Toys R Us filed for bankruptcy this week. And the obvious response was “another retailer slaughtered by Amazon and on-line retailing.” But this conclusion comes short of describing why Toys R Us leadership did not do the obvious things to keep Toys R Us relevant.

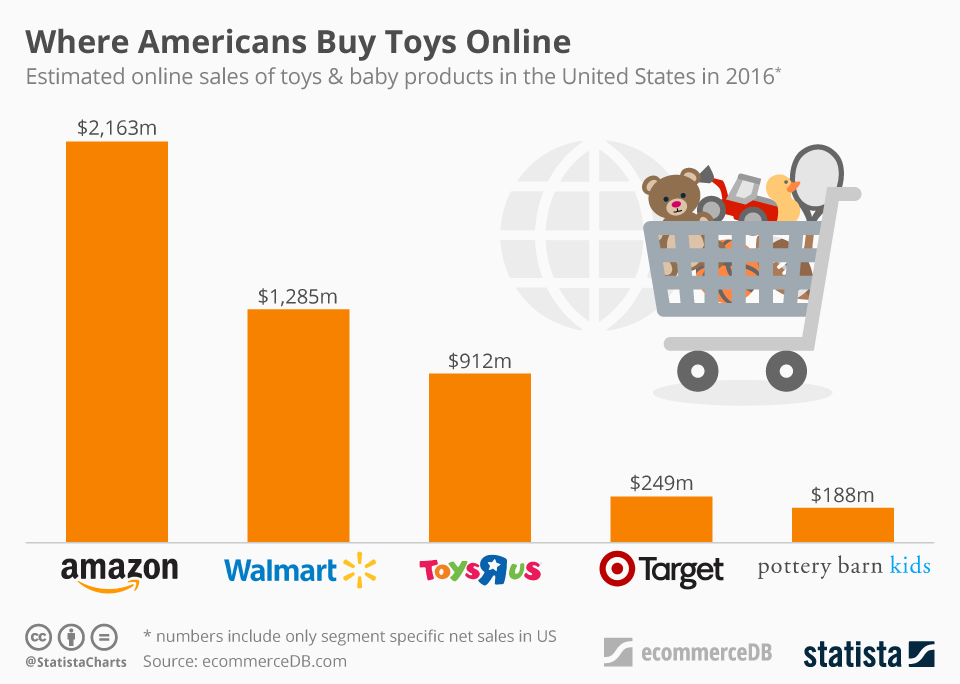

Amazon and WalMart both eclipsed Toys R Us in toy retail sales.

Chart courtesy of Felix Richter, Statista

Everyone, and I mean everyone, knew over the last decade that customers were buying more stuff on-line, including toys. And everyone also knew that WalMart was pushing extremely hard to keep customers going to their stores by offering products like toys at low prices. And, it was clear that customers were shifting to buying more toys from both these retailers. If this was so obvious to everyone, why didn’t Toys R Us leadership do something? After all, Toys R Us is a multi-billion dollar revenue company.

The LBO

It was over 30 years ago when financiers discovered they could buy a company, sell off some assets and otherwise increase the company’s cash, then convince banks and bondholders to load the company with debt. These financiers would then pull out the cash for themselves, and leave the company with a ton of debt. The LBO (leveraged buy out) was born, invented by investment bankers like KKR (named for founders Kohlberg, Kravis & Roberts.) They would use a small bit of private equity, and then use the company’s own assets to raise debt money (leverage) to buy the company. By “restructuring” the company to a lower cost of operations, usually with draconian reductions, they would increase cash flow to make higher debt repayments. Then they would either take the money out directly, or take the company public where they could sell their shares, and make themselves rich. This form of deal making birthed what we now call the Private Equity business.

In 2005, KKR and Bain Capital (which included former Presidential candidate Mitt Romney) bought Toys R Us for about $6.6billion, plus assuming just under $1B of debt, for a total valuation of $7.5billion. But the private equity guys didn’t buy the company with equity. They only put in $1.3billion, and used the company’s assets to raise $5.3billion in additional debt, making total debt a whopping $6.2B. Total debt was now a remarkable 82.7% of total capital! At the time of the deal interest rates on that debt were around 7.25%, creating a cash outflow of $450million/year just to pay interest on the loans. At the time Toys R Us was barely making a profit of 2% – so the debt was double company net profits.

Debt led to bad management decisions and ultimately bankruptcy of the U.S. company

The biggest assumption behind a debt-financed takeover is that the company can cut costs to improve cash flow and thus pay the interest. But behind that assumption is an even bigger assumption. That the marketplace won’t change dramatically. The KKR and Bain Capital leaders assumed they could shrink Toys R Us in a way that would lower operating costs. They also assumed they could sell some under-utilized assets to raise cash. They did not assume they would need contingency money if competition, and the marketplace, changed in some unplanned way.

eCommerce was pretty new in 2005. Amazon was an $8.5 billion company, but it didn’t make any profits and very few predicted then it would become today’s $100 billion behemoth. Because the financiers didn’t anticipate a big market shift to ecommerce, they focused on the war with Walmart and Target. Their plans were to lower operating costs, close some stores that were underperforming, license some offshore stores, and sell some assets (like real estate owned or leases) to raise cash and repay the debt.

But they weren’t prepared to take on another, entirely different competitor on-line. As Amazon’s growth affected all retailers, Toys R Us simply did not have the resources to fight the traditional discount and dollar brick-and-mortar retailers, and build a major on-line presence, and keep paying that debt. While it is easy to sit on the sidelines and say that Toys R Us should have spent more money building its on-line presence in order to remain relevant, the fact is that the deal in 2005 left the company with insufficient cash flow to do so. Regardless of what leadership might have wanted to do, simply keeping the lights on was a tough challenge when having to pay out so much cash to bondholders.

And the investors simply did not expect that the growth of on-line retailing would stall traditional retail stores, thus creating a major loss of value for retail real estate. U.S. retail real estate value had increased in value for decades. The assumption was that the real estate, whether owned or leased, would continue to go up in value. Real estate was a “hard” asset that KKR and Bain Capital could bank on for raising cash to repay the debt. But as on-line retail grew, and traditional retail declined, America became “over stored” with far too much retail space. Prices were shattered in many markets, and it was not possible for Toys R Us to sell those assets for a gain that would meet the debt obligations.

With $400 million of debt coming due next year, Toys R Us simply doesn’t have the cash flow, or assets, to repay those bondholders

Old assumptions about finance are a big problem for companies today. Assumptions about “leveraging” hard assets, and intangibles like brand value, are no longer true. Competitors emerge, markets change, and old assets can lose value very fast. Assumptions about business model stability are no longer true, as new competitors using newer technology create new ways to sell, and often at lower cost than was ever expected. Assumptions about customer loyalty, and market share stability, are no longer true as new competitors appeal to customers differently and cause big shifts in buying behavior very fast. The speed with which technology, competitors, markets and customers shift now requires companies have the funds available to invest in change.

This story isn’t just about debt. The very popular activity of “returning money to shareholders by repurchasing stock” is a terrible idea. Stock repurchases do not make a company more valuable, nor a stronger competitor. Instead they burn through cash to reduce the company’s capitalization, and manipulate ratios like EPS (earnings per share) and P/E (price/earnings) multiple. Stock repurchases hurt companies, and make them less competitive. Good companies return money to shareholders by investing in growth, which raises sales, profits and increases the stock price making the company truly more valuable.

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

The important part of the Toys R Us story is realizing that the wrong financial decisions can doom your organization. You can have a great vision, and even great ideas about new ways to compete. But if you don’t have the money to invest in growth, it won’t happen. If leaders don’t have the money to spend on new projects and new markets, because they’re sending it all to bondholders or using it to repurchase shares in hopes of propping up a stock price, eventually there will be a market shift that will doom the old business model and leave it unable to compete.

To succeed today leaders need the money to invest in change, and they have to constantly invest it in change, or their companies will lose relevancy and end up like Toys R Us, Radio Shack, Circuit City, Aeropostale, The Limited, Payless Shoes, Gander Mountain, Golfsmith, Sports Authority, Borders Books and the great, original American retailer A&P.

I'd like to receive newsletters.

Thank you for an interesting article!