by Adam Hartung | Oct 5, 2015 | Current Affairs, In the Rapids, Innovation, Leadership, Web/Tech

Twitter’s Board decided in July to oust the CEO, Dick Costolo, due to frustration over company profits. As I wrote at the time, Twitter had continued to add members, at a rate comparable to its social media competition. And it had grown revenues, while remaining the industry leader in revenue per active user.

But the concern was a lack of profits. Oh my, if rapid revenue growth but weak profits were a reason to fire a CEO, how does Jeff Bezos keep his job?

Anyway, Mr. Costolo was replaced by an original founder and former Twitter CEO Jack Dorsey on an interim basis. Four months later, after failing in its effort to find a suitable full-time CEO, the Board has made Mr. Dorsey the permanent CEO. While he simultaneously remains full time CEO of Square, a mobile payments processing company.

As I said in my last column on this subject, investors better beware.

Facebook is tearing up the social media market. It has grown to be not only #1 in active monthly users, but at 1.5B monthly active users (MSUs) the site has 5 times the number of users that Twitter has. By adding a slew of new features and functions Facebook has become more valuable to its users – and advertisers.

According to Statista, simultaneously Facebook has grown Facebook Messenger to 700M MSUs, acquired WhatsApp with 800M MSUs and Instagram with 400M MSUs. By constantly expanding the ecosphere Facebook now has 3.4B MSUs – over 10 times the number of Twitter. Facebook is so dominant that even muscular Google, with all its resources, abandoned its efforts to compete with the juggernaut by killing Google+ (which had 300M MSUs) earlier in 2015.

Twitter had great organic growth numbers, but unlike competitors it does not dominate any particular category of social media. Linked in, with only 100M MSUs dominates business networking, and bosts a user base that skews older and more professional. Pinterest and Instagram are battling it out for leadership in photo sharing. But it is unclear how one would describe a social growth category that Twitter dominates.

I actively use Twitter. But among my peers I am the exception. When I ask people over 40 if they use Twitter I regularly hear “I don’t get it. It all looks completely chaotic. Why would I want to follow people on Twitter, and why would I want to post.” This sounds a lot like what people said of Facebook and Linked in 5 years ago. But those companies found their connection with users and people now “get it.”

So the question is whether Mr. Dorsey will make Twitter into a site that is ubiquitous, at least for one category. Can he make the product so useful that users can’t live without it, and that continues drawing in massive new numbers of users?

Twitter has not changed much at all since it was founded. It still depends on users to sign on, start tweeting, and search out others a user wants to follow. And that means follow for some reason other than that person is a celebrity or politician that simply can’t stop spouting off. The Twitter user has to hunt for like minded individuals, find a way to connect with folks who are informative to their needs and then create a dialogue — and all with pretty much the same character limits and shrunken link technology available many years ago.

Apple floundered as a manufacturer of niche PCs. The returning CEO, Steve Jobs, resurrected the company by putting all his money on mobile. It wasn’t an improved Mac that turned around Apple, but rather the launch of the iPod and iTunes, followed by the iPhone and the iPad. The way Apple stole the thunder from previously dominant Microsoft was by creating new products built on the mobile trend that led to explosive growth.

Mr. Costolo left Twitter in far better shape than Apple was in when Mr. Jobs retook the reins. But will Mr. Dorsey be able to launch a series of new products that can create an Apple-like growth explosion?

Square, where Mr. Dorsey ostensibly spends half his time, is preparing to go public. But, even though it is currently considered by many the leader in its marketplace, Square is looking down the barrel of ApplePay – a technology on every iPhone that could make it obsolete. Then there’s also Google Wallet that is on all the other smartphones. Plus well funded outfits like PayPal and Mastercard. Square will need a very competent, capable and visionary CEO to guide its development competing with these – and other – well funded and powerful companies. Square will need to add features, functions and benefits if it is create long-term value.

A lot of new products are needed by two relatively small companies in short order if they are to survive. Success will not happen by cutting costs in either. It will require intensive product development with very rapid product cycles that bring in millions upon millions of new users.

Twitter was once a disruptive innovator. Now it is hard to recognize any innovation at Twitter. Does Mr. Dorsey get it? And if he does, can he do it? And do it twice, simultaneously?

by Adam Hartung | Apr 30, 2015 | Current Affairs, Defend & Extend, In the Rapids, Innovation, Leadership, Web/Tech

Last week saw another slew of quarterly earnings releases. For long term investors, who hold stocks for years rather than months, these provide the opportunity to look at trends, then compare and contrast companies to determine what should be in their portfolio. It is worthwhile to compare the trends supporting the valuations of market leaders Google and Facebook.

Google once again reported higher sales and profits. And that is a good thing. But, once again, the price of Google’s primary product declined. Revenues increased because volume gains exceeded the price decline, which indicates that the market for internet ads keeps growing. But this makes 15 straight quarters of price declines for Google. Due to this long series of small declines, the average price of Google’s ads (cost per click) has declined 70%* since Q3 2011!

Google once again reported higher sales and profits. And that is a good thing. But, once again, the price of Google’s primary product declined. Revenues increased because volume gains exceeded the price decline, which indicates that the market for internet ads keeps growing. But this makes 15 straight quarters of price declines for Google. Due to this long series of small declines, the average price of Google’s ads (cost per click) has declined 70%* since Q3 2011!

While this is a miraculous example of what economists call demand elasticity, one has to wonder how long growth will continue to outpace price degradation. At some point the marginal growth in demand may not equal the marginal decline in pricing. Should that happen, revenues will start going down rather than up.

Part of what drives this price/growth effect has been the creation of programmatic ad buying, which allows Google to place more ads in more specific locations for advertisers via such automated products as AdMob, AdExchange and DoubleClick Bid Manager. But such computerized ad buying relies on ever more content going onto the web, as well as ever more consumption by internet users.

Further, Google’s revenues are almost entirely search-based advertising, and Google dominates this category. But this is largely a PC-related sale. Today 67.5% of Google ad revenue is from PC searches, while only 32.5% is from mobile searches. Due to this revenue skew, and the fact that people do more mobile interaction via apps, messaging apps and social media than browser, search ad growth has fallen considerably. What was a 24% year over year growth rate in Q1 2012 has dropped to more like 15% for the last 8 quarters.

So while the market today is growing, and Google is making more money, it is possible to see that the growth is slowing. And Google’s efforts to create mobile ad sales outside of search has largely failed, as witnessed by the recent death of Google+ as competition for Twitter or Facebook. It is the market shift, to mobile, which creates the greatest threat to Google’s ability to grow; certainly at historical rates.

Simultaneously, Facebook’s announcements showed just how strongly it is continuing to dominate both social media and mobile, and thus generate higher revenues and profits with outstanding growth. The #1 site for social media and messenger apps is Facebook, by quite a large margin. But, Facebook’s 2014 acquisition of What’sApp is now #2. WhatsApp has doubled its monthly active users (MAUs) just since the acquisition, and now reaches 800million. Growth is clearly accelerating, as this is from a standing start in 2011.

Facebook Messenger at #3, just behind WhatsApp. And #5 is Instagram, another Facebook acquisition. Altogether 4 of the top 5 sites, and the ones with greatest growth on mobile, are Facebook. And they total over 3billion MAUs, growing at over 300million new MAUs/month. Thus Facebook has already emerged as the dominant force, with the most users, in the fast-growing, accelerating, mobile and app sectors. (Just as Google did in internet search a decade ago, beating out companies like Yahoo, Ask Jeeves, etc.)

Google is moving rapidly to monetize this user base. From nothing in early 2012, Facebook’s mobile revenue is now $2.5B/quarter and represents 67% of global revenue (the inverse of Google’s revenues.) Further, Facebook is now taking its own programmatic ad buying tool, Atlas, to advertisers in direct competition with Google. Only Atlas places ads on both social media and internet browser pages – a one-two marketing punch Google has not yet cracked.

Google’s $17.3B Q1 2015 revenue is 30 times the revenue of Facebook. There is no doubt Google is growing, and generating enormous profits. But, for long-term investors, growth is slowing and there is reason to be concerned about the long term growth prospects of Google as the market shifts toward more social and more mobile. Google has failed to build any substantial revenues outside of search, and has had some notable failures recently outside its core markets (Google + and Google Glass.) Just how long Google will continue growing, and just how fast the market will shift is unclear. Technology markets have shown the ability to shift a lot faster than many people expected, leaving some painful losers in their wake (Dell, HP, Sun Microsystems, Yahoo, etc.)

Meanwhile, Facebook is squarely positioned as the leader, without much competition, in the next wave of market growth. Facebook is monetizing all things social and mobile at a rapid clip, and wisely using acquisitions to increase its strength. As these markets continue on their well established trends it is hard to be anything other than significantly optimistic for Facebook long-term.

* 1x .93 x .88 x .84 x .85 x .94 x .96 x .94 x .93 x .89 x .91 x .94 x .98 x .97 x .95 x .93 = .295

by Adam Hartung | Dec 11, 2014 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Lifecycle, Television, Web/Tech

The trend toward the death of broadcast TV as we’ve known it keeps moving forward. This trend may not happen as fast as the death of desktop computers, but it is a lot faster than glacier melting.

This television season (through October) Magna Global has reported that even the oldest viewers (the TV Generation 55-64) watched 3% less TV. Those 35-54 watched 5% less. Gen Xers (25-34) watched 8% less, and Millenials (18-24) watched a whopping 14% less TV. Live sports viewing is not even able to maintain its TV audience, with NFL viewership across all networks down 10-19%.

Everyone knows what is happening. People are turning to downloaded entertainment, mostly on their mobile devices. With a trend this obvious, you’d think everyone in the media/TV and consumer goods industries would be rethinking strategy and retooling for a new future.

But, you would be wrong. Because despite the obviousness of the trend, emotional ties to hoping the old business sticks around are stronger than logic when it comes to forecasting.

CBS predicted at the beginning of 2014 TV ad revenue would grow 4%. Oops. Now CBS’s lead forecaster is admitting he was way off, and adjusted revenues were down 1% for the year. But, despite the trend in viewer behavior and ad expenditures in 2014, he now predicts a growth of 2% for 2015.

That, my young friends, is how “hockey stick” forecasts are created. A lot of old assumptions, combined with a willingness to hope trends will be delayed, and you can ignore real data while promising people that the future will indeed look like the past – even when it defies common sense.

To compensate for fewer ads the networks have raised prices on all ads. But how long can that continue? This requires a really committed buyer (read more about CMO weaknesses below) who simply refuses to acknowledge the market has shifted and the dollars need to shift with it. That cannot last forever.

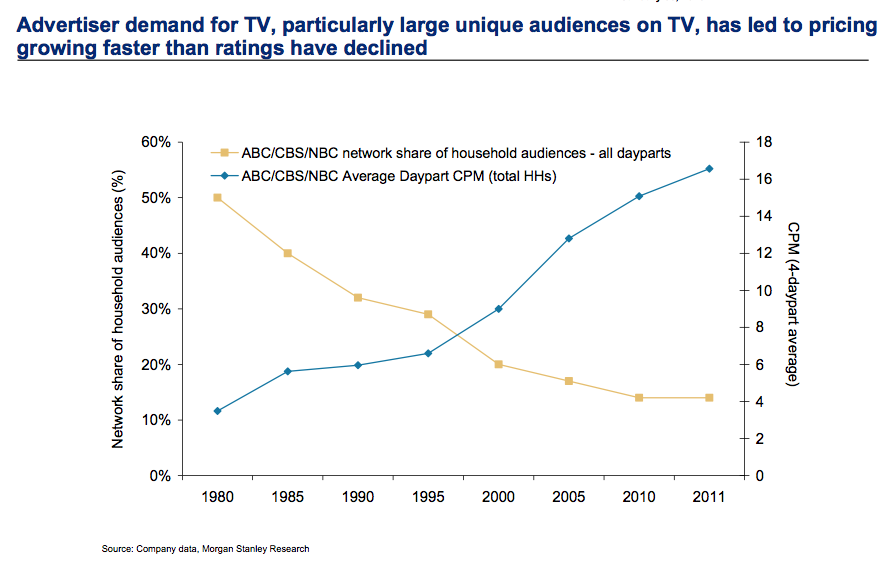

Meanwhile, us old folks can remember the days when Nielsen ratings determined what was programmed on TV, as well as what advertisers paid. Nielsen had a lock on measuring TV audience viewing, and wielded tremendous power in the media and CPG world.

But now AC Nielsen is struggling to remain relevant. With TV viewership down, time shifting of shows common and streaming growing like the proverbial weed Nielsen has no idea what entertainment the public watches. They don’t know what, nor when, nor where. Unwilling to move quickly to develop tools for catching all the second screen viewing, Nielsen has no plan for telling advertisers what the market really looks like – and the company looks to become a victim of changing markets.

Which then takes us to looking at those folks who actually buy ads that drive media companies. The Chief Marketing Officers (CMOs) of CPG companies. Surely these titans of industry are on top of these trends, and rapidly shifting their spending to catch the viewers with the most ads placed for the lowest cost.

You would wish.

Unfortunately, because these senior executives are in the oldest age groups, they are a victim of their own behavior. They still watch TV, so assume others must as well. If there is cyber-data saying they are wrong, well they simply discount that data. The Nielsen’s aren’t accurate, but these execs still watch the ratings “because it’s the best info we have” – a blatant untruth by the way. But Nielsen does conveniently reinforce their built in assumptions, and their hope that they won’t have to change their media spend plans any time soon.

Further, very few of these CMOs actually use social media. The vast majority watch their children, grandchildren and young employees use mobile devices constantly – and they bemoan all the activity on YouTube, Facebook, Instagram and Twitter – or for the most part even Linked-in. But they don’t actually USE these products. They don’t post information. They don’t set up and follow channels. They don’t connect with people, share information, exchange photos or tell stories on social media. Truthfully, they ignore these trends in their own lives. Which leaves them woefully inept at figuring out how to change their company marketing so it can be more relevant.

The trend is obvious. The answer, equally so. Any modern marketer should be an avid user of social media. Most network heads and media leaders are farther removed from social media than the Pope! They don’t constantly download entertainment, and exchanging with others on all the platforms. They can’t manage the use of these channels when they don’t have a clue how they work, or how other people use them, or understand why they are actually really valuable tools.

Are you using these modern tools? Are you actually living, breathing, participating in the trends? Or are you, like these outdated execs, biding your time wasting money on old programs while you look forward to retirement? And likely killing your company.

When trends emerge it is imperative we become part of that trend. You can’t simply observe it, because your biases will lead you to hope the trend reverts as you continue doing more of the same. A leader has to adopt the trend as a leader, be a practicing participant, and learn how that trend will make a substantial difference in the business. And then apply some vision to remain relevant and successful.

by Adam Hartung | Feb 24, 2014 | Current Affairs, Defend & Extend, In the Rapids, Leadership, Transparency, Web/Tech

Facebook is acquiring WhatsApp, a company with at most $300M revenues, and 55 employees, for $19billion. That’s billion – with a “b.” An astonishing figure that is second only to HP’s acquisition of market leader Compaq, which had substantial revenues and profits, as tech acquisitions. $19B is 13 times Facebook’s (not WhatsApp’s) entire 2013 net income – and almost 2.5 times Facebook’s (again, not WhatsApp’s) 2013 gross revenues!

On the mere face of it this valuation should make the most dispassionate analyst swoon. In today’s world very established, successful companies sell for far, far lower valuations. Apple is valued at about 13 times earnings. Microsoft about 14 times earnings. Google 33 times. These are small fractions of the nearly infinite P/E placed on WhatsApp.

But there is a leadership lesson offered here by CEO Zuckerberg’s team that is well worth learning.

Irrelevancy can happen remarkably quickly. True in any industry, but especially in digital technology. Examples: Research-in-Motion/Blackberry. Motorola. Dell. HP all lost relevancy in months and are struggling. (For those who want non-tech examples think of Circuit City, Best Buy, Sears, JCPenney, Abercrombie and Fitch.) Each of these companies was an industry leader that lust its luster, most of its customers, a big chunk of its employees and much of its market valuation in months when the company missed a market shift.

Although leadership knew what it had historically done to sell products profitably, in a very short time market trends reduced the value of the company’s historical success formula leaving investors, as well as management, wondering how it was going to compete.

Facebook is not immune to changing market trends. Although it has been the benchmark for social media, it only achieved that goal after annihilating early leader MySpace. And although Facebook was built by youthful folks, trends away from using laptops and toward mobile devices have challenged the Facebook platform. Simultaneously, changing communication requirements have altered the use, and impact, of things like images, photos, charts and text. All of these have the potential impact of slowly (or not so slowly) eroding the value (which is noticably lofty) of Facebook.

Most leaders address these kinds of challenges by launching new products to leverage the trend. And Facebook did just that. Facebook not only worked on making the platform more mobile friendly, but developed its own platform apps for photos and texting and all kinds of new features.

But, and this is critical, external companies did a better job. Two years ago Instagram emerged as a leader in image sharing. And WhatsApp has developed a superior answer for messaging.

Historically leadership usually said “we need to find a way to beat these new guys.” They would make it hard to integrate new solutions with their dominant platform in an effort to block growth. They would spend huge amounts on marketing and branding to try overcoming the emerging leader. Often they filed intellectual property litigation in an effort to cause short-term business interuption and threaten viability. They might even try hiring the emerging company’s tech leader away to stop development.

All of these actions were efforts to defend & extend the early leader’s market position. Even though the market is shifting, and trends are developing externally from the company, leadership will tend to look inside for an answer. It will often ignore the trend, disparage the competition, keep promising improvements to its historical products and services and blanket the media with PR as to its stated superiority.

But, as that list (above) of companies that lost relevancy demonstrates, this rarely works. In a highly interconnected, fast-paced, globally competitive marketplace customers go where they want. Quickly. Often leaving the early leader with a management team (and Board of Directors) scratching its head and wondering how it lost so much market position, and value, so quickly.

Hand it to Mr. Zuckerberg’s team. Instead of ignoring trends in its effort to defend & extend its early lead, they reached out and brought the leader to them. $1B for Instagram was a big investment, especially so close to launching an IPO. But, it kept Facebook relevant in mobile platforms and imaging.

And making a nosebleed-creating $19B deal for WhatsApp focuses on maintaining relevancy as well. WhatsApp already processes almost as many messages as the entire telecom industry. It has 450million users with 70% active daily, which is already 60% the size of Facebook’s daily user community (550million.) By bringing these people into the Facebook corporate family it assures the company of continued relevancy as the market shifts. It doesn’t matter if these are the same people, or different people. The issue is that it keeps Facebook relevant, rather than losing relevance to a competitor.

How will this all be monetized into $19B? The second brilliant leadership call by Facebook is to not answer that question.

Facebook didn’t know how to monetize its early leadership in users, but management knew it had to find a way. Now the company has grown from almost no revenues in 2008 to almost $8B in just 5 years. (Does your company have a plan to add $8B/year of organic revenue growth by 2019?)

So just as Facebook had to find its revenue model (which it is still exploring,) Zuckerberg’s team allows the leadership of Instagram and WhatsApp to remain independent, operating in their own White Space, to grow their user base and learn how to monetize what is an extraordinarily large group of happy folks. When looking to grow in new markets, and you find a team with the skills to understand the trends, it is independence rather than integration that makes the most sense organizationally.

Thirdly, back to that valuation issue. $19B is a huge amount of money. Unless you don’t really spend $19B. Facebook has the blessed ability to print its own. Private money that it can use for such acquisitions. As long as Facebook has a very high market valuation it can make acquisitions with shares, rather than real money.

In the case of both Instagram and WhatsApp the acquisition is being made in a mix of cash, Facebook stock and restricted Facebook stock for employees. The latter two of these three items are not real money. They are simply pieces of paper giving claims to ownership of Facebook, which itself is valued at 22 times 2013 revenue and 116 times 2013 earnings. The price of those shares are all based on expectations; expectations which now require the performance of Instagram and WhatsApp to make happen.

By making acquisitions with Facebook shares the leadership team is able to link the newly acquired managers to the same overall goals as Facebook, while offering an extremely high price but without actually having to raise any money – or spend all that money.

All companies risk of becoming irrelevant. New technologies, customer behavior patterns, regulations, inventions and innovations constantly challenge old success formulas. Most leaders fall into a pattern of trying to defend & extend their old business in the face of market shifts, hastening the fall into irrelevancy. Or they try to acquire a new business, then integrate it into the old business which strips away the new business value and leads, inevitably, to irrelevancy.

The leaders of Facebook are giving us a lesson in an alternative approach. (1) Recognize the market shift. Accept it. If there is a better solution, rush toward it rather than ignoring it. (2) Bring it into the company, and leave it independent. Eschew integration and efforts to find “synergy.” (You never know, in 3 years the company may need to be renamed WhatsApp to reflect a new market paradigm.) (3) And as long as you can convince investors that you are maintaining your relevancy use your highly valued stock as currency to keep the company moving forward.

These are 3 great lessons for all leadership teams. And I continue to think Facebook is the one stock to own in 2014.

by Adam Hartung | Jan 8, 2014 | Current Affairs, In the Rapids, Innovation, Leadership, Web/Tech

Most investors really aren’t. They are traders. They sell too fast, and make too many transactions. That’s why most small “investors” don’t do as well as the market averages. In fact, most don’t even do as well as if they simply put money into certificates of deposit or treasury bills.

I subscribe to the idea you should be able to invest in a company, and then simply forget about it. Whether you invest $10 or $100,000, you should feel confident when you buy a stock that you won’t touch it for 3, 5 or even 10 years. Let the traders deal with volatility, just wait and let the company do its thing and go up in value. Then sometime down the road sell it for a multiple of what you paid.

That means investing in big trends. Find a trend that is long-lasting, perhaps permanent, and invest in the leader. Then let the trend do all the work for you.

Imagine you bought AT&T in the 1950s as communication was about to proliferate and phones went into every business and home. Or IBM in the 1960s as computer technology overtook slide rules, manual databases and bookkeeping. Microsoft in the 1980s as personal computers became commonplace. Oracle in the 1990s as applications were built on relational databases. Google, Amazon and Apple in the last decade as people first moved to the internet in droves, and as mobile computing became the next “big thing.”

In each case investors put their money in a big trend, and invested in a leader far ahead of competitors with a strong management team and product pipeline. Then they could forget about it for a few years. All of these went up and down, but over time the vicissitudes were obliterated by long-term gains.

Today the biggest trend is social media. While many people still decry its use, there is no doubt that social media platforms are becoming commonplace in how we communicate, look for information, share information and get a lot of things done. People inherently like to be social; like to communicate. They trust referrals and comments from other people a lot more than they trust an ad – and often more than they trust conventional media. Social media is the proverbial fast flowing river, and getting in that boat is going to take you to a higher value destination.

And the big leader in this trend is Facebook. Although investors were plenty upset when Facebook tumbled after its IPO in 2012, if you had simply bought then, and kept buying a bit each quarter, you’d already be well up on your investment. Almost any purchase made in the first 12 months after the IPO would now have a value 2 to 3 times the acquisition price – so a 100% to 200% return.

But, things are just getting started for Facebook, and it would be wrong to think Facebook has peaked.

Few people realize that Facebook became a $5B revenue company in 2012 – growing revenue 20X in 4 years. And revenue has been growing at 150% per year since reaching $1B. That’s the benefit of being on the “big trend.” Revenues can grow really, really, really fast.

And the market growth is far from slowing. In 2013 the number of U.S. adults using Facebook grew to 71% from 67% in 2012. And that is 3.5 times as often as they used Linked-In or Twitter (22% and 18%.) And Facebook is not U.S. user dependent. Europe, Asia and Rest-of-World have even more users than the USA. ROW is 33% bigger than the USA, and Facebook is far from achieving saturation in these much higher population markets.

Advertisers desiring to influence these users increased their budgets 40% in 2013. And that is sure to grow as users and their interactions climb. According to Shareaholic, over 10% of all internet referrals come from Facebook, up from 7% share of market the previous year. This is 10 times the referral level of Twitter (1%) and 100 times the levels of Linked in and Google+ (less than .1% each.) Thus, if an advertiser wants to users to go to its products Facebook is clearly the place to be.

Facebook acquires more of these ad dollars than all of its competition combined (57% share of market,) and is 4 times bigger than competitors Twitter and YouTube (a Google business.) The list of Grade A advertisers is long, including companies such as Samsung ($100million,) Proctor & Gamble ($60million,) Microsoft ($35million,) Amazon, Nestle, Unilever, American Express, Visa, Mastercard and Coke – just to name a few.

And Facebook has a lot of room to grow the spending by these companies. Google, the internet’s largest ad revenue generator, achieves $80 of ad revenue per user. Facebook only brings in $13/user – less than Yahoo ($18/user.) So the opportunity for advertisers to reach users more often alone is a 6x revenue potential – even if the number of users wasn’t growing.

But on top of Facebook’s “core” growth there are new revenue sources. Since buying revenue-free Instagram, Facebook has turned it into what Evercore analysts estimate will be a $340M revenue in 2014. And as its user growth continues revenue is sure to be even larger in future years.

Even a larger opportunity for growth is the 2013 launched Facebook Ad Exchange (FBX) which is a powerful tool for remarketing unused digital ad space and targeting user behavior – even in mid-purchase. According to BusinessInsider.com FBX already sells to advertisers millions of ads every second – and delivers up billions of impressions daily. All of which is happening in real-time, allowing for exponential growth as Facebook and advertisers learn how to help people use social media to make better purchase decisions. FBX is currently only a small fraction of Facebook revenue.

Stock investing can seem like finding a needle in a haystack. Especially to small investors who have little time to do research. Instead of looking for needles, make investing easier. Eschew complicated mathematical approaches, deep portfolio theory and reams of analyst reports and spreadsheets. Invest in big trends that are growing, and the leaders building insurmountable market positions.

In 2014, that means buy Facebook. Then see where your returns are in 2017.