by Adam Hartung | Jan 27, 2011 | Current Affairs, Innovation, Leadership, Lock-in, Science, Web/Tech

Summary:

- The President has called for more innovation in America

- But American business management doesn’t know how to be innovative

- Business leaders focus on efficiency, not innovation

- America has no inherent advantage in innovation

- To increase innovation we need a change in incentives, to favor innovation over efficiency and traditional brick-and-mortar investments

- We need to highlight leaders that have demonstrated the ability to create jobs in the information economy, not the “old guard” just because they run big, but floundering, companies

It was good to hear the U.S. President call for more innovation in his State of the Union address this week. And it sounded like he wants most of that to come from business, rather than government. But I’m reminded the President is a lawyer and politician. As a businessman, well, let’s say he’s a bit naive. Most businesses don’t have a clue how to be innovative, as Forbes pointed out in November, 2009 in “Why the Pursuit of Innovation Usually Fails.”

Businesses by and large are not designed to be innovative. Modern management theory, going back to the days of Frederick Taylor, has been dominated by efficiency. For the last decade businesses have reacted to global competitive forces by seeking additional efficiency. Thus the offshoring movement for information technology and manufacturing eliminated millions of American jobs driving unemployment to double digits, and undermines new job creation keeping unemployment stubbornly high.

It is not surprising business leaders avoid innovation, when the august Wall Street Journal headlines on January 20 “In Race to Market, It Pays to Be Latecomer.” Citing a number of innovator failures, including automobiles, browsers and small computers, the journal concludes that it is smarter business to not innovate. Rather leaders should wait, let someone else innovate and then hope they can take the idea and make something of it down the road. Not a ringing pledge for how good management supports the innovation agenda!

The professors cited in the Journal article take a fairly common point of view. Because innovators fail, don’t be one. Lower your risk, come in later, hope you can catch the market at a future time. It’s easy to see in hindsight how innovators fail, so why take the risk? Keep your eyes on being efficient – and innovation is anything but efficient! Because most businesspeople don’t understand how to manage innovation, don’t try.

As discussed in my last blog, about Sara Lee, executives, managers and investors have come to believe that cost cutting, and striving for more efficiency, is the solution for most business problems. According to the Washington Post, “Immelt To Head New Advisory Board on Job Creation.” The President appointed the GE Chairman to this highly visible position, yet Mr. Immelt has spent most of the last decade shrinking GE, and pushing jobs offshore, rather than growing the company – especially domestically. Gone are several GE businesses created in the 1990s – including the recent spin out of NBC to Comcast. It’s ironic that the President would appoint someone who has overseen downsizings and offshoring to this position, instead of someone who has demonstrated the ability to create jobs over the last decade.

As one can easily imagine, efficiency is not the handmaiden of innovation. To the contrary, as we build organizations the desire for efficiency and “professional management” impedes innovation. According to Portfolio.com in “Can Google Be Entrepreneurial” even Google, a leading technology company with such exciting new products as Android and Chrome, has replaced its CEO Eric Schmidt with founder Larry Page in order to more effectively manage innovation. The contention is that the 55 year old professional manager Schmidt created innovation barriers. If a company as young and successful as Google struggles to innovate, one can only imagine the difficulties at traditional, aged American businesses!

While many will trumpet America’s leadership in all business categories, Forbes‘ Fred Allen is correct to challenge our thinking in “The Myth of American Superiority at Innovation.” For decades America’s “Myth of Efficiency” has pushed organizations to streamline, cutting anything that is not totally necessary to do what it historically did better, faster or cheaper. Innovation inside businesses was designed to improve existing processes, usually cutting cost and jobs, not create new markets with high growth that creates jobs and economic growth. Most executives would 10x rather see a plan to cut costs saving “hard dollars” in the supply chain, or sales and marketing, than something involving new product introduction into new markets where they have to deal with “unknowns.” Where our superiority in innovation originates, if at all, is unclear.

Lawyers are not historically known for their creativity. Hours spent studying precedent doesn’t often free the mind to “think outside the box.” Business folks have their own “precedent managers” – internal experts who set themselves up intentionally to block experimentation and innovation in the name of lowering risk, being conservative and carefully managing the core business. To innovate most organizations will be forced to “Fire the Status Quo Police” as I called for last September here in Forbes. But that isn’t easy.

America can be very innovative. Just look at the leadership America exerts in all things “social media” – from Facebook to Groupon! And look at how adroitly Apple has turned around by moving beyond its roots in personal computing to success in music (iPod and iTunes), mobile telephony and data (iPhone) and mobile computing (iPad). Netflix has used a couple of rounds of innovation to unseat old leader Blockbuster! But Apple and Netflix are still the rarities – innovators amongst the hoards of myopic organizations still focused on optimization. Look no further than the problems Microsoft – a tech company – has had balancing its desire to maintain PC domination while ineffectively attempting to market innovation.

What America needs is less bully pulpit, and more action if you really want innovation Mr. President:

- Increase tax credits for R&D

- Increase tax deductions and credits for new product launches by expanding the definition of what constitutes R&D in the tax code

- Implement penalties on offshore outsourcing to discourage the efficiency focus and the chronic push to low-cost global resources

- Lower capital gains taxes to encourage wealth creation through new business creation

- Manage the deficit by implementing VAT (value added taxes) which add cost to supply chain transactions, thus lowering the value of “efficiency” moves

- Make it much easier for foreign graduate students in America to receive their green cards so we can keep them here and quit exporting some of the brightest innovators we develop to foreign countries

- Create more tax incentives for investing in high tech – from nanotech to biotech to infotech – and quit wasting money trying to favor investments in manufacturing. Provide accelerated or double deductions for buying lab equipment, and stretch out deductions for brick-and-mortar spending. Better yet, quit spending so much on road construction and simply give credits to people who buy lab equipment and other innovation tools.

- Propose regulations on executive compensation so leaders aren’t encouraged to undertake short-term cost cutting measures merely to prop up short-term profits at the expense of long-term viability

- Quit putting “old guard” leaders who have seen their companies do poorly in highly placed positions. Reach out to those who really understand the information economy to fill such positions – like Eric Schmidt from Google, or John Chambers at Cisco Systems.

- Reform the FDA so new bio-engineered solutions do not follow regulations based on 50 year old pharma technology and instead streamline go-to-market processes for new innovations

- Quit spending so much money on border fences, DEA crack-downs on marijuana users and giant defense projects. Put the money into grants for universities and entrepreneurs to create and implement innovation.

Mr. President,, don’t expect traditional business to do what it has not done for over a decade. If you want innovation, take actions that will create innovation. American business can do it, but it will take more than asking for it. it will take a change in incentives and management.

by Adam Hartung | Jan 25, 2011 | Current Affairs, Food and Drink, In the Whirlpool, Leadership

Summary:

- It sounds good to refocus a business on its core

- It sounds good to centralize for cost reductions and belt tightening as part of refocusing

- It sounds good to sell “non-essential” businesses to raise cash

- It sounds good to have a company buy back shares

- But these efforts serve to destroy the company, killing it softly as it sounds good, but guts the business of revenues and innovation

- Sara Lee’s CEO destroyed the company softly by following such a strategy

The vultures are swirling around Sara Lee. “Sara Lee Said to Get Bid from Bain, Apollo Group Exceeding $18.70 a Share” was the Bloomberg headline. JBS and Blackstone Group are reportedly considering making an offer, according to the Wall Street Journal. This has, of course, driven up the share price from its steady decline of 67% between 2006 and 2009.. But unless you’re a short-term trader, even this acquisition offer is barely going to get you back to break even for your 5 year old investment.

Source: Marketwatch.com

Five years ago Brenda Barnes took leadership at Sara Lee to much fanfare, as she broke the long-problematic glass ceiling for women executives. But her plan for Sara Lee hasn’t worked out so well. Although her compensation has been in the millions, for investors, employees and suppliers this has been a very rough 5 years.

Ms. Barnes took over Sara Lee saying it was a “hodgepodge” of inefficient brands and businesses. Her goal was to streamline Sara Lee, refocus the company and regenerate its core. That certainly sounded good.

Her first steps were to consolidate operations into a central headquarters, including all R&D for the far-flung businesses. She started cutting costs, and heads, as she reduced the number of marketers and centralized purchasing. Going after “synergies,” consolidations were forced on all functions, and the re-launched R&D was staffed at a fraction of earlier product development efforts. The intent, accomplished, was to launch fewer products, and focus on cost reductions. To many listeners, this sounded so soothing. After all, who wouldn’t think there was “fat” to be cut? Who ever believes cost-cutting reaches an end? Why not try to “milk” more out of the old products rather than undertake costly new product launches?

Simultaneously, Ms. Barnes began selling businesses. Gone was the European meats and apparel units, soon followed by the direct sales business sale to Tupperware, and the Body Care business sale to Unilever. Branded apparel was spun out as a seperate company, and the bakery business was sold to Group Bimbo [transaction not yet closed.] Revenues declined from $13.2B in June, 2008 to $10.8B in June 2010 – and after the bakery sale would fall to $8.7B – a revenue drop of 1/3 in just a few years. But this was to refocus, and generate billions of cash for share buybacks. To many that sounded good as well.

All of this streamlining, cost cutting, consolidating and refocusing did raise cash. But, for investors, quarterly dividends were cut from 19.75 cents/share in April, 2006 to 10 cents/share in August, 2006. Only recently have dividends been raised to 11.5 cents/share, but this is still a reduction of over 40% from where dividends were prior to implementing the new refocusing strategy.

After years of implementation, Sara Lee investors in 2010 were holding stock worth less, and had lower dividends, than before this new plan was put into effect.

It all sounded so good, like the lyrics of a lullaby. Refocus. Go back to the business core. Get out of non-essential businesses. Consolidate operations with belt-tightening. Centralize functions to get more done with fewer resources. Sell businesses to raise cash. And invest that cash in share buybacks that would raise the company value. (The alchemy of this last statement still mystifies me. At the end, you’ve sold all the businesses to raise money to buy the last shares – and nobody is left with anything. It’s like selling parts of the house to pay the maintenance – eventually there’s nowhere left to live. How anybody thinks this is good for any constituency of the company is hard to fathom.)

What has been accomplished under the Barnes leadership?

- The equity value cratered, only to be uplifted by a private equity takeover effort that may allow investors to regain their original investment

- Cash dividends have been gutted

- Sara Lee is now a much smaller company, with no new products and no growth plan

- Operating cash flow has declined

- Cash has been dispersed in meaningless stock buybacks that have accomplished nothing

- Tens of thousands of jobs have been lost

- Suppliers have been squeezed out, or if still selling to Sara Lee had their margins squeezed

- Downers Grove, IL ,where the headquarters is located, can link declines in commercial and residential real estate to the downfall of Sara Lee

While it may sound like a comforting song, business leadership that turns to cutting the business throws it into a growth stall from which there is almost no hope of recovery. Even though short-term there may be bragging about the effort to refocus, cut costs and raise cash, these actions simply kill the business – softly and slowly perhaps, but kill it nonetheless.

Sales and profit problems are the result of remaining stuck in old market approaches long after the market has shifted to superior solutions. The only way to “fix” the business is to get closer to the market and launch new products, technologies, processes or solutions that are aligned with emerging market trends. You can’t cost-cut, refocus or re-align a business to success. You have to grow it.

by Adam Hartung | Jan 19, 2011 | Current Affairs, Disruptions, Games, In the Rapids, In the Swamp, Innovation, Leadership, Lock-in, Music, Openness, Web/Tech

The Wall Street Journal headlined Monday, “Apple Chief to Take Leave.” Forbes.com Leadership editor Fred Allen quickly asked what most folks were asking “Where does Steve Jobs Leave Apple Now?” as he led multiple bloggers covering the speculation about how long Mr. Jobs would be absent from Apple, or if he would ever return, in “What They Are Saying About Steve Jobs.” The stock took a dip as people all over raised the question covered by Steve Caulfield in Forbes’ “Timing of Steve Jobs Return Worries Investors, Fans.”

If you want to make money investing, this is what’s called a “buying opportunity.” As Forbes’ Eric Savitz reported “Apple is More Than Just Steve Jobs.” Just look at the most recent results, as reported in Ad Age “Apple Posts ‘Record Quarter’ on Strong iPhone, Mac, iPad Sales:”

- Quarterly revenue is up 70% vs. last year to $26.7B (Apple is a $100B company!)

- Quarterly earnings rose 77% vs last year to $6B

- 15 million iPads were sold in 2010, with 7.3 million sold in the last quarter

- Apple has $50B cash on hand to do new product development, acquisitions or pay dividends

ZDNet demonstrated Apple’s market resiliency headlining “Apple’s iPad Represents 90% of All Tablets Shipped.” While it is true that Droid tablets are now out, and we know some buyers will move to non-Apple tablets, ZDNet predicts the market will grow more than 250% in 2011 to over 44 million units, giving Apple a lot of room to grow even with competitors bringing out new products.

Apple is a tremendously successful company because it has a very strong sense of where technology is headed and how to apply it to meet user needs. Apple is creating market shifts, while many other companies are reacting. By deeply understanding its competitors, being willing to disrupt historical markets and using White Space to expand applications Apple will keep growing for quite a while. With, or without Steve Jobs.

On the other hand, there’s the stuck-in-the-past management team at Microsoft. Tied to all those aging, outdated products and distribution plans built on PC technology that is nearing end of life. But in the midst of the management malaise out of Seattle Kinect suddenly showed up as a bright spot! SFGate reported that “Microsoft’s Xbox Kinect beond hackers, hobbyists.” Seems engineers around the globe had started using Kinect in creative ways that were way beyond anything envisioned by Microsoft! Put into a White Space team, it was possible to start imagining Kinect could be powerful enough to resurrect innovation, and success, at the aging monopolist!

But, unfortunately, Microsoft seems far too stuck in its old ways to take advantage of this disruptive opportunity. Joel West at SeekingAlpha.com tells us “Microsoft vs. Open Kinect: How to Miss a Significant Opportunity.” Microsoft is dedicated to its plan for Kinect to help the company make money in games – and has no idea how to create a White Space team to exploit the opportunity as a platform for myriad uses (like Apple did with its app development approach for the iPhone.)

In the end, ZDNet joined my chorus looking to oust Ballmer (possibly a case study in how to be the most misguided CEO in corporate America) by asking “Ballmer’s 11th Year as Microsoft’s CEO – Is it Time for Him to Go?” Given Ballmer’s massive shareholding, and thus control of the Board, it’s doubtful he will go anywhere, or change his management approach, or understand how to leverage a breakthrough innovation. So as the Cloud keeps decreasing demand for traditional PCs and servers, Brett Owens at SeekingAlpha concludes in “A Look at Valuations of Google, Apple, Microsoft and Intel” that Microsoft has nowhere to go but down! Given the amazingly uninspiring ad program Microsoft is now launching (as described in MediaPost “Microsoft Intros New Corporate Tagline, Strategy“) we can see management has no idea how to find, or sell, innovation.

We often hear advice to buy shares of a company. Rarely recommendations to sell. But Apple is the best positioned company to maintain growth for several more years, while Microsoft has almost no hope of moving beyond its Lock-in to old products and markets which are declining. Simplest trade of 2011 is to sell Microsoft and buy Apple. Just read the headlines, and don’t get suckered into thinking Apple is nothing more than Steve Jobs. He’s great, but Apple can remain great in his absence.

by Adam Hartung | Jan 13, 2011 | Current Affairs, In the Rapids, Innovation, Leadership, Web/Tech

Before there was Facebook, the social media juggernaut which is changing how we communicate – and might change the face of media – there was MySpace. MySpace was targeted at the same audience, had robust capability, and was to market long before Facebook. It generated enormous interest, received a lot of early press, created huge valuation when investors jumped in, and was undoubtedly not only an early internet success – but a seminal web site for the movement we now call social media. On top of that, MySpace was purchased by News Corporation, a powerhouse media company, and was given professional managers to help guide its future as well as all the resources it ever wanted to support its growth. By almost all ways we look at modern start-ups, MySpace was the early winner and should have gone on to great glory.

But things didn’t turn out that way. Facebook was hatched by some college undergrads, and started to grow. Meanwhile MySpace stagnated as Facebook exploded to 600 million active users. During early 2010, according to The Telegraph in “Facebook Dominance Forces Rival Networks to Go Niche,” MySpace gave up on its social media leadership dreams and narrowed its focus to the niche of being a “social entertainment destination.” As the number of users fell, MySpace was forced to cut costs, laying off half its staff this week according to MediaPost.com “MySpace Confirms Massive Layoffs.” After losing a reported $350million last year, it appears that MySpace may disappear – “MySpace Versus Facebook – There Can Be Only One” reported at Gigaom.com. The early winner now appears a loser, most likely to be unplugged, and a very expensive investment with no payoff for NewsCorp investors.

What went wrong? A lot of foks will be relaying the tactics of things done and not done at MySpace. As well as tactics done and not done at Facebook. But underlying all those tactics was a very simple management mistake News Corp. made. News Corp tried to guide MySpace, to add planning, and to use “professional management” to determine the business’s future. That was fatally flawed when competing with Facebook which was managed in White Space, lettting the marketplace decide where the business should go.

If the movie about Facebook’s founding has any veracity, we can accept that none of the founders ever imagined the number of people and applications that Facebook would quickly attract. From parties to social games to product reviews and user networks – the uses that have brought 600 million users onto Facebook are far, far beyond anything the founders envisioned. According to the movie, the first effort to sell ads to anyone were completely unsuccessful, as uses behond college kids sharing items on each other were not on the table. It appeared like a business bust at the beginning.

But, the brilliance of Mark Zuckerberg was his willingness to allow Facebook to go wherever the market wanted it. Farmville and other social games – why not? Different ways to find potential friends – go for it. The founders kept pushing the technology to do anything users wanted. If you have an idea for networking on something, Facebook pushed its tech folks to make it happen. And they kept listening. And looking within the comments for what would be the next application – the next promotion – the next revision that would lead to more uses, more users and more growth.

And that’s the nature of White Space management. No rules. Not really any plans. No forecasting markets. Or foretelling uses. No trying to be smarter than the users to determine what they shouldn’t do. Not prejudging ideas so as to limit capability and focus the business toward a projected conclusion. To the contrary, it was about adding, adding, adding and doing whatever would allow the marketplace to flourish. Permission to do whatever it takes to keep growing. And resource it as best you can – without prejudice as to what might work well, or even best. Keep after all of it. What doesn’t work stop resourcing, what does work do more.

Contrarily, at NewsCorp the leaders of MySpace had a plan. NewsCorp isn’t run by college kids lacking business sense. Leaders create Powerpoint decks describing where the business will head, where they will invest, how they will earn a positive ROI, projections of what will work – and why – and then plans to make it happen. They developed the plan, and then worked the plan. Plan and execute. The professional managers at News Corp looked into the future, decided what to do, and did it. They didn’t leave direction up to market feedback and crafty techies – they ran MySpace like a professional business.

And how’d that work out for them?

Unfortunately, MySpace demonstrates a big fallacy of modern management. The belief that smart MBAs, with industry knowledge, will perform better. That “good management” means you predict, you forecast, you plan, and then you go execute the plan. Instead of reacting to market shifts, fast, allowing mistakes to happen while learning what works, professional managers should be able to predict and perform without making mistakes. That once the bright folks who create the strategy set a direction, its all about executing the plan. That execution will lead to success. If you stumble, you need to focus harder on execution.

When managing innovation, including operating in high growth markets, nothing works better than White Space. Giving dedicated people permission to do whatever it takes, and resources, then holding their feet to the fire to demonstrate performance. Letting dedicated people learn from their successes, and failures, and move fast to keep the business in the fast moving water. There is no manager, leader or management team that can predict, plan and execute as well as a team that has its ears close to the market, and the flexibility to react quickly, willing to make mistakes (and learn from them even faster) without bias for a predetermined plan.

The penchant for planning has hurt a lot of businesses. Rarely does a failed business lack a plan. Big failures – like Circuit City, AIG, Lehman Brothers, GM – are full of extremely bright, well educated (Harvard, Stanford, University of Chicago, Wharton) MBAs who are prepared to study, analyze, predict, plan and execute. But it turns out their crystal ball is no better than – well – college undergraduates.

When it comes to applying innovation, use White Space teams. Drop all the business plan preparation, endless crunching of historical numbers, multi-tabbed Excel spreadsheets and powerpoint matrices. Instead, dedicate some people to the project, push them into the market, make them beg for resources because they are sure they know where to put them (without ROI calculations) and tell them to get it done – or you’ll fire them. You’ll be amazed how fast they (and your company) will learn – and grow.

by Adam Hartung | Jan 10, 2011 | Defend & Extend, Disruptions, Innovation, Leadership, Web/Tech

Summary:

- Communication is now global, instantaneous and free

- As a result people, and businesses, now adopt innovation more quickly than ever

- Competitors adapt much quicker, and react much stronger than ever in history

- Profits are squeezed by competitors rapidly adopting innovations

- But many business leaders avoid disruptions, leading to slower growth and declining returns

- To maintain, and grow, revenues and profits you must be willing to implement disruptions in order to stay ahead of fast moving competitors

- Amidst fast shifting markets, greatest value (P/E multiple and market cap) is given to those companies that create disruptions (like Facebook, Groupon, Twitter)

All business leaders know the pace of competitive change has increased.

It took decades for everyone to obtain an old-fashioned land line telephone. Decades for everyone to buy a TV. And likewise, decades for color TV adoption. Microwave ovens took more than a decade. Thirty years ago the words “long distance” implied a very big cost, even if it was a call from just a single interchange away (not even an area code away – just a different set of “prefix” numbers.) People actually wrote letters, and waited days for responses! Social change, and technology adoption, took a lot longer – and was considered expensive.

Now we assume communications at no cost with colleagues, peers, even competitors not only across town state, or nation, but across the globe! Communication – whether email, or texting, or old fashioned voice calls – has become free and immediate. (Consider Skype if you want free phone calls [including video no less] and use a PC at your local library or school building if you don’t own one.) Factoring inflation, it is possible to provide every member of a family of 5 with instant phone, email and text communication real-time, wirelessly, 24×7, globally for less than my parents paid for a single land-line, local-exchange only (no long distance) phone 50 years ago! And these mobile devices can send pictures!

As a result, competitors know more about each other a whole lot faster, and take action much more quickly, than ever in history. Facebook, for example, is now connecting hundreds of millions of people with billions of communications every day. According to statistics published on Facebook.com, every 20 minutes the Facebook website produces:

- 1,000,000 shared links

- 1,323,000 tagged photos

- 1,484,000 event invitations

- 1,587,000 Wall posts

- 1,851,000 Status updates

- 1,972,000 Friend requests accepted

- 2,716,000 photos uploaded

- 4,632,000 messages

- 10,208,000 comments

Multiply those numbers by 3 to get hourly. By 72 to get daily. Big numbers! Alexander Graham Bell had to invent the hardware and string thousands of miles of cable to help people communicate with his disruption. His early “software” were thousands of “operators” connecting calls through central switchboards. Mark Zuckerberg and friends only had to create a web site using existing infrastructure and existing tools to create theirs. Rapidly adopting, and using, existing innovations allowed Facebook’s founders to create a disruptive innovation of their own! Disruption has allowed Facebook to thrive!

Facebook has disrupted the way we communicate, learn, buy and sell. “Word of mouth” referrals are now possible from friends – and total strangers. Product benefits and problems are known instantaneously. Networks of people arguably have more influence that TV networks! Many employees are likely to make more facebook communications in a day than have conversations with co-workers! Facebook (or twitter) is rapidly becoming the new “water cooler.” Only it is global and has inputs from anyone. Yet only a fraction of businesses have any plans for using Facebook – internally or to be more competitive!

Far too many business leaders are unwilling to accept, adopt, invest in or implement disruptions.

InnovateOnPurpose.com highlights why in “Why Innovation Makes Executives Uncomfortable:”

- Innovation is part art, and not all science. Many execs would like to think they can run a business like engineering a bridge. They ignore the fact that businesses implement in society, and innovation is where we use the social sciences to help us gain insight into the future. Success requires more than just extending the past – because market shifts happen. If you can’t move beyond engineering principles you can’t lead or manage effectively in a fast-changing world where the rules are not fixed.

- Innovation requires qualitative insights not just quantitative statistics. Somewhere in the last 50 years the finance pros, and a lot of expensive strategy consultants, led business leaders to believe that if they simply did enough number crunching they could eliminate all risk and plan a guaranteed great future. Despite hundreds of math PhDs, that approach did not work out so well for derivative investors – and killed Lehman Brothers (and would have killed AIG insurance had the government not bailed it out.) Math is a great science, and numbers are cool, but they are insufficient for success when the premises keep changing.

- Innovation requires hunches, not facts. Well, let’s say more than a hunch. Innovation requires we do more scenario planning about the future, rather than just pouring over historical numbers and expecting projections to come true. We don’t need crystal balls to recognize there will be change, and to develop scenario plans that help us prepare for change. Innovation helps us succeed in a dynamic world, and implementation requires a willingness to understand that change is inevitable, and opportunistic.

- Innovation requires risks, not certainties. Unfortunately, there are NO certainties in business. Even the status quo plan is filled with risk. It’s not that innovation is risky, but rather that planning systems (ERP systems, CRM systems, all systems) are heavily biased toward doing more of the same – not something new! Markets can shift incredibly fast, and make any success formula obsolete. But most executives would rather fail doing the same thing faster, working harder, doing what used to work, than implement changes targeted at future market needs. Leaders perceive following the old strategy is less risky, when in reality it’s loaded with risk too! Too many businesses have failed at the hands of low-risk, certainty seeking leadership unable to shift with changing markets (GM, Chrysler, Circuit City, Fannie Mae, Brach’s, Sun Microsystems, Quest, the old AT&T, Lucent, AOL, Silicon Graphics, Yahoo, to name a few.)

Markets are shifting all around us. Faster than imaginable just 2 decades ago. Leaders, strategists and planners that enter 2011 hoping they can win by doing more, better, faster, cheaper will have a very tough time. That is the world of execution, and modern communication makes execution incredibly easy to copy, incredibly fast. Even Wal-Mart, ostensibly one of the best execution-oriented companies of all time, has struggled to grow revenue and profit for a decade. Today, companies that thrive embrace disruption. They are willing to disrupt within their organizations to create new ideas, and they are willing to take disruptive opportunities to market. Compare Apple to Dell, or Netflix to Blockbuster.

Recent investments have valued Facebook at $50B, Groupon at $6B and Twitter at almost $4B. Apple is now the second most valuable company (measured by market capitalization). Why? Because they are disrupting the way we do things. To thrive (perhaps survive by 2015) requires moving beyond the status quo, overcoming the perceived risk of innovation (and change) and taking the actions necessary to provide customers what they want in the future! Any company can thrive if it embraces the disruptions around it, and uses them to create a few disruptions of its own.

by Adam Hartung | Jan 8, 2011 | Books, Openness

My guest blogger today is Nick Morgan, Founder and CEO of America’s leading firm for developing and coaching great speeches. Leaders, especially those who promote innovation, need to be great communicators. You are never good enough when market shifts make the stakes so high. Here Nick offers particularly good insight to everyone who finds themselves in front of an audience in 2011:

“The only reason to give a speech is to change the world.” An old friend of mine, a speechwriter, used to say that to me. He meant it as a challenge. It was his way of saying that, if you’re going to take all the trouble to prepare and deliver a speech, make it worthwhile. Change the world.

Otherwise, why bother? Preparing speeches, giving speeches, and listening to speeches—each of these activities is fraught with peril. The opportunities for failure are many, and for success correspondingly few. An oft-quoted study suggests that executives would rather die than speak. Of all their fears, public speaking is number one, and death comes much further down the list, just before nuclear war. That must explain why they often put off the task of preparing speeches to the last minute—or give the task to someone else.

If speechmaking is hard work for presenters, it’s also hard work for their audiences. Most business presentations are dreadful—boring, platitudinous, and delivered with a compelling lack of enthusiasm. People don’t remember much of what they learn from speeches—something on the order of 10 to 30 percent. With some business talks I’ve attended, that failure rate must be close to 100 percent. How many presentations have you sat through where your mind started wandering a few minutes into the talk and never really came back? Where you surreptitiously picked up your smartphone and started planning your calendar for the next millennium or two? Where you ended up more familiar with the number of acoustic tiles in the ceiling than the number of points in the outline of the speech?

So why do we bother? We bother giving speeches because of the opportunities they offer presenters with passion and a cause. There is something profound about gathering a group of people together in a hall and giving them the full force of your ideas presented live and in person. There is something essential about the intellectual, emotional, and physical connections a good speaker can make with an audience, something that cannot happen on the printed page. There is something powerful about the chemistry that happens in the moment of contact that no other medium can reproduce.

It’s what I call the kinesthetic connection. It’s something I’ve observed in over 25 years of teaching and coaching public speaking. When it happens, it’s powerful. When it’s missing, everyone feels it—even the hapless speaker.

Why People Will Always Give Speeches

We still need speeches. We need them to move audiences to action. People may learn to believe in your expertise from the printed page. But they will only be moved to action if they come to trust you from hearing and seeing you offer a solution to a problem they have. That kind of trust is visceral as well as intellectual and emotional, and it only comes from presence.

From the audience’s point of view, we still need to validate our impulse to action by seeing our champions, to test the sense of their messages and the integrity of their beings. Partly, we’re reading their nonverbal messages, those gestures and habits that we learn to interpret unconsciously for the most part, the ones that tell us something about the credibility and courage of the presenter. Partly, we’re testing to see if they can structure and present their ideas coherently in real time, abilities that tell us about how articulate and organized they are. And partly, we’re watching to see if we can find some sense of common humanity in the speaker, in order to make common cause with that speaker’s passion.

When Roger Mudd asked Ted Kennedy, on 60 Minutes in 1980, why he wanted to be president, Senator Kennedy famously fumbled the answer. Millions of Americans watched Kennedy at close hand, thanks to the eye of the camera, and judged his incoherent, rambling answer to lack credibility. The campaign was over almost before it began. Kennedy had changed the world—not in the way he intended, perhaps, but inescapably and irretrievably nonetheless. Potential backers slunk away from the Kennedy camp. Potential workers joined other campaigns. Potential voters resolved to find another candidate. And all of that happened through the faux-familiarity of television. Imagine how much more devastating it would have been in person.

Does changing the world seem like a daunting challenge? There’s good news buried in the challenge. With a powerful, audience-centered presentation, you can change the world. And that goes whether you’re talking to a small group of employees or colleagues—or a keynote audience of thousands. The principles are the same.

And there’s more good news to come: Regardless of how good you are now, you can learn how to give a better speech, one that makes a kinesthetic connection with your listeners. One that creates a sense of trust in you and moves them to action.

You Need to Listen to Your Audience

At the heart of this connection lies a counterintuitive truth: the secret to forming a strong bond between you and the people in the audience is to listen to them—from the very beginning.

Wait a minute, you say. I’m the one that has to do the talking. How can I listen to them? And what do you mean by kinesthetic? You’ve already used that word twice.

The answers to these questions are related. Let’s take the easy one first. Kinesthetic means being aware of the position and movement of the body in space. And to listen to the audience, you need to listen (and to show you’re listening) with your whole body. To give a simple example, consider the nervous executive in front of the shareholders for an annual meeting. He has some less-than-spectacular numbers to report, and everyone knows it. He’s prepared for the worst. He begins his talk with a curt, “Good morning,” arms folded, staring tensely over the audience members’ heads, looking into the middle distance, trying not to acknowledge the anger he sees in front of him. He immediately launches into a defensive talk aimed at minimizing the damage and second-guessing what the audience might ask him.

Not a pretty picture. Contrast that with a different executive in a similar pickle. She knows the meeting is going to be tough, but she’s ready. She stands up in front of the shareholders, smiles, and asks, “How are you?” Her arms are comfortably open at her sides. And she waits for a couple of seconds, making eye contact with at least one of the audience members on the right hand side of the room. Then she asks, no longer smiling, raising her eyebrows to invite response, “Are you angry about last year’s numbers? [Pause. Looking at someone else, on the left, now.] You have every right to be. We’re as disappointed as you are. Let’s talk about them. What’s on your mind?”

Not many chief executives would have the guts, frankly, to take the second approach. But which company would you rather hold stock in?

The second executive is well on the way to giving an audience-centered speech. She’s going to find kinesthetic moments to connect with her audience, and she’s begun by actually listening to them—reading their entire range of responses, including the nonverbal—from the start.

Indeed, even in this simplified example, the key to success is in making those rhetorical questions real. When you ask, “How are you?” of an audience, wait to see how some members of that audience actually are. Don’t continue until you’ve learned the answer, either verbally or nonverbally. It’s a small but vital way to begin an audience-centered talk. Success in public speaking is made up of a myriad little moments of connection like that.

And one big thing: charisma. That’s the magic quality, isn’t it? The one that everyone craves. And yet charisma doesn’t come from doing something difficult or esoteric that it takes years to master (and lots of expensive advice from speech coaches like me). We know now, thanks to the communications research of the last thirty years, what charisma is. Quite simply, it’s focused expressiveness. Expressiveness is the willingness to be open to your audience, both verbally and nonverbally. To show how you feel about your subject. To get past nervousness and self-consciousness and get to the stuff that you care about, and give that to the audience. That’s why they call it “giving a speech.” If you can unlock your own passion about the subject, and give that to the audience, in a focused way, you will be charismatic. The audience will not be able to take its eyes off you.

And so we’re back to audience-centered speaking, and kinesthetics. The only reason to give a speech is to change the world. You accomplish that by moving your audience to action. To do that, you have to be willing to listen to the audience, and to give it your passion. To get to that happy state, you need to find kinesthetic connections with the audience.

That’s audience-centered speaking in a paragraph. It’s a simple as that.

And lest you think that when I say “changing the world” I’m only talking about the big speeches (the ones that CEOs give to shareholders, for example) understand that I’m talking about every speech ever given. These principles apply to all public speaking, whether to five thousand people or five, for a grand public occasion or simply a regular meeting to report on 3Q numbers. After all, if you give a brilliant, inspiring, audience-centered presentation about those 3Q numbers, you will change the attitudes of your team in the room with you. And if you change their attitudes, you just might change their behavior. And if you change their behavior, you’ve changed the world in the only way that counts.

So that’s my wish for you in 2011: that you’ll start changing the world with every speech or presentation you give.

If you want to make sure yoru points are clear and communicated well consider contacting Nick and Public Words. Their clients have improved their communications dramatically for positive results. At the very least, pick up Nick’s books from Amazon or another source and use his recommendations – you’ll be glad you did! Reach out to Nick via his web site http://www.PublicWords.com

by Adam Hartung | Jan 5, 2011 | Defend & Extend, In the Rapids, In the Swamp, Leadership, Lock-in, Openness

Summary:

- Business planning systems are designed to defend historical markets

- Rapidly shifting markets makes it impossible to grow by defense alone

- Growth requires understanding what customers want, and creating new solutions that most likely aren’t part of the current business

- You can’t grow if you don’t plan to grow, but to plan for growth you have to shift resources from traditional planning into scenario planning

- High growth companies like Virgin, Apple and Google plan to fulfill future needs, not defend & extend past practicess

Imagine you see a pile of hay. Above it is a sign flashing “find the needle.” That achievement would be hard. Change the sign to “find the hay” and suddenly achieving the goal becomes much easier. So, as the comedian Bill Engvall might ask, what’s your sign? Unfortunately, most businesses plan for 2011, and beyond, using the first sign. Very few do planning using the latter. Most businesses won’t grow, because they simply don’t know how to plan for growth!!

Most businesses start planning with “I’m in the horseshoe (for example) business. My market isn’t growing, and there is more capacity than demand. How can I grow?” For these people, their sign is “find the needle.”

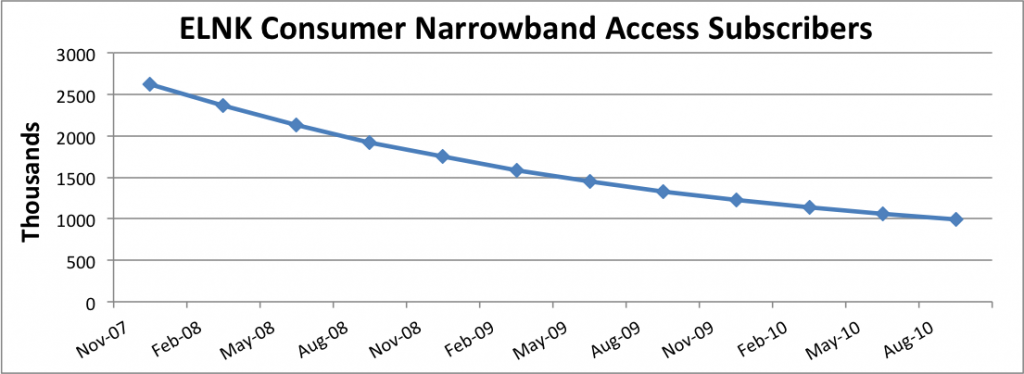

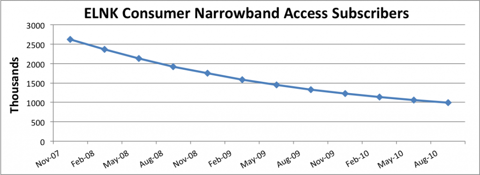

Take for example Earthlink. The company’s growth looked like a rocket ship in the early internet days as people by the millions signed up for dial-up service. But along came broadband, and the market for dial up died – never to return. Earthlink has no hope of growing as long as it thinks of itself as a dial-up company

Chart at SeekingAlpha.com author Ananthan Thangavel

Despite the absolute certainty that the market is shrinking, at this point almost all business planners will develop plans to defend this dying business as long as possible. Despite the impossibility of achieving good returns, there will be a plethora of actions to try and keep serving all the way to the very last customer. Just look at how AOL has invested millions trying to defend its dying internet access busiuness. Reality is, the company that walks away – gives up- is the smartest. There’s no way to make money as oversupply keeps too many companies spending too much to service too few customers.

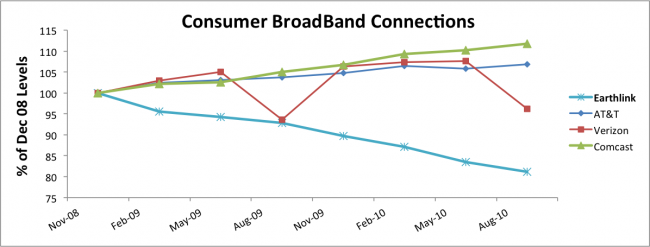

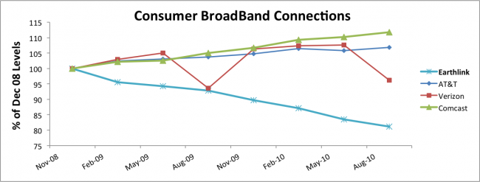

The next step for most planners is to attempt extending the business into something adjacent. For example, Earthlink would say “let’s invest in Broadband. We’ll hang onto customers as they want to switch, and maybe pick up a few customers.” But this completely ignores the fact that competitors already have a substantial lead. Competitors have learned the technology, and the marketplace. They are growing, and have no intention of giving up any room to a new competitor.

Chart at SeekingAlpha.com author Ananthan Thangavel

Planning systems are designed to keep the business doing more of what it always did, or possibly extending the business into adjacent markets after returns have faltered. Planning systems have no way of recognizing when a business, or market, has become obsolete. And practically never do they recognize the power of exsting competitors when looking at adjacent markets. As a result, the planning system produces no growth plans, leading 2011 to end with the self-fulfilling prophecy that the plan predicted – little or no growth.

The future for Earthlink is pretty grim. As it is for most companies that plan based upon history, trying to Defend & Extend their historical markets. In the highly dynamic, global marketplaces of 2011 trying to find growth by remaining focused on the past is like looking for the needle in a haystack. Maybe there’s something in there – but it’s not likely – and it’s even a lot less likely you’ll find it – and if you did, the cost of finding it will almost assuredly be greater than the value.

Alternatively, why not use planning resources to find, and develop, growth markets. Instead of looking at what you did (as in the past tense) try to figure out what you should do. Rather than studying past products, customers and markets, why not develop scenarios about the future that give you insight to what people will want to buy in 2011, 2012 and beyond? Rather than looking for needles, why not go explore the hay?

Newspapers kept focusing on declining subscriptions, when they should have been studying Craig’s List, eBay, Vehix.com and other on-line environments to learn the future of advertising. Had Tribune company poured its resources into its early internet investments, such as cars.com and careerbuilder.com, rather than trying to defend its traditional newspapers, it may well have avoided bankruptcy. But rather than looking to the future when doing its planning, and understanding that on-line news was going to explode, Tribune kept looking for the needle (cost cuts, layoffs, outsourcing, etc.) to save the old success formula.

Direct mail companies and Sunday insert printers have continued looking for ways to defend & extend their coupon printing business – despite the fact that nobody reads junk mail or uses printed coupons. Several have failed, and larger companies have merged trying to find “synergies” and more cost cuts. Simultaneously a 28 year old music major from Nothwestern university starts figuring out how to help companies acquire new customers by offering email coupons, and within 2 years his company, Groupon, is valued at around $6B. There’s nothing that stopped coupon powerhouse Advo from being Groupon, except that its planning system was devoted to finding the needle, while Groupon’s leaders decided to go play in the hay.

Hallmark and American Greetings want us to buy birthday and holiday cards for various occasions – in a world where almost nobody mails cards any longer. As they keep trying to defend their old business, and extend it into a few new opportunities for on-line cards, Twitter captures the wave of instant communications by offering everyone 140 character ways to communicate. Because Twitter is out where the growth is, the company raises $200M giving it a value of $3.7B.

Nothing stops any business from being anything it wants to be. But as most enter 2011 they will use their planning resources, including all those management meetings and hours of forms completion, to do nothing more than re-examine the historical business. Most will devolve into trying to figure out how to do more with less. As future forecasts look grim, or perhaps cautiously optimistic (based on a lot of things going right – like a mysterious pick-up in demand) there will be much nashing of teeth – and meetings looking for a needle that can be offered to employees and investors as a hope for rising future value.

Smart companies get out of that rut. They focus their planning on the future. What do customers want, and how can we give them what they want? How can we create whole new markets. Apple was a PC company, but by exploring mobility it became a provider of MP3 consumer electronics, downloadable music, a mobile device and app supplier and the early winner in cloud accessing tablets. Google has moved from a search engine to a powerhouse ad placement company and is pushing the edges of growth in mobile computing as well as several other markets. Virgin started as a distributor of long-playing vinyl record albums, but by exploring what customers really wanted it has become an international airline, cell phone company, international lender and space travel pioneer (to mention just a few of its businesses.)

You can grow in 2011, but to do so you need to shed the old planning system (and its resource wasting processes) and get serious about scenario planning. Focus on the future, not the past.