Anyone who reads my column knows I’ve been no fan of Steve Ballmer as CEO of Microsoft. On multiple occasions I chastised him for bad decisions around investing corporate funds in products that are unlikely to succeed. I even called him the worst CEO in America. The Washington Post even had difficulty finding reputable folks to disagree with my argument.

Unfortunately, Microsoft suffered under Mr. Ballmer. And Windows 8, as well as the Surface tablet, have come nowhere close to what was expected for their sales – and their ability to keep Microsoft relevant in a fast changing personal technology marketplace. In almost all regards, Mr. Ballmer was simply a terrible leader, largely because he had no understanding of business/product lifecycles.

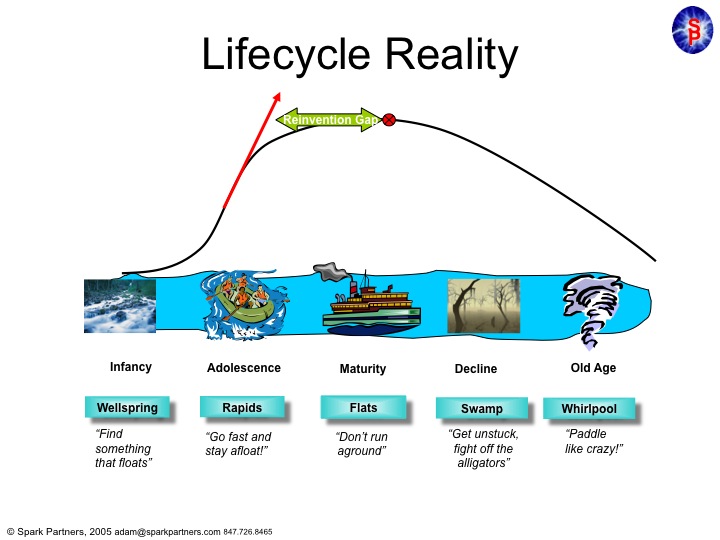

Microsoft was founded by Bill Gates, who did a remarkable job of taking a start-up company from the Wellspring of an idea into one of the fastest growing adolescents of any American company.

Under Mr. Gates leadership Microsoft single-handedly overtook the original PC innovator – Apple – and left it a niche company on the edge of bankruptcy in little over a decade.

Mr. Gates kept Microsoft’s growth constantly in the double digits by not only making superior operating system software, but by pushing the company into application software which dominated the desktop (MS Office.) And when the internet came along he had the vision to be out front with Internet Explorer which crushed early innovator, and market maker, Netscape.

But then Mr. Gates turned the company over to Mr. Ballmer. And Mr. Ballmer was a leader lacking vision, or innovation. Instead of pushing Microsoft into new markets, as had Mr. Gates, he allowed the company to fixate on constant upgrades to the products which made it dominant – Windows and Office. Instead of keeping Microsoft in the Rapids of growth, he offered up a leadership designed to simply keep the company from going backward. He felt that Microsoft was a company that was “mature” and thus in need of ongoing enhancement, but not much in the way of real innovation. He trusted the market to keep growing, indefinitely, if he merely kept improving the products handed him.

As a result Microsoft stagnated. A “Reinvention Gap” developed as Vista, Windows 7, then Windows 8 and one after another Office updates did nothing to develop new customers, or new markets. Microsoft was resting on its old laurels – monopolistic control over desktop/laptop markets – without doing anything to create new markets which would keep it on the old growth trajectory of the Gates era.

Things didn’t look too bad for several years because people kept buying traditional PCs. And Ballmer famously laughed at products like Linux or Unix – and then later at entertainment devices, smart phones and tablets – as Microsoft launched, but then abandoned products like Zune, Windows CE phones and its own tablet. Ballmer kept thinking that all the market wanted was a faster, cheaper PC. Not anything really new.

And he was dead wrong. The Reinvention Gap emerged to the public when Apple came along with the iPod, iTunes, iPhone and iPad. These changed the game on Microsoft, and no longer was it good enough to simply have a better edition of an outdated technology. As PC sales began declining it was clear that Ballmer’s leadership had left the company in the Swamp, fighting off alligators and swatting at mosquitos with no strategy for how it would regain relevance against all these new competitors.

So the Board pushed him out, and demoted Gates off the Chairman’s throne. A big move, but likely too late. Fewer than 7% of companies that wander into the Swamp avoid the Whirlpool of demise. Think Univac, Wang, Lanier, DEC, Cray, Sun Microsystems (or Circuit City, Montgomery Wards, Sears.) The new CEO, Satya Nadella, has a much, much more difficult job than almost anyone thinks. Changing the trajectory of Microsoft now, after more than a decade creating the Reinvention Gap, is a task rarely accomplished. So rare we make heros of leaders who do it (Steve Jobs, Lou Gerstner, Lee Iacocca.)

So what will happen at the Clippers?

Critically, owning an NBA team is nothing like competing in the real business world. It is a closed marketplace. New competitors are not allowed, unless the current owners decide to bring in a new team. Your revenues are not just dependent upon you, but are even shared amongst the other teams. In fact your revenues aren’t even that closely tied to winning and losing. Season tickets are bought in advance, and with so many games away from home a team can do quite poorly and still generate revenue – and profit – for the owner. And this season the Indiana Pacers demonstrated that even while losing, fans will come to games. And the Philadelphia 76ers drew crowds to see if they would set a new record for the most consecutive games lost.

In America the major sports only modestly overlap, so you have a clear season to appeal to fans. And even if you don’t make it into the playoffs, you still share in the profits from games played by other teams. As a business, a team doesn’t need to win a championship to generate revenue – or make a profit. In fact, the opposite can be true as Wayne Huizenga learned owning the Championship winning Florida Marlins baseball team. He payed so much for the top players that he lost money, and ended up busting up the team and selling the franchise!

In short, owning a sports franchise doesn’t require the owner to understand lifecycles. You don’t have to understand much about business, or about business competition. You are protected from competitors, and as one of a select few in the club everyone actually works together – in a wholly uncompetitive way – to insure that everyone makes as much money as possible. You don’t even have to know anything about managing people, because you hire coaches to deal with players, and PR folks to deal with fans and media. And as said before whether or not you win games really doesn’t have much to do with how much money you make.

Most sports franchise owners are known more for their idiosyncrasies than their business acumen. They can be loud and obnoxious all they want (with very few limits.) And now that Mr. Ballmer has no investors to deal with – or for that matter vendors or cooperative parties in a complex ecosystem like personal technology – he doesn’t have to fret about understanding where markets are headed or how to compete in the future.

When it comes to acting like a person who knows little about business, but has a huge ego, fiery temper and loves to be obnoxious there is no better job than being a sports franchise owner. Mr. Ballmer should fit right in.

Microsoft needed a great Christmas season. After years of product stagnation, and a big market shift toward mobile devices from PCs, Microsoft's future relied on the company seeing customers demonstrate they were ready to jump in heavily for Windows8 products – including the new Surface tablet.

Looking deeper, for the 4th quarter PC sales declined by almost 5% according to Gartner research, and by almost 6.5% according to IDC. Both groups no longer expect a rebound in PC shipments, as they believe homes will no longer have more than 1 PC due to the mobile device penetration – the market where Surface and Win8 phones have failed to make any significant impact or move beyond a tiny market share. Users increasingly see the complexity of shifting to Win8 as not worth the effort; and if a switch is to be made consumer and businesses now favor iOS and Android.

These trends mean nothing short of the ruin of Microsoft. Microsoft makes more than 75% of its profits from Windows and Office. Less than 25% comes from its vaunted servers and tools. And Microsoft makes nothing from its xBox/Kinect entertainment division, while losing vast sums on-line (negative $350M-$750M/quarter). No matter how much anyone likes the non-Windows Microsoft products, without the historical Windows/Office sales and profits Microsoft is not sustainable.

So what can we expect at Microsoft:

Ballmer has committed to fight to the death in his effort to defend & extend Windows. So expect death as resources are poured into the unwinnable battle to convert users from iOS and Android.

As resources are poured out of the company in the Quixotic effort to prolong Windows/Office, any hope of future dividends falls to zero.

Expect enormous layoffs over the next 3 years. Something like 50-60%, or more, of employees will go away.

Expect closure of the long-suffering on-line division in order to conserve resources.

The entertainment division will be spun off, sold to someone like Sony or even Barnes & Noble, or dramatically reduced in size. Unable to make a profit it will increasingly be seen as a distraction to the battle for saving Windows – and Microsoft leadership has long shown they have no idea how to profitably grow this business unit.

As more and more of the market shifts to competitive cloud businesses Apple, Amazon and others will grow significantly. Microsoft, losing its user base, will demonstrate its inability to build a new business in the cloud, mimicking its historical experiences with Zune (mobile music) and Microsoft mobile phones. Microsoft server and tool sales will suffer, creating a much more difficult profit environment for the sole remaining profitable division.

Missing the market shift to mobile has already forever tarnished the Microsoft brand. No longer is Microsoft seen as a leader, and instead it is rapidly losing market relevancy as people look to Apple, Google, Amazon, Samsung, Facebook and others for leadership. The declining sales, and lack of customer interest will lead to a tailspin at Microsoft not unlike what happened to RIM. Cash will be burned in what Microsoft will consider an "epic" struggle to save the "core of the company."

But failure is already inevitable. At this stage, not even a new CEO can save Microsoft. Steve Ballmer played "Bet the Company" on the long-delayed release of Win8, losing the chance to refocus Microsoft on other growing divisions with greater chance of success. Unfortunately, the other players already had enough chips to simply bid Microsoft out of the mobile game – and Microsoft's ante is now long gone – without holding a hand even remotely able to turn around the product situation.

Game over. Ballmer loses. And if you keep your money invested in Microsoft it will disappear along with the company.

Steve Ballmer received only half his maximum bonus for last year

But Microsoft has failed at almost every new product initiative the last several years

Microsoft's R&D costs are wildly out of control, and yielding little new revenue

Microsoft is lagging in all new growth markets – without competitive products

Microsoft's efforts at developing new markets have created enormous losses

Cloud computing could obsolete Microsoft's "core" products

Why didn't the Board fire Mr. Ballmer?

Reports are out, including at AppleInsider.com that "Failures in Mobile Space Cost Steve Ballmer Half his Bonus." Apparently the Board has been disappointed that under Mr. Ballmer's leadership Microsoft has missed the move to high growth markets for smartphones and tablets. Product failures, like Kin, have not made them too happy. But the more critical question is — why didn't the Board fire Mr. Ballmer?

A decade ago Microsoft was the undisputed king of personal software. Its near monopoly on operating systems and office automation software assured it a high cash flow. But over the last 10 years, Microsoft has done nothing for its shareholders or customers. The XBox has been a yawn, far from breaking even on the massive investments. All computer users have received for massive R&D investments are Vista, Windows 7 and Office 2007 followed by Office 2010 — the definition of technology "yawners." None of the new products have created new demand for Microsoft, brought in any new customers or expanded revenue. Meanwhile, the 45% market share Microsoft had in smartphones has shrunk to single digits, at best, as Apple and Google are cleaning up the marketplace. Early editions of tablets were dropped, and developers such as HP have abandoned Microsoft projects.

Yet, other tech companies have done quite well. Even though Apple was 45 days from bankruptcy in 2000, and Google was a fledgling young company, both Apple and Google have launched new products in smartphones, mobile computing and entertainment. And Apple has sold over 4 million tablets already in 2010 – while investors and customers wait for Microsoft to maybe get one to market in 2011.

Despite its market domination, Microsoft's revenues have gone nowhere. And are projected to continue going relatively nowhere. While Apple has developed new growth markets, Microsoft has invested in defending its historical revenue base.

Yet, Microsoft spent 8 times as much on R&D in 2009 to accomplish this much lower revenue growth. At a recent conference Mr. Ballmer admitted he thought as much as 200 man years of effort was wasted on Vista development in recent years. That Microsoft has hit declining rates of return on its investment in "defending the base" is quite obvious. Equally obvious is its clear willingness to throw money at projects even though it has no skill for understanding market needs sin order for development to yield anything commercially successful!

And investments in opportunities outside the "core" business have not only failed to produce significant revenue, they've created vast losses. Such as the horrible costs incurred in on-line markets. Trying to launch Bing and compete with Google in ad sales far too late and with weak products has literally created losses that exceed revenues!

And the result has been a disaster for Microsoft shareholders – literally no gain the last several years. This has allowed Apple to create a market value that actually exceeds Microsoft's. An idea that seemed impossible during most of the decade!

Under Mr. Ballmer's leadership Microsoft has done nothing more than protect market share in its original business – and at a huge cost that has not benefited shareholders with dividends or growth. No profitable expansion into new businesses, despite several newly emerging markets. And now late in practically every category. Costs for business development that are wildly out of control, despite producing little incremental revenue. And sitting on a business in operating systems and office software that is coming under more critical attack daily by the shift toward cloud computing. A shift that could make its "core" products entirely obsolete before 2020.

Given this performance, giving Mr. Ballmer his "target" bonus for last year seems ridiculous – even if half the maximum. The proper question should be why does he still have his job? And if you still own Microsoft stock — why as well?

Google is growing, and GM is trying to get out of bankruptcy. On the surface there are lots of obvious differences. Different markets, different customers, different products, different size of company, different age. But none of these get to the heart of what's different about the two companies. None of these really describe why one is doing well while the other is doing poorly.

GM followed, one could even say helped create, the "best practices" of the industrial era. GM focused on one industry, and sought to dominate that market. GM eschewed other businesses, selling off profitable businesses in IT services and aircraft electronics. Even selling off the parts business for its own automobiles. GM focused on what it knew how to do, and didn't do anything else.

GM also figured out its own magic formula to succeed, and then embedded that formula into its operating processes so the same decisions were replicated again and again. GM Locked-in on that Success Formula, doing everything possible to Defend & Extend it. GM built tight processes for everything from procurement to manufacturing operations to new product development to pricing and distribution. GM didn't focus on doing new things, it focused on trying to make its early money making processes better. As time went by GM remained committed to reinforcing its processes, believing every year that the tide would turn and instead of losing share to competitors it would again gain share. GM believed in doing what it had always done, only better, faster and cheaper. Even into bankruptcy, GM believed that if it followed its early Success Formula it would recapture earlier rates of return.

Google is an information era company, defining the new "best practices". It's early success was in search engine development, which the company turned into a massive on-line advertising placement business that superceded the first major player (Yahoo!). But after making huge progress in that area, Google did not remain focused alone on doing "search" better year after year. Since that success Google has also launched an operating system for mobile phones (Android), which got it into another high-growth market. It has entered the paid search marketplace. And now, "Google takes on Windows with Chrome OS" is the CNN headline.

"Google to unveil operating system to rival Microsoft" is the Marketwatch headline. This is not dissimilar from GM buying into the airline business. For people outside the industry, it seems somewhat related. But to those inside the industry this seems like a dramatic move. For participants, these are entirely different technologies and entirely different markets. Not only that, but Microsoft's Windows has dominated (over 90% market share) the desktop and laptop computer markets for years. To an industrial era strategist the Windows entry barriers would be considered insurmountable, making it not worthwhile to pursue any products in this market.

Google is unlike GM in that

it has looked into the future and recognizes that Windows has many obstacles to operating effictively in a widely connected world. Future scenarios show that alternative products can make a significant difference in the user experience, and even though a company currently dominates the opportunity exists to Disrupt the marketplace;

Google remains focused on competitors, not just customers. Instead of talking to customers, who would ask for better search and ad placement improvements, Google has observed alternative, competitive operating system products, like Unix and Linux, making headway in both servers and the new netbooks. While still small share, these products are proving adept at helping people do what they want with small computers and these customers are not switching to Windows;

Google is not afraid to Disrupt its operations to consider doing something new. It is not focused on doing one thing, and doing it right. Instead open to bringing to market new technologies rapidly when they can Disrupt a market; and

Google uses extensive White Space to test new solutions and learn what is needed in the product, distribution, pricing and promotion. Google gives new teams the permission and resources to investigate how to succeed – rather than following a predetermined path toward an internally set goal (like GM did with its failed electric car project).

Nobody today wants to be like GM. Struggling to turn around after falling into bankruptcy. To be like Google you need to quit following old ideas about focusing on your core and entry barriers – instead develop scenarios about the future, study competitors for early market insights, Disrupt your practices so you can do new things and test lots of ideas in White Space to find out what the market really wants so you can continue growing.

"With Oracle, Sun avoids becoming another Yahoo," headlines Marketwatch.com today. As talks broke down because IBM was unwilling to up its price for Sun Microsystems, Oracle Systems swept in and made a counter-offer that looks sure to acquire the company. Unlike Yahoo – Sun will now disappear. The shareholders will get about 5% of the value Sun was worth a decade ago at its peak. That's a pretty serious value destruction, in any book. And if you don't think this is bad news for the employees and vendors just wait a year and see how many remain part of Oracle. A sale to IBM would have fared no better for investors, employees or vendors.

It was clear Sun wasn't able to survive several years ago. That's why I wrote about the company in my book Create Marketplace Disruption. Because the company was unwilling to allow any internal Disruptions to its Success Formula and any White Space to exist which might transform the company. In the fast paced world of information products, no company can survive if it isn't willing to build an organization that can identify market shifts and change with them.

I was at a Sun analyst conference in 1995 where Chairman McNealy told the analysts "have you seen the explosive growth over at Cisco System? I ask myself, how did we miss that?" And that's when it was clear Sun was in for big, big trouble. He was admitting then that Sun was so focused on its business, so focused on its core, that there was very little effort being expended on evaluating market shifts – which meant opportunities were being missed and Sun would be in big trouble when its "core" business slowed – as happens to all IT product companies. Sun had built its Success Formula selling hardware. Even though the real value Sun created shifted more and more to the software that drove its hardware, which became more and more generic (and less competitive) every year, Sun wouldn't change its strategy or tactics – which supported its identity as a hardware company – its Success Formula. Even though Sun became a leader in Unix operating systems, extensions for networking and accessing lots of data, as well as the creator and developer of Java for network applications because software was incompatible with the Success Formula, the company could not maintain independent software sales and the company failed.

Sort of like Xerox inventing the GUI (graphical user interface), mouse, local area network to connect a PC to a printer, and the laser printer but never capturing any of the PC, printer or desktop publishing market. Just because Xerox (and Sun) invented a lot of what became future growth markets did not insure success, because the slavish dedication to the old Success Formula (in Xerox's case big copiers) kept the company from moving forward with the marketplace.

Instead, Sun Microsystems kept trying to Defend & Extend its old, original Success Formula to theend. Even after several years struggling to sell hardware, Sun refused to change into the software company it needed to become. To unleash this value, Sun had to be acquired by another software company, Oracle, willing to let the hardware go and keep the software – according to the MercuryNews.com "With Oracle's acquisition of Sun, Larry Ellison's empire grows." Scott McNealy wouldn't Disrupt Sun and use White Space to change Sun, so its value deteriorated until it was a cheap buy for someone who could use the software pieces to greater value in another company.

Compare this with Steve Jobs. When Jobs left Apple in disrepute he founded NeXt to be another hardware company – something like a cross between Apple and Sun. But he found the Unix box business tough sledding. So he changed focus to a top application for high powered workstations – graphics – intending to compete with Silicon Graphics (SGI). But as he learned about the market, he realized he was better off developing application software, and he took over leadership of Pixar. He let NeXt die as he focused on high end graphics software at Pixar, only to learn that people weren't as interesed in buying his software as he thought they would be. So he transitioned Pixar into a movie production company making animated full-length features as well as commercials and short subjects. Mr. Jobs went through 3 Success Formulas getting the business right – using Disruptions and White Space to move from a box company to a software company to a movie studio (that also supplied software to box companies). By focusing on future scenarios, obsessing about competitors and Disrupting his approach he kept pushing into White Space. Instead of letting Lock-in keep him pushing a bad idea until it failed, he let White Space evolve the business into something of high value for the marketplace. As a result, Pixar is a viable competitor today – while SGI and Sun Microsystems have failed within a few months of each other.

It's incredibly easy to Defend & Extend your Success Formula, even after the business starts failing. It's easy to remain Locked-in to the original Success Formula and keep working harder and faster to make it a little better or cheaper. But when markets shift, you will fail if you don't realize that longevity requires you change the Success Formula. Where Unix boxes were once what the market wanted (in high volume), shifts in competitive hardware (PC) and software (Linux) products kept sucking the value out of that original Success Formula.

Sun needed to Disrupt its Lock-ins – attack them – in order to open White Space where it could build value for its software products. Where it could learn to sell them instead of force-bundling them with hardware, or giving them away (like Java.) And this is a lesson all companies need to take to heart. If Sun had made these moves it could have preserved much more of its value – even if acquired by someone else. Or it might have been able to survive as a different kind of company. Instead, Sun has failed costing its investors, employees and vendors billions.