by Adam Hartung | Feb 3, 2016 | Current Affairs, Leadership, Lifecycle, Web/Tech

The three highest valued publicly traded companies today (2/3/16) are Google/Alphabet, Apple and Microsoft. All 3 are tech companies, and they compete – although with different business models – in multiple markets. However, investor views as to their futures are wildly different. And that has everything to do with how the leadership teams of these 3 companies have explained their recent results, and described their futures.

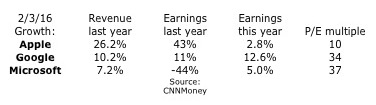

Looking at the financial performance of these companies, it is impossible to understand the price/earnings multiple assigned to each. Apple clearly had better revenue and earnings performance in all but the most recent year. Yet, both Alphabet and Microsoft have price to earnings (P/E) multiples that are 3-4 times that of Apple.

Much was made this week about Alphabet’s valuation exceeding that of Apple’s. But the really big story is the difference in multiples. If Apple had a multiple even half that of Alphabet or Microsoft it’s value would be much, much higher.

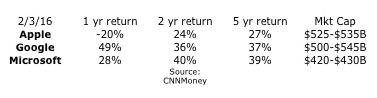

But, as we can see, investors did the best over both 2 years and 5 years by investing in Microsoft. And Apple investors have fared the poorest of all 3 companies regardless of time frame. Looking at investment performance, one would think that the revenue and earnings performance of these companies would be the reverse of what’s seen in the first chart.

The missing piece, of course, is future expectations. In this column a few days ago, I pointed out that Apple has done a terrible job explaining its future. In that column I pointed out how Facebook and Amazon both had stratospheric P/E multiples because they were able to keep investors focused on their future growth story, even more than their historical financial performance.

Alphabet stole the show, and at least briefly the #1 valuation spot, from Apple by convincing investors they will see significant, profitable growth. Starting even before earnings announcements the company was making sure investors knew that revenues and profits would be up. But even more they touted the notion that Alphabet has a lot of growth in non-monetized assets. For example, vastly greater ad sales should be expected from YouTube and Google Maps, as well as app sales for Android phones through Google Play. And someday on the short horizon profits will emerge from Fiber transmission revenues, smart home revenues via Nest, and even auto market sales now that the company has logged over 1million driverless miles.

This messaging clearly worked, as Alphabet’s value shot up. Even though 99% of the company’s growth was in “core” products that have been around for a decade! Yes, ad revenue was up 15%, but most of that was actually on the company’s own web sites. And most was driven by further price erosion. The number of paid clicks were up 30%, but price/click was actually down yet another 15% – a negative price trend that has been happening for years. Eventually prices will erode enough that volume will not make up the difference – and what will investors do then? Rely on the “moonshot” projects which still have almost no revenue, and no proven market performance!

But, the best performer has been Microsoft. Investors know that PC sales have been eroding for years, that PC sales will continue eroding as users go mobile, and that PC’s are the core of Microsoft’s revenue. Investors also knows that Microsoft missed the move to mobile, and has practically no market share in the war between Apple’s iOS and Google’s Android. Further, investors have known forever that gaming (xBox,) search and entertainment products have always been a money-loser for Microsoft. Yet, Microsoft investors have done far better than Apple investors, and long-term better than Google investors!

Microsoft has done an absolutely terrific job of constantly trumpeting itself as a company with a huge installed base of users that it can leverage into the future. Even when investors don’t know how that eroding base will be leveraged, Microsoft continually makes the case that the base is there, that Microsoft is the “enterprise” brand and that those users will stay loyal to Microsoft products.

Forget that Windows 8 was a failure, that despite the billions spent on development Win8 never reached even 10% of the installed base and the company is even dropping support for the product. Forget that Windows 10 is a free upgrade (meaning no revenue.) Just believe in that installed base.

Microsoft trumpeted that its Surface tablet sales rose 22% in the last quarter! Yay! Of course there was no mention that in just the last 6 weeks of the quarter Apple’s newly released iPad Pro actually sold more units than all Surface tablets did for the entire quarter! Or that Microsoft’s tablet market share is barely registerable, not even close to a top 5 player, while Apple still maintains 25% share. And investors are so used to the Microsoft failure in mobile phones that the 49% further decline in sales was considered acceptable.

Instead Microsoft kept investors focused on improvements to Windows 10 (that’s the one you can upgrade to for free.) And they made sure investors knew that Office 365 revenue was up 70%, as 20million consumers now use the product. Of course, that is a cumulative 20million – compared to the 75million iPhones Apple sold in just one quarter. And Azure revenue was up 140% – to something that is almost a drop in the bucket that is AWS which is over 10 times the size of all its competitors combined.

To many, this author included, the “growth story” at Microsoft is more than a little implausible. Sales of its core products are declining, and the company has missed the wave to mobile. Developers are writing for iOS first and foremost, because it has the really important installed base for today and tomorrow. And they are working secondarily on Android, because it is in some flavor the rest of the market. Windows 10 is a very, very distant third and largely overlooked. xBox still loses money, and the new businesses are all relatively quite small. Yet, investors in Microsoft have been richly rewarded the last 5 years.

Meanwhile, investors remain fearful of Apple. Too many recall the 1980s when Apple Macs were in a share war with Wintel (Microsoft Windows on Intel processors) PCs. Apple lost that war as business customers traded off the Macs ease of use for the lower purchase cost of Windows-based machines. Will Apple make the same mistake? Will iPad sales keep declining, as they have for 2 years now? Will the market shift to mobile favor lower-priced Android-based products? Will app purchases swing from iTunes to Google Play as people buy lower cost Android-based tablets? Have iPhone sales really peaked, and are they preparing to fall? What’s going to happen with Apple now? Will the huge Apple mobile share be eroded to nothing, causing Apple’s revenues, profits and share price to collapse?

This would be an interesting academic discussion were the stakes not so incredibly high. As I said in the opening paragraph, these are the 3 highest valued public companies in America. Small share price changes have huge impacts on the wealth of individual and institutional investors. It is rather quite important that companies tell their stories as good as possible (which Apple clearly has not, and Microsoft has done extremely well.) And likewise it is crucial that investors do their homework, to understand not only what companies say, but what they don’t say.

by Adam Hartung | Aug 29, 2014 | Current Affairs, In the Whirlpool, Leadership

It’s Labor Day, and a time when we naturally think about our jobs.

When it comes to jobs creation, no role is more critical than the CEO. No company will enter into a growth phase, selling more product and expanding employment, unless the CEO agrees. Likewise, no company will shrink, incurring job losses due to layoffs and mass firings, unless the CEO agrees. Both decisions lay at the foot of the CEO, and it is his/her skill that determines whether a company adds jobs, or deletes them.

Over 2 years ago (5 May, 2012) I published “The 5 CEOs Who Should Be Fired.” Not surprisingly, since then employment at all 5 of these companies has lagged economic growth, and in all but one case employment has shrunk. Yet, 3 of these CEOs remain in their jobs – despite lackluster (and in some cases dismal) performance. And all 5 companies are facing significant struggles, if not imminent failure.

#5 – John Chambers at Cisco

In 2012 it was clear that the market shift to public networks and cloud computing was forever changing the use of network equipment which had made Cisco a modern growth story under long-term CEO Chambers. Yet, since that time there has been no clear improvement in Cisco’s fortunes. Despite 2 controversial reorganizations, and 3 rounds of layoffs, Cisco is no better positioned today to grow than it was before.

Increasingly, CEO Chambers’ actions reorganizations and layoffs look like so many machinations to preserve the company’s legacy rather than a clear vision of where the company will grow next. Employee morale has declined, sales growth has lagged and although the stock has rebounded from 2012 lows, it is still at least 10% short of 2010 highs – even as the S&P hits record highs. While his tenure began with a tremendous growth story, today Cisco is at the doorstep of losing relevancy as excitement turns to cloud service providers like Amazon. And the decline in jobs at Cisco is just one sign of the need for new leadership.

#4 Jeff Immelt at General Electric

When CEO Immelt took over for Jack Welch he had some tough shoes to fill. Jack Welch’s tenure marked an explosion in value creation for the last remaining original Dow Jones Industrials component company. Revenues had grown every year, usually in double digits; profits soared, employment grew tremendously and both suppliers and investors gained as the company grew.

But that all stalled under Immelt. GE has failed to develop even one large new market, or position itself as the kind of leading company it was under Welch. Revenues exceeded $150B in 2009 and 2010, yet have declined since. In 2013 revenues dropped to $142B from $145B in 2012. To maintain revenues the company has been forced to continue selling businesses and downsizing employees every year. Total employment in 2014 is now less than in 2012.

Yet, Mr. Immelt continues to keep his job, even though the stock has been a laggard. From the near $60 it peaked at his arrival, the stock faltered. It regained to $40 in 2007, only to plunge to under $10 as the CEO’s over-reliance on financial services nearly bankrupted the once great manufacturing company in the banking crash of 2009. As the company ponders selling its long-standing trademark appliance business, the stock is still less than half its 2007 value, and under 1/3 its all time high. Where are the jobs? Not GE.

#3 Mike Duke at Wal-Mart

Mr. Duke has left Wal-Mart, but not in great shape. Since 2012 the company has been rocked by scandals, as it came to light the company was most likely bribing government officials in Mexico. Meanwhile, it has failed to defend its work practices at the National Labor Relations Board, and remains embattled regarding alleged discrimination of female employees. The company’s employment practices are regularly the target of unions and those supporting a higher minimum wage.

The company has had 6 consecutive quarters of declining traffic, as sales per store continue to lag – demonstrating leadership’s inability to excite people to shop in their stores as growth shifts to dollar stores. The stock was $70 in 2012, and is now only $75.60, even though the S&P 500 is up about 50%. So far smaller format city stores have not generated much attention, and the company remains far behind leader Amazon in on-line sales. WalMart increasingly looks like a giant trapped in its historical house, which is rapidly delapidating.

One big question to ask is who wants to work for WalMart? In 2013 the company threatened to close all its D.C. stores if the city council put through a higher minimum wage. Yet, since then major cities (San Francisco, Chicago, Los Angeles, Seattle, etc.) have either passed, or in the process of passing, local legislation increasing the minimum wage to anywhere from $12.50-$15.00/hour. But there seems no response from WalMart on how it will create profits as its costs rise.

#2 Ed Lampert at Sears

Nine straight quarterly losses. That about says it all for struggling Sears. Since the 5/2012 column the CEO has shuttered several stores, and sales continue dropping at those that remain open. Industry pundits now call Sears irrelevant, and the question is looming whether it will follow Radio Shack into oblivion soon.

CEO Lampert has singlehandedly destroyed the Sears brand, as well as that of its namesake products such as Kenmore and Diehard. He has laid off thousands of employees as he consolidated stores, yet he has been unable to capture any value from the unused real estate. Meanwhile, the leadership team has been the quintessential example of “a revolving door at headquarters.” From about $50/share 5/2012 (well off the peak of $190 in 2007,) the stock has dropped to the mid-$30s which is about where it was in its first year of Lampert leadership (2004.)

Without a doubt, Mr. Lampert has overtaken the reigns as the worst CEO of a large, publicly traded corporation in America (now that Steve Ballmer has resigned – see next item.)

#1 Steve Ballmer at Microsoft

In 2013 Steve Ballmer resigned as CEO of Microsoft. After being replaced, within a year he resigned as a Board member. Both events triggered analyst enthusiasm, and the stock rose.

However, Mr. Ballmer left Microsoft in far worse condition after his decade of leadership. Microsoft missed the market shift to mobile, over-investing in Windows 8 to shore up PC sales and buying Nokia at a premium to try and catch the market. Unfortunately Windows 8 has not been a success, especially in mobile where it has less than 5% share. Surface tablets were written down, and now console sales are declining as gamers go mobile.

As a result the new CEO has been forced to make layoffs in all divisions – most substantially in the mobile handset (formerly Nokia) business – since I positioned Mr. Ballmer as America’s worst CEO in 2012. Job growth appears highly unlikely at Microsoft.

“CEOs – From Makers to Takers”

Forbes colleague Steve Denning has written an excellent column on the transformation of CEOs from those who make businesses, to those who take from businesses. Far too many CEOs focus on personal net worth building, making enormous compensation regardless of company performance. Money is spent on inflated pay, stock buybacks and managing short-term earnings to maximize bonuses. Too often immediate cost savings, such as from outsourcing, drive bad long-term decisions.

CEOs are the ones who determine how our collective national resources are invested. The private economy, which they control, is vastly larger than any spending by the government. Harvard professor William Lazonick details how between 2003 and 2012 CEOs gave back 54% of all earnings in share buybacks (to drive up stock prices short term) and handed out another 37% in dividends. Investors may have gained, but it’s hard to create jobs (and for a nation to prosper) when only 9% of all earnings for a decade go into building new businesses!

There are great CEOs out there. Steve Jobs and his replacement Tim Cook increased revenues and employment dramatically at Apple. Jeff Bezos made Amazon into an enviable growth machine, producing revenues and jobs. These leaders are focused on doing what it takes to grow their companies, and as a result the jobs in America.

It’s just too bad the 5 fellows profiled above have done more to destroy value than create it.

by Adam Hartung | Jul 28, 2014 | Current Affairs, Defend & Extend, In the Whirlpool, Web/Tech

Over the last couple of weeks big announcements from Apple, IBM and Microsoft have set the stage for what is likely to be Microsoft’s last stand to maintain any sense of personal technology leadership.

Custer Tries Holding Off An Unstoppable Native American Force

To many consumers the IBM and Apple partnership probably sounded semi-interesting. An app for airplane fuel management by commercial pilots is not something most people want. But what this announcement really amounted to was a full assault on regaining dominance in the channel of Value Added Resellers (VARs) and Value Added Dealers (VADs) that still sell computer “solutions” to thousands of businesses. Which is the last remaining historical Microsoft stronghold.

Think about all those businesses that use personal technology tools for things like retail point of purchase, inventory control, loan analysis in small banks, restaurant management, customer data collection, fluid control tracking, hotel check-in, truck routing and management, sales force management, production line control, project management — there is a never-ending list of business-to-business applications which drive the purchase of literally millions of devices and applications. Used by companies as small as a mom-and-pop store to as large as WalMart and JPMorganChase. And these solutions are bundled, sold, delivered and serviced by what is collectively called “the channel” for personal technology.

This “channel” emerged after Apple introduced the Apple II running VisiCalc, and businesses wanted hundreds of these machines. Later, bundling educational software with the Apple II created a near-monopoly for Apple channel partners who bundled solutions for school systems.

But, as the PC emerged this channel shifted. IBM pioneered the Microsoft-based PC, but IBM had long used a direct sales force. So its foray into personal computing did a very poor job of building a powerful sales channel. Even though the IBM PC was Time magazine’s “Man of the Year” in 1982, IBM lost its premier position largely because Microsoft took advantage of the channel opportunity to move well beyond IBM as a supplier.

Microsoft focused on building a very large network of developers creating an enormous variety of business-to-business applications on the Windows+Intel (Wintel) platform. Microsoft created training programs for developers to use its operating system and tools, while simultaneously cultivating manufacturers (such as Dell and Compaq) to build low cost machines to run the software. “Solution selling” was where VARs bundled what small businesses – and even many large businesses – needed by bringing together developer applications with manufacturer hardware.

It only took a few years for Microsoft to overtake Apple and IBM by dominating and growing the VAR channel. Apple did a poor job of creating a powerful developer network, preferring to develop everything users should want itself, so quickly it lacked a sufficient application base. IBM constantly tried to maintain its direct sales model (and upsell clients from PCs to more expensive hardware) rather than support the channel for developing applications or selling solutions based on PCs.

But, over the last several years Microsoft played “bet the company” on its launch of Windows 8. As mobile grew in hardware sales exponentially, and PC sales flattened (then declined,) Microsoft was tepid regarding any mobile offering. Under former CEO Steve Ballmer, Microsoft preferred creating an “all-in-one” solution via Win8 that it hoped would keep PC sales moving forward while slowly allowing its legions of Microsoft developers to build Win8 apps for mobile Surface devices — and what it further hoped would be other manufacturer’s tablets and phones running Win8.

This flopped. Horribly. Apple already had the “installed base” of users and mobile developers, working diligently to create new apps which could be released via its iTunes distribution platform. As a competitive offering, Google had several years previously launched the Android operating system, and companies such as HTC and Samsung had already begun building devices. Developers who wanted to move beyond Apple were already committed to Android. Microsoft was simply far too late to market with a Win8 product which gave developers and manufacturers little reason to invest.

Now Microsoft is in a very weak position. Despite much fanfare at launch, Microsoft was forced to take a nearly $1B write-off on its unsellable Surface devices. In an effort to gain a position in mobile, Microsoft previously bought phone maker Nokia, but it was simply far too late and without a good plan for how to change the Apple juggernaut.

Apple is now the dominant player in mobile, with the most users, developers and the most apps. Apple has upended the former Microsoft channel leadership position, as solution sellers are now offering Apple solutions to their mobile-hungry business customers. The merger with IBM brings even greater skill, and huge resources, to augmenting the base of business apps running on iOS and its devices (presently and in the future.) It provides encouragement to the VARs that a future stream of great products will be coming for them to sell to small, medium and even large businesses.

Caught in a situation of diminishing resources, after betting the company’s future on Windows 8 development and launch, and then seeing PC sales falter, Microsoft has now been forced to announce it is laying off 18,000 employees. Representing 14% of total staff, this is Microsoft’s largest reduction ever. Costs for the downsizing will be a massive loss of $1.1-$1.6B – just one year (almost to the day) after the huge Surface write-off.

Recognizing its extraordinarily weak market position, and that it’s acquisition of Nokia did little to build strength with developers while putting it at odds with manufacturers of other mobile devices, the company is taking some 12,000 jobs out of its Nokia division – ostensibly the acquisition made at a cost of $7.2B to blunt iPhone sales. Every other division is also suffering headcount reductions as Microsoft is forced to “circle the wagons” in an effort to find some way to “hold its ground” with historical business customers.

Today Apple is very strong in the developer community, already has a distribution capability with iTunes to which it is adding mobile payments, and is building a strong channel of VARs seeking mobile solutions. The IBM partnership strengthens this position, adds to Apple’s iOS developers, guarantees a string of new solutions for business customers and positions iOS as the platform of choice for VARs and VADs who will use iBeacon and other devices to help businesses become more capable by utilizing mobile/cloud technology.

Meanwhile, Microsoft is looking like the 7th Cavalry at the Little Bighorn. Microsoft is surrounded by competitors augmenting iOS and Android (and serious cloud service suppliers like Amazon,) resources are depleting as sales of “core” products stagnate and decline and write-offs mount, and watching as its “supply line” developer channel abandons Windows 8 for the competitive alternatives.

CEO Nadella keeps saying that that cloud solutions are Microsoft’s future, but how it will effectively compete at this late date is as unclear as the email announcement on layoffs Nokia’s head Stephen Elop sent to employees. Keeping its channel, long the source of market success for Microsoft, from leaving is Microsoft’s last stand. Unfortunately, Nadella’s challenge puts him in a position that looks a lot like General Custer.

by Adam Hartung | Sep 4, 2013 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Lock-in, Web/Tech

Just over a week after Microsoft announces plans to replace CEO Steve Ballmer the company announced it will spend $7.2B to buy the Nokia phone/tablet business. For those looking forward to big changes at Microsoft this was like sticking a pin in the big party balloon!

Everyone knows that Microsoft's future is at risk now that PC sales are declining globally at nearly 10% – with developing markets shifting even faster to mobile devices than the USA. And Microsoft has been the perpetual loser in mobile devices; late to market and with a product that is not a game changer and has only 3% share in the USA.

But, despite this grim reality, Microsoft has doubled-down (that's doubled its bet for non-gamblers) on its Windows 8 OS strategy, and continues to play "bet the company". Nokia's global market share has shriveled to 15% (from 40%) since former Microsoft exec-turned-Nokia-CEO Stephen Elop committed the company to Windows 8. Because other Microsoft ecosystem companies like HP, Acer and HP have been slow to bring out Win 8 devices, Nokia has 90% of the miniscule market that is Win 8 phones. So this acquisition brings in-house a much deeper commitment to spending on an effort to defend & extend Microsoft's declining O/S products.

As I predicted in January, the #1 action we could expect from a Ballmer-led Microsoft is pouring more resources into fighting market leaders iOS and Android – an unwinnable war. Previously there was the $8.5B Skype and the $400M Nook, and now a $7.2B Nokia. And as 32,000 Nokia employees join Microsoft losses will surely continue to rise. While Microsoft has a lot of cash – spending it at this rate, it won't last long!

Some folks think this acquisition will make Microsoft more like Apple, because it now will have both hardware and software which in some ways is like Apple's iPhone. The hope is for Apple-like sales and margins soon. But, unfortunately, Google bought Motorola months ago and we've seen that such revenue and profit growth are much harder to achieve than simply making an acquisition. And Android products are much more popular than Win8. Simply combining Microsoft and Nokia does not change the fact that Win8 products are very late to market, and not very desirable.

Some have postulated that buying Nokia was a way to solve the Microsoft CEO succession question, positioning Mr. Elop for Mr. Ballmer's job. While that outcome does seem likely, it would be one of the most expensive recruiting efforts of all time. The only reason for Mr. Elop to be made Microsoft CEO is his historical company relationship, not performance. And that makes Mr. Elop is exactly the wrong person for the Microsoft CEO job!

In October, 2010 when Mr. Elop took over Nokia I pointed out that he was the wrong person for that job – and he would destroy Nokia by making it a "Microsoft shop" with a Microsoft strategy. Since then sales are down, profits have evaporated, shareholders are in revolt and the only good news has been selling the dying company to Microsoft! That's not exactly the best CEO legacy.

Mr. Elop's job today is to sell more Win8 mobile devices. Were he to be made Microsoft CEO it is likely he would continue to think that is his primary job – just as Mr. Ballmer has believed. Neither CEO has shown any ability to realize that the market has already shifted, that there are two leaders far, far in front with brand image, products, apps, developers, partners, distribution, market share, sales and profits. And it is impossible for Microsoft to now catch up.

It is for good reason that short-term traders pushed down Microsoft's share value after the acquisition was announced. It is clear that current CEO Ballmer and Microsoft's Board are still stuck fighting the last war. Still trying to resurrect the Windows and Office businesses to previous glory. Many market anallysts see this as the last great effort to make Ballmer's bet-the-company on Windows 8 pay off. But that's a bet which every month is showing longer and longer odds.

Microsoft is not dead. And Microsoft is not without the ability to turn around. But it won't happen unless the Board recognizes it needs to steer Microsoft in a vastly different direction, reduce (rather than increase) investments in Win8 (and its devices,) and create a vision for 2020 where Microsoft is highly relevant to customers. So far, we're seeing all the wrong moves.

by Adam Hartung | Nov 29, 2012 | Defend & Extend, In the Swamp, In the Whirlpool, Leadership, Web/Tech

The web lit up yesterday when people started sharing a Fortune quote from Marissa Mayer, CEO of Yahoo, "We are literally moving the company from BlackBerrys to smartphones." Why was this a big deal? Because, in just a few words, Ms. Mayer pointed out that Research In Motion is no longer relevant. The company may have created the smartphone market, but now its products are so irrelevant that it isn't even considered a market participant.

Ouch. But, more importantly, this drove home that no matter how good RIM thinks Blackberry 10 may be, nobody cares. And when nobody cares, nobody buys. And if you weren't convinced RIM was headed for lousy returns and bankruptcy before, you certainly should be now.

But wait, this is certainly a good bit of the pot being derogatory toward the kettle. Because, other than the highly personalized news about Yahoo's new CEO, very few people care about Yahoo these days as well. After being thoroughly trounced in ad placement and search by Google, it is wholly unclear how Yahoo will create its own relevancy. It may likely be soon when a major advertiser says "When placing our major internet ad program we are focused on the split between Google and Facebook," demonstrating that nobody really cares about Yahoo anymore, either.

And how long will Yahoo survive?

The slip into irrelevancy is the inflection point into failure. Very few companies ever return. Once you are no longer relevant, customer quickly stop paying attention to practically anything you do. Even if you were once great, it doesn't take long before the slide into no-growth, cost cutting and lousy financial performance happens.

Consider:

- Garmin once led the market for navigation devices. Now practically everyone uses their mobile phone for navigation. The big story is Apple's blunder with maps, while Google dominates the marketplace. You probably even forgot Garmin exists.

- Radio Shack once was a consumer electronics powerhouse. They ran superbowl ads, and had major actresses parlaying with professional sports celebrities in major network ads. When was the last time you even thought about Radio Shack, much less visited a store?

- Sears was once America's premier, #1 retailer. The place where everyone shopped for brands like Craftsman, DieHard and Kenmore. But when did you last go into a Sears? Or even consider going into one? Do you even know where one is located?

- Kodak invented amateur photography. But when that market went digital nobody cared about film any more. Now Kodak is in bankruptcy. Do you care?

- Motorola Razr phones dominated the last wave of traditional cell phones. As sales plummeted they flirted with bankruptcy, until Motorola split into 2 pieces and the money losing phone business became Google – and nobody even noticed.

- When was the last time you thought about "building your body 12 ways" with Wonder bread? Right. Nobody else did either. Now Hostess is liquidating.

Being relevant is incredibly important, because markets shift quickly today. As they shift, either you are part of the trend going forward – or you are part of the "who cares" past. If you are the former, you are focused on new products that customers want to evaluate. If you are the latter, you can disappear a whole lot faster than anyone expected as customers simply ignore you.

So now take a look at a few other easy-to-spot companies losing relevancy:

- HP headlines are dominated by write offs of its investments in services and software, causing people to doubt the viability of its CEO, Meg Whitman. Who wants to buy products from a company that would spend billions on Palm, business services and Autonomy ERP software only to decide they overspent and can never make any money on those investments? Once a great market leader, HP is rapidly becoming a company nobody cares about; except for what appears to be a bloody train wreck in the making. In tech – lose customesr and you have a short half-life.

- Similarly Dell. A leader in supply chain management, what Dell product now excites you? As you think about the money you will spend this holiday, or in 2013, on tech products you're thinking about mobile devices — and where is Dell?

- Best Buy was the big winner when Circuit City went bankrupt. But Best Guy didn't change, and now margins have cratered as people showroom Amazon while in their store to negotiate prices. How long can Best Buy survive when all TVs are the same, and price is all that matters? And you download all your music and movies?

- Wal-Mart has built a huge on-line business. Did you know that? Do you care? Regardless of Wal-mart's on-line efforts, the company is known for cheap looking stores with cheap merchandise and customers that can't maintain credit cards. When you look at trends in retailing, is Wal-Mart ever the leader – in anything – anymore? If not, Wal-mart becomes a "default" store location when all you care about is price, and you can't wait for an on-line delivery. Unless you decide to go to the even cheaper Dollar General or Aldi.

And, the best for last, is Microsoft. Steve Ballmer announced that Microsoft phone sales quadrupled! Only, at 4 million units last quarter that is about 10% of Apple or Android. Truth is, despite 3 years of development, a huge amount of pre-release PR and ad spending, nobody much cares about Win8, Surface or new Microsoft-based mobile phones. People want an iPhone or Samsung product.

After its "lost decade" when Microsoft simply missed every major technology shift, people now don't really care about Microsoft. Yes, it has a few stores – but they dwarfed in number and customers by the Apple stores. Yes, the shifting tiles and touch screen PCs are new – but nobody real talks about them; other than to say they take a lot of new training. When it comes to "game changers" that are pushing trends, nobody is putting Microsoft in that category.

So the bad news about a $6 billion write-down of aQuantive adds to the sense of "the gang that can't shoot straight" after the string of failures like Zune, Vista and early Microsoft phones and tablets. Not to mention the lack of interest in Skype, while Internet Explorer falls to #2 in browser market share behind Chrome.

Chart Courtesy Jay Yarrow, BusinessInsider.com 5-21-12

Chart Courtesy Jay Yarrow, BusinessInsider.com 5-21-12

When a company is seen as never able to take the lead amidst changing

trends, investors see accquisitions like $1.2B for Yammer as a likely future write down. Customers lose interest and simply spend money elsewhere.

As investors we often hear about companies that were once great brands, but selling at low multiples, and therefore "value plays." But the truth is these are death traps that wipe out returns. Why? These companies have lost relevancy, and that puts them one short step from failure.

As company managers, where are you investing? Are you struggling to be relevant as other competitors – maybe "fringe" companies that use "voodoo solutions" you don't consider "enterprise ready" or understand – are obtaining a lot more interest and media excitment? You can work all you want to defend & extend your past glory, but as markets shift it is amazingly easy to lose relevancy. And it's a very, very tough job to play catch- up.

Just look at the money being spent trying at RIM, Microsoft, HP, Dell, Yahoo…………

–