by Adam Hartung | Nov 3, 2020 | Finance, Investing, Strategy, Trends

In September, 2015 (5 years ago) I wrote that Tesla was going to change global oil demand. Why? Because Tesla had proven there was a market shift toward electric vehicles (EV’s). Yes, the market was small. But every major auto company had seen the trend emerge, and all had EV’s on the drawing tables. Simultaneously, this was showing a shift to “electrification” at the same time that solar energy costs were dropping in price similar to computer chips in the 1990s.

The combination of shifts away from internal combustion engine (ICE) automobiles operating on petroleum, and the growth in renewable energy production from solar and wind was becoming obvious. In sailing, there are small lengths of cloth attached to the sails specifically to obtain an early read on wind direction. These are called “telltales.” Looking at Tesla and growing renewable electricity generation, the telltales gave me confidence to specifically predict it would

really hurt Exxon.

Now, 5 years later, most pundits think the world has reached “peak oil” usage, and demand for oil will only fall.Since 2015 Exxon’s equity value (XOM) has declined 65%. Due to declining demand, the company is being forced to restructure and possibly

cut its dividend as the company shrinks.

Some would look only at short-term issues like the pandemic, but the economy in China has fully recovered – yet its demand for oil has not. Or some might say that oil prices are down only because Saudi Arabia and Russia are battling over market share – but this only portends more bad news for Exxon because 2 giants with the lowest cost battling for share will only make it harder for Exxon to sell products, even at a lower price and little or no margin.

Unfortunately, the pandemic has created an acceleration in the trends that are dooming profits for oil companies like Exxon. Once business happened in physical meetings where we transported ourselves by auto or plane fueled by oil. Now, meetings are being held on-line, virtually. Increasingly individuals, and companies, have learned not only how to use this technology but that they are more productive. Less wasted commuting time, less wasted hallway conversation time, fewer interruptions, and a recognition that it is possible to cut meeting time allowing attendees to better streamline work and decision-making. Speaking of work, virtual meetings are leading to better employee concentration due to better scheduling of time for meetings, and scheduling time for individual work.

Recall 2010 and the effort put into driving to work, or flying to meetings. Exxon, GM, Ford, Boeing, United Airlines and American Airlines were economic leaders, reflecting the work methods of the Industrial Era. Exxon was one of the 30 stocks on the Dow Jones Industrial Average. But the Great Recession had taken GM off the Dow, and now declining oil demand has removed Exxon – following the path I previously predicted.

Look at current 11/2020 market capitalizations:

Exxon – $133B

General Motors – $49B

Ford – $31B

Boeing – $83B

United Airlines – $10B

American Airlines – $6B

The world has changed. Trends have prevailed. We are now more mobile-oriented, work more asynchronously and use

more gig resources. Now we connect by Zoom and travel on electrons.

REUTERS/Lucy Nicholson

Zoom market cap – $146B

Tesla market cap – $380BWhy this walk down the path of recent history? Markets shift – often a lot faster than we would like to imagine. The economic hurt on those left behind is enormous. The opportunity for new leaders even more enormous. On the back end of trends is a LOT of pain. On the front end of trends is a lot of happy, happy. It is incredibly important to pick out the telltales and incorporate them into your planning. Earlier rather than later.Let trends direct your investments and your business decisions – look forward not backward. You want to be Zoom or Tesla (or own the stocks,) not Exxon, GM or Boeing (nor own those stocks.)

If you don’t have a clear line of sight to the future, ask for help – it’s my job. Do you remember anyone else predicting this enormous shift back in 2015? Back then oil was $100/barrel and Exxon was trading at $100/share. More pundits were expecting the future to look like the past than to make a radical shift. But we are always looking at the early telltales, always developing new scenarios, always preparing for market shifts and their implications.

Did you see the trends, and were you expecting the changes that would happen to oil demand? It IS possible to use trends to make good forecasts, and prepare for big market shifts. If you don’t have time to do it, maybe you should contact us!! We track hundreds of trends, and are experts at developing scenarios applied to your business to help you make better decisions.

Or, to keep up on trends, subscribe to our weekly podcasts and posts on trends and how they will affect the world of business at www.SparkPartners.comTRENDS MATTER. If you align with trends your business can do GREAT! Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business. Click for Assessment info.

Give us a call or send an email. Adam@sparkpartners.com 847-331-6384

by Adam Hartung | Jul 22, 2020 | Disruptions, Innovation, Leadership, Marketing, Trends

As the pandemic dropped on the USA with full force mid-April the price of oil dropped to less than $0. OK, it was something of a fluke. Demand dropped so fast that supply couldn’t fall fast enough, so oil was flowing into refineries and tanks and pipelines so fast that nobody knew where to put it – and that resulted in suppliers having to pay someone to take their oil.

But… the point was very real. Oil prices depend on demand – every bit as much as supply. Even though for a generation we’ve taken growing oil demand for granted, and focused on how to create additional supply, it is a fact that NOW declining demand will limit the value of oil and gas (which is, after all, a commodity.) The TREND has changed course, with demand in the USA barely, or not, growing – and globally demand growth primarily all in Asia (mostly China.) Overall, supply growth has beaten demand growth by a wide margin, and prices are not only low now – they will likely go lower. Even oil company CEOs are predicting US production will decline – but to lower demand

In 2015, I predicted that Tesla could put a big hurt on Exxon. Most people thought that was a joke. Tesla was a fraction the size of GM, and “small potatoes” in the car industry. Meanwhile Exxon was one of the world’s largest oil producers and refiners. That really would be a very small David smacking a very big Goliath – and with a very small rock. But what I pointed out in 2015 was that traditional analysts predicted a very gradual growth in electric cars, and a continued growth in petroleum powered cars, and pretty much constant growth in oil & gas consumption with economic growth. In other words,analysts were using old assumptions all around and expecting only a tiny impact from a few weirdos buying electric cars.

But I asked, what if those assumptions were wrong? In 2015, the world was awash in oil, inventories were then at record levels, and electric car sales were taking off. And the truth was, a lot was happening to reduce demand for oil. Renewable energy programs, conservation, and a change in economic activity from basic manufacturing and commodity processing to a knowledge economy. These trends were all putting big dampers on oil demand. And electric auto sales were poised for a big boom. I predicted demand for oil would drop substantially, inventories would skyrocket and industry problems would worsen as prices cratered.

Uh-hum – what was the price of oil in April?

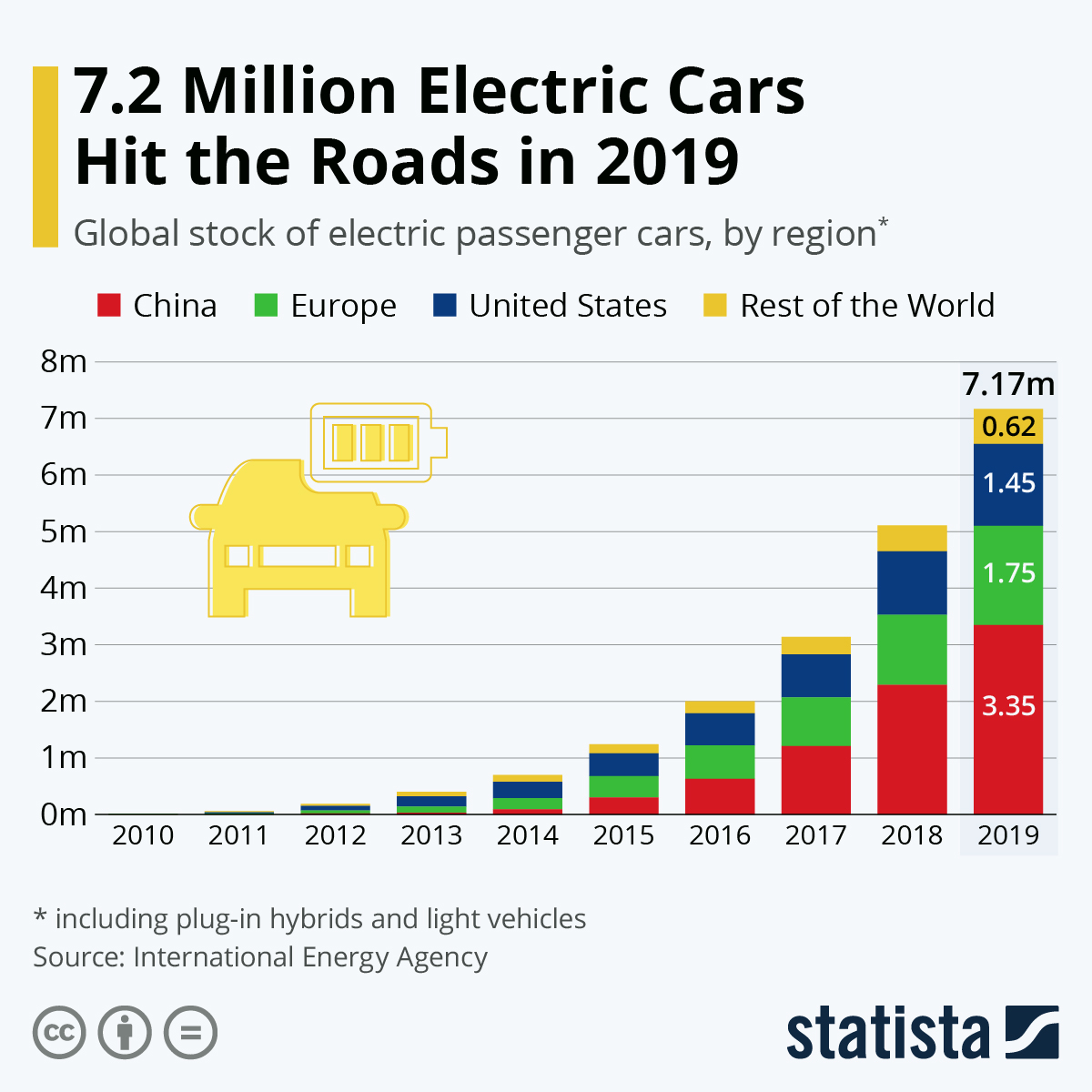

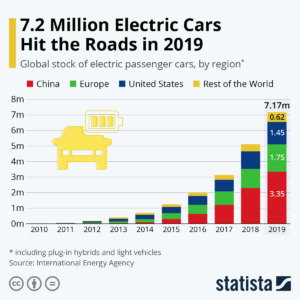

In 2009, I made the case that electric cars were a small base, but that geometric demand growth would make them an important economic impact . Today, most Americans still think that’s the case. In 2009 less than 100,000 new cars were electric. But by 2015, over 1 million electric cars had been sold. Then, with the help of game changers like the Tesla Model 3 in 2019 sales exceeded 7 million! A 7-fold increase in 5 years, or nearly 50%/year market growth!!

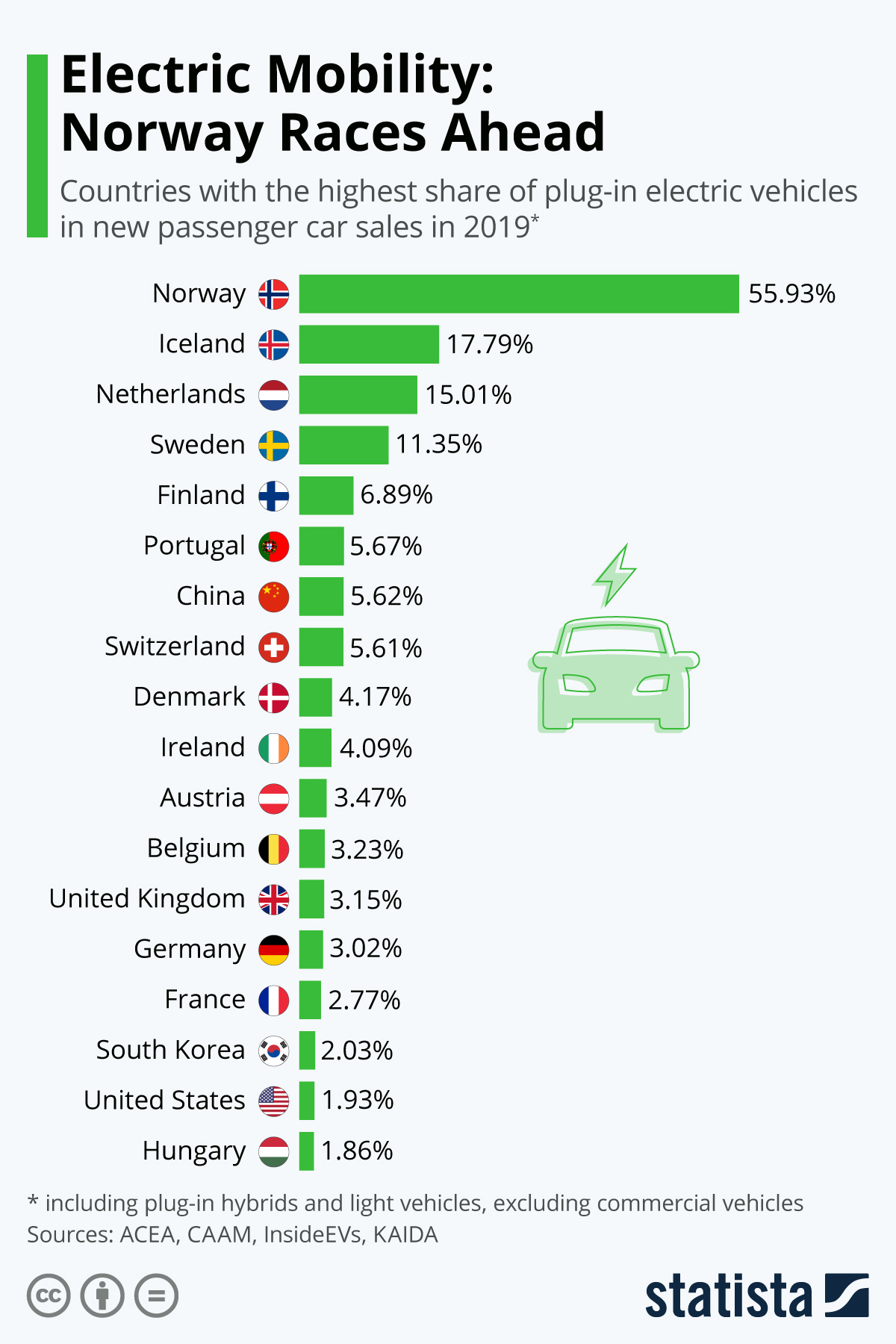

Americans aren’t aware of this phenomenon largely because the big growth centers are outside the USA. Where electrics are ~2% of US car sales, in some European countries they are well over 10% of the market. Even in China they represent over 5% of sales!

Remember what I said above about demand growth depending on China? Look again at who’s buying the most electric cars.

Lessons:

1 – Never think your product is beyond attack by market forces. Be paranoid.

2 – Very small, fringe competition can sneak up and steal your market faster than you think.

3 – Fringe changers don’t have to take a huge market share to make a BIG impact on your market and pricing.

4 – Disruptive events favor the upstarts, who are on trend, and hurt big incumbents, who depend on “business as usual.”

5 – Don’t expect markets to “return to normal.” Markets always move forward, with trends.

6 – Don’t plan from the past, plan for the future – and pay attention to disruptions, they can break you.

TRENDS MATTER. If you align with trends your business can do GREAT! Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business (https://adamhartung.com/assessments/)

Give us a call or send an email. Adam @Sparkpartners.com

by Adam Hartung | Sep 22, 2015 | Current Affairs, Disruptions, In the Rapids, Innovation

A recent analyst took a look at the impact of electric vehicles (EVs) on the demand for oil, and concluded that they did not matter. In a market of 95million barrels per day production, electric cars made a difference of 25,000 to 70,000 barrels of lost consumption; ~.05%.

You can’t argue with his arithmetic. So far, they haven’t made any difference.

But then he goes on to say they won’t matter for another decade. He forecasts electric vehicle sales grow 5-fold in one decade, which sounds enormous. That is almost 20% growth year over year for 10 consecutive years. Admittedly, that sounds really, really big. Yet, at 1.5million units/year this would still be only 5% of cars sold, and thus still not a material impact on the demand for gasoline.

But then he goes on to say they won’t matter for another decade. He forecasts electric vehicle sales grow 5-fold in one decade, which sounds enormous. That is almost 20% growth year over year for 10 consecutive years. Admittedly, that sounds really, really big. Yet, at 1.5million units/year this would still be only 5% of cars sold, and thus still not a material impact on the demand for gasoline.

This sounds so logical. And one can’t argue with his arithmetic.

But one can argue with the key assumption, and that is the growth rate.

Do you remember owning a Walkman? Listening to compact discs? That was the most common way to listen to music about a decade ago. Now you use your phone, and nobody has a walkman.

Remember watching movies on DVDs? Remember going to Blockbuster, et.al. to rent a DVD? That was common just a decade ago. Now you likely have shelved the DVD player, lost track of your DVD collection and stream all your entertainment. Bluckbuster, infamously, went bankrupt.

Do you remember when you never left home without your laptop? That was the primary tool for digital connectivity just 6 years ago. Now almost everyone in the developed world (and coming close in the developing) carries a smartphone and/or tablet and the laptop sits idle. Sales for laptops have declined for 5 years, and a lot faster than all the computer experts predicted.

Markets that did not exist for mobile products 10 years ago are now huge. Way beyond anyone’s expectations. Apple alone has sold over 48million mobile devices in just 3 months (Q3 2015.) And replacing CDs, Apple’s iTunes was downloading 21million songs per day in 2013 (surely more by now) reaching about 2billion per quarter. Netflix now has over 65million subscribers. On average they stream 1.5hours of content/day – so about 1 feature length movie. In other words, 5.85billion streamed movies per quarter.

What has happened to old leaders as this happened? Sony hasn’t made money in 6 years. Motorola has almost disappeared. CD and DVD departments have disappeared from stores, bankrupting Circuit City and Blockbuster, and putting a world of hurt on survivors like Best Buy.

The point? When markets shift, they often shift a lot faster than anyone predicts. 20%/year growth is nothing. Growth can be 100% per quarter. And the winners benefit unbelievably well, while losers fall farther and faster than we imagine.

Tesla was barely an up-and-comer in 2012 when I said they would far outperform GM, Ford and Toyota. The famous Bob Lutz, a long-term widely heralded auto industry veteran chastised me in his own column “Tesla Beating Detroit – That’s Just Nonsense.”

Mr. Lutz said I was comparing a high-end restaurant to McDonald’s, Wendy’s and Pizza Hut, and I was foolish because the latter were much savvier and capable than the former. He should have used as his comparison Chipotle, which I predicted would be a huge winner in 2011. Those who followed my advice would have made more money owning Chipotle than any of the companies Mr. Lutz preferred.

The point? Market shifts are never predicted by incumbents, or those who watch history. The rate of change when it happens is so explosive it would appear impossible to achieve, and far more impossible to sustain. The trends shift, and one market is rapidly displaced by another.

While GM, Ford and Toyota struggle to maintain their mediocrity, Tesla is winning “best car” awards one after another – even “breaking” Consumer Reports review system by winning 103 points out of a maximum 100, the independent reviewer liked the car so much. Tesla keeps selling 100% of its production, even at its +$100K price point.

So could the market for EVs wildly grow? BMW has announced it will make all models available as electrics within 10 years, as it anticipates a wholesale market shift by consumers promoted by stricter environmental regulations. Petroleum powered car sales will take a nosedive.

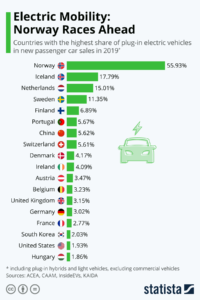

The International Energy Agency (IEA) points out that EVs are just .08% of all cars today. And of the 665,000 on the road, almost 40% are in the USA, where they represent little more than a rounding error in market share. But there are smaller markets where EV sales have strong share, such as 12% in Norway and 5% in the Netherlands.

So what happens if Tesla’s new lower priced cars, and international expansion, creates a sea change like the iPod, iPhone and iPad? What happens if people can’t get enough of EVs? What happens if international markets take off, due to tougher regulations and higher petrol costs? What happens if people start thinking of electric cars as mainstream, and gasoline cars as old technology — like two-way radios, VCRs, DVD players, low-definition picture tube TVs, land line telephones, fax machines, etc?

What if demand for electric cars starts doubling each quarter, and grows to 35% or 50% of the market in 10 years? If so, what happens to Tesla? Apple was a nearly bankrupt, also ran, tiny market share company in 2000 before it made the world “i-crazy.” Now it is the most valuable publicly traded company in the world.

Already awash in the greatest oil inventory ever, crude prices are down about 60% in the last year. Oil companies have already laid-off 50,000 employees. More cuts are planned, and defaults expected to accelerate as oil companies declare bankruptcy.

It is not hard to imagine that if EVs really take off amidst a major market shift, oil companies will definitely see a precipitous decline in demand that happens much faster than anticipated.

To little Tesla, which sold only 1,500 cars in 2010 could very well be positioned to make an enormous difference in our lives, and dramatically change the fortunes of its shareholders — while throwing a world of hurt on a huge company like Exxon (which was the most valuable company in the world until Apple unseated it.)

[Note: I want to thank Andreas de Vries for inspiring this column and assisting its research. Andreas consults on Strategy Management in the Oil & Gas industry, and currently works for a major NOC in the Gulf.]

by Adam Hartung | Apr 14, 2012 | Current Affairs, Leadership, Transparency, Web/Tech

Apple's amazing increase in value is more than just a "rah-rah" story for a turnaround. Fundamentally, Apple is telling everyone – globally – that there has been a tectonic shift in markets. And if leaders don't understand this shift, and incorporate it into their strategy and tactics, their organizations are going to have a very difficult future.

Recently Apple's value peaked at $600B. Yes, that is an astounding number, for it reflects not only 50% greater value than the oil giant Exxon/Mobil (~$390B), but more than the entire value of the stock markets in Spain, Greece and Portugal combined!

Source: Business Insider.com

This astounding valuation causes many to be reticent about owning Apple shares, for it seems implausible that any one company – especially a tech company with so few employees – could be worth so much.

Unless we look at this information in the context of a major, global economic shift. That what the world values has changed dramatically. And that what investors are telling business (and government) leaders is that in a globalized, fast paced world value is based upon what you know, when you know it – in other words information. Not land, buildings or the ability to make things.

Three hundred years ago the wealthiest people in the world owned land. Wars were fought for centuries to control land. Kings owned land, and controlled everything on the land while capturing the value of everything produced on that land. As changes came along, reducing the role of kings, land barons became the wealthiest people in the world. In an agrarian economy, where most human resources (and all others for that matter) were deployed in food production owning land was the most valuable thing on the planet.

But then some 120 years ago, along came the industrial reveolution. Suddenly, productivity rose dramatically by applying new machines to jobs formerly performed by humans. With this shift, value changed. The great industrialists were able to capture the value of greater productivity – making people like Cyrus McCormick, Henry Ford and Andrew Carnegie the wealthiest of the wealthy. Worth more than most states, and many foreign countries.

The age of manufacturing was based upon the productivity of machines and the application of industrial processes to what formerly was hand labor. Creating tools – from entignes to automobiles to airplanes – created great wealth. Knowing how to make these machines, and making them, created enormous value. And companies like General Motors, General Dynamics and General Electric were worth much more than the land upon which food was produced. And the commodity suppliers, like Exxon/Mobil, feeding industrial companies captured huge value as well.

By the middle 1900s America's farmers were forced to create ever larger farms to remain in business, and were constantly begging for government subsidies to stay alive via price controls (parity programs) and land "set-asides" run by the Agriculture Department. By the 1980s family farms going broke by the thousands, agricultural land values plummeted and the ability to create value by growing or processing food was a struggle. Across the developed world, wealth shifted into the hands of industrial companies from landowners.

Sometime in the 1990s the world shifted again, and that's what the chart above shows us. Countries with little or no technology companies – no information economy – cannot create value. On the other hand, companies that can drive new levels of productivity via the creation, management, use and sale of information can create enormous value.

Think about the incredible shift that has happened in retail. America's largest and most successful retailer from the 1900 turn of the century well into the 1960s was Sears. In an industry that long equated success with "location, location, location" Sears has had, and continues to control, enormous amounts of land and buildings. But the value of Sears has declined like a stone pitched off a bridge, now worth only $6B (1% the Apple value) despite all that real estate!

Simultaneously, America's largest retailer Wal-Mart has seen its value go nowhere for over a decade, despite its thousands of locations that span every state. Even though Wal-Mart keeps adding stores, and enlarging stores, adding more and more land and buildings to its "asset" base the company's customer base, sales and value are mired, unable to rise.

Yet, Amazon – which has no land, and almost no buildings – has used the last 20 years to go from start up to an $86B valuation – doing much better for shareholders than its traditional, industrial thinking competitors. In the last 5 years, Amazon's value has roughly quadrupled!

Source: Yahoo Finance

Yes, Amazon is a retailer. But the company has learned that applying an industrial strategy is far less valuable than applying an information strategy. As an internet leader, first with most browser formats on PCs and smartphones, Amazon has reached far more new customers than any traditional real-estate focused company. By launching Kindle Amazon focused on the information in books, rather than the format (print) revolutionizing the market and capturing enormous value.

By launching Kindle Fire Amazon takes information one step further, making it possible for customers to access new products faster, order faster and build their own retail world without ever going to a building. By becoming a tech company, Amazon is clearly well on the way to dominating retail, as Sears falls into irrelevancy and almost surely bankruptcy, and Wal-Mart stalls under the overhead of all that land, buildings and vast number of minimum-wage, uninsured employees.

We now must realize that value is not created by what accountants have long called "hard assets" – land, buildings and equipment. In fact, the 2 great U.S. recessions since 2000 have demonstrated to everyone that there is no security in these – the value can decline, decline fast, and decline far. Just because these things are easy to see and count does not insure value. They can easily be worth less than they cost to make – or own.

Successful competition in 2012 (and going forward) requires businesses know about customers, products and have the ability to supply solutions fast with great reach. Winning is about what you know, knowing it early, acting upon the information and then being able to disseminate that solution fast to those who have emerging needs.

Which is why you have to be excited about the brilliant move Facebook made to acquire Instagram last week. In one fast, quick step Facebook bought the ability to easily and effectively provide mobile image solutions – across any application – to millions of existing users. Something that every single person, and business, on the planet is either doing now, or will be doing very soon.

Source: Wired

On a cost-per-existing-customer basis, Facebook stole Instagram. And that's before Facebook spreads out the solution to the rest of its 780million users! Forget about how many employees Instagram has, or its historical revenues or its assets. In an innovation economy, if you have a product that 35million people hear about and start using in less than a year, you have something very valuable!

Kudos go to Mark Zuckerberg as CEO, and his team, for making this acquisition so quickly. Before Instagram had a chance to hire bankers, market itself and probably raise its value 10x. That's why Mr. Zuckerberg was Time Magazine's "Man of the Year" at the start of 2011 – and why he's been able to create so much more value for his shareholders than the CEOs of industrial companies – like say GE.

Going forward, no company can plan to survive with an industrial strategy. That approach, and those rules, simply don't create high returns. To be successful you MUST become a tech company. And while this may not feel comfortable, it is reality. Every business must shift, or die.

by Adam Hartung | Sep 26, 2010 | Current Affairs, In the Rapids, Leadership, Openness, Web/Tech

Summary:

- Apple is worth more than Microsoft today, even though Microsoft is larger, because it has better growth prospects

- Apple is closing in on the most valuable company in the world – Exxon

- Exxon’s value is stalled because it has no growth markets

- Exxon once developed, then abandoned, a growth business called Exxon Office Systems

- Apple’s value may eclipse Exxon, which has almost 8 times the revenue, because its growth prospects are so bright

- Profitable growth is worth more than monopolistic market share – or even huge revenue

We all know that over the last 10 years Apple has moved from the brink of bankruptcy to great success. Apple has been able to dramatically increase its revenues, growing at double-digit rates for several years. And Apple now competes in markets like mobile computing and entertainment where its hardware and software products are demonstrating a leading position as users migrate toward different platforms (iPods and downloadable music or video, iPads and downloadable video or text, iPhones and downloadable apps of all sorts).

Because of this profitable growth, Apple’s market value now exceeds Microsoft’s. An accomplishment nobody predicted a decade ago.

As this chart from Silicon Alley Insider shows, Apple’s profitable revenue growth has allowed its value to soar. Even though Microsoft is larger, and dominates its market of PC operating systems and office automation software, its value has stalled due to lack of growth. Because Apple is in very large, emerging markets with successful products it is generating a very high valuation.

In fact, Apple’s market cap is closing in on the most valuable company in the world – Exxon:

Source: Silicon Alley Insider

Exxon and Apple have nothing in common. Exxon is a petroleum company. It’s growth almost all from acquisition. You could say it’s nonsensical to compare the two.

But for those of us with long memories, we can remember in the early 1980s when Exxon opened Exxon Office Systems. As the price of crude oil, and its refined products, hit record highs Exxon made record profits. Leadership invested a few billion dollars into creating a new business intended to compete with IBM and Xerox – leading office equipment companies of the time. But, when the price of crude oil fell Exxon abandoned this venture – by then already achieving more than $1B/year in revenue. All the suppliers and customers were left in the lurch, and the employees were left looking for new jobs. Within weeks Exxon Office Products disappeared.

Exxon abandoned its opportunity for growth into new markets in order to “focus” on its “core” business of oil exploration and production, oil refining, and marketing of petroleum products. As a result, Exxon – augmented via its many acquisitions across the years – is now the world’s largest “oil” company as well as the world’s highest market capitalization company. But it has no growth. And thus, its value is totally dependent upon the price of oil – a commodity. Over the last 2 years this has caused Exxon’s value to decline.

At $43B in 2009, Apple has nowhere near the revenue of Exxon’s $310B. But what Apple has is new markets, and growth. Someday we’ll run out of oil (long time yet, to be sure). What will Exxon do then? But in the case of Apple we already know there will be future revenues from all the new products for a long time after the Mac has run its course and disappeared from backpacks. It’s that willingness to seek out new markets, to develop new products for emerging markets and constantly push for new, profitable revenues that makes Apple worth so much.

Could Apple become the world’s most valuable company? Possibly. If so, it won’t be from industry domination. That sort of monopolistic thinking drove the industrial era, and companies like AT&T as well as Exxon — and Microsoft. What’s worth more today than monopolism is entering new markets and generating profitable growth. It’s what once made the original Standard Oil worth so much, and it initially made Microsoft worth more than any other tech company. Too many of us forget that profitable growth, more than anything else, generates huge value and wealth. And that’s true in spades in 2010!