by Adam Hartung | Jan 30, 2016 | Current Affairs, In the Rapids, Leadership, Web/Tech

Apple announced earnings for the 4th quarter this week, and the company was creamed. Almost universally industry analysts and stock analysts had nothing good to say about the company’s reports, and forecast. The stock ended the week down about 5%, and down a whopping 27.8% from its 52 week high.

Wow, how could the world’s #1 mobile device company be so hammered? After all, sales and earnings were both up – again! Apple’s brand is still one of the top worldwide brands, and Apple stores are full of customers. It’s PC sales are doing better than the overall market, as are its tablet sales. And it is the big leader in wearable devices with Apple Watch.

Yet, let’s compare the stock price to earnings (P/E) multiple of some well known companies (according to CNN Money 1/29/16 end of day):

- Apple – 10.3

- Used car dealer AutoNation – 10.7

- Food company Archer Daniel Midland (ADM) – 12.2

- Industrial equipment maker Caterpillar Tractor – 12.9

- Farm equipment maker John Deere – 13.3

- Defense equipment maker General Dynamics – 15.1

- Utility American Electric Power – 16.9

- Industrial product company Illinois Tool Works (ITW) – 17.7

- Industrial product company 3M – 19.5

What’s wrong with this picture? It all goes to future expectations. Investors watched Apple’s meteoric rise, and many wonder if it will have a similar, meteoric fall. Remember the rise and fall of Digital Equipment? Wang? Sun Microsystems? Palm? Blackberry (Research in Motion)? Investors don’t like companies where they fear growth has stalled.

And Apple’s presentation created growth stall fears. While iPhone sales are enormous (75million units/quarter,) there was little percentage growth in Q4. And CEO Tim Cook actually predicted a sales decline next quarter! iPod sales took off like a rocket years ago, but they have now declined for 6 straight quarters and there was no prediction of a return to higher sales volumes. And as for future products, the company seems only capable of talking about Apple Watch, and so far few people have seen any reason to buy one. Amidst this gloom, Apple presented an unclear story about a future based on services – a market that is at the very least vague, where Apple has no market presence, little experience and no brand position. And wasn’t that IBM’s story some 2.5 decades ago?

In other words, Apple fed investor’s worst fears. That growth had stopped. And usually, like in the examples above, when growth stops – especially in tech companies – it presages a dramatic reversal in sales and profits. Sales have been known to fall far, far faster than management predicts. Although Apple has not yet entered a Growth Stall (which is 2 consecutive quarters of declining sales and/or profits, or 2 consecutive quarters than the previous year’s sales or profits) investors are now worried that one is just around the corner.

Contrast this with Facebook. P/E – 113.3. Facebook said ad revenues rose 57%, and net income was up 2.2x the previous year’s quarter. But what was really important was Facebook’s story about its future:

- Facebook is now a “must buy” for advertisers

- Mobile is the #1 ad trend, and 80% of revenues are from mobile

- Revenue/user is up 33%, and growing

- There are multiple unmonetized new markets that Facebook is just developing – Instagram, WhatsApp, FB Messenger and Oculus

In other words, the past was great – but the future will be even better. The short-term result? FB stock rose 7.4% for the week, and intraday hit a new 52 week high. Facebook might have seemed like a fad 3 years ago, especially to older folks. But now the company’s story is all about market trends, and how Facebook is offering products on those trends that will drive future revenue and profit growth.

Amazon may be an even better example of smart communications. As everyone knows, Amazon makes no profit. So it sells for an astonishing P/E of 846.9. Amazon sales increased 22% in Q4, and Amazon continued gaining share of the fast growing, #1 trend in retail — ecommerce. While WalMart and Macy’s are closing stores, Amazon is expanding and even creating its own logistics system.

Profits were up, but only 2/3 of expectations – ouch! Anticipating higher sales and earnings announcements the stock had run up $40/share. But the earnings miss took all that away and more as the stock crashed about $70/share! A wild 12.5% peak-to-trough swing was capped at end of week down a mere 2.5%.

But, Amazon did a great job, once again, of selling its future. In addition to the good news on retail sales, there was ongoing spectacular growth in cloud services – meaning Amazon Web Services (AWS.) JPMorganChase, Wells Fargo, Raymond James and Benchmark all raised their future price forecasts after the announcement, based on future performance expectations. Even analysts who cut their price targets still kept price targets higher than where Amazon actually ended the week. And almost all analysts expect Amazon one year from now to be worth more than its historical 52 week high, which is 19% higher than current pricing.

So, despite bad earnings news, Amazon continued to sell its growth story. Growth can heal all wounds, if investors continue to believe. We’ll see how it plays out, but for now things appear at least stable.

Steve Jobs was, by most accounts, an excellent showman. But what he did particularly well was tell a great growth story. No matter Apple’s past results, or concerns about the company, when Steve Jobs took the stage his team had crafted a story about Apple’s future growth. It wasn’t about cash flow, cash in the bank, assets in place, market share or historical success – boring, boring. There was an Apple growth story. There was always a reason for investor’s to believe that competitors will falter, markets will turn to Apple, and growth will increase!

Should investors think Apple is without future growth? Unfortunately, the communications team at Apple last week let investors think so. It is impossible to believe this is true, but the communicators this week simply blew it. Because what they said led to nothing but headlines questioning the company’s future.

What should Apple have said?

- Give investors a great news story about wearables. Show applications in health care, retail, etc. that really makes investors think all those people with a Timex or Rolex will wear an AppleWatch in the future. Apple sold investors the future of iPhone apps long before most of people used anything other than maps and weather – and the story led investors to believe if people didn’t have an iPhone they would miss out on something important, so they were bound to go buy one. Where’s that story when it comes to wearables?

- ApplePay is going to change the world. While ApplePay is #1, investors are wondering if mobile payments is ever going to be big. What will make it big, when, and what is Apple doing to make this a multi-billion dollar business? ApplePay launched to a lot of hype, but very little has been said since. Is this going to be the Apple version of Microsoft’s Zune? Make investors believers in ApplePay. Convince them this is worth a lot of future value.

- iBeacons are one of the most important technology products in retail and inventory control. iBeacons were launched as a great tool for local businesses, but since then Apple has said almost nothing. B2B may not be as sexy as consumer markets, but Microsoft made investors believers in the value of enterprise products. Demonstrate that Apple’s technology is the best, and give investors some stories about how companies are winning. Most investors have forgotten about beacons and thus they no longer plan for substantial revenues.

- Apple has the #1 mobile developer community, and the best products are yet to come – so sales are far from stalling. Honestly, the developer war is critical. The platform with the most developers wins the most customers. Microsoft taught investors that. But Apple never talks about its developer community. IBM has made a huge commitment to develop iOS enterprise apps that should drive substantial future sales, but Apple isn’t exciting investors about that opportunity. Tell investors more stories about how Apple is king of the developer world, and will remain in the top spot – better than Android or anyone – for years. Tell investors this will turn users toward tablets from PCs faster, and iPod sales will start growing again as smartphone and wearable sales join suit.

- Apple will win big revenues in auto markets. There was lots of rumors about hiring people to design a car, and now firing the lead guy. What is going on? Google has been pretty clear about its plans, but Apple offers investors no encouragement to think the company will succeed at even winning the war to be in other manufacturer’s cars, much less build its own. Given that the story sounds limited for Apple’s “core” products, investors need some stories about Apple’s own “moonshot” projects.

- Apple is not a 1-pony, iPhone story. Make investors believe it.

Tim Cook and the rest of Apple leadership are obviously competent. But when it comes to storytelling, this week their messaging looked like it was created as a high school communications project. Growth is what matters, and Apple completely missed the target. And investors are moving on to better stories – fast.

by Adam Hartung | May 30, 2014 | Current Affairs, In the Swamp, In the Whirlpool, Leadership, Sports, Web/Tech

Anyone who reads my column knows I’ve been no fan of Steve Ballmer as CEO of Microsoft. On multiple occasions I chastised him for bad decisions around investing corporate funds in products that are unlikely to succeed. I even called him the worst CEO in America. The Washington Post even had difficulty finding reputable folks to disagree with my argument.

Unfortunately, Microsoft suffered under Mr. Ballmer. And Windows 8, as well as the Surface tablet, have come nowhere close to what was expected for their sales – and their ability to keep Microsoft relevant in a fast changing personal technology marketplace. In almost all regards, Mr. Ballmer was simply a terrible leader, largely because he had no understanding of business/product lifecycles.

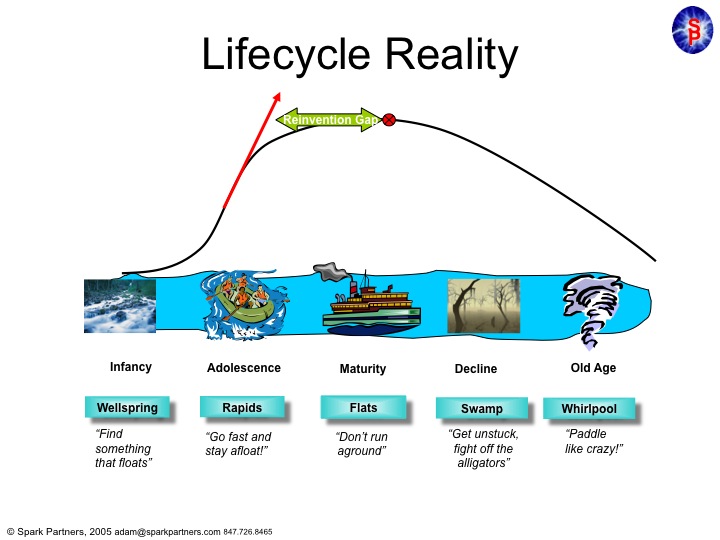

Microsoft was founded by Bill Gates, who did a remarkable job of taking a start-up company from the Wellspring of an idea into one of the fastest growing adolescents of any American company.

Microsoft was founded by Bill Gates, who did a remarkable job of taking a start-up company from the Wellspring of an idea into one of the fastest growing adolescents of any American company.

Under Mr. Gates leadership Microsoft single-handedly overtook the original PC innovator – Apple – and left it a niche company on the edge of bankruptcy in little over a decade.

Mr. Gates kept Microsoft’s growth constantly in the double digits by not only making superior operating system software, but by pushing the company into application software which dominated the desktop (MS Office.) And when the internet came along he had the vision to be out front with Internet Explorer which crushed early innovator, and market maker, Netscape.

But then Mr. Gates turned the company over to Mr. Ballmer. And Mr. Ballmer was a leader lacking vision, or innovation. Instead of pushing Microsoft into new markets, as had Mr. Gates, he allowed the company to fixate on constant upgrades to the products which made it dominant – Windows and Office. Instead of keeping Microsoft in the Rapids of growth, he offered up a leadership designed to simply keep the company from going backward. He felt that Microsoft was a company that was “mature” and thus in need of ongoing enhancement, but not much in the way of real innovation. He trusted the market to keep growing, indefinitely, if he merely kept improving the products handed him.

As a result Microsoft stagnated. A “Reinvention Gap” developed as Vista, Windows 7, then Windows 8 and one after another Office updates did nothing to develop new customers, or new markets. Microsoft was resting on its old laurels – monopolistic control over desktop/laptop markets – without doing anything to create new markets which would keep it on the old growth trajectory of the Gates era.

Things didn’t look too bad for several years because people kept buying traditional PCs. And Ballmer famously laughed at products like Linux or Unix – and then later at entertainment devices, smart phones and tablets – as Microsoft launched, but then abandoned products like Zune, Windows CE phones and its own tablet. Ballmer kept thinking that all the market wanted was a faster, cheaper PC. Not anything really new.

And he was dead wrong. The Reinvention Gap emerged to the public when Apple came along with the iPod, iTunes, iPhone and iPad. These changed the game on Microsoft, and no longer was it good enough to simply have a better edition of an outdated technology. As PC sales began declining it was clear that Ballmer’s leadership had left the company in the Swamp, fighting off alligators and swatting at mosquitos with no strategy for how it would regain relevance against all these new competitors.

So the Board pushed him out, and demoted Gates off the Chairman’s throne. A big move, but likely too late. Fewer than 7% of companies that wander into the Swamp avoid the Whirlpool of demise. Think Univac, Wang, Lanier, DEC, Cray, Sun Microsystems (or Circuit City, Montgomery Wards, Sears.) The new CEO, Satya Nadella, has a much, much more difficult job than almost anyone thinks. Changing the trajectory of Microsoft now, after more than a decade creating the Reinvention Gap, is a task rarely accomplished. So rare we make heros of leaders who do it (Steve Jobs, Lou Gerstner, Lee Iacocca.)

So what will happen at the Clippers?

Critically, owning an NBA team is nothing like competing in the real business world. It is a closed marketplace. New competitors are not allowed, unless the current owners decide to bring in a new team. Your revenues are not just dependent upon you, but are even shared amongst the other teams. In fact your revenues aren’t even that closely tied to winning and losing. Season tickets are bought in advance, and with so many games away from home a team can do quite poorly and still generate revenue – and profit – for the owner. And this season the Indiana Pacers demonstrated that even while losing, fans will come to games. And the Philadelphia 76ers drew crowds to see if they would set a new record for the most consecutive games lost.

In America the major sports only modestly overlap, so you have a clear season to appeal to fans. And even if you don’t make it into the playoffs, you still share in the profits from games played by other teams. As a business, a team doesn’t need to win a championship to generate revenue – or make a profit. In fact, the opposite can be true as Wayne Huizenga learned owning the Championship winning Florida Marlins baseball team. He payed so much for the top players that he lost money, and ended up busting up the team and selling the franchise!

In short, owning a sports franchise doesn’t require the owner to understand lifecycles. You don’t have to understand much about business, or about business competition. You are protected from competitors, and as one of a select few in the club everyone actually works together – in a wholly uncompetitive way – to insure that everyone makes as much money as possible. You don’t even have to know anything about managing people, because you hire coaches to deal with players, and PR folks to deal with fans and media. And as said before whether or not you win games really doesn’t have much to do with how much money you make.

Most sports franchise owners are known more for their idiosyncrasies than their business acumen. They can be loud and obnoxious all they want (with very few limits.) And now that Mr. Ballmer has no investors to deal with – or for that matter vendors or cooperative parties in a complex ecosystem like personal technology – he doesn’t have to fret about understanding where markets are headed or how to compete in the future.

When it comes to acting like a person who knows little about business, but has a huge ego, fiery temper and loves to be obnoxious there is no better job than being a sports franchise owner. Mr. Ballmer should fit right in.

by Adam Hartung | Jun 28, 2013 | Current Affairs, Defend & Extend, In the Rapids, In the Whirlpool, Innovation, Leadership, Web/Tech

The last 12 months Tesla Motors stock has been on a tear. From $25 it has more than quadrupled to over $100. And most analysts still recommend owning the stock, even though the company has never made a net profit.

There is no doubt that each of the major car companies has more money, engineers, other resources and industry experience than Tesla. Yet, Tesla has been able to capture the attention of more buyers. Through May of 2013 the Tesla Model S has outsold every other electric car – even though at $70,000 it is over twice the price of competitors!

During the Bush administration the Department of Energy awarded loans via the Advanced Technology Vehicle Manufacturing Program to Ford ($5.9B), Nissan ($1.4B), Fiskar ($529M) and Tesla ($465M.) And even though the most recent Republican Presidential candidate, Mitt Romney, called Tesla a "loser," it is the only auto company to have repaid its loan. And did so some 9 years early! Even paying a $26M early payment penalty!

How could a start-up company do so well competing against companies with much greater resources?

Firstly, never underestimate the ability of a large, entrenched competitor to ignore a profitable new opportunity. Especially when that opportunity is outside its "core."

A year ago when auto companies were giving huge discounts to sell cars in a weak market I pointed out that Tesla had a significant backlog and was changing the industry. Long-time, outspoken industry executive Bob Lutz – who personally shepharded the Chevy Volt electric into the market – was so incensed that he wrote his own blog saying that it was nonsense to consider Tesla an industry changer. He predicted Tesla would make little difference, and eventually fail.

For the big car companies electric cars, at 32,700 units January thru May, represent less than 2% of the market. To them these cars are simply not seen as important. So what if the Tesla Model S (8.8k units) outsold the Nissan Leaf (7.6k units) and Chevy Volt (7.1k units)? These bigger companies are focusing on their core petroleum powered car business. Electric cars are an unimportant "niche" that doesn't even make any money for the leading company with cars that are very expensive!

This is the kind of thinking that drove Kodak. Early digital cameras had lots of limitations. They were expensive. They didn't have the resolution of film. Very few people wanted them. And the early manufacturers didn't make any money. For Kodak it was obvious that the company needed to remain focused on its core film and camera business, as digital cameras just weren't important.

Of course we know how that story ended. With Kodak filing bankruptcy in 2012. Because what initially looked like a limited market, with problematic products, eventually shifted. The products became better, and other technologies came along making digital cameras a better fit for user needs.

Tesla, smartly, has not tried to make a gasoline car into an electric car – like, say, the Ford Focus Electric. Instead Tesla set out to make the best car possible. And the company used electricity as the power source. By starting early, and putting its resources into the best possible solution, in 2013 Consumer Reports gave the Model S 99 out of 100 points. That made it not just the highest rated electric car, but the highest rated car EVER REVIEWED!

As the big car companies point out limits to electric vehicles, Tesla keeps making them better and addresses market limitations. Worries about how far an owner can drive on a charge creates "range anxiety." To cope with this Tesla not only works on battery technology, but has launched a program to build charging stations across the USA and Canada. Initially focused on the Los-Angeles to San Franciso and Boston to Washington corridors, Tesla is opening supercharger stations so owners are never less than 200 miles from a 30 minute fast charge. And for those who can't wait Tesla is creating a 90 second battery swap program to put drivers back on the road quickly.

This is how the classic "Innovator's Dilemma" develops. The existing competitors focus on their core business, even though big sales produce ever declining profits. An upstart takes on a small segment, which the big companies don't care about. The big companies say the upstart products are pretty much irrelevant, and the sales are immaterial. The big companies choose to keep focusing on defending and extending their "core" even as competition drives down results and customer satisfaction wanes.

Meanwhile, the upstart keeps plugging away at solving problems. Each month, quarter and year the new entrant learns how to make its products better. It learns from the initial customers – who were easy for big companies to deride as oddballs – and identifies early limits to market growth. It then invests in product improvements, and market enhancements, which enlarge the market.

Eventually these improvements lead to a market shift. Customers move from one solution to the other. Not gradually, but instead quite quickly. In what's called a "punctuated equilibrium" demand for one solution tapers off quickly, killing many competitors, while the new market suppliers flourish. The "old guard" companies are simply too late, lack product knowledge and market savvy, and cannot catch up.

- The integrated steel companies were killed by upstart mini-mill manufacturers like Nucor Steel.

- Healthier snacks and baked goods killed the market for Hostess Twinkies and Wonder Bread.

- Minolta and Canon digital cameras destroyed sales of Kodak film – even though Kodak created the technology and licensed it to them.

- Cell phones are destroying demand for land line phones.

- Digital movie downloads from Netflix killed the DVD business and Blockbuster Video.

- CraigsList plus Google stole the ad revenue from newspapers and magazines.

- Amazon killed bookstore profits, and Borders, and now has its sites set on WalMart.

- IBM mainframes and DEC mini-computers were made obsolete by PCs from companies like Dell.

- And now Android and iOS mobile devices are killing the market for PCs.

There is no doubt that GM, Ford, Nissan, et. al., with their vast resources and well educated leadership, could do what Tesla is doing. Probably better. All they need is to set up white space companies (like GM did once with Saturn to compete with small Japanese cars) that have resources and free reign to be disruptive and aggressively grow the emerging new marketplace. But they won't, because they are busy focusing on their core business, trying to defend & extend it as long as possible. Even though returns are highly problematic.

Tesla is a very, very good car. That's why it has a long backlog. And it is innovating the market for charging stations. Tesla leadership, with Elon Musk thought to be the next Steve Jobs by some, is demonstrating it can listen to customers and create solutions that meet their needs, wants and wishes. By focusing on developing the new marketplace Tesla has taken the lead in the new marketplace. And smart investors can see that long-term the odds are better to buy into the lead horse before the market shifts, rather than ride the old horse until it drops.

by Adam Hartung | May 25, 2012 | Defend & Extend, In the Whirlpool, Leadership, Web/Tech

Things are bad at HP these days. CEO and Board changes have confused the management team and investors alike. Despite a heritage based on innovation, the company is now mired in low-growth PC markets with little differentiation. Investors have dumped the stock, dropping company value some 60% over two years, from $52/share to $22 – a loss of about $60billion.

Reacting to the lousy revenue growth prospects as customers shift from PCs to tablets and smartphones, CEO Meg Whitman announced plans to eliminate 27,000 jobs; about 8% of the workforce. This is supposedly the first step in a turnaround of the company that has flailed ever since buying Compaq and changing the company course into head-to-head PC competition a decade ago. But, will it work?

Not a chance.

Fixing HP requires understanding what went wrong at HP. Simply, Carly Fiorina took a company long on innovation and new product development and turned it into the most industrial-era sort of company. Rather than having HP pursue new technologies and products in the development of new markets, like the company had done since its founding creating the market for electronic testing equipment, she plunged HP into a generic manufacturing war.

Pursuing the PC business Ms. Fiorina gave up R&D in favor of adopting the R&D of Microsoft, Intel and others while spending management resources, and money, on cost management. PCs offered no differentiation, and HP was plunged into a gladiator war with Dell, Lenovo and others to make ever cheaper, undifferentiated machines. The strategy was entirely based upon obtaining volume to make money, at a time when anyone could buy manufacturing scale with a phone call to a plethora of Asian suppliers.

Quickly the Board realized this was a cutthroat business primarily requiring supply chain skills, so they dumped Ms. Fiorina in favor of Mr. Hurd. He was relentless in his ability to apply industrial-era tactics at HP, drastically cutting R&D, new product development, marketing and sales as well as fixating on matching the supply chain savings of companies like Dell in manufacturing, and WalMart in retail distribution.

Unfortunately, this strategy was out of date before Ms. Fiorina ever set it in motion. And all Mr. Hurd accomplished was short-term cuts that shored up immediate earnings while sacrificing any opportunities for creating long-term profitable new market development. By the time he was forced out HP had no growth direction. It's PC business fortunes are controlled by its suppliers, and the PC-based printer business is dying. Both primary markets are the victim of a major market shift away from PC use toward mobile devices, where HP has nothing.

HPs commitment to an outdated industrial era supply-side manufacturing strategy can be seen in its acquisitions. What was once the world's leading IT services company, EDS, was bought in 2008 after falling into financial disarray as that market shifted offshore. After HP spent nearly $14B on the purchase, HP used that business to try defending and extending PC product sales, but to little avail. The services group has been downsized regularly as growth evaporated in the face of global trends toward services offshoring and mobile use.

In 2009 HP spent almost $3B on networking gear manufacturer 3Com. But this was after the market had already started shifting to mobile devices and common carriers, leaving a very tough business that even market-leading Cisco has struggled to maintain. Growth again stagnated, and profits evaporated as HP was unable to bring any innovation to the solution set and unable to create any new markets.

In 2010 HP spent $1B on the company that created the hand-held PDA (personal digital assistant) market – the forerunner of our wirelessly connected smartphones – Palm. But that became an enormous fiasco as its WebOS products were late to market, didn't work well and were wholly uncompetitive with superior solutions from Apple and Android suppliers. Again, the industrial-era strategy left HP short on innovation, long on supply chain, and resulted in big write-offs.

Clearly what HP needs is a new strategy. One aligned with the information era in which we live. Think like Apple, which instead of chasing Macs a decade ago shifted into new markets. By creating new products that enhanced mobility Apple came back from the brink of complete failure to spectacular highs. HP needs to learn from this, and pursue an entirely new direction.

But, Meg Whitman is certainly no Steve Jobs. Her career at eBay was far from that of an innovator. eBay rode the growth of internet retailing, but was not Amazon. Rather, instead of focusing on buyers, and what they want, eBay focused on sellers – a classic industrial-era approach. eBay has not been a leader in launching any new technologies (such as Kindle or Fire at Amazon) and has not even been a leader in mobile applications or mobile retail.

While CEO at eBay Ms. Whitman purchased PayPal. But rather than build that platform into the next generation transaction system for web or mobile use, Paypal was used to defend and extend the eBay seller platform. Even though PayPal was the first leader in on-line payments, the market is now crowded with solutions like Google Wallets (Google,) Square (from a Twitter co-founder,) GoPayment (Intuit) and Isis (collection of mobile companies.)

Had Ms. Whitman applied an information-era strategy Paypal could have been a global platform changing the way payment processing is handled. Instead its use and growth has been limited to supporting an historical on-line retail platform. This does not bode well for the future of HP.

HP cannot save its way to prosperity. That never works. Try to think of one turnaround where it did – GM? Tribune Corp? Circuit City? Sears? Best Buy? Kodak? To successfully turn around HP must move – FAST – to innovate new solutions and enter new markets. It must change its strategy to behave a lot more like the company that created the oscilliscope and usher in the electronics age, and a lot less like the industrial-era company it has become – destroying shareholder value along the way.

Is HP so cheap that it's a safe bet. Not hardly. HP is on the same road as DEC, Wang, Lanier, Gateway Computers, Sun Microsystems and Silicon Graphics right now. And that's lousy for investors and employees alike.

by Adam Hartung | Jan 14, 2012 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership

A lot of excitement was generated this week when Mitt Romney said the words "I like to fire people." I'm sure he wishes he could rephrase his comment, as he easily could have made his point about changing service providers without those words. Nonetheless, the aftermath turned to a discussion of job losses, and why Bain Capital has eliminated jobs while simultaneously creating some.

Surprisingly, a number of economists suddenly started saying that firms like Bain Capital are justified in their job eliminations because they are merely implementing "creative destruction." Although the leap is not obvious, the argument goes that some businesses are made inefficient and unprofitable by new technologies or business processes – so buyers (like Bain Capital) of hurting businesses often cannot "fix" the situation and have no choice but to close them. Bain Capital inevitably will be stuck with losers it has no choice but to shutter – eliminating the jobs with the company.

Unfortunately, that argument is simply not true. The only thing that allows "creative destruction" to kill a company is a lack of good leadership. Any company can find a growth path if its leaders are willing to learn from trends and steer in the growing direction.

Start by looking at recent events surrounding Kodak and Hostess, both quickly heading for Chapter 11. Neither needed to fail. Management made the decisions which steered them into the whirlpool of failure.

Kodak watched the market for amateur photography shrink for 30 years – drying up profits for film and paper. Yet, management consistently – quarter after quarter and year after year – made the decision to try defending and extending the historical market rather than move the company into faster growing, more profitable opportunities. Kodak even invented much of the technology for digital photography, but chose to license it to others rather than develop the market because Kodak feared cannibalizing existing sales – as they became increasingly at risk!

Hostess is making a return trip to Chapter 11 this decade. But it's not like the trend away from highly processed, shelf stable white bread and sugary pastry snacks is anything new. While 1960s parents and youth might have enjoyed the vitamin enriched Wonder Bread "helping grow bodies 12 ways" the trend toward fresher, and healthier, staples has been happening for 40 years. In the 1980s when the company was known as Continental Baking profits were problematic, and it was clear that to keep what was then the nation's largest truck fleet profitable required new products as consumers were shifting to fresher "bake off" goods in the grocery store as well as brands promising more fiber and taste. But despite these obvious trends, leadership continued trying to defend and extend the business rather than shift it.

These stories weren't "creative destruction." They were simply bad leadership. Decisions were made to do more of the same, when clearly something desperately different was needed! At the Harvard Business School Working Knowledge web site famed strategiest Michael Porter states "the granddaddy of all mistakes is competing to be the best, going down the same path as everybody else and thinking that somehow you can achieve better results." Failure happened because the leaders were so internally focused they chose to ignore external inputs, trends, which would have driven better decisions!

In the 1980s Singer realized that the sewing machine market was destined to decline as women left homemaking for paying jobs, and as textile industry advances made purchased clothing cheaper than self-made. Over a few years the company transitioned out of the traditional, but dying, business and became a very successful defense industry contractor! Rather than letting itself be "creatively destroyed" Singer identified the market trends and moved from decline to growth!

Similarly, IBM almost failed as the computer market shifted from mainframes to PCs, but before all was lost (including jobs as well as investor value) leaders changed company focus from hardware to services and vertical market solutions allowing IBM to grow and thrive.

The failure of Digital Equipment (DEC) at the same time was not "creative destruction" but company leadership unwillingness to shift from declining mini-computer and high priced workstation sales into new businesses.

More recently, over the last decade a nearly dead Apple resurrected itself by tying into the large trend for mobility, rather than focusing on its niche Mac product sales. Company leaders took the company into consumer electronics (ipod, ipod touch,) tablet computing and cloud-based solutions (iPad) and mobile telephony with digital apps (iPhone.) Apple had no legacy in any of these markets, but by linking to trends rather than fixating on past businesses "creative destruction" was avoided.

There are many businesses today that are in trouble because leaders simply won't pay attention to trends. Avon, Sears and Barnes & Noble are three companies with limited futures simply because leaders seem unable to pull their heads out of the internal strategic planning sand and look at environmental trends in order to shift.

My favorite target is, of course, Microsoft. Nobody thinks we will be carrying laptop PCs around in 5 years. Yet, Microsoft has been unable to recognize the trend away from PCs and do anything effective. Its efforts in music (Zune) and mobile handsets have been indifferent, insufficiently supported and mostly dropped. Mr. Ballmer continues to speak about a long future for PC sales even as Q4 volume dropped 1.4% according to IDC and Gartner. Even though everyone knows this trend is due to limited PC innovation and rapidly accelerating mobile-based solutions, Microsoft blamed the problem on, of all things, floods in Thailand that restricted manufacturing output. Really.

We'll learn soon enough just how many jobs Bain Capital created, and killed. But those lost were not due to "creative destruction." They were due to leadership decisions to discontinue the business rather than invest in trends and transitioning to new markets. Creative destruction is an easy excuse to avoid blaming leaders for failures caused by their unwillingness to recognize trends and take actions to invest in them which will create winning businesses.