by Adam Hartung | Dec 29, 2020 | eBooks, Innovation, Investing, Strategy, Trends

Thrive to the Future – 4 top trends for 2021 and beyond.

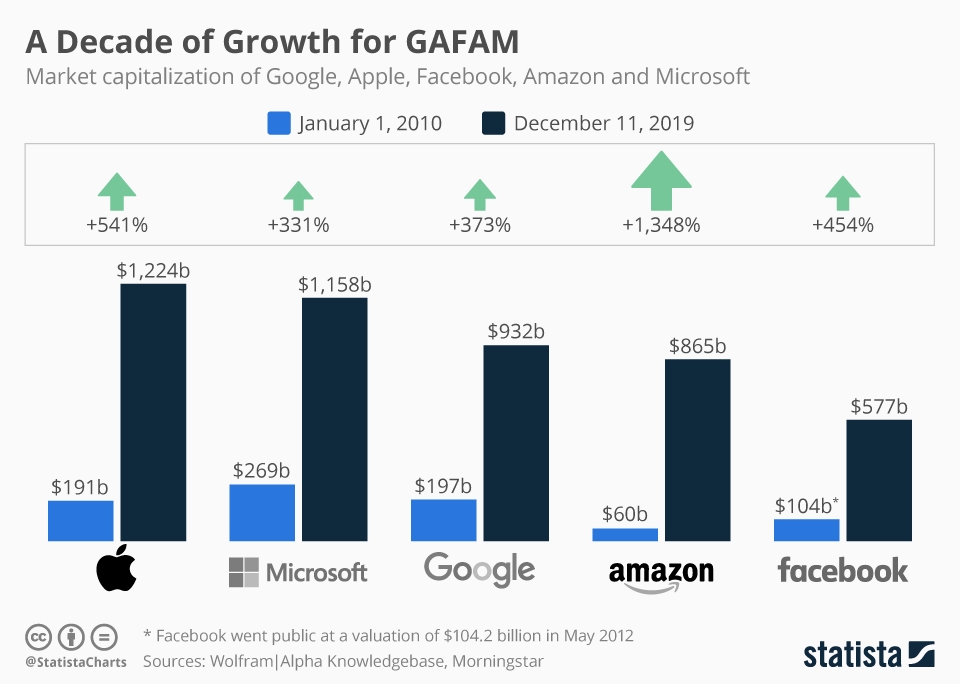

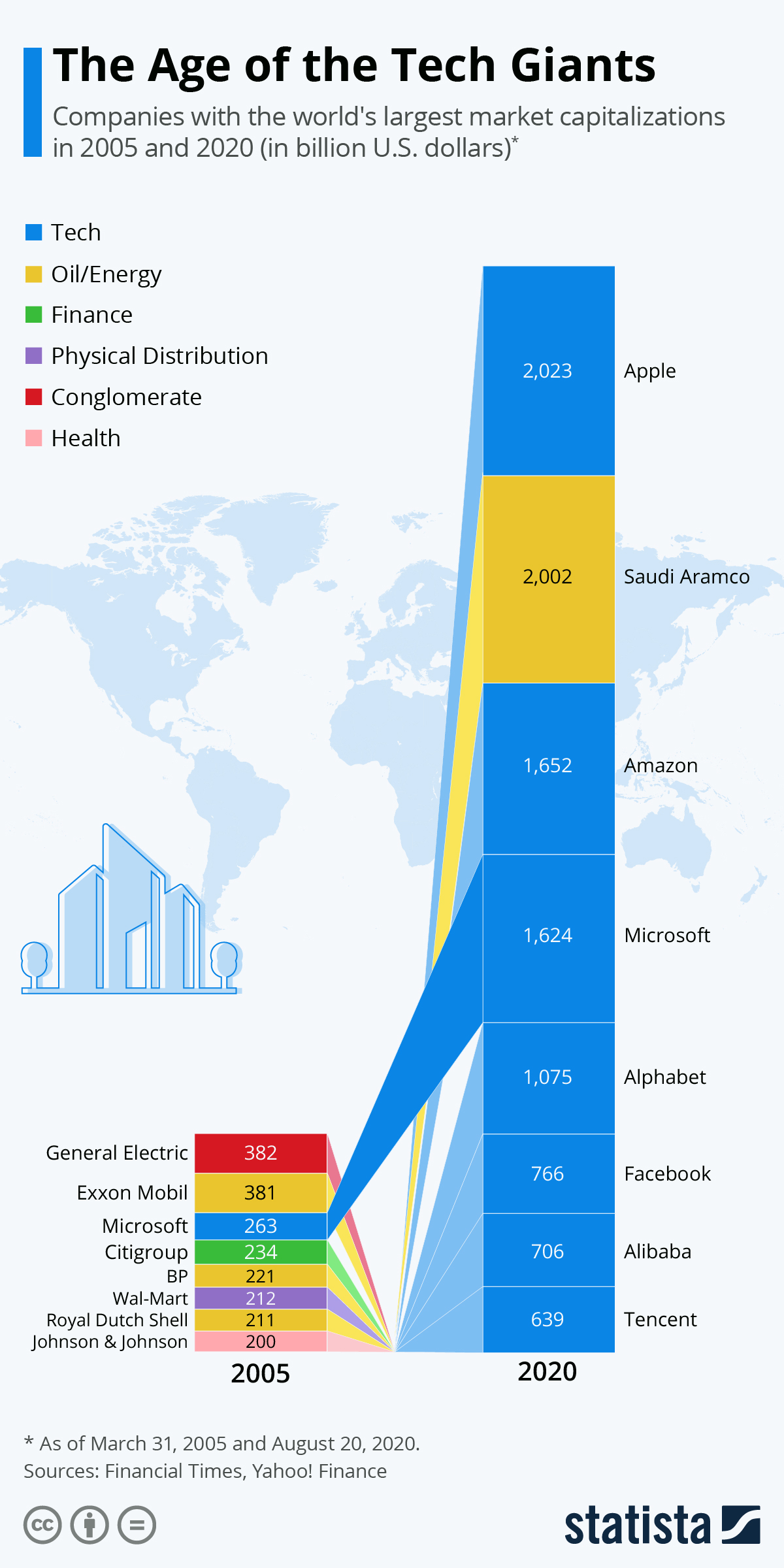

When looking at America’s 8 largest companies, a LOT has changed in 15 years. Back in 2005 the most valuable company was GE. The list was dominated by oil & gas companies; ExxonMobil, BP, Royal Dutch Shell. The biggest bank (Citi) and biggest retailer (Walmart) and 1 pharma company (J&J.) There was only 1 tech company on the list (Microsoft.)

But the world has changed, and that has impacted these companies dramatically. Most had GREAT pasts, but they did not adapt to a changing world. GE’s market cap has fallen 75% as it failed to keep up with trends. Oil companies failed to move into renewables and other industries (like electric car production) and they’ve lost over HALF their value. Walmart is most noted for missing the e-commerce trend, the big banks were clobbered by the Great Recession and “big pharma” hasn’t produced a blockbuster for many years. All down significantly.

But, the value of the top 8 companies is MUCH higher than 15 years ago – 5X more. These losers were replaced by some very serious winners. From $2.1T in combined value, the top 8 are now worth $10.5T. But notably, only 1 company is still on that list – Microsoft – which is up 620%!

The list is now dominated by 7 technology companies.

And for good reason – they all followed trends. Apple, Amazon, Microsoft, Alphabet (Google,) Facebook, Alibaba and Tencent all built their strategies around developing solutions for people to follow the major trends of being mobile, operating asynchronously, supporting gig work and adding artificial intelligence (AI) to their customers. By refusing to rest on past laurels they have become the mega-giants of today. (Hartung, “Thrive to the Future – The 4 Top Trends for 2021 and Beyond)

That these companies would overtake old leaders was not a foregone conclusion – nor an obvious one to most people. Not only were the previous giants big, they had incredible reputations and extremely strong management teams. And these tech companies were not without problems.

That these companies would overtake old leaders was not a foregone conclusion – nor an obvious one to most people. Not only were the previous giants big, they had incredible reputations and extremely strong management teams. And these tech companies were not without problems.

- Apple almost went bankrupt just a few years prior to 2005, trying to be the “Mac” company. But Apple built one innovation after another helping people meet the emerging big trends – until it became the most valuable company on the planet (10 yr value increase 540%)

- Microsoft was locked in to its Windows/Office domination and seemed unable (or unwilling) to acknowledge the big trends and its value languished under a terribly myopic CEO (Ballmer.) Yet, new leadership was able to see the trends and moved radically to build out cloud services and support for alternative customer solutions that changed the company and its fortunes (10 year value increase 330%)

- Amazon was a former book seller turned general merchandiser. But Amazon started applying technology to understand its customers and help them be better shoppers, using AI to make them the leader in all things e-commerce. Simultaneously Amazon built the worlds largest and most secure cloud services business (AWS) helping support all major trends (10 year value increase 1,350%)

- Google was a search engine, with an unclear business model. But Google went to unexpected lengths to make ALL forms of information digital, and accessible, and searchable. And it monetized that digitization in ways far beyond anyone expected leading to the end of newspapers and many other publishers (10 year value increase 370%)

- Facebook was considered a fad for young people. Most business leaders thought Facebook’s users would disappear, and its young leaders would learn there was no revenue in attracting eyeballs (just as News Corps learned and shut down MySpace.) But Facebook built out the trend for social contact in a mobile, asynchronous smart way creating an entirely new business market called “social media.” Facebook looked at trends in how people connected, making brilliant acquisitions early of Instagram and WhatsApp that allowed Facebook family of products to become the #1 use of the internet (10 year value increase 450%)

Key lessons?

First, the world is growing and leading businesses will grow. If you’re not growing, you’re dying. Just like GE and Exxon. Second, never plan from past success, but instead plan for the future. You don’t grow value by being operationally excellent, because the world is forever changing and it will make your past business less valuable even if you do run it well. Third, make sure your plans are all built on trends. Let trends be the wind in your sales, or the current under your boat, or whatever analogy you like – just be sure you’re using TRENDS to drive you business planning, product development and solutions generation. Customers buy trends and help for them to achieve the future.

Do you know your Value Proposition? Can you clearly state that Value Proposition without any linkage to your Value Delivery System? If not, you better get on that pretty fast. Otherwise, you’re very likely to end up like encyclopedias and newspaper companies. Or you’ll develop a neat technology that’s the next Segway. It’s always know your customer and their needs first, then create the solution. Don’t be a solution looking for an application. Hopefully Uber and Aurora will both now start heading in the right directions.

Did you see the trends, and were you expecting the changes that would happen to your demand? It IS possible to use trends to make good forecasts, and prepare for big market shifts. If you don’t have time to do it, perhaps you should contact us, Spark Partners. We track hundreds of trends, and are experts at developing scenarios applied to your business to help you make better decisions.

TRENDS MATTER. If you align with trends your business can do GREAT! Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business. Click for Assessment info. Or, to keep up on trends, subscribe to our weekly podcasts and posts on trends and how they will affect the world of business at www.SparkPartners.com

Give us a call or send an email. Adam@sparkpartners.com 847-331-6384

by Adam Hartung | Jun 20, 2018 | Boards of Directors, Growth Stall, Investing, Manufacturing, Strategy

An American epoch has ended. General Electric was part of the first ever Dow Jones Index in 1896. When the Dow Jones Industrial Average was formed in 1907 GE was a participant. GE has been the only company to remain on the index. All other original companies long ago completely disappeared.

GE did so well because its leadership had been able to constantly change the company to keep it relevant, and growing. During the century prior to hiring Jeff Immelt as CEO GE went from light bulbs to generating electricity and making all kinds of electrical infrastructure equipment, electric locomotives, mainframe computers, medical equipment, computer services, financial services, entertainment…. The list is very long.

Although not all GE CEOs were great, the Board was able to place CEOs in office who could sense market shifts and make good decisions. GE leadership thoughtfully analyzed markets, and made investment decisions to sell businesses that were not growing. And they made investment decisions to invest in trends which created growth. One of the best of these was Jack Welch, who developed the nickname “Neutron Jack” for his willingness to jettison businesses that were not growing and leading their industry, while willingly investing in entirely new growth markets where trends showed high rates of return like financial services and entertainment – wildly “non-industrial” markets.

But CEO Immelt was completely tone-deaf to the outside world. He was wholly unable to understand how to lead a team that could make good investments. Instead under Immelt’s leadership GE over-invested in historical products where they were losing advantage but trying to “keep up.” Selling businesses that were growing but faced stiff competition, rather than investing in growth. And refusing to invest in new external growth opportunities that could keep revenues increasing – and drive a higher GE market capitalization.

All the way back in 2009 I pointed out that GE was in a Growth Stall, and had only a 7% chance of consistently growing at 2%. I warned investors. At the time I said GE had to go all-out on a growth strategy, or things would turn ugly. But a lot of investors, employees – and apparently the Board of Directors – were ready to blame the Growth Stall on the economy. And blame it on Welch, who had been gone for 8 years. And say GE was lucky Immelt saved the company from bankruptcy with a loan from Warren Buffett’s Berkshire Hathaway.

Say what? Saved the company? Why did Immelt, and the Board, let GE get into such terrible shape? It was time to replace the CEO, not double down on his failed strategy.

Six years ago, May, 2012, I published in Forbes “5 CEOs that Should Have Already Been Fired.” At the time I said Immelt was the 4th worst CEO in America. I cited the 2009 column, and pointed out things really weren’t any better in 2012 than in 2009. That column had well over 1million reads. There was no way GE’s board was not aware of the column, and the realization that Immelt was a horrible CEO.

The Board of #3 (Walmart) fired Mike Duke. And the Board of #1 (Microsoft) fired Steve Ballmer. There is no real board at #2 Sears (which will file bankruptcy soon enough) because the CEO is also the largest shareholder (via his hedge fund) and he controls all board decisions. He should have fired himself, but had too much ego. But the board of GE – well it did nothing. Even though GE almost went bankrupt under Immelt, and its value was being destroyed quarter after quarter it left him in place.

I revisited the performance of these five CEOs and their companies in August, 2014 and reminded hundreds of thousands of readers – which I’m sure included GE’s Board of Directors – that company revenues had declined every year since 2009. And this string of failures had caused the company’s value to decline by 2/3. Yet, the board did nothing to replace this horrific CEO.

By March, 2017 I was so exasperated I finally titled my column “GE Needs a New Strategy and a New CEO.” Again, I detailed all the things that went wrong. It took 7 more months before the Board pushed Immelt out. But the new CEO failed to offer a better strategy, continuing to promote the notion of selling businesses to raise cash to “fix” the broken businesses – without identifying any growth strategy at all.

The only thing that can “fix” GE – save it from being dismembered and sold off – is a growth strategy. I offered how the new CEO could undertake this effort in October, 2017. But the Board, still wholly incompetent, still isn’t listening. Nobody should be surprised that GE is now removed from the Dow, and the new CEO is clearly without a clue how to find a path back to relevancy.

Too bad for investors, employees, suppliers, customers and the communities where the GE businesses reside. This didn’t have to happen. But due to an incompetent Board of Directors, which did nothing to properly govern an incompetent CEO, it did. And there’s little doubt it won’t be long before GE meets the same end as DuPont.

by Adam Hartung | Aug 29, 2014 | Current Affairs, In the Whirlpool, Leadership

It’s Labor Day, and a time when we naturally think about our jobs.

When it comes to jobs creation, no role is more critical than the CEO. No company will enter into a growth phase, selling more product and expanding employment, unless the CEO agrees. Likewise, no company will shrink, incurring job losses due to layoffs and mass firings, unless the CEO agrees. Both decisions lay at the foot of the CEO, and it is his/her skill that determines whether a company adds jobs, or deletes them.

Over 2 years ago (5 May, 2012) I published “The 5 CEOs Who Should Be Fired.” Not surprisingly, since then employment at all 5 of these companies has lagged economic growth, and in all but one case employment has shrunk. Yet, 3 of these CEOs remain in their jobs – despite lackluster (and in some cases dismal) performance. And all 5 companies are facing significant struggles, if not imminent failure.

#5 – John Chambers at Cisco

In 2012 it was clear that the market shift to public networks and cloud computing was forever changing the use of network equipment which had made Cisco a modern growth story under long-term CEO Chambers. Yet, since that time there has been no clear improvement in Cisco’s fortunes. Despite 2 controversial reorganizations, and 3 rounds of layoffs, Cisco is no better positioned today to grow than it was before.

Increasingly, CEO Chambers’ actions reorganizations and layoffs look like so many machinations to preserve the company’s legacy rather than a clear vision of where the company will grow next. Employee morale has declined, sales growth has lagged and although the stock has rebounded from 2012 lows, it is still at least 10% short of 2010 highs – even as the S&P hits record highs. While his tenure began with a tremendous growth story, today Cisco is at the doorstep of losing relevancy as excitement turns to cloud service providers like Amazon. And the decline in jobs at Cisco is just one sign of the need for new leadership.

#4 Jeff Immelt at General Electric

When CEO Immelt took over for Jack Welch he had some tough shoes to fill. Jack Welch’s tenure marked an explosion in value creation for the last remaining original Dow Jones Industrials component company. Revenues had grown every year, usually in double digits; profits soared, employment grew tremendously and both suppliers and investors gained as the company grew.

But that all stalled under Immelt. GE has failed to develop even one large new market, or position itself as the kind of leading company it was under Welch. Revenues exceeded $150B in 2009 and 2010, yet have declined since. In 2013 revenues dropped to $142B from $145B in 2012. To maintain revenues the company has been forced to continue selling businesses and downsizing employees every year. Total employment in 2014 is now less than in 2012.

Yet, Mr. Immelt continues to keep his job, even though the stock has been a laggard. From the near $60 it peaked at his arrival, the stock faltered. It regained to $40 in 2007, only to plunge to under $10 as the CEO’s over-reliance on financial services nearly bankrupted the once great manufacturing company in the banking crash of 2009. As the company ponders selling its long-standing trademark appliance business, the stock is still less than half its 2007 value, and under 1/3 its all time high. Where are the jobs? Not GE.

#3 Mike Duke at Wal-Mart

Mr. Duke has left Wal-Mart, but not in great shape. Since 2012 the company has been rocked by scandals, as it came to light the company was most likely bribing government officials in Mexico. Meanwhile, it has failed to defend its work practices at the National Labor Relations Board, and remains embattled regarding alleged discrimination of female employees. The company’s employment practices are regularly the target of unions and those supporting a higher minimum wage.

The company has had 6 consecutive quarters of declining traffic, as sales per store continue to lag – demonstrating leadership’s inability to excite people to shop in their stores as growth shifts to dollar stores. The stock was $70 in 2012, and is now only $75.60, even though the S&P 500 is up about 50%. So far smaller format city stores have not generated much attention, and the company remains far behind leader Amazon in on-line sales. WalMart increasingly looks like a giant trapped in its historical house, which is rapidly delapidating.

One big question to ask is who wants to work for WalMart? In 2013 the company threatened to close all its D.C. stores if the city council put through a higher minimum wage. Yet, since then major cities (San Francisco, Chicago, Los Angeles, Seattle, etc.) have either passed, or in the process of passing, local legislation increasing the minimum wage to anywhere from $12.50-$15.00/hour. But there seems no response from WalMart on how it will create profits as its costs rise.

#2 Ed Lampert at Sears

Nine straight quarterly losses. That about says it all for struggling Sears. Since the 5/2012 column the CEO has shuttered several stores, and sales continue dropping at those that remain open. Industry pundits now call Sears irrelevant, and the question is looming whether it will follow Radio Shack into oblivion soon.

CEO Lampert has singlehandedly destroyed the Sears brand, as well as that of its namesake products such as Kenmore and Diehard. He has laid off thousands of employees as he consolidated stores, yet he has been unable to capture any value from the unused real estate. Meanwhile, the leadership team has been the quintessential example of “a revolving door at headquarters.” From about $50/share 5/2012 (well off the peak of $190 in 2007,) the stock has dropped to the mid-$30s which is about where it was in its first year of Lampert leadership (2004.)

Without a doubt, Mr. Lampert has overtaken the reigns as the worst CEO of a large, publicly traded corporation in America (now that Steve Ballmer has resigned – see next item.)

#1 Steve Ballmer at Microsoft

In 2013 Steve Ballmer resigned as CEO of Microsoft. After being replaced, within a year he resigned as a Board member. Both events triggered analyst enthusiasm, and the stock rose.

However, Mr. Ballmer left Microsoft in far worse condition after his decade of leadership. Microsoft missed the market shift to mobile, over-investing in Windows 8 to shore up PC sales and buying Nokia at a premium to try and catch the market. Unfortunately Windows 8 has not been a success, especially in mobile where it has less than 5% share. Surface tablets were written down, and now console sales are declining as gamers go mobile.

As a result the new CEO has been forced to make layoffs in all divisions – most substantially in the mobile handset (formerly Nokia) business – since I positioned Mr. Ballmer as America’s worst CEO in 2012. Job growth appears highly unlikely at Microsoft.

“CEOs – From Makers to Takers”

Forbes colleague Steve Denning has written an excellent column on the transformation of CEOs from those who make businesses, to those who take from businesses. Far too many CEOs focus on personal net worth building, making enormous compensation regardless of company performance. Money is spent on inflated pay, stock buybacks and managing short-term earnings to maximize bonuses. Too often immediate cost savings, such as from outsourcing, drive bad long-term decisions.

CEOs are the ones who determine how our collective national resources are invested. The private economy, which they control, is vastly larger than any spending by the government. Harvard professor William Lazonick details how between 2003 and 2012 CEOs gave back 54% of all earnings in share buybacks (to drive up stock prices short term) and handed out another 37% in dividends. Investors may have gained, but it’s hard to create jobs (and for a nation to prosper) when only 9% of all earnings for a decade go into building new businesses!

There are great CEOs out there. Steve Jobs and his replacement Tim Cook increased revenues and employment dramatically at Apple. Jeff Bezos made Amazon into an enviable growth machine, producing revenues and jobs. These leaders are focused on doing what it takes to grow their companies, and as a result the jobs in America.

It’s just too bad the 5 fellows profiled above have done more to destroy value than create it.

by Adam Hartung | May 12, 2012 | Current Affairs, Defend & Extend, In the Swamp, In the Whirlpool, Leadership, Web/Tech

This has been quite the week for CEO mistakes. First was all the hubbub about Scott Thompson, CEO of Yahoo, inflating his resume to include a computer science degree he did not actually receive. According to Mr. Thompson someone at a recruiting firm added that degree claim in 2005, he didn't know it and he's never read his bio since. A simple oversight, if you can believe he hasn't once read his bio in 7 years, and he didn't think it was ever important to correct someone who introduced him or mentioned it. OOPS – the easy answer for someone making several million dollars per year, and trying to guide a very troubled company from the brink of failure. Hopefully he is more persistent about checking company facts.

But luckily for him, his errors were trumped on Thursday when Jamie Dimon, CEO of J.P.MorganChase notified the world that the bank's hedging operation messed up and lost $2B!! OOPS! According to Mr. Dimon this is really no big deal. Which reminded me of the apocryphal Senator Everett Dirksen statement "a billion here, a billion there and pretty soon it all adds up to real money!"

Interesting "little" mistake from a guy who paid himself some $50M a few years ago, and benefitted greatly from the government TARP program. He said this would be "fodder for pundits," as if we all should simply overlook losing $2B? He also said this was "unfortunate timing." As if there's a good time to lose $2B?

But neither of these problems will likely result in the CEOs losing their jobs. As obviously damaging as both mistakes are, which would naturally have caused us mere employees to instantly lose our jobs – and potentially be prosecuted – CEOs are a rare breed who are allowed wide lattitude in their behavior. These are "one off" events that gain a lot of attention, but the media will have forgotten within a few days, and everyone else within a few months.

By comparison, there are at least 5 CEOs that make these 2 mistakes appear pretty small. For these 5, frequently honored for their position, control of resources and personal wealth, they are doing horrific damage to their companies, hurting investors, employees, suppliers and the communities that rely on their organizations. They should have been fired long before this week.

#5 – John Chambers, Cisco Systems. Mr. Chambers is the longest serving CEO on this list, having led Cisco since 1995 and championed much of its rapid growth as corporations around the world began installing networks. Cisco's stock reached $70/share in 2001. But since then a combination of recessions that cut corporate IT budgets and a market shift to cloud computing has left Cisco scrambling for a strategy, and growth.

Mr. Chambers appears to have been great at operating Cisco as long as he was in a growth market. But since customers turned to cloud computing and greater use of mobile telephony networks Cisco has been unable to innovate, launch and grow new markets for cloud storage, services or applications. Mr. Chambers has reorganized the company 3 times – but it has been much like rearranging the deck chairs on the Titanic. Lots of confusion, but no improvement in results.

Between 2001 and 2007 the stock lost half its value, falling to $35. Continuing its slide, since 2007 the stock has halved again, now trading around $17. And there is no sign of new life for Cisco – as each earnings call reinforces a company lacking a strategy in a shifting market. If ever there was a need for replacing a stayed-in-the-job too long CEO it would be Cisco.

#4 – Jeffrey Immelt, General Electric (GE). GE has only had 9 CEOs in its 100+ year life. But this last one has been a doozy. After more than a decade of rapid growth in revenue, profits and valuation under the disruptive "neutron" Jack Welch, GE stock reached $60 in 2000. Which turns out to have been the peak, as GE's value has gone nowhere but down since Mr. Immelt took the top job.

GE was once known for entering and changing markets, unafraid to disrupt how the market performed with innovation in products, supply chain and operations. There was no market too distant, or too locked-in for GE to not find a way to change to its advantage – and profit. But what was the last market we saw GE develop? What has Mr. Immelt, in his decade at the top of GE, done to keep GE as one of the world's most innovative, high growth companies? He has steered the ship away from trouble, but it's only gone in circles as it's used up fuel.

From that high in 2001, GE fell to a low of $8 in 2009 as the financial crisis revealed that under Mr. Immelt GE had largely transitioned from a manufacturing and products company into a financial house. He had taken what was then the easy road to managing money, rather than managing a products and services company. Saved from bankruptcy by a lucrative Berkshire Hathaway, GE lived on. But it's stock is still only $19, down 2/3 from when Mr. Immelt took the CEO position.

"Stewardship" is insufficient leadership in 2012. Today markets shift rapidly, incur intensive global competition and require constant innovation. Mr. Immelt has no vision to propel GE's growth, and should have been gone by 2010, rather than allowed to muddle along with middling performance.

#3 – Mike Duke, WalMart. Mr. Duke has been CEO since 2009, but prior to that he was head of WalMart International. We now know Mr. Duke's business unit saw no problems with bribing foreign officials to grow its business. Just on the basis of knowing about illegal activity, not doing anything about it (and probably condoning and recommending more,) and then trying to change U.S. law to diminish the legal repurcussions, Mr. Duke should have long ago been fired.

It's clear that internally the company and its Board new Mr. Duke was willing to do anything to try and grow WalMart, even if unethical and potentially illegal. Recollections of Enron's Jeff Skilling, Worldcom's Bernie Ebbers and Hollinger's Conrdad Black should be in our heads. How far do we allow leaders to go before holding them accountable?

But worse, not even bribes will save WalMart as Mr. Duke follows a worn-out strategy unfit for competition in 2012. The entire retail market is shifting, with much lower cost on-line companies offering more selection at lower prices. And increasingly these companies are pioneering new technologies to accelerate on-line shopping with easy to use mobile devices, and new apps that make shopping, paying and tracking deliveries easier all the time. But WalMart has largely eschewed the on-line world as its CEO has doggedly sticks with WalMart doing more of the same. That pursuit has limited WalMart's growth, and margins, while the company files further behind competitively.

Unfortunately, WalMart peaked at about $70 in 2000, and has been flat ever since. Investors have gained nothing from this strategy, while employees often work for wages that leave them on the poverty line and without benefits. Scandals across all management layers are embarrassing. Communities find Walmart a mixed bag, initially lowering prices on some goods, but inevitably gutting the local retailers and leaving the community with no local market suppliers. WalMart needs an entirely new strategy to remain viable – and that will not come from Mr. Duke. He should have been gone long before the recent scandal, and surely now.

#2 Edward Lampert, Sears Holdings. OK, Mr. Lampert is the Chairman and not the CEO – but there is no doubt who calls the shots at Sears. And as Mr. Lampert has called the shots, nobody has gained.

Once the most critical force in retailing, since Mr. Lampert took over Sears has become wholly irrelevant. Hoping that Mr. Lampert could make hay out of the vast real estate holdings, and once glorious brands Craftsman, Kenmore and Diehard to turn around the struggling giant, the stock initially took off rising from $30 in 2004 to $170 in 2007 as Jim Cramer of "Mad Money" fame flogged the stock over and over on his rant-a-thon show. But when it was clear results were constantly worsening, as revenues and same-store-sales kept declining, the stock fell out of bed dropping into the $30s in 2009 and again in 2012.

Hope springs eternal in the micro-managing Mr. Lampert. Everyone knows of his personal fortune (#367 on Forbes list of billionaires.) But Mr. Lampert has destroyed Sears. The company may already be so far gone as to be unsavable. The stock price is based upon speculation of asset sales. Mr. Lampert had no idea, from the beginning, how to create value from Sears and he surely should have been gone many months ago as the hyped expectations demonstrably never happened.

#1 – Steve Ballmer, Microsoft. Without a doubt, Mr. Ballmer is the worst CEO of a large publicly traded American company. Not only has he singlehandedly steered Microsoft out of some of the fastest growing and most lucrative tech markets (mobile music, handsets and tablets) but in the process he has sacrificed the growth and profits of not only his company but "ecosystem" companies such as Dell, Hewlett Packard and even Nokia. The reach of his bad leadership has extended far beyond Microsoft when it comes to destroying shareholder value – and jobs.

Microsoft peaked at $60/share in 2000, just as Mr. Ballmer took the reigns. By 2002 it had fallen into the $20s, and has only rarely made it back to its current low $30s value. And no wonder, since execution of new rollouts were constantly delayed, and ended up with products so lacking in any enhanced value that they left customers scrambling to find ways to avoid upgrades. By Mr. Ballmer's own admission Vista had over 200 man-years too much cost, and its launch still, years late, has users avoiding upgrades. Microsoft 7 and Office 2012 did nothing to excite tech users, in corporations or at home, as Apple took the leadership position in personal technology.

So today Microsoft, after dumping Zune, dumping its tablet, dumping Windows CE and other mobile products, is still the same company Mr. Ballmer took control over a decade ago. Microsoft is PC company, nothing more, as demand for PCs shifts to mobile. Years late to market, he has bet the company on Windows 8 – as well as the future of Dell, HP, Nokia and others. An insane bet for any CEO – and one that would have been avoided entirely had the Microsoft Board replaced Mr. Ballmer years ago with a CEO that understands the fast pace of technology shifts and would have kept Microsoft current with market trends.

Although he's #19 on Forbes list of billionaires, Mr. Ballmer should not be allowed to take such incredible risks with investor money and employee jobs. Best he be retired to enjoy his fortune rather than deprive investors and employees of building theirs.

There were a lot of notable CEO changes already in 2012. Research in Motion, Best Buy and American Airlines are just three examples. But the 5 CEOs in this column are well on the way to leading their companies into the kind of problems those 3 have already discovered. Hopefully the Boards will start to pay closer attention, and take action before things worsen.

by Adam Hartung | Dec 17, 2010 | Current Affairs, Defend & Extend, In the Rapids, In the Swamp, Leadership, Web/Tech

Summary:

- Many people think it is OK for large companies to grow slowly

- Many people admire caretaker CEOs

- In dynamic markets, low-growth companies fail

- It is harder to generate $1B of new revenue, than grow a $100B company by $10B

- Large companies have vastly more resources, but they squander them badly

- We allow large company CEOs too much room for mediocrity and failure

- Good CEOs never lose a growth agenda, and everyone wins!

“I may just be your little rent collector Mr. Potter, but that George Bailey is making quite a bit happen in that new development of his. If he keeps going it may just be time for this smart young man to go asking George Bailey for a job.” From “It’s a Wonderful Life“ an employee of the biggest employer in mythical Beford Falls talks about the growth of a smaller competitor.

My last post gathered a lot of reads, and a lot of feedback. Most of it centered on how GE should not be compared to Facebook, largely because of size differences, and therefore how it was ridiculous to compare Jeff Immelt with Mark Zuckerberg. Many readers felt that I overstated the good qualities of Mr. Zuckerberg, while not giving Mr. Immelt enough credit for his skills managing “lower growth businesses” in a “tough economy.” Many viewed Mr. Immelt’s task as incomparably more difficult than that of managing a high growth, smaller tech company from nothing to several billion revenue in a few years. One frequent claim was that it is enough to maintain revenue in a giant company, growth was less important.

Why do so many people give the CEOs of big companies a break? Given that they make huge salaries and bonuses, have fantastic perquesites (private jets, etc.), phenominal benefits and pensions, and receive remarkable payouts whether they succeed or fail I would think we’d have very high standards for these leaders – and be incensed when their performance is sub-par.

Facebook started with almost no resources (as did Twitter and Groupon). Most leaders of start-ups fail. It is remarkably difficult to marshal resources – both enough of them and productively – to grow a company at double digit rates, produce higher revenue, generate cash flow (or loans) and keep employees happy. Growing to a billion dollars revenue from nothing is inexplicably harder than adding $10B to a $100B company. Compared to Facebook, GE has massive resources. Mr. Immelt entered the millenium with huge cash flow, huge revenues, and an army of very smart employees. Mr. Zuckerberg had to come out of the blocks from a standing start and create ALL his company’s momentum, while comparatively Mr. Immelt took on his job riding a bullet out of a gun! GE had huge momentum, a low cost of capital, and enough resources to do anything it wanted.

Yet somehow we should think that we don’t have as high expectations from Mr. Immelt as we do Mr. Zuckerberg? That would seem, at the least, distorted.

In business school I read the story of how American steel manufacturers were eclipsed by the Japanese. Ending WWII America had almost all the steel capacity. Manufacturers raked in the profits. Japanese and German companies that were destroyed had to rebuild, which they progressively did with more efficient assets. By the 1960s American companies were no longer competitive. Were we to believe that having their industrial capacity destroyed somehow was a good thing for the foreign competitors? That if you want to improve your competitiveness (say in autos) you should drop a nuclear bomb on the facilities (some may like that idea – but not many who live in Detroit I dare say.) In reality the American leaders simply refused to invest in new technologies and growth markets, allowing competitors to end-run them. The American leaders were busy acting as caretakers, and bragging about their success, instead of paying attention to market shifts and keeping their companies successful!

Big companies, like GE, are highly advantaged. They not only have brand, and market position, but cash, assets, employees and vendors in position to help them be even more successful! A smart CEO uses those resources to take the company into growth markets where it can grow revenues, and profits, faster than the marketplace. For example Steve Jobs at Apple, and Eric Schmidt at Google have found new markets, revenues and cash flow beyond their original “core” markets. That’s what Mr. Welch did as predecessor to Mr. Immelt. He didn’t so much take advantage of a growth economy as help create it! Unfortunately, far too many large company CEOs squander their resources on low rate of return projects, trying to defend their existing business rather than push forward.

Most big companies over-invest in known markets, or technologies, that have low growth rates, rather than invest in growth markets, or technologies they don’t know as well. Think about how Motorola invented the smart phone technology, but kept investing in traditional cellular phones. Or Sears, the inventor of “at home shopping” with catalogues closed that division to chase real-estate based retail, allowing Amazon to take industry leadership and market growth. Circuit City ended up investing in its approach to retail until it went bankrupt in 2010 – even though it was a darling of “Good to Great.” Or Microsoft, which launched a tablet and a smart phone, under leader Ballmer re-focused on its “core” operating system and office automation markets letting Apple grab the growth markets with R&D investments 1/8th of Microsoft’s. These management decisions are not something we should accept as “natural.” Leaders of big companies have the ability to maintain, even accelerate, growth. Or not.

Why give leaders in big companies a break just because their historical markets have slower growth? Singer’s leadership realized women weren’t going to sew at home much longer, and converted the company into a defense contractor to maintain growth. Netflix converted from a physical product company (DVDs) into a streaming download company in order to remain vital and grow while Blockbuster filed bankruptcy. Apple transformed from a PC company into a multi-media company to create explosive growth generating enough cash to buy Dell outright – although who wants a distributor of yesterday’s technology (remember Circuit City.) Any company can move forward to be anything it wants to be. Excusing low growth due to industry, or economic, weakness merely gives the incumbent a pass. Good CEOs don’t sit in a foxhole waiting to see if they survive, blaming a tough battleground, they develop strategies to change the battle and win, taking on new ground while the competition is making excuses.

GM was the world’s largest auto company when it went broke. So how did size benefit GM? In the 1980s Roger Smith moved GM into aerospace by acquiring Hughes electronics, and IT services by purchasing EDS – two remarkable growth businesses. He “greenfielded” a new approach to auto manufucturing by opening the wildly successful Saturn division. For his foresight, he was widely chastised. But “caretaker” leadership sold off Hughes and EDS, then forced Saturn to “conform” to GM practices gutting the upstart division of its value. Where one leader recognized the need to advance the company, followers drove GM to bankruptcy by selling out of growth businesses to re-invest in “core” but highly unprofitable traditional auto manufacturing and sales. Meanwhile, as the giant failed, much smaller Kia, Tesla and Tata are reshaping the auto industry in ways most likely to make sure GM’s comeback is short-lived.

CEOs of big companies are paid a lot of money. A LOT of money. Much more than Mr. Zuckerberg at Facebook, or the leaders of Groupon and Netflix (for example). So shouldn’t we expect more from them? (Marketwatch.com “Top CEO Bonuses of 2010“) They control vast piles of cash and other resources, shouldn’t we expect them to be aggressively investing those resources in order to keep their companies growing, rather than blaming tax strategies for their unwillingness to invest? (Wall Street Journal “Obama Pushes CEOs on Job Creation“) It’s precisely because they are so large that we should have high expectations of big companies investing in growth – because they can afford to, and need to!

At the end of the day, everyone wins when CEOs push for growth. Investors obtain higher valuation (Apple is worth more than Microsoft, and almost more than 10x larger Exxon!,) employees receive more pay (see Google’s recent 10% across the board pay raise,) employees have more advancement opportunities as well as personal growth, suppliers have the opportunity to earn profits and bring forward new innovation – creating more jobs and their own growth – rather than constantly cutting price. Answering the Economist in “Why Do Firms Exist?” it is to deliver to people what they want. When companies do that, they grow. When they start looking inward, and try being caretakers of historical assets, products and markets then their value declines.

Can Mr. Zuckerberg run GE? Probably. I’d sure rather have him at the helm of GM, Chrysler, Kraft, Sara Lee, Motorola, AT&T or any of a host of other large companies that are going nowhere the caretaker CEOs currently making excuses for their lousy performance. Think what the world would be like if the aggressive leaders in those smaller companies were in such positions? Why, it might just be like having all of American business run the way Steve Jobs, Jeff Bezos and John Chambers have led their big companies. I struggle to see how that would be a bad thing.