by Adam Hartung | Jul 27, 2016 | Food and Drink, Growth Stall, In the Swamp, Leadership, Web/Tech

Growth Stalls are deadly for valuation, and both Mcdonald’s and Apple are in one.

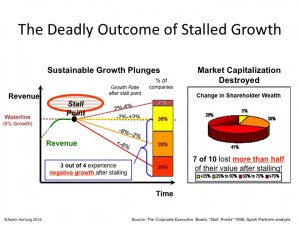

August, 2014 I wrote about McDonald’s Growth Stall. The company had 7 straight months of revenue declines, and leadership was predicting the trend would continue. Using data from several thousand companies across more than 3 decades, companies in a Growth Stall are unable to maintain a mere 2% growth rate 93% of the time. 55% fall into a consistent revenue decline of more than 2%. 20% drop into a negative 6%/year revenue slide. 69% of Growth Stalled companies will lose at least half their market capitalization in just a few years. 95% will lose more than 25% of their market value. So it is a long-term concern when any company hits a Growth Stall.

A new CEO was hired, and he implemented several changes. He implemented all-day breakfast, and multiple new promotions. He also closed 700 stores in 2015, and 500 in 2016. And he announced the company would move its headquarters from suburban Oakbrook to downtown Chicago, IL. While doing something, none of these actions addressed the fundamental problem of customers switching to competitive options that meet modern consumer food trends far better than McDonald’s.

A new CEO was hired, and he implemented several changes. He implemented all-day breakfast, and multiple new promotions. He also closed 700 stores in 2015, and 500 in 2016. And he announced the company would move its headquarters from suburban Oakbrook to downtown Chicago, IL. While doing something, none of these actions addressed the fundamental problem of customers switching to competitive options that meet modern consumer food trends far better than McDonald’s.

McDonald’s stock languished around $94/share from 8/2014 through 8/2015 – but then broke out to $112 in 2 months on investor hopes for a turnaround. At the time I warned investors not to follow the herd, because there was nothing to indicate that trends had changed – and McDonald’s still had not altered its business in any meaningful way to address the new market realities.

Yet, hopes remained high and the stock peaked at $130 in May, 2016. But since then, the lack of incremental revenue growth has become obvious again. Customers are switching from lunch food to breakfast food, and often switching to lower priced items – but these are almost wholly existing customers. Not new, incremental customers. Thus, the company trumpets small gains in revenue per store (recall, the number of stores were cut) but the growth is less than the predicted 2%. The only incremental growth is in China and Russia, 2 markets known for unpredictable leadership. The stock has now fallen back to $120.

Given that the realization is growing as to the McDonald’s inability to fundamentally change its business competitively, the prognosis is not good that a turnaround will really happen. Instead, the common pattern emerges of investors hoping that the Growth Stall was a “blip,” and will be easily reversed. They think the business is fundamentally sound, and a little management “tweaking” will fix everything. Small changes will lead to the classic hockey-stick forecast of higher future growth. So the stock pops up on short-term news, only to fall back when reality sets in that the long-term doesn’t look so good.

Unfortunately, Apple’s Q3 2016 results (reported yesterday) clearly show the company is now in its own Growth Stall. Revenues were down 11% vs. last year (YOY or year-over-year,) and EPS (earnings per share) were down 23% YOY. 2 consecutive quarters of either defines a Growth Stall, and Apple hit both. Further evidence of a Growth Stall exists in iPhone unit sales declining 15% YOY, iPad unit sales off 9% YOY, Mac unit sales down 11% YOY and “other products” revenue down 16% YOY.

This was not unanticipated. Apple started communicating growth concerns in January, causing its stock to tank. And in April, revealing Q2 results, the company not only verified its first down quarter, but predicted Q3 would be soft. From its peak in May, 2015 of $132 to its low in May, 2016 of $90, Apple’s valuation fell a whopping 32%! One could say it met the valuation prediction of a Growth Stall already – and incredibly quickly!

But now analysts are ready to say “the worst is behind it” for Apple investors. They are cheering results that beat expectations, even though they are clearly very poor compared to last year. Analysts are hoping that a new, lower baseline is being set for investors that only look backward 52 weeks, and the stock price will move up on additional company share repurchases, a successful iPhone 7 launch, higher sales in emerging countries like India, and more app revenue as the installed base grows – all leading to a higher P/E (price/earnings) multiple. The stock improved 7% on the latest news.

So far, Apple still has not addressed its big problem. What will be the next product or solution that will replace “core” iPhone and iPad revenues? Increasingly competitors are making smartphones far cheaper that are “good enough,” especially in markets like China. And iPhone/iPad product improvements are no longer as powerful as before, causing new product releases to be less exciting. And products like Apple Watch, Apple Pay, Apple TV and IBeacon are not “moving the needle” on revenues nearly enough. And while experienced companies like HBO, Netflix and Amazon grow their expanding content creation, Apple has said it is growing its original content offerings by buying the exclusive rights to “Carpool Karaoke“ – yet this is very small compared to the revenue growth needs created by slowing “core” products.

Like McDonald’s stock, Apple’s stock is likely to move upward short-term. Investor hopes are hard to kill. Long-term investors will hold their stock, waiting to see if something good emerges. Traders will buy, based upon beating analyst expectations or technical analysis of price movements. Or just belief that the P/E will expand closer to tech industry norms. But long-term, unless the fundamental need for new products that fulfill customer trends – as the iPad, iPhone and iPod did for mobile – it is unclear how Apple’s valuation grows.

by Adam Hartung | Jun 7, 2015 | Defend & Extend, In the Swamp, Innovation, Leadership, Transparency

Did you ever notice that Human Resource (HR) practices are designed to lock-in the past rather than grow? A quick tour of what HR does and you quickly see they like to lock-in processes and procedures, insuring consistency but offering no hope of doing something new. And when it comes to hiring, HR is all about finding people that are like existing employees – same school, same degrees, same industry, same background. And HR tries its very hardest to insure conformity amongst employees to historical standard – especially regarding culture.

Several years ago I was leading an innovation workshop for leaders in a company that made nail guns, screw guns, nails and screws. Once a market leader, sales were struggling and profits were nearly nonexistent due to the emergence of competitors from Asia. Some of their biggest distributors were threatening to drop this company’s line altogether unless there were more concessions – which would insure losses.

They liked to call themselves a “fastener company,” which has long been the trend with companies that like to make it sound as if they do more than they actually do.

I asked the simple question “where is the growth in fasteners?” The leaders jumped right in with sales numbers on all their major lines. They were sure that growth was in auto-loading screwguns, and they were hard at work extending this product line. To a person, these folks were sure they new where growth existed.

But I had prepared prior to the meeting. There actually was much higher growth in adhesives. Chemical attachment was more than twice the growth rate of anything in the old nail and screw business. Even loop-and-hook fasteners [popularly referred to by the tradename Velcro(c)] was seeing much greater growth than the old-line mechanical products.

They looked at me blank-faced. “What does that have to do with us?” the head of sales finally asked. The CEO and everyone else nodded in agreement.

I pointed out to them they said they were in the fastener business. Not the nail and screw business. The nail and screw business had become a bloody fight, and it was not going to get any better. Why not move into faster growing, less competitive products?

Competitors were making lots of battery powered and air powered tools beyond nail guns and screw guns, and their much deeper product lines gave them much higher favorability with retail merchandisers and professional tool distributors. Plus, competitor R&D into batteries was already showing they could produce more powerful and longer-lasting tools than my client. In a few major retailers competitors already had earned the position of “category leader” recommending the shelf space and layout for ALL competitors, giving them a distinct advantage.

This company had become myopic, and did not even realize it. The people were so much alike that they could finish each others sentences. They liked working together, and had built a tightly knit culture. The HR head was very proud of his ability to keep the company so harmonious.

Only, it was about to go bankrupt. Lacking diversity in background, they were unable to see beyond their locked-in business model. And there sure wasn’t anyone who would “rock the boat” by admitting competitors were outflanking them, or bringing up “wild ideas” for new markets or products.

According to the New York Times 80% of hiring is done based on “cultural fit.” Which means we hire people we want to hang out with. Which almost always means people that are a lot like ourselves. Regardless of what we really need in our company. Thus companies end up looking, thinking and acting very homogenously.

It is common amongst management authors and keynote speakers to talk about creating “high-performance teams.” The vaunted Jim Collins in “Good to Great” uses the metaphor of a company as a bus. Every company should have a “core” and every employee should be single-mindedly driving that “core.” He says that it is the role of good leaders to get everyone on the bus to “core.” Anyone who isn’t 100% aligned – well, throw them off the bus (literally, fire them.)

We see this phenomenon in nepotism. Where a founder, CEO or Chairperson who succeeds uses their leadership position to promote relatives into high positions.

Wal-Mart’s Board of Directors, for example, recently elected the former Chairman’s son-in-law to the position of Chairman. He appears accomplished, but today Wal-Mart’s problem is Amazon and other on-line retail. Wal-Mart desperately needs outside thinking so it can move beyond its traditional brick-and-mortar business model, not someone who’s indoctrinated in the past.

The Reputation Institute just completed its survey of the most reputable retailers in the USA. Top of the list was Amazon, for the third straight year. Wal-Mart wasn’t even in the top 10, despite being the largest U.S. retailer by a considerable margin. Wal-Mart needs someone at the top much more like Jeff Bezos than someone who comes from the family.

Despite what HR often says, it is incredibly important to have high levels of diversity. It’s the only way to avoid becoming myopic, and finding yourself with “best practices” that don’t matter as competitors overwhelm your market.

Despite what HR often says, it is incredibly important to have high levels of diversity. It’s the only way to avoid becoming myopic, and finding yourself with “best practices” that don’t matter as competitors overwhelm your market.

Ever wonder why so many CEOs turn to layoffs when competitors cause sales and/or profits to stall? They are trying to preserve the business model, and everyone reporting to them is doing the same thing. Instead of looking for creative ways to grow the business – often requiring a very different business model – everyone is stuck in roles, processes and culture tied to the old model. As everyone talks to each other there is no “outsider” able to point out obvious problems and the need for change.

In 2011, while he was still CEO, I wrote a column titled “Why Steve Jobs Couldn’t Find a Job Today.” The premise was pretty simple. Steve Jobs was not obsessed with “cultural fit,” nor was he a person who shied away from conflict. He obsessed about results. But no HR person would consider a young Steve Jobs as a manager in their company. He would be considered too much trouble.

Yet, Steve Jobs was able to take a nearly dead Macintosh company and turn it into a leader in mobile products. Clearly, a person very talented in market sensing and identifying new solutions that fit trends. And a person willing to move toward the trend, rather than obsess about defending and extending the past.

Does your organization’s HR insure you would seek out, recruit and hire Steve Jobs, or Jeff Bezos? Or are you looking for good “cultural fit” and someone who knows “how to operate within that role.” Do you look for those who spot and respond to trends, or those with a history related to how your industry or business has always operated? Do you seek people who ask uncomfortable questions, and propose uncomfortable solutions – or seek people who won’t make waves?

Does your organization’s HR insure you would seek out, recruit and hire Steve Jobs, or Jeff Bezos? Or are you looking for good “cultural fit” and someone who knows “how to operate within that role.” Do you look for those who spot and respond to trends, or those with a history related to how your industry or business has always operated? Do you seek people who ask uncomfortable questions, and propose uncomfortable solutions – or seek people who won’t make waves?

Too many organizations suffer failure simply because they lack diversity. They lack diversity in geographic sales, markets, products and services – and when competition shifts sales stall and they fall into a slow death spiral.

And this all starts with insufficient diversity amongst the people. Too much “cultural fit” and not enough focus on what’s really needed to keep the organization aligned with customers in a fast-changing world. If you don’t have the right people around you, in the discussion, then you’re highly unlikely to develop the right solution for any problem. In fact, you’re highly unlikely to even ask the right question.

by Adam Hartung | Nov 6, 2013 | Defend & Extend, Innovation, Leadership, Web/Tech

Can you believe it has been only 12 years since Apple introduced the iPod? Since then Apple’s value has risen from about $11 (January, 2001) to over $500 (today) – an astounding 45X increase.

With all that success it is easy to forget that it was not a “gimme” that the iPod would succeed. At that time Sony dominated the personal music world with its Walkman hardware products and massive distribution through consumer electronics chains such as Best Buy, and broad-line retailers like Wal-Mart. Additionally, Sony had its own CD label, from its acquisition of Columbia Records (renamed CBS Records,) producing music. Sony’s leadership looked impenetrable.

But, despite all the data pointing to Sony’s inevitable long-term domination, Apple launched the iPod. Derided as lacking CD quality, due to MP3’s compression algorithms, industry leaders felt that nobody wanted MP3 products. Sony said it tried MP3, but customers didn’t want it.

All the iPod had going for it was a trend. Millions of people had downloaded MP3 songs from Napster. Napster was illegal, and users knew it. Some heavy users were even prosecuted. But, worse, the site was riddled with viruses creating havoc with all users as they downloaded hundreds of millions of songs.

Eventually Napster was closed by the government for widespread copyright infreingement. Sony, et.al., felt the threat of low-priced MP3 music was gone, as people would keep buying $20 CDs. But Apple’s new iPod provided mobility in a way that was previously unattainable. Combined with legal downloads, including the emerging Apple Store, meant people could buy music at lower prices, buy only what they wanted and literally listen to it anywhere, remarkably conveniently.

The forecasted “numbers” did not predict Apple’s iPod success. If anything, good analysis led experts to expect the iPod to be a limited success, or possibly failure. (Interestingly, all predictions by experts such as IDC and Gartner for iPhone and iPad sales dramatically underestimated their success, as well – more later.) It was leadership at Apple (led by the returned Steve Jobs) that recognized the trend toward mobility was more important than historical sales analysis, and the new product would not only sell well but change the game on historical leaders.

Which takes us to the mistake Intel made by focusing on “the numbers” when given the opportunity to build chips for the iPhone. Intel was a very successful company, making key components for all Microsoft PCs (the famous WinTel [for Windows+Intel] platform) as well as the Macintosh. So when Apple asked Intel to make new processors for its mobile iPhone, Intel’s leaders looked at the history of what it cost to make chips, and the most likely future volumes. When told Apple’s price target, Intel’s leaders decided they would pass. “The numbers” said it didn’t make sense.

Uh oh. The cost and volume estimates were wrong. Intel made its assessments expecting PCs to remain strong indefinitely, and its costs and prices to remain consistent based on historical trends. Intel used hard, engineering and MBA-style analysis to build forecasts based on models of the past. Intel’s leaders did not anticipate that the new mobile trend, which had decimated Sony’s profits in music as the iPod took off, would have the same impact on future sales of new phones (and eventually tablets) running very thin apps.

Harvard innovation guru Clayton Christensen tells audiences that we have complete knowledge about the past. And absolutely no knowledge about the future. Those who love numbers and analysis can wallow in reams and reams of historical information. Today we love the “Big Data” movement which uses the world’s most powerful computers to rip through unbelievable quantities of historical data to look for links in an effort to more accurately predict the future. We take comfort in thinking the future will look like the past, and if we just study the past hard enough we can have a very predictible future.

But that isn’t the way the business world works. Business markets are incredibly dynamic, subject to multiple variables all changing simultaneously. Chaos Theory lecturers love telling us how a butterfly flapping its wings in China can cause severe thunderstorms in America’s midwest. In business, small trends can suddenly blossom, becoming major trends; trends which are easily missed, or overlooked, possibly as “rounding errors” by planners fixated on past markets and historical trends.

Markets shift – and do so much, much faster than we anticipate. Old winners can drop remarkably fast, while new competitors that adopt the trends become “game changers” that capture the market growth.

In 2000 Apple was the “Mac” company. Pretty much a one-product company in a niche market. And Apple could easily have kept trying to defend & extend that niche, with ever more problems as Wintel products improved.

But by understanding the emerging mobility trend leadership changed Apple’s investment portfolio to capture the new trend. First was the iPod, a product wholly outside the “core strengths” of Apple and requiring new engineering, new distribution and new branding. And a product few people wanted, and industry leaders rejected.

Then Apple’s leaders showed this talent again, by launching the iPhone in a market where it had no history, and was dominated by Motorola and RIMM/BlackBerry. Where, again, analysts and industry leaders felt the product was unlikely to succeed because it lacked a keyboard interface, was priced too high and had no “enterprise” resources. The incumbents focused on their past success to predict the future, rather than understanding trends and how they can change a market.

Too bad for Intel. And Blackberry, which this week failed in its effort to sell itself, and once again changed CEOs as the stock hit new lows.

Then Apple did it again. Years after Microsoft attempted to launch a tablet, and gave up, Apple built on the mobility trend to launch the iPad. Analysts again said the product would have limited acceptance. Looking at history, market leaders claimed the iPad was a product lacking usability due to insufficient office productivity software and enterprise integration. The numbers just did not support the notion of investing in a tablet.

Anyone can analyze numbers. And today, we have more numbers than ever. But, numbers analysis without insight can be devastating. Understanding the past, in grave detail, and with insight as to what used to work, can lead to incredibly bad decisions. Because what really matters is vision. Vision to understand how trends – even small trends – can make an enormous difference leading to major market shifts — often before there is much, if any, data.

by Adam Hartung | Aug 18, 2011 | Current Affairs, Defend & Extend, In the Swamp, Innovation, Leadership, Lifecycle, Web/Tech

The business world was surprised this week when Google announced it was acquiring Motorola Mobility for $12.5B – a 63% premium to its trading price (Crain’s Chicago Business). Surprised for 3 reasons:

- because few software companies move into hardware

- effectively Google will now compete with its customers like Samsung and HTC that offer Android-based phones and tablets, and

- because Motorola Mobility had pretty much been written off as a viable long-term competitor in the mobile marketplace. With less than 9% share, Motorola is the last place finisher – behind even crashing RIM.

Truth is, Google had a hard choice. Android doesn’t make much money. Android was launched, and priced for free, as a way for Google to try holding onto search revenues as people migrated from PCs to cloud devices. Android was envisioned as a way to defend the search business, rather than as a profitable growth opportunity. Unfortunately, Google didn’t really think through the ramifications of the product, or its business model, before taking it to market. Sort of like Sun Microsystems giving away Java as a way to defend its Unix server business. Oops.

In early August, Google was slammed when the German courts held that the Samsung Galaxy Tab 10.1 could not be sold – putting a stop to all sales in Europe (Phandroid.com “Samsung Galaxy Tab 10.1 Sales Now Blocked in Europe Thanks to Apple.”) Clearly, Android’s future in Europe was now in serious jeapardy – and the same could be true in the USA.

This wasn’t really a surprise. The legal battles had been on for some time, and Tab had already been blocked in Australia. Apple has a well established patent thicket, and after losing its initial Macintosh Graphical User Interface lead to Windows 25 years ago Apple plans on better defending its busiensses these days. It was also well known that Microsoft was on the prowl to buy a set of patents, or licenses, to protect its new Windows Phone O/S planned for launch soon.

Google had to either acquire some patents, or licenses, or serously consider dropping Android (as it did Wave, Google PowerMeter and a number of other products.) It was clear Google had severe intellectual property problems, and would incur big legal expenses trying to keep Android in the market. And it still might well fail if it did not come up with a patent portfolio – and before Microsoft!

So, Google leadership clearly decided “in for penny, in for a pound” and bought Motorola. The acquisition now gives Google some 16-17,000 patents. With that kind of I.P. war chest, it is able to defend Android in the internicine wars of intellectual property courts – where license trading dominates resolutions between behemoth competitors.

Only, what is Google going to do with Motorola (and Android) now? This acquisition doesn’t really fix the business model problem. Android still isn’t making any money for Google. And Motorola’s flat Android product sales don’t make any money either.

Source: Business Insider.com

In fact, the Android manufacturers as a group don’t make much money – especially compared to industry leader Apple:

Source: Business Insider.com

There was a lot of speculation that Google would sell the manufacturing business and keep the patents. Only – who would want it? Nobody needs to buy the industry laggard. Regardless of what the McKinsey-styled strategists might like to offer as options, Google really has no choice but to try running Motorola, and figuring out how to make both Android and Motorola profitable.

And that’s where the big problem happens for Google. Already locked into battles to maintain search revenue against Bing and others, Google recently launched Google+ in an all-out war to take on the market-leading Facebook. In cloud computing it has to support Chrome, where it is up against Microsoft, and again Apple. Oh my, but Google is now in some enormously large competitive situations, on multiple fronts, against very well-heeled competitors.

As mentioned before, what will Samsung and HTC do now that Google is making its own phones? Will this push them toward Microsoft’s Windows offering? That would dampen enthusiasm for Android, while breathing life into a currently non-competitor in Microsoft. Late to the game, Microsoft has ample resources to pour into the market, making competition very, very expensive for Google. It shows all the signs of two gladiators willing to fight to the loss-amassing death.

And Google will be going into this battle with less-than-stellar resources. Motorola is the market also ran. Its products are not as good as competitors, and its years of turmoil – and near failure – leading to the split-up of Motorola has left its talent ranks decimated – even though it still has 19,000 employees Google must figure out how to manage (“Motorola Bought a Dysfunctional Company and the Worst Android Handset Maker, says Insider“).

Acquisitions that “work” are ones where the acquirer buys a leader (technology, products, market) usually in a high growth area – then gives that acquisition the permission and resources to keep adapting and growing – what I call White Space. That’s what went right in Google’s acquisitions of YouTube and DoubleClick, for example. With Motorola, the business is so bad that simply giving it permssion and resources will lead to greater losses. It’s hard to disaagree with 24/7 Wall Street.com when divulging “S&P Gives Big Downgrade on Google-Moto Deal.”

Some would like to think of Google as creating some transformative future for mobility and copmuting. Sort of like Apple.

Yea, right.

Google is now stuck defending & extending its old businesses – search, Chrome O/S for laptops, Google+ for mail and social media, and Android for mobility products. And, as is true with all D&E management, its costs are escalating dramatically. In every market except search Google has entered into gladiator battles late against very well resourced competitors with products that are, at best, very similar – lacking game-changing characteristics. Despite Mr. Page’s potentially grand vision, he has mis-positioned Google in almost all markets, taken on market-leading and well funded competition, and set Google up for a diasaster as it burns through resources flailing in efforts to find success.

If you weren’t convinced of selling Google before, strongly consider it now. The upcoming battles will be very, very expensive. This acquisition is just so much chum in the water – confusing but not beneficial.

And if you still don’t own Apple – why not? Nothing in this move threatens the technology, product and market leader which continues bringing game-changers to market every few months.

by Adam Hartung | Jul 20, 2011 | Current Affairs, In the Rapids, In the Whirlpool, Leadership, Web/Tech

“Buy Low, Sell High” was an industrial era investor expression. Before we shifted into an information economy, investors were admonished to invest along with economic cycles, buying during recessions, selling during booms.

In today’s information economy it’s not nearly so simple. While growth occurs, companies falter and disappear (Sun Microsystems and Silicon Graphics, for example.) Meanwhile, during bad economic periods there are flourishing growth companies.

Company performance today has much more to do with whether the company’s products and services are aligned with trends, and market shifts created by trends, than the overall economy. When revenues first show signs fo faltering, often the company fails completely, unable to react to market shifts. Competitors quickly steal customers, revenue and precious cash flow. Investors frequently have little warning, or time, before company value slides into the oblivion, leaving them with negative returns.

So now it’s more important to look at trends in where product and service markets are headed than overall economic conditions. The economy won’t save a company that’s against the trend – or hurt a company that’s delivering the market trend.

Yahoo caught the early trend toward internet usage. In the early years people didn’t quite know what to do on the internet, so content providers, aggregators, and ability to search were valuable. People like Yahoo because it gave them what they wanted, and the company flourished as it became the home page for over 80% of internet users. Advertisers loved the user base, so they bought ads.

Then the market shifted. Users gained more experience, and didn’t need the aggregation function Yahoo provided. Increasingly they wanted to find answers themselves, making the quality of search more important than content. A white page with a simple box (Google) that did great searching across the entire web overtook Yahoo’s content. And, as time progressed people started using the internet as a primary location for socially connecting with friends and colleagues, making the content aggregation even less valuable. Time spent on Yahoo as a percent of time on-line began dropping:

Source: Business Insider

But although this trend began in 2009, and was clear in 2010, Yahoo’s CEO kept pushing the same business model. She missed the trend.

The market kept right on shifting, and by 2011, Yahoo is in a very bad competitive position:

Source: Business Insider

So, nobody should be surprised that revenue would fall – correct? It’s not that the folks at Yahoo are wasteful, or not working hard. They simply are becoming out of step with the market trend. The result one would expect is worsening results in the old, “core” business – and that’s exactly what is happening:

Source: Business Insider

Meanwhile, where the eyeballs go is where the display ad revenues go as well. And with the trends, that means we would expect display ad revenu growth to move away from Yahoo – as it has done:

Source: Business Insider

So yesterday when Yahoo announced sales and earnings, it was a disappointment. What increase Yahoo had in fast growing display ads (5%) was insufficient to cover the decline in search ads (down 15%). Clearly, Yahoo missed the market shift. But, the CEO did not admit that the business model was ineffective (as results indicate.) Rather, she said the company needed more salespeople!

This proclivity to look inward, as if working harder, faster and better would “fix” Yahoo, defies the reality that the company is no longer competitive given where the market is headed. Ms. Bartz can’t succeed by trying to defend and extend the traditional Yahoo business model. Yahoo doesn’t need more salespeople, it needs an entirely different business!

Source: Business Insider

Alternatively, Apple exemplifies the other side of this coin. I have been an unabashed bull on Apple for months. Why? Because it does create solutions tightly linked to market trends. People, as consumers or in business, demand more mobility. And Apple’s products deliver that mobility more seamlessly and effectively than any other solution provider.

Apple could well have kept itself focused on Mac sales. Had it done so, it would likely be out of business today. Instead, Apple focused the bulk of its development on delivering products that fulfilled trends. The result has been expansion into new markets, which have delivered massive revenue gains.

Source: Business Insider

Last quarter Apple sold more iPhones and even more iPad tablets (9.25million units, $6.1B) than it sold Macs (~4 million units, $5.1B.) The old business has been replaced (cannibalized) by new, growing businesses that support the market trend. iPads are now 11% of the PC business overall, and growing fast as they obsolete PCs. Combined, iPads and Macs sold 13.25 million “computing devices” which would make it second in the world, behind only HP (15.3million PCs.) Bigger than Dell, for example, that has stuck to its “core” PC business.

Because Apple is all about delivering on trends, there’s really no reason to think revenues, and profits, won’t continue growing. The shift to mobility has just taken hold, and there are legions of people still without an apps-powerful smartphone (lots of Blackberry customers out there to shift.) The shift to tablets has just started. As these trends continue, Apple is continuing to develop new solutions that keep it ahead of competitors.

Where Yahoo’s CEO wants to add more salespeople, in hopes she can push outdated products, Mr. Jobs said in the earnings call yesterday “Right now we’re very focused and excited about bringing iOS5 and iCloud to our users this fall.” Yahoo is trying to do more of what it always did, as the market moves away. While Apple keeps its collective management eyes on the future – and where the market is headed – to constantly bring new solutions that deliver on the trends.

Sell Yahoo, if you haven’t already. And buy Apple. It’s all about investing with the trends.

Note: update on “Is Cisco a Value Stock? Skip It.” In the month since publishing that blog (6/23/11) Cisco has demonstrated that it is running headlong from the rapids of growth into the swamp of stagnation. Not only has it been killing off new products, but as it announced weak results the CEO has taken to a massive cutback. 11,500 employees are being laid off, or sent off to work for other companies as facilities are being sold to a Chinese company.

Worse, the CEO is now stooping to financial machinations in order to make the future look better. According to HuffingtonPost.com Cisco is taking a massive $1.3B charge. This allows Cisco to write off various costs that are old, current and even future to the current P&L. This will inflate future earnings, regardless of actual performance, while deflating current results. The net impact is P&L manipulation designed to make the company – quarter over quarter or year over year – look better than it is actually performing. Transparency is being intentionally muddled, to hide the company’s inability to provide solutions delivering on market trends.

Cisco shows all the signs of a company in a growth stall. Unable to shift with market trends, it is now shedding products, employees and assets in an effort to pad the P&L. It is “reorganizing” the company, rather than linking to market needs. Remember that fewer than 7% of companies that slip into a growth stall ever successfully maintain an ongoing 2% growth rate. Because they are focused on internal issues, and financial management – rather being clearly focused market trends.

Don’t just skip buying Cisco – if you are a shareholder, SELL!

And buy Apple.