by Adam Hartung | Mar 30, 2011 | Current Affairs, In the Swamp, Innovation, Leadership

Summary:

- Too many leaders spend too much effort minimizing uncertainty

- Stock buybacks reflect fear of uncertainty, but are a losing investment

- Good performing organizations invest in new markets, products and services

- Success comes from not only investing, but in learning quickly what works (or doesn’t) and rapidly adapting

“If you don’t ever do anything, you can never screw up” my boss said.

I was 20 years old working in the blazing Oklahoma July sun at a grain elevator. I had asked the maintenance lead to modify a tool, thinking I could work faster. Unfortunately, my idea failed and my production started lagging. Offload production was slowing. I had to ask that the tool be put back to original condition, and I apologized to the elevator manager for my mistake.

That’s when he used my opening line, and went on to say “Don’t ever quit trying to do better. You’re a clever kid. Sometimes ideas work, sometimes they don’t, but if we dont’ try them we’ll never know. That’s why I agreed to your idea originally. I’ll accept a few well-intentioned ‘mistakes’ as long as you learn from them. Now go back to work and try to make up that production before end of day.”

Far too few leaders today give, or follow, such advice. The Economist recently waxed eloquently about how much today’s leaders dislike any kind of uncertainty (see “From Tsunami’s to Typhoons“). Most very consciously make decisions intended to reduce uncertainty – regardless of the impact on results! Rather than take advantage of events and trends, doing something new and different, they intentionally downplay market changes and diligently seek ways to make it appear as if things are not changing – amidst massive change! The mere fact that there is uncertainty seems to be the most troubling issue, as leaders don’t want to deal with it, nor know how.

This fear of uncertainty manifest itself in decisions to buy back stock, rather than invest in new products, services and markets. 24/7 Wall Street reported $34B in announced share buybacks in early February (2011 Stock Buybacks on Fire), only to update that to $40B by end of the month. Literally dozens of companies choosing to spend money on buying their own shares, which creates no economic value at all, rather than invest in something that could create growth! And these aren’t just companies with limited prospects, but include what have been considered growth entities like Pfizer, Astra-Zeneca, Electronic Arts, MedcoHealth, Verizon, Semantec, Yum! Brands, Quest, Kohl’s, Varian and Gamestop to name just a few.

All of these companies have opportunities to grow – heck, all companies have the opportunity to grow. But there is inherent uncertainty in spending money on something that might not work out. So, instead, they are taking hard earned cash flow and spending it on buying back the company stock. The real certainty, from this investment, is that it limits growth — and eventually will lead to a smaller company that’s worth less. Don’t forget, the only investment Sara Lee made under Brenda Barnes the last 5 years was buying back stock – and now the company has shriveled up to less than half its former size while the equity value has disintegrated. Nobody wins from share buybacks – with the possible exception of senior executives who have compensation tied to stock price.

At the Harvard Business Review Umar Haque admonishes leaders today “Fail Bigger Cheaper: A Three Word Manifesto.” Silicon valley investors, deep into understanding our change to an information economy, are far less interested in “scale” and more interested in how leaders, and their companies, are learning faster – so they see where they might fail faster – and then being nimble enough to adjust based upon what they learned. And not just to do more of the same better, but in order to identify bigger targets – larger opportunities – than originally imagined. Often the “failure” can direct the business into grander opportunities which have even higher payoffs.

That’s why we don’t see companies like Google, Apple, Netflix, Virgin, or Cisco buying back their own stock. They see opportunities, and they invest. They don’t all work out. Remember Google Wave? Looked great – didn’t make it – but so what? Google learns from what works, and what doesn’t, and uses that information to help it develop newer, more powerful growth markets.

Long ago Apple let its lack of success with the Newton PDA cause it to retrench into strictly Mac development – which took the company to the brink of disaster by 2000. Since then, by investing in new markets and new products, Apple has grown revenues and profits like crazy, making it more valuable than arch-rival Microsoft and close to being the most valuable publicly traded company.

Source: Silicon Alley Insider of BusinessInsider.com

Virgin used its success in music retailing to enter the trans-atlantic airline business (Virgin Atlantic). Since then it has launched dozens of businesses. Some didn’t work out – like Virgin Bridal – but many more have, such as Virgin Money, Virgin Mobil, Virgin Connect – to name just a handful of the many Virgin businesses that contribute to company growth and value creation.

Nobody wants to screw up. But, unless you do nothing, it is inevitable. No leader, or company, can create high value if they don’t overcome their fear of uncertainty and invest in innovation. But, hand-in-glove with such investing is the requirement to learn fast whether an innovation is working, or not. And to adapt. Some things need time for the market to develop, others need technology advances, and others need a change in direction toward different customers. It’s the ability to invest in uncertain situations, then pay attention to market feedback in order to recognize how well the idea is working, and constantly adapt to market learning that sets apart those companies creating wealth today.

Update 4/1/2011 – AOLSmallBusiness.com reminds us of another great adaptation story, based upon entering an unknown market and learning, in “Yes, Even Apple Screws Up Sometimes.” When personal computers were all text-based machines Apple introduced the Lisa as the first commercial computer to utilize on-screen icons, and a mouse for navigation, as well as other key productivity enhancers like the trash can. But the Lisa failed. Apple studied the market, kept what was desirable and modified what wasn’t, re-introducing the product as the Macintosh in 1984. The Mac was a huge success, creating enormous value for Apple which was undeterred by both the uncertainty of the fledgling PC market and its initial failure at various changes in the user interface.

by Adam Hartung | Feb 9, 2011 | Current Affairs, Defend & Extend, In the Swamp, In the Whirlpool, Leadership, Lock-in, Weblogs

Summary:

- Start-ups that flourish give themselves permission to do whatever is necessary to succeed

- Most acquisitions kill that kind of permssion, forcing the acquired company to adopt the acquirers legacy

- AOL’s legacy business has been dying for several years

- AOL’s history of acquisitions has been horrible, because it doesn’t learn from the acquisitions.

- AOL’s acquisition, and announced integration, of Huffington Post will likely do nothing to turn around AOL, and probably leave HuffPo about as well off as AOL’s acquisition of Bebo

After the Super Bowl Sunday Night AOL announced it’s acquisition of The Huffington Post for $350M. Given that you can’t give away a newspaper company these days, the acquisition shows there is still value in “news” if you understand the right way to deliver it. HuffPo’s team of bloggers has shown that it’s possible to build a profitable news organization today – if you do it right. Something the folks at Tribune Corporation still don’t understand.

BusinessInsider.com headlined “AOL’s Huffington Post Acquisition Makes Sense for Both Sides.” For Arianna Huffington and her investors the big cash payout shows a clear win. They are receiving a pretty penny for their start-up. Beyond them, it’s less clear. AOL’s been losing subscribers, and site vistors for years. They’ve made a number of acquisitions to spark up interest including blogs Engadget, Joystiq, ad network Tacoda and social networking site Bebo. None of those have flourished – in fact the opposite has happened. AOL investors lost almost all the $850M spent on Bebo as Facebook crushed it. So far, the AOL track record has been horrible!

AOL clearly hopes HuffPo will bring it new visitors – but whether that works, and whether HuffPo continues growing, is now an open question. MediaPost.com reports “AOL Starts Mapping Plans for Huffington Post.” Unfortunately, it sounds much more as if AOL is trying to integrate HuffPo into its traditional organization – which will most likely do for HuffPo what integrating at News Corp did for MySpace – namely, layering it with “professional management,” additional systems, more overhead and rules for operating. Or, in other words, bury it in company legacy that strangles its abilitiy to innovate and shift with rapidly emerging market needs. The company that’s actually growing, winning in the marketplace, isn’t AOL. It’s HuffPo. If there’s any “integrating” needed it should be figuring out how to push AOL into HuffPo – not vice-versa.

As the New York Times headlined, this acquisition is “AOL’s Bet on Another Makeover.” And that’s what’s wrong. The acquisitions AOL made were pre-purchase successful because they were White Space endeavors that had close connection to the market. The founders gave their organization permission to do whatever it took to be successful, without artificial constraints based upon legacy. Their acquisitions have not used by AOL to create White Space with better market receptors – to teach AOL where growth lies. Rather, AOL has hoped they can use the acquisition to defend and extend their old success formula. AOL has hoped the acquisitions would allow them to slow the market shift, and preserve legacy operations.

As we’ve seen, that simply does not work. Markets shift for good reason, and the only way a business can thrive is to shift with them. At AOL the smart move would be to let Arianna run the show! A few months ago AOL purchased TechCrunch and ever since Michael Arrington, the founder, has been villifying AOL management for its bureaucracy and inability to adapt. What Mr. Armstrong, the relatively new CEO at AOL misses is that AOL’s business is dead. AOL needs to find an entirely new way of operating – and that’s what these acquisitions bring. AOL needs to get out of the way, let the acquisitions flourish, and learn something from them. AOL management needs to accept that the old AOL business model is rubbish, and what it must do is allow the acquisitions to operate in White Space, then learn from them! But that’s not been the history of AOL’s purchases, and doesn’t look like the case this time.

Mr. Armstrong could learn a lot from Sir Richard Branson. Virgin has made many acquisitions, and developed several new companies. He doesn’t try to integrate them, or drive them toward any particular business model From Virgin Airways to Virgin Money to Virgin Health Bank to Virgin Games (and all the other businesses) the requirement is that the business be tightly linked to market needs, operate in new ways and find out how to grow profitably. Virgin moves toward the new markets and businesses, it doesn’t expect the businesses to conform to the Virgin model.

I’d like to think AOL could learn from HuffPo and dramatically change. But from the announcements this week, it doesn’t look likely. AOL still looks like a management team desperately trying to save its old business, but without a clue how to do so. Too bad for AOL. Could be even worse for those who read HuffPo.

by Adam Hartung | Jan 5, 2011 | Defend & Extend, In the Rapids, In the Swamp, Leadership, Lock-in, Openness

Summary:

- Business planning systems are designed to defend historical markets

- Rapidly shifting markets makes it impossible to grow by defense alone

- Growth requires understanding what customers want, and creating new solutions that most likely aren’t part of the current business

- You can’t grow if you don’t plan to grow, but to plan for growth you have to shift resources from traditional planning into scenario planning

- High growth companies like Virgin, Apple and Google plan to fulfill future needs, not defend & extend past practicess

Imagine you see a pile of hay. Above it is a sign flashing “find the needle.” That achievement would be hard. Change the sign to “find the hay” and suddenly achieving the goal becomes much easier. So, as the comedian Bill Engvall might ask, what’s your sign? Unfortunately, most businesses plan for 2011, and beyond, using the first sign. Very few do planning using the latter. Most businesses won’t grow, because they simply don’t know how to plan for growth!!

Most businesses start planning with “I’m in the horseshoe (for example) business. My market isn’t growing, and there is more capacity than demand. How can I grow?” For these people, their sign is “find the needle.”

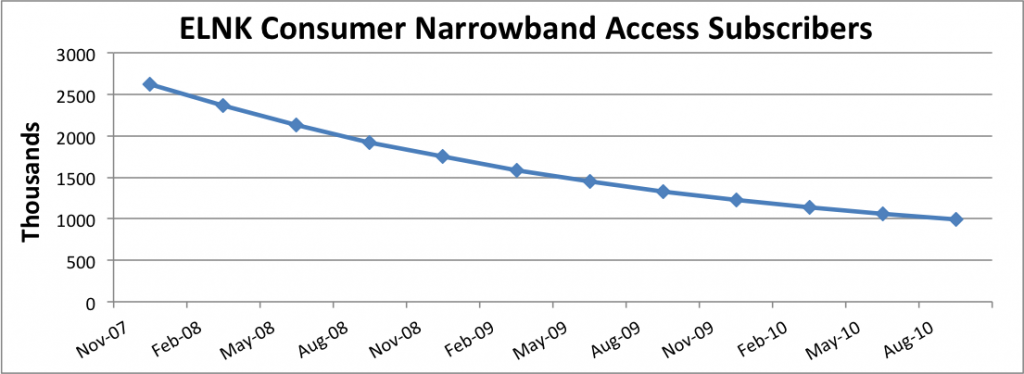

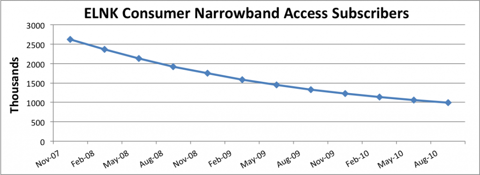

Take for example Earthlink. The company’s growth looked like a rocket ship in the early internet days as people by the millions signed up for dial-up service. But along came broadband, and the market for dial up died – never to return. Earthlink has no hope of growing as long as it thinks of itself as a dial-up company

Chart at SeekingAlpha.com author Ananthan Thangavel

Despite the absolute certainty that the market is shrinking, at this point almost all business planners will develop plans to defend this dying business as long as possible. Despite the impossibility of achieving good returns, there will be a plethora of actions to try and keep serving all the way to the very last customer. Just look at how AOL has invested millions trying to defend its dying internet access busiuness. Reality is, the company that walks away – gives up- is the smartest. There’s no way to make money as oversupply keeps too many companies spending too much to service too few customers.

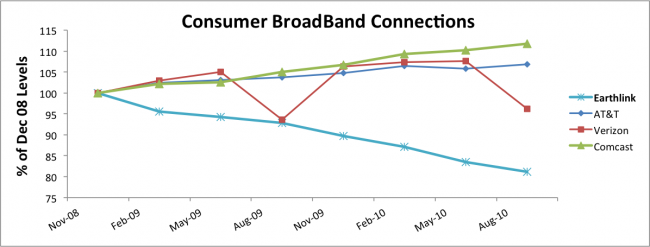

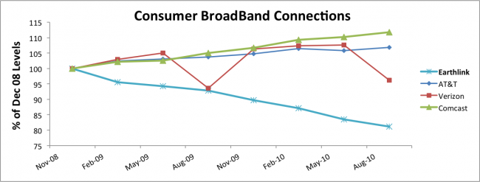

The next step for most planners is to attempt extending the business into something adjacent. For example, Earthlink would say “let’s invest in Broadband. We’ll hang onto customers as they want to switch, and maybe pick up a few customers.” But this completely ignores the fact that competitors already have a substantial lead. Competitors have learned the technology, and the marketplace. They are growing, and have no intention of giving up any room to a new competitor.

Chart at SeekingAlpha.com author Ananthan Thangavel

Planning systems are designed to keep the business doing more of what it always did, or possibly extending the business into adjacent markets after returns have faltered. Planning systems have no way of recognizing when a business, or market, has become obsolete. And practically never do they recognize the power of exsting competitors when looking at adjacent markets. As a result, the planning system produces no growth plans, leading 2011 to end with the self-fulfilling prophecy that the plan predicted – little or no growth.

The future for Earthlink is pretty grim. As it is for most companies that plan based upon history, trying to Defend & Extend their historical markets. In the highly dynamic, global marketplaces of 2011 trying to find growth by remaining focused on the past is like looking for the needle in a haystack. Maybe there’s something in there – but it’s not likely – and it’s even a lot less likely you’ll find it – and if you did, the cost of finding it will almost assuredly be greater than the value.

Alternatively, why not use planning resources to find, and develop, growth markets. Instead of looking at what you did (as in the past tense) try to figure out what you should do. Rather than studying past products, customers and markets, why not develop scenarios about the future that give you insight to what people will want to buy in 2011, 2012 and beyond? Rather than looking for needles, why not go explore the hay?

Newspapers kept focusing on declining subscriptions, when they should have been studying Craig’s List, eBay, Vehix.com and other on-line environments to learn the future of advertising. Had Tribune company poured its resources into its early internet investments, such as cars.com and careerbuilder.com, rather than trying to defend its traditional newspapers, it may well have avoided bankruptcy. But rather than looking to the future when doing its planning, and understanding that on-line news was going to explode, Tribune kept looking for the needle (cost cuts, layoffs, outsourcing, etc.) to save the old success formula.

Direct mail companies and Sunday insert printers have continued looking for ways to defend & extend their coupon printing business – despite the fact that nobody reads junk mail or uses printed coupons. Several have failed, and larger companies have merged trying to find “synergies” and more cost cuts. Simultaneously a 28 year old music major from Nothwestern university starts figuring out how to help companies acquire new customers by offering email coupons, and within 2 years his company, Groupon, is valued at around $6B. There’s nothing that stopped coupon powerhouse Advo from being Groupon, except that its planning system was devoted to finding the needle, while Groupon’s leaders decided to go play in the hay.

Hallmark and American Greetings want us to buy birthday and holiday cards for various occasions – in a world where almost nobody mails cards any longer. As they keep trying to defend their old business, and extend it into a few new opportunities for on-line cards, Twitter captures the wave of instant communications by offering everyone 140 character ways to communicate. Because Twitter is out where the growth is, the company raises $200M giving it a value of $3.7B.

Nothing stops any business from being anything it wants to be. But as most enter 2011 they will use their planning resources, including all those management meetings and hours of forms completion, to do nothing more than re-examine the historical business. Most will devolve into trying to figure out how to do more with less. As future forecasts look grim, or perhaps cautiously optimistic (based on a lot of things going right – like a mysterious pick-up in demand) there will be much nashing of teeth – and meetings looking for a needle that can be offered to employees and investors as a hope for rising future value.

Smart companies get out of that rut. They focus their planning on the future. What do customers want, and how can we give them what they want? How can we create whole new markets. Apple was a PC company, but by exploring mobility it became a provider of MP3 consumer electronics, downloadable music, a mobile device and app supplier and the early winner in cloud accessing tablets. Google has moved from a search engine to a powerhouse ad placement company and is pushing the edges of growth in mobile computing as well as several other markets. Virgin started as a distributor of long-playing vinyl record albums, but by exploring what customers really wanted it has become an international airline, cell phone company, international lender and space travel pioneer (to mention just a few of its businesses.)

You can grow in 2011, but to do so you need to shed the old planning system (and its resource wasting processes) and get serious about scenario planning. Focus on the future, not the past.

by Adam Hartung | Sep 23, 2010 | Current Affairs, In the Rapids, Leadership, Openness, Travel

Summary:

- Most people misunderstand the way toward building a valuable company

- Richard Branson has developed massive wealth by finding and entering growth markets

- Success comes from developing new solutions that fulfill unmet needs – not maximizing performance of core capabilities

- Virgin is now moving into luxury hotels, a market being ignored by most investors, with new products that fit still unmet needs

Very few people are as wealthy as Richard Branson. But few people can manage like he does.

Branson started out selling records via mail-order in Britain. Over the years he got into retailing, international airlines, domestic airlines, mobile telephony, international lending (amongst other businesses) – and now his company is investing $500milion in hotels and hotel management. According to Bloomberg.com “Branson’s Virgin Group to Invest $500million in Hotels.”

Despite all we hear about how impossible it is to be an entrepreneur in Europe, Sir Branson has done quite well, building a wildly successful, profitable company. Although he didn’t follow conventional wisdom. Instead of “sticking to his core” Sir Branson has built a company that invests in opportunities which are highly profitable – regardless of the industry or market. He doesn’t grow by doing more of the same better, faster or cheaper. Instead, he takes advantage of shifting markets – getting into businesses with opportunities and exiting those that don’t earn high rates of return.

During last decade’s building boom there were a lot of high-end hotels built. Now, with the economy not growing, excess capacity has made it difficult for these to cover the mortgage. Bankers don’t want to refinance – they want out of the buildings. Occupancy has been so low that many traditional name brands, such as Ritz Carlton or Intercontinental, have been forced to abandon properties. As a result, several hotels have closed, and the property offered for sale at a fraction of original construction cost. With most investors shying away from all things real estate, prices have plummeted. Some hotels, nearly new, have sold for the value of underlying land.

And now Virgin enters the market. Although Virgin has no background in real estate or hotel management, it is clear that there is demand for luxury goods and luxury travel — if someone can make it attractive and affordable. By purchasing premier properties at a fraction (literally 10-25% of their initial cost) Virgin will be able to offer hotel guests a superior experience at an attractive price! Management sees an unmet need by high-income, well educated “creative class” customers. By getting into the market Virgin will learn, just as it did in airlines, how to meet customer expectations in a way that allows for highly profitable delivery when meeting a currently unmet need.

While some would say that if the current competitors, steeped in experience and tradition, can’t succeed Virgin should not think it can. But a Virgin executive rightly says “If you look at Virgin’s history, we have come into markets with big powerful players, where customers are generally satisfied but not in love, and we have been able to cut through that.” Well said. Virgin doesn’t do what competitors do – it develops a solution that locks competitors into their position while positioning Virgin to meet the untapped market.

Even though this opportunity is available to everyone, almost no companies are interested in buying these undervalued hotels. “It’s not our business.” “We don’t know how to operate hotels.” “We don’t invest in real estate.” “I’m too busy taking care of my current business to consider something new.” “What if we’re wrong?” These are all things people say to stop themselves from taking action to enter new opportunities with high rates of return. The magic of Virgin is its willingness to overcome Lock-in to its existing business, look for market opportunities, and then (as Nike advertises) Do It!

by Adam Hartung | Sep 19, 2010 | In the Rapids, Leadership, Openness

Summary:

- Richard Branson has built a wildly successful Virgin company on very unconventional “secrets to success”

- Most business leaders follow management theory than is built on myth

- Virgin has been wildly successful, even over the last decade when many companies have suffered, by being agile and market oriented

- It’s time to throw out traditional management, and its myths, for a different approach.

In my speaking and blogging I regularly comment on what great results have been achieved Virgin under Chairman/CEO Richard Branson. The founder, and the company, both started quite humbly. Even though nobody can easily define exactly what business Virgin is in, it has done very well. So I was pleased to read at BNet.com “Richard Branson: Five Secrets to Business Success“:

- Enjoy what you are doing. Really.

- Create something that stands out

- Create something of which you and your employees are proud

- Be a good leader – which he defines as listen a lot, ask questions, heap the praise. Don’t fire people, help them to be happy

- Be visible. Get out into the market and listen, listen, listen.

I am struck at how this is nothing like the recommendations in most management books. Let’s see what Richard Branson didn’t say:

- Sacrifice. Work hard. Be diligent. Be tough. Cut out anything unnecessary

- Find one thing to be good at and excel – search for excellence

- Know your core competency, and maximize it’s use. Avoid things that aren’t “core”

- Make sure everyone is “on the bus” doing the one thing you want to do. Get rid of anyone else

- EXECUTE! Optimize your business model. Focus on execution

- Cut costs. Run a tight ship. Tighten your belt.

- Focus on results. Run the business by the numbers

- Focus on quality – implement Six Sigma and/or TQM and/or LEAN processes

- Outsource anything you don’t absolutely have to do

- Hire the “right” leaders (or employees)

Business if full of myth. And we now know that many gurus have been recommending actions for years that simply haven’t produce long-term positive results. The companies considered “great” by Jim Collins have fared far more poorly than average. Most of the companies Tom Peters considered “excellent” have not made it to 2010 in good shape – if they even survived! Most of the 10 myths were things that simply sounded good. They appeal to the American way of training. But they haven’t helped those companies which applied these ideas succeed.

Sir Richard Branson has created businesses from selling recordings to bridal shops, international banking, traditional airlines and even a business flying people into outer space. By all the traditional recommendations, he and his company should have failed. It followed none of the recommendations for hiring, firing, focus or execution. Yet he has created billions in personal fortune, billions for investors and given thousand of people very rewarding places to work. By all counts, he and Virgin have been a success.

It’s time to give up our management myths, and learn to compete in today’s rapidly shifting market. It’s now more about listening to the market and managing an agile organization than “focusing on core” or “execution.”