by Adam Hartung | Jan 5, 2011 | Defend & Extend, In the Rapids, In the Swamp, Leadership, Lock-in, Openness

Summary:

- Business planning systems are designed to defend historical markets

- Rapidly shifting markets makes it impossible to grow by defense alone

- Growth requires understanding what customers want, and creating new solutions that most likely aren’t part of the current business

- You can’t grow if you don’t plan to grow, but to plan for growth you have to shift resources from traditional planning into scenario planning

- High growth companies like Virgin, Apple and Google plan to fulfill future needs, not defend & extend past practicess

Imagine you see a pile of hay. Above it is a sign flashing “find the needle.” That achievement would be hard. Change the sign to “find the hay” and suddenly achieving the goal becomes much easier. So, as the comedian Bill Engvall might ask, what’s your sign? Unfortunately, most businesses plan for 2011, and beyond, using the first sign. Very few do planning using the latter. Most businesses won’t grow, because they simply don’t know how to plan for growth!!

Most businesses start planning with “I’m in the horseshoe (for example) business. My market isn’t growing, and there is more capacity than demand. How can I grow?” For these people, their sign is “find the needle.”

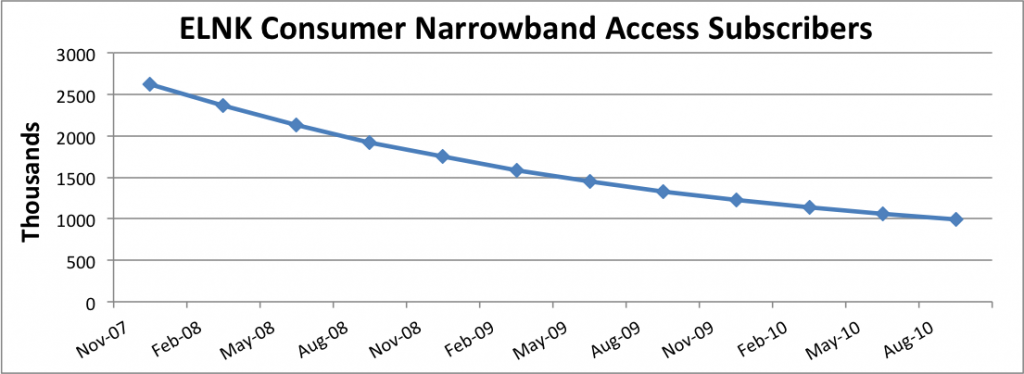

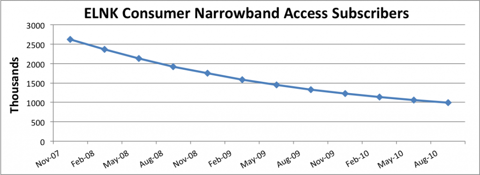

Take for example Earthlink. The company’s growth looked like a rocket ship in the early internet days as people by the millions signed up for dial-up service. But along came broadband, and the market for dial up died – never to return. Earthlink has no hope of growing as long as it thinks of itself as a dial-up company

Chart at SeekingAlpha.com author Ananthan Thangavel

Despite the absolute certainty that the market is shrinking, at this point almost all business planners will develop plans to defend this dying business as long as possible. Despite the impossibility of achieving good returns, there will be a plethora of actions to try and keep serving all the way to the very last customer. Just look at how AOL has invested millions trying to defend its dying internet access busiuness. Reality is, the company that walks away – gives up- is the smartest. There’s no way to make money as oversupply keeps too many companies spending too much to service too few customers.

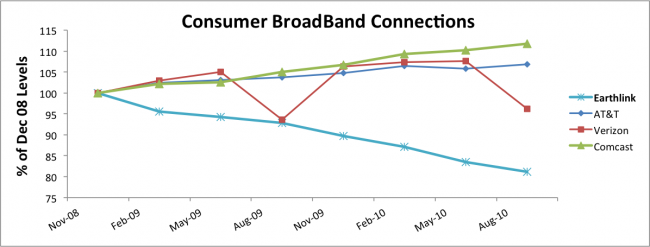

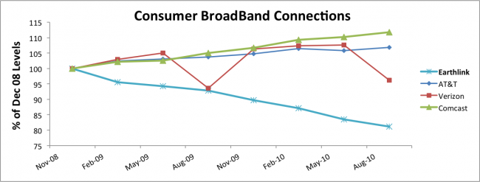

The next step for most planners is to attempt extending the business into something adjacent. For example, Earthlink would say “let’s invest in Broadband. We’ll hang onto customers as they want to switch, and maybe pick up a few customers.” But this completely ignores the fact that competitors already have a substantial lead. Competitors have learned the technology, and the marketplace. They are growing, and have no intention of giving up any room to a new competitor.

Chart at SeekingAlpha.com author Ananthan Thangavel

Planning systems are designed to keep the business doing more of what it always did, or possibly extending the business into adjacent markets after returns have faltered. Planning systems have no way of recognizing when a business, or market, has become obsolete. And practically never do they recognize the power of exsting competitors when looking at adjacent markets. As a result, the planning system produces no growth plans, leading 2011 to end with the self-fulfilling prophecy that the plan predicted – little or no growth.

The future for Earthlink is pretty grim. As it is for most companies that plan based upon history, trying to Defend & Extend their historical markets. In the highly dynamic, global marketplaces of 2011 trying to find growth by remaining focused on the past is like looking for the needle in a haystack. Maybe there’s something in there – but it’s not likely – and it’s even a lot less likely you’ll find it – and if you did, the cost of finding it will almost assuredly be greater than the value.

Alternatively, why not use planning resources to find, and develop, growth markets. Instead of looking at what you did (as in the past tense) try to figure out what you should do. Rather than studying past products, customers and markets, why not develop scenarios about the future that give you insight to what people will want to buy in 2011, 2012 and beyond? Rather than looking for needles, why not go explore the hay?

Newspapers kept focusing on declining subscriptions, when they should have been studying Craig’s List, eBay, Vehix.com and other on-line environments to learn the future of advertising. Had Tribune company poured its resources into its early internet investments, such as cars.com and careerbuilder.com, rather than trying to defend its traditional newspapers, it may well have avoided bankruptcy. But rather than looking to the future when doing its planning, and understanding that on-line news was going to explode, Tribune kept looking for the needle (cost cuts, layoffs, outsourcing, etc.) to save the old success formula.

Direct mail companies and Sunday insert printers have continued looking for ways to defend & extend their coupon printing business – despite the fact that nobody reads junk mail or uses printed coupons. Several have failed, and larger companies have merged trying to find “synergies” and more cost cuts. Simultaneously a 28 year old music major from Nothwestern university starts figuring out how to help companies acquire new customers by offering email coupons, and within 2 years his company, Groupon, is valued at around $6B. There’s nothing that stopped coupon powerhouse Advo from being Groupon, except that its planning system was devoted to finding the needle, while Groupon’s leaders decided to go play in the hay.

Hallmark and American Greetings want us to buy birthday and holiday cards for various occasions – in a world where almost nobody mails cards any longer. As they keep trying to defend their old business, and extend it into a few new opportunities for on-line cards, Twitter captures the wave of instant communications by offering everyone 140 character ways to communicate. Because Twitter is out where the growth is, the company raises $200M giving it a value of $3.7B.

Nothing stops any business from being anything it wants to be. But as most enter 2011 they will use their planning resources, including all those management meetings and hours of forms completion, to do nothing more than re-examine the historical business. Most will devolve into trying to figure out how to do more with less. As future forecasts look grim, or perhaps cautiously optimistic (based on a lot of things going right – like a mysterious pick-up in demand) there will be much nashing of teeth – and meetings looking for a needle that can be offered to employees and investors as a hope for rising future value.

Smart companies get out of that rut. They focus their planning on the future. What do customers want, and how can we give them what they want? How can we create whole new markets. Apple was a PC company, but by exploring mobility it became a provider of MP3 consumer electronics, downloadable music, a mobile device and app supplier and the early winner in cloud accessing tablets. Google has moved from a search engine to a powerhouse ad placement company and is pushing the edges of growth in mobile computing as well as several other markets. Virgin started as a distributor of long-playing vinyl record albums, but by exploring what customers really wanted it has become an international airline, cell phone company, international lender and space travel pioneer (to mention just a few of its businesses.)

You can grow in 2011, but to do so you need to shed the old planning system (and its resource wasting processes) and get serious about scenario planning. Focus on the future, not the past.

by Adam Hartung | Dec 23, 2010 | Defend & Extend, General, In the Rapids, Innovation, Leadership, Openness

“Goodbye 2010, the Year of Austerity” is the headline from Mediapost.com‘s Marketing Daily. And that could be the mantra for many, many companies. Nobody is winning today by trying to save their way to prosperity! As we move into this decade, it is important business leaders realize that the only way to create a strong bottom line (profit) is to develop a strong top line (revenue.) Recommendations:

- Never be desperate. Go to where the growth is, and where you can make money. Don’t chase any business, chase the business where you can profitably growth. Be somewhat selective.

- Focus efforts on markets you know best. I add that it’s important you understand not to do just what you like, but learn to do what customers VALUE.

- Let go of crap, traditions and “playing it safe” actions. Growth is all about learning to do what the market wants, not trying to protect the past – whether processes, products or even customers.

- More lemonade making. You can’t grow unless you’re willing to learn from everything around you. We constantly find ourselves holding lemons, but those who prosper don’t give up – they look for how to turn those into desirable lemonade. What is your willingness to learn from the market?

- Austerity measures are counterproductive 99% of the time. Efficiency is the biggest obstacle to innovation. You don’t have to be a spendthrift to succeed, but you can’t be a miser investing in only the things you know, and have done before.

- Communicate, communicate, communicate. We don’t learn if we don’t share. Developing insight from the environment happens when all inputs are shared, and lots of people contribute to the process.

- Get off the downbeat buss. There’s more to success than the power of positive thinking, but it is very hard to gain insight and push innovation when you’re a pessimist. Growth is an opportunity to learn, and do exciting things. That should be a positive for everybody – except the status quo police.

Realizing that you can’t beat the cost-cutting horse forever (in fact, most are about ready for the proverbial glue factory), it’s time to realize that businesses have been under-investing in innovation for the last decade. While GM, Circuit City, Blockbuster, Silicon Graphics and Sun Microsystems have been failing, Apple, Google, Cisco, Netflix, Facebook and Twitter have maintained double-digit growth! Those who keep innovating realize that markets aren’t dead, they’re just shifting! Growth is there for businesses who are willing to innovate new solutions that attract customers and their dollars! For every dead DVD store there’s somebody making money streaming downloads. Businesses simply have to work harder at innovating.

Fast Company gives us “Five Innovative New Year’s Resolutions:”

- Associate. Work harder at trying to “connect the dots.” Pick up on weak signals, before others, and build scenarios to help understand the impact of these signals as they become stronger. For example, 24x7WallStreet.com clues us in that greater use of mobile devices will wipe out some businesses in “The Ten Businesses The Smartphone Has Destroyed.” But for each of these (and hundreds others over the next few years) there will be a large number of new business opportunities emerging. Just look at the efforts of Foursquare and Groupon and the direction those growth businesses are headed.

- Observe. Pay attention to what’s happening in the world, and think about what it means for your (and every other) business. $100/barrel oil has an impact; what opportunity does it create? Declining network TV watching has an impact – how will you leverage this shift? Don’t just wander through the market, and reacting. Figure out what’s happening and learn to recognize the signs of growth opportunities. Use market events to drive being proactive.

- Experiment. If you don’t have White Space teams trying figure out new business models, how will you be a future winner? Nobody “lucks” into a growth market. It takes lots of trial and learning – and that means the willingness to experiment. A lot. Plan on experimenting. Invest in it. And then plan on the positive results.

- Question. Keep asking “why” until the market participants are so tired they throw you out of the room. Then, invent scenarios and ask “why not” until they throw you out again. Markets won’t tell you what the next big thing is, but if you ask a lot of questions your scenarios about the future will be a whole lot better – and your experimentation will be significantly more productive.

- Network. You can’t cast your net too wide in the effort to obtain multiple points of view. Nothing is narrower than our own convictions. Only by actively soliciting input from wide-ranging sources can you develop alternative solutions that have higher value. We become so comfortable talking to the same people, inside our companies and outside, that we don’t realize how we start hearing only reinforcement for our biases. Develop, and expand, your network as fast as possible. Oil and water may be hard to mix, but it blending inputs creates a good salad dressing.

ChiefExecutive.net headlined “2010 CEO Wealth Creation Index Shows a Few Surprises.” Who creates wealth? Included in thte Top 10 list are the CEOs of Priceline.com, Apple, Amazon, Colgate-Palmolive and DeVry. These CEOs are driving industry innovation, and through that growth. This has produced above-average cash flow, and higher valuations for their shareholders. As well as more, and better quality jobs for employees. Meanwhile suppliers are in a position to offer their own insights for ways to grow, rather than constantly battling price discussions.

Who destroys wealth? In the Top 10 list are the CEOs of Dean Foods, Kraft, Computer Sciences (CSC) and Washington Post. These companies have long eschewed innovation. None have introduced any important innovations for over a decade. Their efforts to defend & extend old practices has hurt revenue growth, providing ample opportunity for competitors to enter their markets and drive down margins through price wars. Penny-pinching has not improved returns as revenues faltered, and investors have watched value languish. Employees are constantly in turmoil, wondering what future opportunities may ever exist. Suppliers never discuss anything but price. These are not fun companies to work in, or with, and have not produced jobs to grow our economy.

Any company can grow in 2011. Will you? If you choose to keep doing what you’ve always done – well you shouldn’t plan on improved performance. On the other hand, embracing market shifts and creating an adaptive organization that identifies and launches innovation could well make you into a big winner. Next holiday season when you look at performance results for 2011 they will have more to do with management’s decisions about how to manage than any other factor. Any company can grow, if it does the right things.

by Adam Hartung | Dec 7, 2010 | Defend & Extend, In the Swamp, Leadership, Web/Tech

Today’s guest blog is provided by Mike Meikle, hope you enjoy:

Summary

- Oracle is at the top of the heap in the Traditional Software market.

- Traditional Software market is deflating with $7 billion less profit than 2009

- Software as a Service, a component of Cloud Computing, has a forecasted 26% annual growth rate over the next five years.

- Oracle Cloud Computing strategy is muddled with bi-polar corporate marketing and platform dependency.

- Customers feel trapped with Oracle and are looking for alternatives.

- Oracle is trapped in a classic Defend and Extend situation.

- Oracle seems to be following Microsoft in using 1990’s corporate strategy in 2011.

Throughout the 1990’s Microsoft held the dominant position in software. Firmly ensconced in Corporate and Consumer arenas, Microsoft generated enormous profits. With an overflowing war chest, MSFT aggressively quashed or bought out the competition – which eventually attracted the attention of the United States Justice Department.

After a little less than 10 years, Microsoft now fights to stay relevant as multiple challengers have exposed gaping holes in its armor. The tech giant’s senior leadership appears rudderless as product lines fail to get off the mark (Windows Phone 7) or flounder (Vista).

With this in mind let us turn toward Oracle. Long viewed as the top Database Management System (DBMS) for the corporate world, its database software underpins much of the global information economy. It has a large war chest stuffed with the profits created by costly traditional software licensing deals with locked-in customers. It has used that cash to acquire new lines of business (PeopleSoft, Sun) and competitors (ATG, MySQL).

However there are some dark clouds on the horizon. The advent of Cloud Computing is a threat to its current licensing model. How will Oracle adapt to corporations implementing virtual servers and databases in the Cloud? Traditional software licensing is down $7 billion industry-wide from 2009. Meanwhile “software as a service” (SaaS) is seeing explosive growth, with a forecasted 26% annual growth rate over the next five years as a natural component of Cloud Computing.

Oracle has made some efforts to delve into the Cloud Computing fray with the Oracle Exalogic Elastic Cloud, or “Cloud-In-a-Box”, leveraging their SUN and ATG acquisitions. However this arrives several years behind the Amazon, Google, and Microsoft triumvirate of Cloud Computing products. Oracle’s Cloud offering will also have to overcome Oracle’s own negative statements about Cloud Computing. CEO Larry Ellison called Cloud Computing “complete gibberish” in late 2008.

Oracle also has problems with its customers. Chafing under the steep licensing costs and sub-standard support, nearly half are looking to shift to lower cost alternatives as they become available. Many have felt trapped by lack of suitable replacements. MySQL was one such competitor, but with Oracle purchasing SUN and getting MySQL in the bargain, that option disappeared. So customers have continued to (reluctantly) fork over licensing and maintenance fees to Oracle, creating the bulk of the organization’s profit stream.

Sound familiar?

Also, the champions of Oracle software offerings, developers, are dissatisfied with the company. The founders of MySQL and the creator of Java, now key software offerings of Oracle, have jumped ship as a result of disagreements with Oracle’s corporate direction.

Now Oracle finds itself in is a classic Defend & Extend situation. Nearly all their profits rely on historical licensing and maintenance for traditional software, a market that is rapidly shrinking. Current customers are unhappy with cost and service; hungry for alternatives and ready to embrace new solutions. But Oracle has arrived late and timidly to the Cloud Computing maketplace, attempting to leverage recently acquired assets where key personnel have left (and taking who knows how much vital market and product knowledge.) Not only will Oracle have to struggle to differentiate itself from other Cloud offerings going forward, it will have to incorporate their newly acquired assets (including technologies) into a cohesive offering while trying to ramp up top notch service.

Oracle will have to break out of the “consistency trap” if it is to drive profits toward new growth. New services that provide value to the customer will have to be developed and aggressively marketed. To grow future revenue and profits Oracle cannot rely on shoehorning customers into poorly fitting licensing and support models based on the fading market of yesteryear.

Or Oracle could choose to not change its old Success Formula. For advice on that approach Oracle’s Mr. Ellison talk to Microsoft’s Mr. Ballmer to see how well his 1990’s corporate strategy is working as Microsoft stumbles into 2011.

Thanks Mike! Mike Meikle shares his insights at “Musings of a Corporate Consigliere” (http://mikemeikle.wordpress.com/). I hope you read more of his thoughts on innovation and corporate change at his blog site. I thank Mike for contributing this blog for readers of The Phoenix Principle today, and hope you’ve enjoyed his contribution to the discussion about innovation, strategy and market shifts.

If you would like to contribute a guest blog please send me an email. I’d be pleased to pass along additional viewpoints on wide ranging topics.

by Adam Hartung | Dec 6, 2010 | Current Affairs, Defend & Extend, Disruptions, Food and Drink, Leadership, Lock-in

Summary:

- Business leaders like consistency

- Consistency leads to repetition, sameness, and lower rates of return

- Kraft's product lines are consistent, but without growth

- Kraft's value has been stagnant for 10 years

- Disruptive competitors make higher rates of return, and grow

- Disruptive competitors have higher valuations – just look at Groupon

"Needless consistency is the hobgoblin of small minds" – Ralph Waldo Emerson

That was my first thought when I read the MediaPost.com Marketing Daily article "Kraft Mac & Cheese Gets New, Unified Look." Whether this 80-something year old brand has a "unified" look is wholly uninteresting. I don't care if all varieties have the same picture – and if they do it doesn't make me want to eat more powdered cheese and curved noodles.

In fact, I'm not at all interested in anything about this product line. It is kind of amusing, in an historical way, to note that people (largely children) still eat the stuff which fueled my no-cash college years (much like ramen noodles does for today's college kids.) While there's nothing I particularly dislike about the product, as an investor or marketer there's nothing really to like about it either. Pasta products always do better in a recession, as people look for cheaper belly-fillers (especially for the kid,) so that more is being sold the last couple of years doesn't tell me anything I would not have guessed on my own. That the entire category has grown to only $800M revenue across this 8 decade period only shows that it's a relatively small business with no excitement! Once people feel their finances are on firm footing sales will soon taper off.

Kraft's Mac & Cheese is emblematic of management teams that lock-in on defending and extending old businesses – even though the lack of growth leaves them struggling to grow cash flow and create a decent valuation. Introducing multiple varieties of this product has not produced growth that even matched inflation across the years. Primarily, marketing programs have been designed to try keeping existing customers from buying something else. This most recent Kraft program is designed to encourage adults to try a product they gave up eating many years ago. This is, at best, "foxhole" marketing. Spending money largely just to keep the brand from going away, rather than really expecting any growth. Truly, does anyone think this kind of spending will generate a billion dollar product line in 2011 – or even 2012?

What's wrong with defensive marketing, creating consistency across the product line – across the brand – and across history? It doesn't produce high rates of return. There are lots of pasta products, even lots of brands of mac & cheese. While Kraft's product surely produces a positive margin, multiple competitors and lack of growth means increased spending over time merely leaves the brand producing a marginal rate of return. Incremental ad spending doesn't generate real growth, just a hope of not losing ground. We know people aren't flocking to the store to buy more of the product. New customers aren't being identified, and short-term growth in revenues does not yield the kinds of returns that would enhance valuation and make the world a better place for investors – or employees.

While Kraft is trying to create headlines with more spending in a very tired product, across town in Chicago Groupon has created a $500M revenue business in just 2 years! And new reports from the failed acquisition attempt by Google indicate revenues are likely to reach $2B in 2011 (CNNMoney.com, Fortune, "Google's Groupon Groping Reveals the Shifting Power of the Web World.") Where's Kraft in this kind of growth market? After all, coupons for Kraft products have been in mailers and Sunday inserts for 50 years. Why isn't Kraft putting money into a real growth business, which is producing enormous value while cash flow grows in multiples? While Groupon has created somewhere around $6B of value in 2 years, Kraft's value has only gone sideways for the last decade (chart at Marketwatch.com.)

Kraft has not introduced a new product since — well — DiGiorno. And that's been more than a decade. While the company has big revenues – so did General Motors. The longer a company plays defense, regardless of size, trying to extend its outdated products (and business model) the riskier that business becomes. While big revenues appear to offer some kind of security, we all know that's not true. Not only does competition drive down margins in these older businesses, but newer products make it harder and harder for the old products to compete at all. Eventually, the effort to maintain historical consistency simply allows competitors to completely steal the business away with new products, creating a big revenue drop, or producing such low returns that failure is inevitable.

Lots of business people like consistency. They like consistency in how the brand is executed, or how products are aligned. They like consistency in the technology base, or production capabilities. They like consistency in customers, and markets. They like being consistent with company history – doing what "made the company famous." They like the similarity of doing something again, and again, hoping that consistency will produce good returns.

But consistency is the hobgoblin of small minds. And those who are more clever find ways to change the game. Xerox figured out how to let everyone be a one-button printer, and killed the small printing press manufacturers. HP's desktop printers knocked the growth out of Xerox. Google figured out a better way to find information, and place ads, just about killing newspapers (and magazines.) Apple found a better way to use mobile minutes, taking a big bite out of cell phone manufacturers. Amazon found a better way to sell things, killing off bookstores and putting a world of hurt on many retailers. Netflix found a better way of distributing DVDs and digital movies, sending Blockbuster to bankruptcy. Infosys and Tata found a better way of doing IT services, wiping out PWC and nearly EDS. Hulu (and soon Netflix, Google and Apple) has found a better way of delivering television programming, killing the growth in cable TV. Groupon is finding a better way of delivering coupons, creating huge concerns for direct mail companies. Now tablet makers (like Apple) are demonstrating a better way of working remotely, sending shivers of worry down the valuation of Microsoft. These companies, failed or in jeapardy, were very consistent.

Those who create disruptions show again and again that they can generate growth and above average returns, even in a recession. While those who keep trying to defend and extend their old business are letting consistency drive their behavior – leading to intense competition, genericization, and lower rates of return. Maybe Kraft should spend more money looking for the next food we would all like, rather than consistently trying to convince us we want more Mac & Cheese (or Velveeta).

by Adam Hartung | Sep 22, 2010 | Current Affairs, Defend & Extend, Film, In the Whirlpool, Leadership, Lifecycle, Lock-in, Music, Web/Tech

Summary:

- Video retailer Blockbuster (and competitor Hollywood Video) are now bankrupt

- Video rentals/sales are at an all time high – but via digital downloads not DVDs

- Nokia, once the cell phone industry leader, is in deep trouble and risk of failure

- Yet mobile use (calls, texts, internet access, email) is at an all time high

- These companies are victims of locking-in to old business models, and missing a market shift

- Commitment to defending your old business can cause failure, even when participating in high growth markets, if you don’t anticipate, embrace and participate in market shifts

- Lock-in is deadly. It can cause you to ignore a market shift.

According to YahooNews, “Blockbuster Video to File Chapter 11.” In February, Movie Gallery – the owner of primary in-kind competitor Hollywood Video – filed for bankruptcy. It’s now decided to liquidate.

The cause is market shift. Netflix made it possible to rent DVDs without the cost of a store – as has the kiosk competitor Red Box. But everyone knows that is just a stopgap, because Netflix and Hulu are leading us all toward a future where there is no physical product at all. We’ll download the things we want to watch. The market is shifting from physical items – video cassettes then DVDs – to downloads. And both Blockbuster and Hollywood Video missed the shift.

Blockbuster (or Hollywood) could have gotten into on-line renting, or kiosks, like its competition. It even could have used profits to be an early developer of downloadable movies. Nothing stopped Blockbuster from investing in YouTube. Except it’s commitment to its Success Formula – as a brick-and-mortar retailer that rented or sold physically reproduced entertainment. Lock-in. And for that commitment to its historical Success Formula the investors now will get a great big goose egg – and employees will get to be laid off – and the thousands of landlords will be left in the lurch, unprepared.

As predictable as Blockbuster was, we can be equally sure about the future of former powerhouse Nokia. Details are provided in the BusinessWeek.com article “How Nokia Fell from Grace.” As the cell phone business exploded in the 1990s Nokia was a big winner. Revenues grew fivefold between 1996 and 2001 as people around the globe gobbled up the new devices. Another example of the fact that when you enter a high growth market you don’t have to be good – just in the right market at the right time.

But the cell phone business has become the mobile device business. And Nokia didn’t anticipate, prepare for or participate in the market shift. From market dominance, it has become an also-ran. The article author blames the failure, and decline, on complacent management. Weak explanation. You can be sure the leadership and management at Nokia was doing all it possibly could to Defend & Extend its cell phone business. The problem is that D&E management doesn’t work when customers simply walk away to a new technology. It may take a few years, and government subsidies may extend Nokia’s life even longer, but Nokia has about as much chance of surviving its market shift as Blockbuster did.

When companies stumble management sees the problems. They know results are faltering. But for decades management has been trained to think that the proper response is to “knuckle down, cut costs, defend the current business at all cost.” Yet, there are more movies rented now than ever – and Blockbuster is failing despite enormous market growth. There are more mobile telephony minutes, text messages, remote emails and mobile internet searches than ever in history – yet Nokia is doing remarkably poorly. It’s not a market problem, it’s a problem of Lock-in to a solution that is now outdated. When the old supplier didn’t give the market what it wanted, the customers went elsewhere. And unwillingness to go with them has left these companies in tatters.

These markets are growing, yet the purveyors of old solutions are failing primarily because they stuck to defending their old business too long. They did not embrace the market shift, and cannibalize historical product sales to enter the new, higher growth markets. Because they chose to protect their “core,” they failed. New victims of Lock-in.