adapting to shifting market needs) has most likely doomed Yahoo. Investors are no longer interested in waiting for a turn-around. They want their Alibaba valuation, and they could care less about Yahoo’s CEO, employees or customers. Many have given up on Ms. Mayer, and simply want an exit strategy so they can move on.

Ms. Mayer’s leadership has shown us some important leadership lessons:

- Hiring an executive from Google (or another tech company) does not magically mean success will emerge. Like Ron Johnson from Apple to JCP, Ms. Mayer showed that even tech execs often lack an ability to understand market trends and the skills to adapt an organization.

- It is incredibly easy for a new leader to buy into an historical success formula and keep tweaking it, rather than doing the hard work of creating a new strategy and adapting. The lure of focusing on tactics and hoping the strategy will take care of itself is remarkably easy fall into. But investors need to realize that tactics do not fix an outdated success formula.

- Youth is not the answer. Ms. Mayer was young, and identified with the youthfulness of Google and internet users. But, in the end, she woefully lacked the strategy and leadership skills necessary to turn around the deeply troubled Yahoo. Young, new and fresh is no substitute for critical thinking and knowing how to lead.

- Boards give CEOs too much time to fail. It was clear within months Ms. Mayer had no strategy for making Yahoo relevant. Yet, the Board did not recognize its mistake and replace the CEOs. There still are not sufficient safeguards to make sure Boards act when CEOs fail to lead effectively.

- CEOs too often have too much hubris. Ms. Mayer went from college to a rapid career acceleration in largely staff positions to CEO of Yahoo and a Board member of Wal-Mart. It is easy to develop hubris, and an over-abundance of self-confidence. Then it is easy to require your staff agree with you, and pledge so support you (as Ms. Mayer recently did.) All of this indicates a leader running on hubris rather than critical thinking, open discourse and effective decision-making. Hubris is not just a weakness of white male leaders.

Could there have been a different outcome. Of course. But for Yahoo’s employees, suppliers, customers and investors the company hired a string of CEOs that simply were not up to the job of redirecting the company into competitiveness. Each one fell victim to trying to maintain the Status Quo. And, unfortunately, Ms. Mayer will be seen as the most recent – and possibly last – CEO to lead Yahoo into failure. Ms. Mayer simply was not up to the job – and now a lot of people will pay the price.

by Adam Hartung | Nov 18, 2015 | Current Affairs, Defend & Extend, In the Swamp, In the Whirlpool, Leadership, Web/Tech

Microsoft recently announced it was offering Windows 10 on xBox, thus unifying all its hardware products on a single operating system – PCs, mobile devices, gaming devices and 3D devices. This means that application developers can create solutions that can run on all devices, with extensions that can take advantage of inherent special capabilities of each device. Given the enormous base of PCs and xBox machines, plus sales of mobile devices, this is a great move that expands the Windows 10 platform.

Only it is probably too late to make much difference. PC sales continue falling – quickly. Q3 PC sales were down over 10% versus a year ago. Q2 saw an 11% decline vs year ago. The PC market has been steadily shrinking since 2012. In Q2 there were 68M PCs sold, and 66M iPhones. Hope springs eternal for a PC turnaround – but that would seem increasingly unrealistic.

The big market shift to mobile devices started back in 2007 when the iPhone began challenging Blackberry. By 2010 when the iPad launched, the shift was in full swing. And that’s when Microsoft’s current problems really began. Previous CEO Steve Ballmer went “all-in” on trying to defend and extend the PC platform with Windows 8 which began development in 2010. But by October, 2012 it was clear the design had so many trade-offs that it was destined to be an Edsel-like flop – a compromised product unable to please anyone.

By January, 2013 sales results were showing the abysmal failure of Windows 8 to slow the wholesale shift into mobile devices. Ballmer had played “bet the company” on Windows 8 and the returns were not good. It was the failure of Windows 8, and the ill-fated Surface tablet which became a notorious billion dollar write-off, that set the stage for the rapid demise of PCs.

And that demise is clear in the ecosystem. Microsoft has long depended on OEM manufacturers selling PCs as the driver of most sales. But now Lenovo, formerly the #1 PC manufacturer, is losing money – lots of money – putting its future in jeopardy. And Dell, one of the other top 3 manufacturers, recently pivoted from being a PC manufacturer into becoming a supplier of cloud storage by spending $67B to buy EMC. The other big PC manufacturer, HP, spun off its PC business so it could focus on non-PC growth markets.

And, worse, the entire OEM market is collapsing. For the largest 4 PC manufacturers sales last quarter were down 4.5%, while sales for the remaining smaller manufacturers dropped over 20%! With fewer and fewer sales, consolidation is wiping out many companies, and leaving those remaining in margin killing to-the-death competition.

And, worse, the entire OEM market is collapsing. For the largest 4 PC manufacturers sales last quarter were down 4.5%, while sales for the remaining smaller manufacturers dropped over 20%! With fewer and fewer sales, consolidation is wiping out many companies, and leaving those remaining in margin killing to-the-death competition.

Which means for Microsoft to grow it desperately needs Windows 10 to succeed on devices other than PCs. But here Microsoft struggles, because it long eschewed its “channel suppliers,” who create vertical market applications, as it relied on OEM box sales for revenue growth. Microsoft did little to spur app development, and rather wanted its developers to focus on installing standard PC units with minor tweaks to fit vertical needs.

Today Apple and Google have both built very large, profitable developer networks. Thus iOS offers 1.5M apps, and Google offers 1.6M. But Microsoft only has 500K apps largely because it entered the world of mobile too late, and without a commitment to success as it tried to defend and extend the PC. Worse, Microsoft has quietly delayed Project Astoria which was to offer tools for easily porting Android apps into the Windows 10 market.

Microsoft realized it needed more developers all the way back in 2013 when it began offering bonuses of $100,000 and more to developers who would write for Windows. But that had little success as developers were more keen to achieve long-term sales by building apps for all those iOS and Android devices now outselling PCs. Today the situation is only exacerbated.

By summer of 2014 it was clear that leadership in the developer world was clearly not Microsoft. Apple and IBM joined forces to build mobile enterprise apps on iOS, and eventually IBM shifted all its internal PCs from Windows to Macintosh. Lacking a strong installed base of Windows mobile devices, Microsoft was without the cavalry to mount a strong fight for building a developer community.

In January, 2015 Microsoft started its release of Windows 10 – the product to unify all devices in one O/S. But, largely, nobody cared. Windows 10 is lots better than Win8, it has a great virtual assistant called Cortana, and it now links all those Microsoft devices. But it is so incredibly late to market that there is little interest.

Although people keep talking about the huge installed base of PCs as some sort of valuable asset for Microsoft, it is clear that those are unlikely to be replaced by more PCs. And in other devices, Microsoft’s decisions made years ago to put all its investment into Windows 8 are now showing up in complete apathy for Windows 10 – and the new hybrid devices being launched.

AM Multigraphics and ABDick once had printing presses in every company in America, and much of the world. But when Xerox taught people how to “one click” print on a copier, the market for presses began to die. Many people thought the installed base would keep these press companies profitable forever. And it took 30 years for those machines to eventually disappear. But by 2000 both companies went bankrupt and the market disappeared.

Those who focus on Windows 10 and “universal windows apps” are correct in their assessment of product features, functions and benefits. But, it probably doesn’t matter. When Microsoft’s leadership missed the mobile market a decade ago it set the stage for a long-term demise. Now that Apple dominates the platform space with its phones and tablets, followed by a group of manufacturers selling Android devices, developers see that future sales rely on having apps for those products. And Windows 10 is not much more relevant than Blackberry.