by Adam Hartung | Dec 7, 2019 | Entertainment, Innovation, Marketing, Strategy, Television, Trends

Seven years ago (12 December, 2012) I said it was “The Day TV Died.” There were a LOT of skeptics. At the time, TV was by far still the dominant medium. But the trends were absolutely clear – ad revenues were quickly moving toward on-line opportunities. Print was already well into the grave, and radio was sputtering along with no growth at all. Eyeball momentum had shifted on-line, and thus ads moved on-line, and it was obvious that programming dollars would soon follow – meaning that TV programming was already in Stage 4 termination.

Trends and Tech drove Netflix growth

Meanwhile, Netflix and its brethren were poised to have a fabulous, furious growth. These same trends led me to a full-throated pitch to buy Netflix nine years ago (Nov. 2010.) After Netflix made the decision to raise prices for DVD distribution in order to push people toward streaming the stock crashed, but trends indicated that customer preferences would lead Netflix to be the content winner so despite widespread despair, I called for people to buy the stock in Oct. 2011. In Jan. 2012, I made Netflix one of my top 4 picks for the year. So by Jan. 2013, I was making it clear that TV was has-been, and Netflix was the company to own.

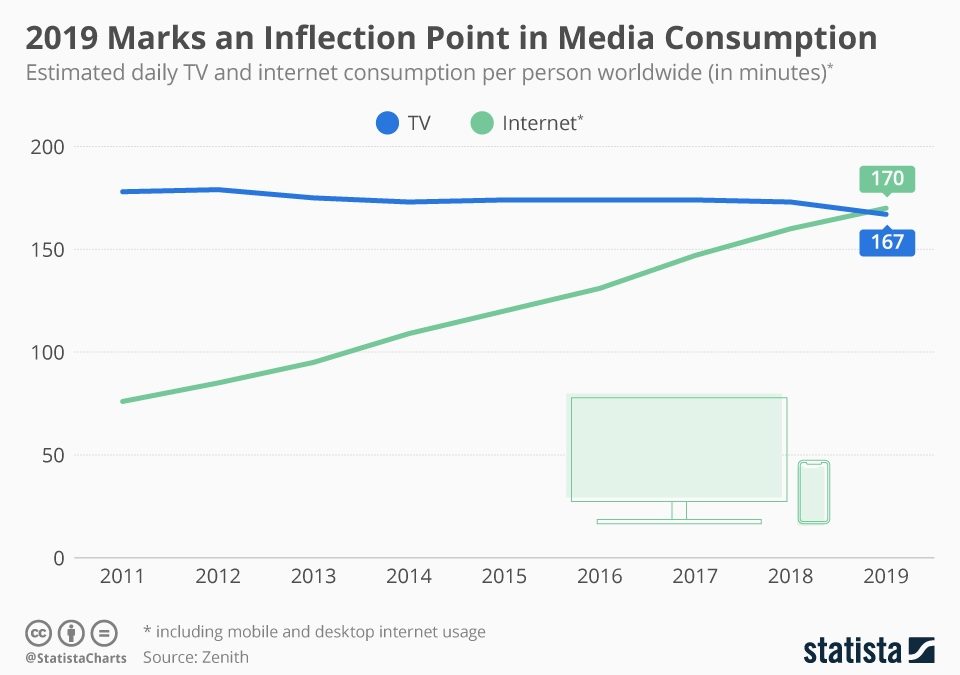

Now, Statista has produced the numbers showing that in 2019 internet media consumption exceeded TV consumption – for the first time ever. And this trend will not stop. It was wholly predictable years ago – and the trends all say this will only accelerate. Where once the competition for entertainment was Netflix, now there is Amazon Prime, Disney+, Comcast Peacock, AT&T HBO Max and Apple TV+. The traditional networks simply don’t have a chance.

Impact of Trends

These trends are having an enormous impact on how we behave, how advertisers behave, what technology we buy, what entertainment we watch, how we use other technology like social media, how we absorb news — and more. So the question is, did you see the trends 7,8,9 years ago? Have you adjusted your strategy? Are you sure where trends are headed, and are you prepared for the future? Will you be a winner as the world changes – in a pretty predictable way – or will you lose out and say “you know, way back when……”

by Adam Hartung | Jul 14, 2017 | In the Rapids, Innovation, Marketing

Amazon just had another record Prime Day, with sales up 60%. And the #1 product sold was Amazon’s Echo Dot speaker. At $34.99 it surpassed last year’s unit sales by seven-fold. And the traditional Echo speaker, marked down 50% to $90, broke all previous sales records.

Amazon just took a commanding lead in the voice assistant platform market

These Echo sales most likely sealed Amazon’s long-term leadership in the war to be the #1 voice assistant. Amazon already has 70% market share in voice activated speakers, nearly 3 times #2 provider Google. And all other vendors in total barely have 5% share.

While it may seem like digital speakers are no big deal, speaker sales are analogous to iPhone sales when evaluating the emergence of smartphones and apps. The iPhone seemed like a small segment until it became clear smartphones were the new personal technology platform. Apple’s early lead allowed iOS to dominate the growth cycle, making the company intensely profitable.

Echo and Echo Dot aren’t just speakers, but interfaces to voice activated virtual assistants. For Echo the platform is Amazon’s Alexa. Alexa is to voice activated devices and applications what iOS was to Smartphones. By talking to Alexa customers are able to do many things, such as shopping, altering their thermostats, opening and closing doors, raising and lowering blinds, recording people in their homes — the list is endless. And as that list grows customers are buying more Alexa devices to gain greater productivity and enhanced lifestyle. Echos are entering more homes, and multiplying across rooms in these homes.

Do you remember when early iPhone ads touted “there’s an app for that?” That tagline told customers if they changed from a standard mobile phone to a smartphone there were a lot of advantages, measured by the number of available apps. Just like iOS apps gave an advantage to owning an iPhone, Alexa skills give an advantage to owning Echo products. In the last year the number of skills available for Alexa has exploded, growing from 135 to 15,000. Quite obviously developers are building on Alexa much faster than any other voice assistant.

By radically cutting the price of both Echo Dot and Echo, and promoting sales, Amazon is creating an installed base of units which encourages developers to write even more skills/apps.

The more Alexa devices are installed, the more likely developers will write additional skills for Alexa. As more devices lead to more skills, skills leads to more Alexa/Echo capability, which encourages more people to buy Alexa activated devices, which further encourages even more skills development. It’s a virtuous circle of goodness, all leading to more Amazon growth.

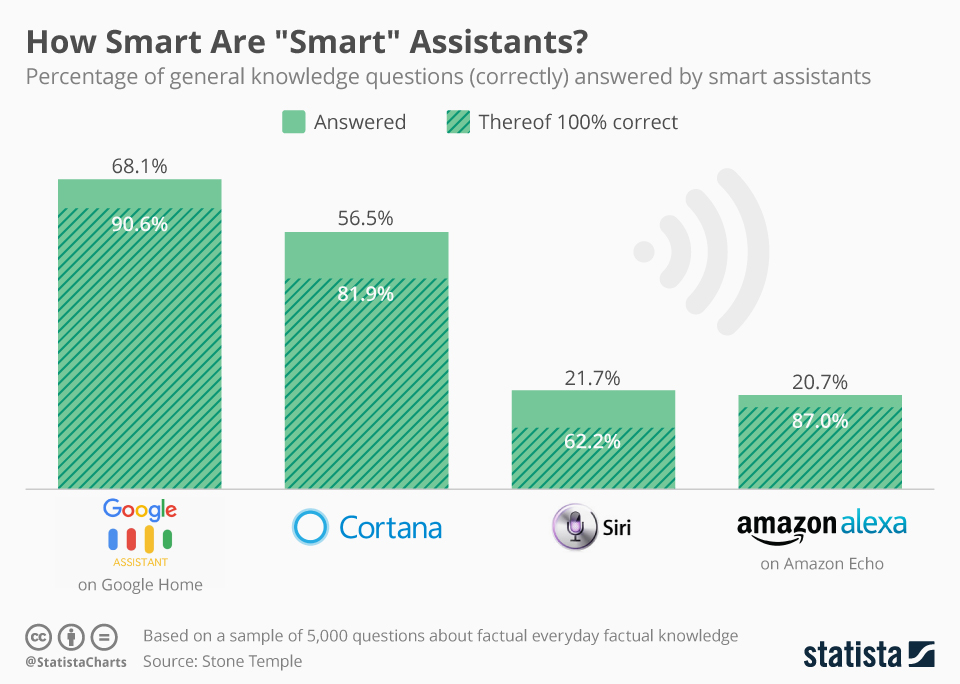

For marketers it is important to realize that success really doesn’t correlate with how “good” Alexa works. Google’s Assistant and Microsoft’s Cortana perform better at voice recognition and providing appropriate responses than Alexa and Siri. But there are relatively few (almost no) devices in the marketplace built with Assistant or Cortana as the interface. Developers need their skills/apps to be on platforms customers use. If customers are buying speakers, thermostats and televisions that are embedded with Alexa, then developers will write for Alexa. Even if it has shortcomings. It’s not the product quality that determines the winner, but rather the ability to create a base of users.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

This is a horrible problem for Google, #2 in this market, because Google does not have the retail clout to place millions of their speakers (and other devices) in the market. Google is not a device company, nor a powerful retailer of Android devices. The Android device makers need to profit from their devices, so they cannot afford to sell devices unprofitably in order to build an installed base for Google. And because Android’s platform is not applied consistently across device manufacturers, Google Assistant skills cannot be assured of operating on every Android phone. All of which makes the decision to build Google Assistant skills problematic for developers.

Can Apple Stop the Alexa juggernaut?

The game is not over. Apple would like customers to use Siri on their iPhones to accomplish what Amazon and Alexa do with Echo. Apple has an enormous iPhone base, and all have Siri embedded. Perhaps Apple can encourage developers to create Siri-integrated apps which will beat back the Amazon onslaught?

Today, Apple customers still cannot use Siri to control their Apple TV (Though as of August, 2017, it’s been improved.), or make payments with ApplePay, for example. Nor can iPhone users tell Siri to execute commands for remote systems which are controlled by apps, like unlocking doors, turning on appliances, shooting remote security video or placing an on-line order. Apple has a lot of devices, and apps, but so far Siri is not integrated in a way that allows voice activation like can be done with Alexa.

Additionally, as big as the iPhone installed base has become, when comparing markets the actual raw number of speakers could catch up with iPhones. Echo Dot is $35. The cheapest iPhone is the SE, at $399 (on the Apple site although available from Best Buy at $160.) And an iPhone 7 starts at $650. The huge untapped Apple markets, such as China and India, will find it a lot easier to purchase low cost speakers than iPhones, especially if their focus is to use some of those 15,000 skills. And because of the low pricing ($35 to $90) it is easy to buy multiple devices for multiple locations in one’s home or office.

Will we look back and call Echo a Disruptive Innovation?

Innovator’s Dilemma

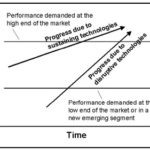

Recall the wisdom of Clayton Christensen‘s “Innovator’s Dilemma.” The incumbent keeps improving their product, hoping to maintain a capability lead over the competition. But eventually the incumbent far overshoots customer needs, developing a product that is overly enhanced. The disruptive innovator enters the market with a considerably “less good” product, but it meets customer needs at a much lower price. People buy the cheaper product to meet their limited goal, and bypass the more capable but more expensive early market leader.

Doesn’t this sound remarkably similar to the development of iPhones (now on version 8 and expected to sell at over $1,000) compared with a $35 speaker that is far less capable, but still does 15,000 interesting things?

The biggest loser in this new market is Microsoft

This week Microsoft announced another 1,500 layoffs in what has become an annual bloodletting ritual for the PC software giant. But even worse was the announcement that Microsoft would no longer support any version of Windows Phone OS version 8.1 or older – which is 80% of the Windows Phone market. Given that Microsoft has less than 2% market share, and that less than .4% of the installed smartphone base operates on Windows Phone, killing support for these phones will lead to sales declines. This action, along with gutting the internal developer team last year, clearly indicates Microsoft has given up on the phone business for good. This means that now Microsoft has no device platform for Cortana, Microsoft’s voice assistant, to use.

Microsoft ignored smartphones, allowing Apple’s iOS to become the early standard. Apple rapidly grew its installed base. Microsoft could not convince developers to write for Windows Phone because there weren’t enough devices in the market. Without a phone base, with tablet and hybrid sales flat to declining, and with PC sales in the gutter Cortana enters the market DOA (Dead On Arrival.) Even if it were the best voice assistant on the planet developers will not create skills for Cortana because there are no devices out there using Cortana as the interface.

So Microsoft completely missed yet another market. This time the market for voice activated devices in the smart phone, smart car or any other smart device in the IoT marketplace. It missed mobile, and now it has missed voice assist. As PC sales decline, Microsoft’s only hope is to somehow emerge a big winner in cloud storage and services (IaaS or Infrastructure as a Service) with Azure. But, Azure was a late-comer to the cloud market and is far behind Amazon’s AWS (Amazon Web Services.) Amazon has +40% market share, which is 40% more than the share of Microsoft, Google and IBM combined.

Build the base and developers will come…

by Adam Hartung | Apr 27, 2016 | Food and Drink, In the Rapids, In the Swamp, Retail, Software, Web/Tech

Growth fixes a multitude of sins. If you grow revenues enough (you don’t even need profits, as Amazon has proven) investors will look past a lot of things. With revenue growth high enough, companies can offer employees free meals and massages. Executives and senior managers can fly around in private jets. Companies can build colossal buildings as testaments to their brand, or pay to have thier names on public buildings. R&D budgets can soar, and product launches can fail. Acquisitions are made with no concerns for price. Bonuses can be huge. All is accepted if revenues grow enough.

Just look at Facebook. Today Facebook announced today that for the quarter ended March, 2016 revenues jumped to $5.4B from $3.5B a year ago. Net income tripled to $1.5B from $500M. And the company is basically making all its revenue – 82% – from 1 product, mobile ads. In the last few years Facebook paid enormous premiums to buy WhatsApp and Instagram – but who cares when revenues grow this fast.

Anticipating good news, Facebook’s stock was up a touch today. But once the news came out, after-hours traders pumped the stock to over $118//share, a new all time high. That’s a price/earnings (p/e) multiple of something like 84. With growth like that Facebook’s leadership can do anything it wants.

But, when revenues slide it can become a veritable poop puddle. As Apple found out.

Rumors had swirled that Apple was going to say sales were down. And the stock had struggled to make gains from lows earlier in 2016. When the company’s CEO announced Tuesday that sales were down 13% versus a year ago the stock cratered after-hours, and opened this morning down 10%. Breaking a streak of 51 straight quarters of revenue growth (since 2003) really sent investors fleeing. From trading around $105/share the last 4 days, Apple closed today at ~$97. $40B of equity value was wiped out in 1 day, and the stock trades at a p/e multiple of 10.

The new iPhone 6se outsold projections, iPads beat expectations. First year Apple Watch sales exceeded first year iPhone sales. Mac sales remain much stronger than any other PC manufacturer. Apple iBeacons and Apple Pay continue their march as major technologies in the IoT (Internet of Things) market. And Apple TV keeps growing. There are about 13M users of Apple’s iMusic. There are 1.5M apps on the iTunes store. And the installed base keeps the iTunes store growing. Share buybacks will grow, and the dividend was increased yet again. But, none of that mattered when people heard sales growth had stopped. Now many investors don’t think Apple’s leadership can do anything right.

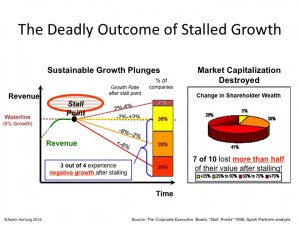

Yet, that was just one quarter. Many companies bounce back from a bad quarter. There is no statistical evidence that one bad quarter is predictive of the next. But we do know that if sales decline versus a year ago for 2 consecutive quarters that is a Growth Stall. And companies that hit a Growth Stall rarely (93% of the time) find a consistent growth path ever again. Regardless of the explanations, Growth Stalls are remarkable predictors of companies that are developing a gap between their offerings, and the marketplace.

Yet, that was just one quarter. Many companies bounce back from a bad quarter. There is no statistical evidence that one bad quarter is predictive of the next. But we do know that if sales decline versus a year ago for 2 consecutive quarters that is a Growth Stall. And companies that hit a Growth Stall rarely (93% of the time) find a consistent growth path ever again. Regardless of the explanations, Growth Stalls are remarkable predictors of companies that are developing a gap between their offerings, and the marketplace.

Which leads us to Chipotle. Chipotle announced that same store sales fell almost 30% in Q1, 2016. That was after a 15% decline in Q4, 2015. And profits turned to losses for the quarter. That is a growth stall. Chipotle shares were $750/share back in early October. Now they are $417 – a drop of over 44%.

Customer illnesses have pointed to a company that grew fast, but apparently didn’t have its act together for safe sourcing of local ingredients, and safe food handling by employees. What seemed like a tactical problem has plagued the company, as more customers became ill in March.

Whether that is all that’s wrong at Chipotle is less clear, however. There is a lot more competition in the fast casual segment than 2 years ago when Chipotle seemed unable to do anything wrong. And although the company stresses healthy food, the calorie count on most portions would add pounds to anyone other than an athlete or construction worker – not exactly in line with current trends toward dieting. What frequently looks like a single problem when a company’s sales dip often turns out to have multiple origins, and regaining growth is nearly always a lot more difficult than leadership expects.

Growth is magical. It allows companies to invest in new products and services, and buoy’s a stock’s value enhancing acquisition ability. It allows for experimentation into new markets, and discovering other growth avenues. But lack of growth is a vital predictor of future performance. Companies without growth find themselves cost cutting and taking actions which often cause valuations to decline.

Right now Facebook is in a wonderful position. Apple has investors rightly concerned. Will next quarter signal a return to growth, or a Growth Stall? And Chipotle has investors heading for the exits, as there is now ample reason to question whether the company will recover its luster of yore.

by Adam Hartung | Sep 19, 2013 | Current Affairs, In the Swamp, Innovation, Leadership, Television, Web/Tech

Apple announced the new iPhones recently. And mostly, nobody cared.

Remember when users waited anxiously for new products from Apple? Even the media became addicted to a new round of Apple products every few months. Apple announcements seemed a sure-fire way to excite folks with new possibilities for getting things done in a fast changing world.

But the new iPhones, and the underlying new iPhone software called iOS7, has almost nobody excited.

Instead of the product launches speaking for themselves, the CEO (Tim Cook) and his top product development lieutenants (Jony Ive and Craig Federighi) have been making the media rounds at BloombergBusinessWeek and USAToday telling us that Apple is still a really innovative place. Unfortunately, their words aren't that convincing. Not nearly as convincing as former product launches.

CEO Cook is trying to convince us that Apple's big loss of market share should not be troubling. iPhone owners still use their smartphones more than Android owners, and that's all we should care about. Unfortunately, Apple profits come from unit sales (and app sales) rather than minutes used. So the chronic share loss is quite concerning.

Especially since unit sales are now growing barely in single digits, and revenue growth quarter-over-quarter, which sailed through 2012 in the 50-75% range, have suddenly gone completely flat (less than 1% last quarter.) And margins have plunged from nearly 50% to about 35% – more like 2009 (and briefly in 2010) than what investors had grown accustomed to during Apple's great value rise. The numbers do not align with executive optimism.

For industry aficianados iOS7 is a big deal. Forbes Haydn Shaughnessy does a great job of laying out why Apple will benefit from giving its ecosystem of suppliers a new operating system on which to build enhanced features and functionality. Such product updates will keep many developers writing for the iOS devices, and keep the battle tight with Samsung and others using Google's Android OS while making it ever more difficult for Microsoft to gain Windows8 traction in mobile.

And that is good for Apple. It insures ongoing sales, and ongoing profits. In the slog-through-the-tech-trench-warfare Apple is continuing to bring new guns to the battle, making sure it doesn't get blown up.

But that isn't why Apple became the most valuable publicly traded company in America.

We became addicted to a company that brought us things which were great, even when we didn't know we wanted them – much less think we needed them. We were happy with CDs and Walkmen until we discovered much smaller, lighter iPods and 99cent iTunes. We were happy with our Blackberries until we learned the great benefits of apps, and all the things we could do with a simple smartphone. We were happy working on laptops until we discovered smaller, lighter tablets could accomplish almost everything we couldn't do on our iPhone, while keeping us 24×7 connected to the cloud (that we didn't even know or care about before,) allowing us to leave the laptop at the office.

Now we hear about upgrades. A better operating system (sort of sounds like Microsoft talking, to be honest.) Great for hard core techies, but what do users care? A better Siri; which we aren't yet sure we really like, or trust. A new fingerprint reader which may be better security, but leaves us wondering if it will have Siri-like problems actually working. New cheaper color cases – which don't matter at all unless you are trying to downgrade your product (sounds sort of like P&G trying to convince us that cheaper, less good "Basic" Bounty was an innovation.)

More (upgrades) Better (voice interface, camera capability, security) and Cheaper (plastic cases) is not innovation. It is defending and extending your past success. There's nothing wrong with that, but it doesn't excite us. And it doesn't make your brand something people can't live without. And, while it keeps the battle for sales going, it doesn't grow your margin, or dramatically grow your sales (it has declining marginal returns, in fact.)

And it won't get your stock price from $450-$475/share back to $700.

We all know what we want from Apple. We long for the days when the old CEO would have said "You like Google Glass? Look at this……. This will change the way you work forever!!"

We've been waiting for an Apple TV that let's us bypass clunky remote controls, rapidly find favorite shows and helps us avoid unwanted ads and clutter. But we've been getting a tease of Dick Tracy-esque smart watches.

From the world's #1 tech brand (in market cap – and probably user opinion) we want something disruptive! Something that changes the game on old companies we less than love like Comcast and DirecTV. Something that helps us get rid of annoying problems like expensive and bad electric service, or routers in our basements and bedrooms, or navigation devices in our cars, or thumb drives hooked up to our flat screen TVs —- or doctor visits. We want something Game Changing!

Apple's new CEO seems to be great at the Sustaining Innovation game. And that pretty much assures Apple of at least a few more years of nicely profitable sales. But it won't keep Apple on top of the tech, or market cap, heap. For that Apple needs to bring the market something big. We've waited 2 years, which is an eternity in tech and financial markets. If something doesn't happen soon, Apple investors deserve to be worried, and wary.

by Adam Hartung | Dec 10, 2012 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Lifecycle, Television

Remember when almost everyone read a daily newspaper?

Newspaper readership peaked around 2000. Since then printed media has declined, as readers shifted on-line. Magazines have folded, and newspapers have disappeared, quit printing, dramatically cut page numbers and even more dramatically cut staff.

Amazingly, almost no major print publisher prepared for this, even though the trend was becoming clear in the late 1990s.

Newspapers are no longer a viable business. While industry revenue grew for

almost 2 centuries, it collapsed in a mere decade.

Chart Source: BusinessInsider.com

This market shift created clear winners, and losers. On-line news sites like Marketwatch and HuffingtonPost were clear winners. Losers were traditional newspaper companies such as Tribune Corporation, Gannett, McClatchey, Dow Jones and even the New York Times Company. And investors in these companies either saw their values soar, or practically disintegrate.

In 2012 it is equally clear that television is on the brink of a major transition. Fewer people are content to have their entertainment programmed for them when they can program it themselves on-line. Even though the number of television channels has exploded with pervasive cable access, the time spent watching television is not growing. While simultaneously the amount of time people spend looking at mobile internet displays (tablets, smartphones and laptops) is growing at double digit rates.

Chart Source: Silicone Alley Insider Chart of the Day 12/5/12

It would be easy to act like newspaper defenders and pretend that television as we've known it will not change. But that would be, at best, naive. Just look around at broadband access, the use of mobile devices, the convenience of mobile and the number of people that don't even watch traditional TV any more (especially younger people) and the trend is clear. One-way preprogrammed advertising laden television is not a sustainable business.

So, now is the time to prepare. And change your business to align with impending new realities.

Losers, and winners, will be varied – and not entirely obvious. Firstly, a look at those trying to maintain the status quo, and likely to lose the most.

Giant consumer goods and retail companies benefitted from the domination of television. Only huge companies like P&G, Kraft, GM and Target could afford to lay out billions of dollars for television ads to build, and defend, a brand. But what advantage will they have when TV budgets no longer control brand building? They will become extremely vulnerable to more innovative companies that have better products and move on fast lifecycles. Their size, hierarchy and arcane business practices will lead to huge problems. Imagine a raft of new Hostess Brands experiences.

Even as the trends have started changing these companies have continued pumping billions into the traditional TV networks as they spend to defend their brand position. This has driven up the value of companies like CBS, Comcast (owns NBC) and Disney (owns ABC) over the last 3 years substantially. But don't expect that to last forever. Or even a few more years.

Just like newspaper ad spending fell off a cliff when it was clear the eyeballs were no longer there, expect the same for television ad spending. As giant advertisers find the cost of television harder and harder to justify their outlays will eventually take the kind of cliff dive observed in the chart (above) for newspaper advertising. Already some consumer goods and ad agency executives are alluding to the fact that the rate of return on traditional TV is becoming sketchy.

So far, we've seen little at the companies which own TV networks to demonstrate they are prepared for the floor to fall out of their revenue stream. While some have positions in a few internet production and delivery companies, most are clearly still doing their best to defend & extend the old business – just like newspaper owners did. Just as newspapers never found a way to replace the print ad dollars, these television companies look very much like businesses that have no apparent solution for future growth. I would not want my 401K invested in any major network company.

And there will be winners.

For smaller businesses, there has never been a better time to compete. A company as small as Tesla or Fisker can now create a brand on-line at a fraction of the old cost. And that brand can be as powerful as Ford, and potentially a lot more trendy. There are very low entry barriers for on-line brand building using not only ad words and web page display ads, but also using social media to build loyal followers who use and promote a brand. What was once considered a niche can become well known almost overnight simply by applying the new dynamics of reaching customers on-line, and increasingly via mobile. Look at the success of Toms Shoes.

Zappos and Amazon have shown that with almost no television ads they can create powerhouse retail brands. The new retailers do not compete just on price, but are able to offer selection, availability and customer service at levels unachievable by traditional brick-and-mortar retailers. They can suggest products and prices of things you're likely to need, even before you realize you need them. They can educate better, and faster, than most retail store employees. And they can offer great prices due to less overhead, along with the convenience of shipping the product right into your home.

And as people quit watching preprogrammed TV, where will they go for content? Anybody streaming will have an advantage – so think Netflix (which recently contracted for all the Disney content,) Amazon, Pandora, Spotify and even AOL. But, this will also benefit those companies providing content access such as Apple TV, Google TV, YouTube (owned by Google) to offer content channels and the increasingly omnipresent Facebook will deliver up not only friends, but content — and ads.

As for content creation, the deep pockets of traditional TV production companies will likely disappear along with their ability to control distribution. That means fewer big-budget productions as risk goes up without revenue assurances.

But that means even more ability for newer, smaller companies to create competitive content seeking audiences. Where once a very clever, hard working Seth McFarlane (creator of Family Guy) had to hardscrabble with networks to achieve distribution, and live in fear of a single person controlling his destiny, in the future these creative people will be able to own their content and capture the value directly as they build a direct audience. A phenomenon like George Lucas will be more achievable than ever before as what might look like chaos during transition will migrate to a much more competitive world where audiences, rather than network executives, will decide what content wins – and loses.

So, with due respects to Don McLean, will today be the day TV Died? We will only know in historical context. Nobody predicted newspapers had peaked in 2000, but it was clear the internet was changing news consumption behavior. And we don't know if TV viewership will begin its rapid decline in 2013, or in a couple more years. But the inevitable change is clear – we just don't know exactly when.

So it would be foolish to not think that the industry is going to change dramatically. And the impact on advertising will be even more profound, much more profound, than it was in print. And that will have an even more profound impact on American society – and how business is done.

What are you doing to prepare?