by Adam Hartung | Feb 18, 2014 | Current Affairs, Games, In the Swamp, Leadership

Microsoft has a new CEO. And a new Chairman. The new CEO says the company needs to focus on core markets. And analysts are making the same cry.

Amidst this organizational change, xBox continues its long history of losing money – as much as $2B/year. And early 2014 results show that xBox One is selling at only half the rate of Sony’s Playstation 4, with cumulative xBox One sales at under 70% of PS4, leading Motley Fool to call xBox One a “total failure.”

While calling xBox One a failure may be premature, Microsoft investors have plenty to worry about.

Firstly, the console game business has not been a profitable market for anyone for quite a while.

The old leader, Nintendo, watched sales crash in 2013, first quarter 2014 estimates reduced by 67% and the CEO now projecting the company will be unproftable for the year. Nintendo stock declined by 2/3 between 2010 and 2012, then after some recovery in 2013 lost 17% on the January day of its disappointing sales expectation. Not a great market indicator.

The new sales leader is Sony, but that should give no one reason to cheer. Sony lost money for 4 straight years (2008-2012), and was barely able to squeek out a 2013 profit only because it took a massive $4.6B 2012 loss which cleared the way to show something slightly better than break-even. Now S&P has downgraded Sony’s debt to near junk status. While PS4 sales are better than xBox One, in the fast shifting world of gaming this is no lock on future sales as game developers constantly jockey dollars between platforms.

Whether Sony will make money on PS4 in 2014 is far from proven. Especially since it sells for $100/unit (20%) less than xBox One – which compresses margins. What investors (and customers) can expect is an ongoing price war between Nintendo, Sony and Microsoft to attract sales. A competition which historically has left all competitors with losses – even when they win the market share war.

And on top of all of this is the threat that console market growth may stagnate as gamers migrate toward games on mobile devices. How this will affect sales is unknown. But given what happened to PC sales it’s not hard to imagine the market for consoles to become smaller each year, dominated by dedicated game players, while the majority of casual game players move to their convenient always-on device.

Due to its limited product range, Nintendo is in a “fight to the death” to win in gaming. Sony is now selling its PC business, and lacks strong offerings in most consumer products markets (like TVs) while facing extremely tough competition from Samsung and LG. Sony, likewise, cannot afford to abandon the Playstation business, and will be forced to engage in this profit killing battle to attract developers and end-use customers.

When businesses fall into profit-killing price wars the big winner is the one who figures out how to exit first. Back in the 1970s when IBM created domination in mainframes the CEO of GE realized it was a profit bloodbath to fight for sales against IBM, Sperry Rand and RCA. Thinking fast he made a deal to sell the GE mainframe business to RCA so the latter could strengthen its campaign as an IBM alternative, and in one step he stopped investing in a money-loser while strenghtening the balance sheet in alternative markets like locomotives and jet engines – which went on to high profits.

With calls to focus, Microsoft is now abandoning XP. It is working to force customers to upgrade to either Windows 7 or Windows 8. As PC sales continue declining, Microsoft faces an epic battle to shore up its position in cloud services and maintain its enterprise customers against competitors like Amazon.

After a decade in gaming, where it has never made money, now is the time for Microsoft to recognize it does not know how to profit from its technology – regardless how good. Microsoft could cleve off Kinect for use in its cloud services, and give its installed xBox base (and developer community) to Nintendo where the company could focus on lower cost machines and maintain its fight with Sony.

Analysts that love focus would cheer. They would cheer the benefit to Nintendo, and the additional “focus” to Microsoft. Microsoft would stop investing in the unprofitable game console market, and use resources in markets more likely to generate high returns. And, with some sharp investment bankers, Microsoft could also probably keep a piece of the business (in Nintendo stock) that it could sell at a future date if the “suicide” console business ever turns into something profitable.

Sometimes smart leadership is knowing when to “cut and run.”

Links:

2012 recognition that Sony was flailing without a profitable strategy

January, 2013 forecast that microsoft would abandon gaming

by Adam Hartung | Nov 6, 2013 | Defend & Extend, Innovation, Leadership, Web/Tech

Can you believe it has been only 12 years since Apple introduced the iPod? Since then Apple’s value has risen from about $11 (January, 2001) to over $500 (today) – an astounding 45X increase.

With all that success it is easy to forget that it was not a “gimme” that the iPod would succeed. At that time Sony dominated the personal music world with its Walkman hardware products and massive distribution through consumer electronics chains such as Best Buy, and broad-line retailers like Wal-Mart. Additionally, Sony had its own CD label, from its acquisition of Columbia Records (renamed CBS Records,) producing music. Sony’s leadership looked impenetrable.

But, despite all the data pointing to Sony’s inevitable long-term domination, Apple launched the iPod. Derided as lacking CD quality, due to MP3’s compression algorithms, industry leaders felt that nobody wanted MP3 products. Sony said it tried MP3, but customers didn’t want it.

All the iPod had going for it was a trend. Millions of people had downloaded MP3 songs from Napster. Napster was illegal, and users knew it. Some heavy users were even prosecuted. But, worse, the site was riddled with viruses creating havoc with all users as they downloaded hundreds of millions of songs.

Eventually Napster was closed by the government for widespread copyright infreingement. Sony, et.al., felt the threat of low-priced MP3 music was gone, as people would keep buying $20 CDs. But Apple’s new iPod provided mobility in a way that was previously unattainable. Combined with legal downloads, including the emerging Apple Store, meant people could buy music at lower prices, buy only what they wanted and literally listen to it anywhere, remarkably conveniently.

The forecasted “numbers” did not predict Apple’s iPod success. If anything, good analysis led experts to expect the iPod to be a limited success, or possibly failure. (Interestingly, all predictions by experts such as IDC and Gartner for iPhone and iPad sales dramatically underestimated their success, as well – more later.) It was leadership at Apple (led by the returned Steve Jobs) that recognized the trend toward mobility was more important than historical sales analysis, and the new product would not only sell well but change the game on historical leaders.

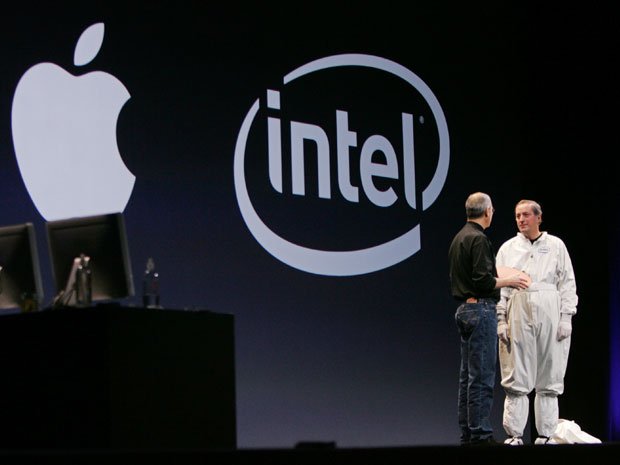

Which takes us to the mistake Intel made by focusing on “the numbers” when given the opportunity to build chips for the iPhone. Intel was a very successful company, making key components for all Microsoft PCs (the famous WinTel [for Windows+Intel] platform) as well as the Macintosh. So when Apple asked Intel to make new processors for its mobile iPhone, Intel’s leaders looked at the history of what it cost to make chips, and the most likely future volumes. When told Apple’s price target, Intel’s leaders decided they would pass. “The numbers” said it didn’t make sense.

Uh oh. The cost and volume estimates were wrong. Intel made its assessments expecting PCs to remain strong indefinitely, and its costs and prices to remain consistent based on historical trends. Intel used hard, engineering and MBA-style analysis to build forecasts based on models of the past. Intel’s leaders did not anticipate that the new mobile trend, which had decimated Sony’s profits in music as the iPod took off, would have the same impact on future sales of new phones (and eventually tablets) running very thin apps.

Harvard innovation guru Clayton Christensen tells audiences that we have complete knowledge about the past. And absolutely no knowledge about the future. Those who love numbers and analysis can wallow in reams and reams of historical information. Today we love the “Big Data” movement which uses the world’s most powerful computers to rip through unbelievable quantities of historical data to look for links in an effort to more accurately predict the future. We take comfort in thinking the future will look like the past, and if we just study the past hard enough we can have a very predictible future.

But that isn’t the way the business world works. Business markets are incredibly dynamic, subject to multiple variables all changing simultaneously. Chaos Theory lecturers love telling us how a butterfly flapping its wings in China can cause severe thunderstorms in America’s midwest. In business, small trends can suddenly blossom, becoming major trends; trends which are easily missed, or overlooked, possibly as “rounding errors” by planners fixated on past markets and historical trends.

Markets shift – and do so much, much faster than we anticipate. Old winners can drop remarkably fast, while new competitors that adopt the trends become “game changers” that capture the market growth.

In 2000 Apple was the “Mac” company. Pretty much a one-product company in a niche market. And Apple could easily have kept trying to defend & extend that niche, with ever more problems as Wintel products improved.

But by understanding the emerging mobility trend leadership changed Apple’s investment portfolio to capture the new trend. First was the iPod, a product wholly outside the “core strengths” of Apple and requiring new engineering, new distribution and new branding. And a product few people wanted, and industry leaders rejected.

Then Apple’s leaders showed this talent again, by launching the iPhone in a market where it had no history, and was dominated by Motorola and RIMM/BlackBerry. Where, again, analysts and industry leaders felt the product was unlikely to succeed because it lacked a keyboard interface, was priced too high and had no “enterprise” resources. The incumbents focused on their past success to predict the future, rather than understanding trends and how they can change a market.

Too bad for Intel. And Blackberry, which this week failed in its effort to sell itself, and once again changed CEOs as the stock hit new lows.

Then Apple did it again. Years after Microsoft attempted to launch a tablet, and gave up, Apple built on the mobility trend to launch the iPad. Analysts again said the product would have limited acceptance. Looking at history, market leaders claimed the iPad was a product lacking usability due to insufficient office productivity software and enterprise integration. The numbers just did not support the notion of investing in a tablet.

Anyone can analyze numbers. And today, we have more numbers than ever. But, numbers analysis without insight can be devastating. Understanding the past, in grave detail, and with insight as to what used to work, can lead to incredibly bad decisions. Because what really matters is vision. Vision to understand how trends – even small trends – can make an enormous difference leading to major market shifts — often before there is much, if any, data.

by Adam Hartung | Sep 12, 2013 | General, In the Whirlpool, Leadership

This week the people who decide what composes the Dow Jones Industrial Average booted off 3 companies and added 3 others. What's remarkable is how little most people cared!

"The Dow," as it is often called, is intended to represent the core of America's economy. "As the Dow goes, so goes America" is the theory. It is one of the most watched indices of all markets, with many people tracking how much it goes up, or down, every trading day. So being a component of the DJIA is a pretty big deal.

It's not a good day when you find out your company has been removed from the index. Because it is a very public statement that your company simply isn't all that important any more. Certainly not as important as it once was! Your relevance, once considered core to representing the economy, has dissipated. And, unfortunately, most companies that fall off the DJIA slip away into oblivion.

I have a simple test. Do like Jay Leno, of Tonight Show fame, and simply ask a dozen college graduates that are between 26 and 31 about a company. If they know that company, and are positively influenced by it, you have relevancy. If they don't care about that company then the CEO and Board should take note, because it is an early indicator that the company may well have lost relevancy and is probably in more trouble than the leaders want to admit.

Ask these folks about Alcoa (AA) and what do you imagine the typical response? "Alcoa?" It is a rare person under 40 who knows that Alcoa was once the king of aluminum — back when we wrapped food in "tin foil" and before we all drank sodas and beer from a can. To most, "Alcoa" is a random set of letters with no meaning – like Altria – rather than its origin as ALuminum COrporation of America.

But, its not even the largest aluminum company any more. Alcoa is now 3rd. In a world where we live on smartphones and tablets, who really cares about a mining company that deals in commodities? Especially the third largest with no growth prospects?

Speaking of smartphones, Hewlett Packard (HPQ) was recently considered a bellweather of the tech industry. An early innovator in test equipment, it was one of the original "Silicon Valley" companies. But its commitment to printers has left people caring little about the company's products, since everyone prints less and less as we read more and more off digital screens.

Past-CEO Fiorina's huge investment in PCs by buying Compaq (which previously bought minicomputer maker DEC,) committed the rest of HP into what is now one of the fastest shrinking markets. And in PCs, HP doesn't even have any technology roots. HP is just an assembler, mostly offshore, as its products are all based on outsourced chip and software technology.

What a few years ago was considered a leader in technology has become a company that the younger crowd identifies with technology products they rarely use, and never buy. And lacking any sort of exciting pipeline, nobody really cares about HP.

Bank of America (BAC) was one of the 2 leaders in financial services when it entered the DJIA. It was a powerhouse in all things banking. But, as the mortgage market disintegrated B of A rapidly fell into trouble. It's shotgun wedding with Merrill Lynch to save the investment bank from failure made the B of A bigger, but not stronger.

Now racked with concerns about any part of the institution having long-term success against larger, and better capitalized, banks in America and offshore has left B of A with a lot of branches, but no market leadership. What innovations B of A may have had in lending or derivatives are now considered headaches most people either don't understand, or largely despise.

These 3 companies were once great lions of their industries. And they were rewarded with placement on the DJIA as icons of the economy. But they now leave with a whimper. Their values so shredded that their departure makes almost no impact on calculating the DJIA using the remaining companies. (Note: the DJIA calculation was significantly impacted by the addition of much higher valued companies Nike, Goldman Sachs and Visa.)

If we look at some past examples of other companies removed from the DJIA, one should be skeptical about the long-term future for these three:

- 2009 – GM removed due to bankruptcy

- 2004 – AT&T and Kodak removed (both ended up in bankruptcy)

- 1999 – Goodyear, Union Carbide, Sears

- 1997 – Westinghouse, Woolworths

- 1991 – American Can, Navistar/International Harvester

Any company can lose relevancy. Markets shift. There is risk incurred by focusing on the status quo (Status Quo Risk.) New technology, regulations, competitors, business practices — innovations of all sorts — enter the market daily. Being really good at something, in fact being the worlds BEST at something, does not insure success or longevity (despite the popularity of In Search of Excellence).

When markets shift, and your company doesn't, you can find yourself without relevancy. And with a fast declining value. Whether you are iconic – or not.

by Adam Hartung | Sep 4, 2013 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Lock-in, Web/Tech

Just over a week after Microsoft announces plans to replace CEO Steve Ballmer the company announced it will spend $7.2B to buy the Nokia phone/tablet business. For those looking forward to big changes at Microsoft this was like sticking a pin in the big party balloon!

Everyone knows that Microsoft's future is at risk now that PC sales are declining globally at nearly 10% – with developing markets shifting even faster to mobile devices than the USA. And Microsoft has been the perpetual loser in mobile devices; late to market and with a product that is not a game changer and has only 3% share in the USA.

But, despite this grim reality, Microsoft has doubled-down (that's doubled its bet for non-gamblers) on its Windows 8 OS strategy, and continues to play "bet the company". Nokia's global market share has shriveled to 15% (from 40%) since former Microsoft exec-turned-Nokia-CEO Stephen Elop committed the company to Windows 8. Because other Microsoft ecosystem companies like HP, Acer and HP have been slow to bring out Win 8 devices, Nokia has 90% of the miniscule market that is Win 8 phones. So this acquisition brings in-house a much deeper commitment to spending on an effort to defend & extend Microsoft's declining O/S products.

As I predicted in January, the #1 action we could expect from a Ballmer-led Microsoft is pouring more resources into fighting market leaders iOS and Android – an unwinnable war. Previously there was the $8.5B Skype and the $400M Nook, and now a $7.2B Nokia. And as 32,000 Nokia employees join Microsoft losses will surely continue to rise. While Microsoft has a lot of cash – spending it at this rate, it won't last long!

Some folks think this acquisition will make Microsoft more like Apple, because it now will have both hardware and software which in some ways is like Apple's iPhone. The hope is for Apple-like sales and margins soon. But, unfortunately, Google bought Motorola months ago and we've seen that such revenue and profit growth are much harder to achieve than simply making an acquisition. And Android products are much more popular than Win8. Simply combining Microsoft and Nokia does not change the fact that Win8 products are very late to market, and not very desirable.

Some have postulated that buying Nokia was a way to solve the Microsoft CEO succession question, positioning Mr. Elop for Mr. Ballmer's job. While that outcome does seem likely, it would be one of the most expensive recruiting efforts of all time. The only reason for Mr. Elop to be made Microsoft CEO is his historical company relationship, not performance. And that makes Mr. Elop is exactly the wrong person for the Microsoft CEO job!

In October, 2010 when Mr. Elop took over Nokia I pointed out that he was the wrong person for that job – and he would destroy Nokia by making it a "Microsoft shop" with a Microsoft strategy. Since then sales are down, profits have evaporated, shareholders are in revolt and the only good news has been selling the dying company to Microsoft! That's not exactly the best CEO legacy.

Mr. Elop's job today is to sell more Win8 mobile devices. Were he to be made Microsoft CEO it is likely he would continue to think that is his primary job – just as Mr. Ballmer has believed. Neither CEO has shown any ability to realize that the market has already shifted, that there are two leaders far, far in front with brand image, products, apps, developers, partners, distribution, market share, sales and profits. And it is impossible for Microsoft to now catch up.

It is for good reason that short-term traders pushed down Microsoft's share value after the acquisition was announced. It is clear that current CEO Ballmer and Microsoft's Board are still stuck fighting the last war. Still trying to resurrect the Windows and Office businesses to previous glory. Many market anallysts see this as the last great effort to make Ballmer's bet-the-company on Windows 8 pay off. But that's a bet which every month is showing longer and longer odds.

Microsoft is not dead. And Microsoft is not without the ability to turn around. But it won't happen unless the Board recognizes it needs to steer Microsoft in a vastly different direction, reduce (rather than increase) investments in Win8 (and its devices,) and create a vision for 2020 where Microsoft is highly relevant to customers. So far, we're seeing all the wrong moves.

by Adam Hartung | Jun 28, 2013 | Current Affairs, Defend & Extend, In the Rapids, In the Whirlpool, Innovation, Leadership, Web/Tech

The last 12 months Tesla Motors stock has been on a tear. From $25 it has more than quadrupled to over $100. And most analysts still recommend owning the stock, even though the company has never made a net profit.

There is no doubt that each of the major car companies has more money, engineers, other resources and industry experience than Tesla. Yet, Tesla has been able to capture the attention of more buyers. Through May of 2013 the Tesla Model S has outsold every other electric car – even though at $70,000 it is over twice the price of competitors!

During the Bush administration the Department of Energy awarded loans via the Advanced Technology Vehicle Manufacturing Program to Ford ($5.9B), Nissan ($1.4B), Fiskar ($529M) and Tesla ($465M.) And even though the most recent Republican Presidential candidate, Mitt Romney, called Tesla a "loser," it is the only auto company to have repaid its loan. And did so some 9 years early! Even paying a $26M early payment penalty!

How could a start-up company do so well competing against companies with much greater resources?

Firstly, never underestimate the ability of a large, entrenched competitor to ignore a profitable new opportunity. Especially when that opportunity is outside its "core."

A year ago when auto companies were giving huge discounts to sell cars in a weak market I pointed out that Tesla had a significant backlog and was changing the industry. Long-time, outspoken industry executive Bob Lutz – who personally shepharded the Chevy Volt electric into the market – was so incensed that he wrote his own blog saying that it was nonsense to consider Tesla an industry changer. He predicted Tesla would make little difference, and eventually fail.

For the big car companies electric cars, at 32,700 units January thru May, represent less than 2% of the market. To them these cars are simply not seen as important. So what if the Tesla Model S (8.8k units) outsold the Nissan Leaf (7.6k units) and Chevy Volt (7.1k units)? These bigger companies are focusing on their core petroleum powered car business. Electric cars are an unimportant "niche" that doesn't even make any money for the leading company with cars that are very expensive!

This is the kind of thinking that drove Kodak. Early digital cameras had lots of limitations. They were expensive. They didn't have the resolution of film. Very few people wanted them. And the early manufacturers didn't make any money. For Kodak it was obvious that the company needed to remain focused on its core film and camera business, as digital cameras just weren't important.

Of course we know how that story ended. With Kodak filing bankruptcy in 2012. Because what initially looked like a limited market, with problematic products, eventually shifted. The products became better, and other technologies came along making digital cameras a better fit for user needs.

Tesla, smartly, has not tried to make a gasoline car into an electric car – like, say, the Ford Focus Electric. Instead Tesla set out to make the best car possible. And the company used electricity as the power source. By starting early, and putting its resources into the best possible solution, in 2013 Consumer Reports gave the Model S 99 out of 100 points. That made it not just the highest rated electric car, but the highest rated car EVER REVIEWED!

As the big car companies point out limits to electric vehicles, Tesla keeps making them better and addresses market limitations. Worries about how far an owner can drive on a charge creates "range anxiety." To cope with this Tesla not only works on battery technology, but has launched a program to build charging stations across the USA and Canada. Initially focused on the Los-Angeles to San Franciso and Boston to Washington corridors, Tesla is opening supercharger stations so owners are never less than 200 miles from a 30 minute fast charge. And for those who can't wait Tesla is creating a 90 second battery swap program to put drivers back on the road quickly.

This is how the classic "Innovator's Dilemma" develops. The existing competitors focus on their core business, even though big sales produce ever declining profits. An upstart takes on a small segment, which the big companies don't care about. The big companies say the upstart products are pretty much irrelevant, and the sales are immaterial. The big companies choose to keep focusing on defending and extending their "core" even as competition drives down results and customer satisfaction wanes.

Meanwhile, the upstart keeps plugging away at solving problems. Each month, quarter and year the new entrant learns how to make its products better. It learns from the initial customers – who were easy for big companies to deride as oddballs – and identifies early limits to market growth. It then invests in product improvements, and market enhancements, which enlarge the market.

Eventually these improvements lead to a market shift. Customers move from one solution to the other. Not gradually, but instead quite quickly. In what's called a "punctuated equilibrium" demand for one solution tapers off quickly, killing many competitors, while the new market suppliers flourish. The "old guard" companies are simply too late, lack product knowledge and market savvy, and cannot catch up.

- The integrated steel companies were killed by upstart mini-mill manufacturers like Nucor Steel.

- Healthier snacks and baked goods killed the market for Hostess Twinkies and Wonder Bread.

- Minolta and Canon digital cameras destroyed sales of Kodak film – even though Kodak created the technology and licensed it to them.

- Cell phones are destroying demand for land line phones.

- Digital movie downloads from Netflix killed the DVD business and Blockbuster Video.

- CraigsList plus Google stole the ad revenue from newspapers and magazines.

- Amazon killed bookstore profits, and Borders, and now has its sites set on WalMart.

- IBM mainframes and DEC mini-computers were made obsolete by PCs from companies like Dell.

- And now Android and iOS mobile devices are killing the market for PCs.

There is no doubt that GM, Ford, Nissan, et. al., with their vast resources and well educated leadership, could do what Tesla is doing. Probably better. All they need is to set up white space companies (like GM did once with Saturn to compete with small Japanese cars) that have resources and free reign to be disruptive and aggressively grow the emerging new marketplace. But they won't, because they are busy focusing on their core business, trying to defend & extend it as long as possible. Even though returns are highly problematic.

Tesla is a very, very good car. That's why it has a long backlog. And it is innovating the market for charging stations. Tesla leadership, with Elon Musk thought to be the next Steve Jobs by some, is demonstrating it can listen to customers and create solutions that meet their needs, wants and wishes. By focusing on developing the new marketplace Tesla has taken the lead in the new marketplace. And smart investors can see that long-term the odds are better to buy into the lead horse before the market shifts, rather than ride the old horse until it drops.