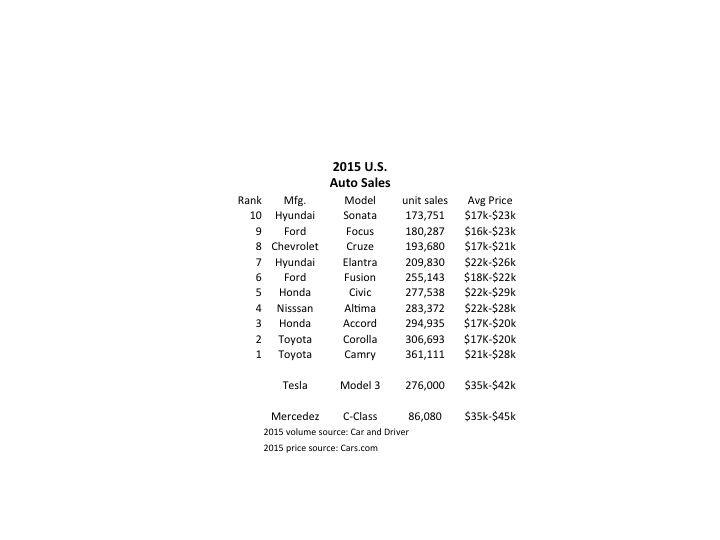

Tesla started taking orders for the Model 3 last week, and the results were remarkable. In 24 hours the company took $1,000 deposits for 198,000 vehicles. By end of Saturday the $1,000 deposits topped 276,000 units. And for a car not expected to be available in any sort of volume until 2017. Compare that with the top selling autos in the U.S. in 2015:

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]

Even more astonishing is the average selling price. Note that top 10 cars are not highly priced, mostly in the $17,000 to $25,000 price range. But the Tesla is base priced at $35,000, and expected with options to sell closer to $42,000. That is almost twice as expensive as the typical top 10 selling auto in the U.S.

Tesla has historically been selling much more expensive cars, the Model S being its big seller in 2015. So if we classify Tesla as a “luxury” brand and compare it to like-priced Mercedes Benz C-Class autos we see the volumes are, again, remarkable. In under 1 week the Model 3 took orders for 3 times the volume of all C-Class vehicles sold in the U.S. in 2015.

Although this has surprised a large number of people, the signs were all pointing to something extraordinary happening. The Tesla Model S sold 50,000 vehicles in 2015 at an average price of $70,000 to $80,000. That is the same number of the Mercedes E-Class autos, which are priced much lower in the $50,000 range. And if you compare to the top line Mercedes S-Class, which is only slightly more expensive at an average $90,0000, the Model S sold over 2 times the 22,000 units Mercedes sold. And while other manufacturers are happy with single digit percentage volume growth, in Q4 Tesla shipments were 75% greater in 2015 than 2014.

In other words, people like this brand, like these cars and are buying them in unprecedented numbers. They are willing to plunk down deposits months, possibly years, in advance of delivery. And they are paying the highest prices ever for cars sold in these volumes. And demand clearly outstrips supply.

Yet, Tesla is not without detractors. From the beginning some analysts have said that high prices would relegate the brand to a small niche of customers. But by outselling all other manufacturers in its price point, Tesla has demonstrated its cars are clearly not a niche market. Likewise many analysts argued that electric cars were dependent on high gasoline prices so that “economic buyers” could justify higher prices. Yet, as gasoline prices have declined to prices not seen for nearly a decade Tesla sales keep going up. Clearly Tesla demand is based on more than just economic analysis of petroleum prices.

People really like, and want, Tesla cars. Even if the prices are higher, and if gasoline prices are low.

Which leads us to the beauty of sales growth. When products tap an under- or unfilled need they frequently far outsell projections. Think about the iPod, iPhone and iPad. There is naturally concern about scaling up production. Will the money be there? Can the capacity come online fast enough?

Of course, of all the problems in business this is one every leader should want. It is certainly a lot more fun to worry about selling too much rather than selling too little. Especially when you are commanding a significant price premium for your product, and thus can be sure that demand is not an artificial, price-induced variance.

With rare exceptions, investors understand the value of high sales at high prices. When gross margins are good, and capacity is low, then it is time to expand capacity because good returns are in the future. The Model 3 release projects a backlog of almost $12B. Booked orders at that level are extremely rare. Further, short-term those orders have produced nearly $300million of short-term cash. Thus, it is a great time for an additional equity offering, possibly augmented with bond sales, to invest rapidly in expansion. Problematic, yes. Insolvable, highly unlikely.

On the face of it Tesla appears to be another car company. But something much more significant is afoot. This sales level, at these prices, when the underlying economics of use seem to be moving in the opposite direction indicates that Tesla has tapped into an unmet need. It’s products are impressing a large number of people, and they are buying at premium prices. Based on recent orders Tesla is vastly outselling competitive electric automobiles made by competitors, all of whom are much bigger and better resourced. And those are all the signs of a real Game Changer.

Many people equate spending on R&D with investing in innovation. The logic goes that R&D spending is lab spending, and out of labs come innovations. Hence, those that spend a lot on R&D are innovative.

That is faulty logic.

This chart shows R&D spending from the top 20 companies in 2011:

Think of your own list of companies that are providing innovations which change your work, or life. Would you include Apple? Amazon? Facebook? Google? Genentech? (Here's the link to Fast Company's 50 most innovative for 2012). Note that none of these companies appear on the list of top R&D spenders.

On the other hand, as you look at the big spender list some things might be apparent:

Microsoft is #5, spending $9B and nearly 13% of revenue. Yet, for this money in 2012 the world received updates to their aging operating system and office automation software. Both of which failed to register favorable reviews by industry gurus, and are considered far from innovative. And Nokia, which is so floundering some consider it a likely bankruptcy candidate soon, is #7! Despite spending nearly $8B on R&D Nokia is now completely reliant on Microsoft if it is to even survive.

Autos make up a big part of the group. Toyota, GM, Volkswagen, Honda and Daimler are all on the list, spending a whopping $36B. Yet, even though they give us improvements nobody considers them (especially GM) very innovative. That award would go to little Tesla Motors. Or maybe Tata Motors in India.

Pharmaceuticals make up the dominant industry. Novartis, Roche, Pfizer, Merck, Johnson & Johnson, Sanofi, GlaxoSmithKline and AstraZeneca are all here – spending a cumulative $54B! Yet, they have all failed to give the world any incredible new drugs, all have profit struggles, and the industry is rife with discussions about weak product pipelines. The future of modern medicine increasingly is shifting to genetic solutions, biologics and more specific alternatives to the historical drug regimes from these aging pharma R&D programs.

Do you see the obvious pattern? Most big R&D spenders are not really seeking innovations. They are spending money on historical programs, following historical patterns and trying to defend and extend the historical business. In other words, they are spending vast sums attempting to sustain (or recapture) historical success. And, as the list shows, largely doing a pretty lousy job of it.

If you were given $10,000 to invest would you select these top 20 R&D spenders – or would you look for other, more innovative companies. From a profitability, rate of return and trend perspective, most of these companies look weak – or downright horrible.

Innovators don't focus on what they spend, but where they spend it.

The companies most known for innovation don't keep spending money year after year on their old business. Instead of digging deeper into what they already know, they invest laterally. They spend money putting the pieces together in new, unique ways. They try to find new solutions to old problems, using new – even fringe – technologies. They try to develop disruptive solutions that actually change the marketplace, rather than trying to make something that already exists better, faster or cheaper.

Lots of people like to think there is "scale" in research. Bigger is better. What's more important, for investors, is that there is "diminishing returns." The more you research an area the more you have to spend to find anything new. The costs keep escalating, as the gains shrink. After investing for a while, continuing to research an area is not a good investment (although it may be very intellectually interesting.)

Most of the companies on this list would be smarter to scrap their existing R&D programs, cut the budget in half (at least,) and then invest it somewhere very different. Instead of looking deeper, they need to look wider – broader. They need to investigate alternative solutions, rather than more of the same. They need to be putting more money on fringe opportunities, and a lot less into the core.

Until they do, few on this list are very good investment bets. You'll do better investing like, and in, the real innovators.

The news is not good for U.S. auto companies. Automakers are resorting to fairly radical promotional programs to spur sales. Chevrolet is offering a 60-day money back guarantee. And Chrysler is offering 90 day delayed financing. Incentives designed to make you want to buy a car, when you really don't want to buy a car. At least, not the cars they are selling.

On the other hand, the barely known, small and far from mainstream Tesla motors gave one of its new Model S cars to Wall Street Journal reviewer Dan Neil, and he gave it a glowing testimonial. He went so far as to compare this 4-door all electric sedan's performance with the Lamborghini and Ford GT supercars. And its design with the Jaguar. And he spent several paragraphs on its comfort, quiet, seating and storage – much more aligned with a Mercedes S series.

There are no manufacturer incentives currently offered on the Tesla Model S.

What's so different about Tesla and GM or Ford? Well, everything. Tesla is a classic case of a disruptive innovator, and GM/Ford are classic examples of old-guard competitors locked into sustaining innovation. While the former is changing the market – like, say Amazon is doing in retail – the latter keeps laughing at them – like, say Wal-Mart, Best Buy, Circuit City and Barnes & Noble have been laughing at Amazon.

Tesla did not set out to be a car company, making a slightly better car. Or a cheaper car. Or an alternative car. Instead it set out to make a superior car.

Its initial approach was a car that offered remarkable 0-60 speed performance, top end speed around 150mph and superior handling. Additionally it looked great in a 2-door European style roadster package. Simply, a wildly better sports car. Oh, and to make this happen they chose to make it all-electric, as well.

It was easy for Detroit automakers to scoff at this effort – and they did. In 2009, while Detroit was reeling and cutting costs – as GM killed off Pontiac, Hummer, Saab and Saturn – the famous Bob Lutz of GM laughed at Tesla and said it really wasn't a car company. Tesla would never really matter because as it grew up it would never compete effectively. According to Mr. Lutz, nobody really wanted an electric car, because it didn't go far enough, it cost too much and the speed/range trade-off made them impractical. Especially at the price Tesla was selling them.

Like all disruptive innovators, Tesla did not make a car for the "mass market." Tesla made a great car, that used a different technology, and met different needs. It was designed for people who wanted a great looking roadster, that handled really well, had really good fuel economy and was quiet. All conditions the electric Tesla met in spades. It wasn't for everyone, but it wasn't designed to be. It was meant to demonstrate a really good car could be made without the traditional trade-offs people like Mr. Lutz said were impossible to overcome.

Now Tesla has a car that is much more aligned with what most people buy. A sedan. But it's nothing like any gasoline (or diesel) powered sedan you could buy. It is much faster, it handles much better, is much roomier, is far quieter, offers an interface more like your tablet and is network connected. It has a range of distance options, from 160 to 300 miles, depending up on buyer preferences and affordability. In short, it is nothing like anything from any traditional car maker – in USA, Japan or Korea.

Again, it is easy for GM to scoff. After all, at $97,000 (for the top-end model) it is a lot more expensive than a gasoline powered Malibu. Or Ford Taurus.

But, it's a fraction of the price of a supercar Ferrari – or even a Porsche Panamera, Mercedes S550, Audi A8, BMW 7 Series, or Jaguar XF or XJ - which are the cars most closely matching size, roominess and performance.

And, it's only about twice as expensive as a loaded Chevy Volt – but with a LOT more advantages. The Model S starts at just over $57,000, which isn't that much more expensive than a $40,000 Volt.

In short, Tesla is demonstrating it CAN change the game in automobiles. While not everybody is ready to spend $100k on a car, and not everyone wants an electric car, Tesla is showing that it can meet unmet needs, emerging needs and expand into more traditional markets with a superior solution for those looking for a new solution. The way, say, Apple did in smartphones compared to RIM.

Why didn't, and can't, GM or Ford do this?

Simply put, they aren't even trying. They are so locked-in to their traditional ideas about what a car should be that they reject the very premise of Tesla. Their assumptions keep them from really trying to do what Tesla has done – and will keep improving – while they keep trying to make the kind of cars, according to all the old specs, they have always done.

Rather than build an electric car, traditionalists denounce the technology. Toyota pioneered the idea of extending a gas car into electric with hybrids – the Prius – which has both a gasoline and an electric engine.

Hmm, no wonder that's more expensive than a similar sized (and performing) gasoline (or diesel) car. And, like most "hybrid" ideas it ends up being a compromise on all accounts. It isn't fast, it doesn't handle particularly well, it isn't all that stylish, or roomy. And there's a debate as to whether the hybrid even recovers its price premium in less than, say, 4 years. And that is all dependent upon gasoline prices.

Ford's approach was so clearly to defend and extend its traditional business that its hybrid line didn't even have its own name! Ford took the existing cars, and reformatted them as hybrids, with the Focus Hybrid, Escape Hybrid and Fusion Hybrid. How is any customer supposed to be excited about a new concept when it is clearly displayed as a trade-off; "gasoline or hybrid, you choose." Hard to have faith in that as a technological leap forward.

And GM gave the market Volt. Although billed as an electric car, it still has a gasoline engine. And again, it has all the traditional trade-offs. High initial price, poor 0-60 performance, poor high-end speed performance, doesn't handle all that well, isn't very stylish and isn't too roomy. The car Tesla-hating Bob Lutz put his personal stamp on. It does achieve high mpg – compared to a gasoline car – if that is your one and only criteria.

Investors are starting to "get it."

There was lots of excitement about auto stocks as 2010 ended. People thought the recession was ending, and auto sales were improving. GM went public at $34/share and rose to about $39. Ford, which cratered to $6/share in July, 2010 tripled to $19 as 2011 started.

But since then, investor enthusiasm has clearly dropped, realizing things haven't changed much in Detroit – if at all. GM and Ford are both down about 50% – roughly $20/share for GM and $9.50/share for Ford.

Meanwhile, in July of 2010 Tesla was about $16/share and has slowly doubled to about $31.50. Why? Because it isn't trying to be Ford, or GM, Toyota, Honda or any other car company. It is emerging as a disruptive alternative that could change customer perspective on what they should expect from their personal transportation.

Like Apple changed perspectives on cell phones. And Amazon did about retail shopping.

Tesla set out to make a better car. It is electric, because the company believes that's how to make a better car. And it is changing the metrics people use when evaluating cars.

Meanwhile, it is practically being unchallenged as the existing competitors – all of which are multiples bigger in revenue, employees, dealers and market cap of Tesla – keep trying to defend their existing business while seeking a low-cost, simple way to extend their product lines. They largely ignore Tesla's Roadster and Model S because those cars don't fit their historical success formula of how you win in automobile competition.

The exact behavior of disruptors, and sustainers likely to fail, as described in The Innovator's Dilemma (Clayton Christensen, HBS Press.)

Choosing to be ignorant is likely to prove very expensive for the shareholders and employees of the traditional auto companies. Why would anybody would ever buy shares in GM or Ford? One went bankrupt, and the other barely avoided it. Like airlines, neither has any idea of how their industry, or their companies, will create long-term growth, or increase shareholder value. For them innovation is defined today like it was in 1960 – by adding "fins" to the old technology. And fins went out of style in the 1960s – about when the value of these companies peaked.

Why do some businesses (or products) seem to launch onto the scene with incredible success? According to a new book, “Enchantment” releasing March 8, 2011 (available on Amazon.com at about 50% off the list price), it is the ability to go beyond normal marketing, PR and other business practices in a way that enchants customers. Author Guy Kawasaki says that being likable, trustworthy and prepared allows you to overcome natural resistance to change and move people to accept, adopt – and even become supporters of your solution.

The book is tailor-made for entrepreneurs. Especially those in high-tech, who are looking for rapid adoption of new platforms. So when Guy sent me a copy and asked for my review I asked him for a 1-on-1 interview where I could focus on how the vast majority of people, who work away in large, less than enchanting, organizations, could gain value from reading his latest effort. I wanted him to answer “how am I supposed to be enchanting when dullness reigns in my environment?”

Here’s his finput from our meeting, and his reasons to buy and read Enchantment:

Guy’s first recommendation – “enchant your boss.” There’s a chapter in the book, but he focused on what to do if your boss is a real dullard. Firstly, don’t ever forget to make the boss’s priority your priority, because without that you won’t be effective. The more you can convince your boss the 2 of you are on the same wavelength, the more he’ll be likely to give you space. And space is what you want/need in order to start to identify the next perfomance curve. Then, if you have some space, you can start to demonstrate how new solutions could work. Use your aligned priorities to help you reframe your boss’s opinion about the future, and always ask for forgiveness if you’re found reaching a bit too far.

Secondly, enchant those who work for you. Give them a MAP. (M) is for Mastery of a new skill or technology. Give your employees permission and encouragement to master new areas that will help them grow – and put them in a position to teach you! (A) is for Autonomy. In other words, give them the space discussed above. (P) is for Purpose. Help people to see their work as having more value than just money. Add purpose to their results so they can feel great. With a MAP they can succeed, and you can too.

Thirdly, enchant your peers by working hard to be likable. Guy offers a chapter in which he deconstructs likability, and provides a series of tactics to make you more likable. This isn’t manipulation (although it may sound like it), but rather a guidebook of what to do to help your true self be more likable. With peers, the #1 objective is to be trustworthy! Show them that you can help expand the pie, so there is more success for everyone, rather than being the kind of person always lining up to get his piece first!

When you find yourself disappointed in your work, or employer, Guy recommends we take from his book the idea that you seek out a dream for what your work group, or employer, can be. Don’t accept that today is the best case, and instead promote the notion that tomorrow can always be better, more fun, more fulfilling. He believes that if you say you’re going to do something that seems impossible, and you undertake it with enchanting techniques, your behavior will become infectious. Behave like an enchanter and you will create other enchanters in the organization. (If this sounds a bit Pied Piper-ish I guess it does take some faith to follow Guy’s recommendations.)

I asked him how a Chief Enchantment Officer could help Microsoft (readers of this blog know I’ve long been a distractor of the strategy and CEO at Microsoft). Guy said he felt Micrsoft could become VERY enchanting if the company would:

Focus on making Micrsooft more likable and trustworthy. Old behaviors were in the past. Going forward, if leadership applied itself Microsoft could implement the things in his book and drive up the company’s likability and trustworthiness amongst constituents – including customers, developers, suppliers and investors.

Rethink the definition of a “product” to make offerings more enchanting. In Guy’s view, Apple would never say a product is good enough based upon its specifications or functionality. An iPad has to go beyond those things to offer something much more. Too many companies (not just, or even specifically, Microsoft he was clear to point out) launch “ugly” products – without realizing they are ugly! With a bit different direction, different thinking, about how to define a product they could be more enchanting, and more successful. (When I compare the iPhone or iPad to the xBox I start to clearly see the difference in product description to which Guy refers. Guy agreed with me that Kinect is a very enchanting product. Unfortunately it appears to me like Microsoft still doesn’t realize the value of this in its xBox efforts.)

Train the organization on the importance of, value of, and ability to be enchanting. Most companies are clueless about the notion, as people work hard delivering solutions with too much of an “engineering mentality”. Apple has trained its organization so the people think about how to make products, services and solutions enchanting, and therefore non-enchanting things are unacceptable. Raise the bar for making sure solutions are likable, trustworthy and prepared for what the customer will want/need. Not merely functional. Build that into the behavioral lock-in and Guy believes any organization cannot miss success!

I told Guy that often I’m frequently pushed to believe that a company is “beyond the pale;” unable to do better, or to be better. Simply incapable fo ever being “enchanting.” Guy is convinced this is balderdash – if you want to change. He talked about Audi, which suffered horribly from problems with unintended acceleration a couple of decades ago. Audi changed itself, and now is doing quite well (according to Guy) while Toyota is suffering. It’s easy for an organization to slip into dis-enchanting behavior over time if it starts cost-cutting and obsessing about optimizing its past. But any company can become enchanting again. “Hey, look at how Apple slipped, then came back, and you can see how enchantment is possible for any company.”

I don’t know that Enchantment will solve all your business problems, but for $14 (and free shipping on Amazon.com) it’s full of ideas about how you can move a company to better performance. And surely make it a better, more compelling place to work!

Guy Kawasaki became famous as a Macintosh Evangelist for Apple back in the 1980s. His passion for creating technology products that help people’s lives, and work, improve, has been compelling for 2 decades. His blog is entitled “How to Change the World,” demonstrating how high Guy sets his sites. Guy also created and remains active in Alltop.com, a compendium of blog listings on important topics, where ThePhoenixPrinciple.com is part of the Innovation section.

"From the day we start kindergarten we fear the teacher's call to our

parents saying, "Hello Mr. and Mrs. Smith. I'm sorry to tell you that

Mary has been disruptive in class." We are taught, trained and

indoctrinated to go along and get along, to not disrupt. In fact we're

constantly told to seek harmony. But in business that can destroy your

entire value."

That's the first paragraph from my Forbes.com column, posted today,"To Succeed You Must Seriously Disrupt." Companies that don't Disrupt remain Locked-in to Success Formulas with declining value until all hope is lost – just look at Sun Microsystems. Although Chairman Scott McNealy was famous for his Disruptive corporate behavior – he was unwilling to tolerate disruptions from his own organization to the company business model. In 10 years Sun went from $200B market cap to out of business.

Now Toyota is struggling because it wouldn't Disrupt. Meanwhile Honda is doing much better than most, because it is willing to Disrupt. Listen to the 40 second video on Disruptions, and read the article so you can see the need for Disruption and adopt in your business!

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]