by Adam Hartung | Jul 27, 2016 | Food and Drink, Growth Stall, In the Swamp, Leadership, Web/Tech

Growth Stalls are deadly for valuation, and both Mcdonald’s and Apple are in one.

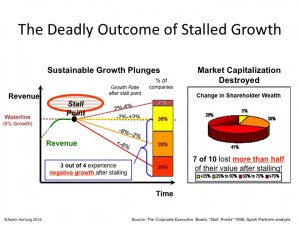

August, 2014 I wrote about McDonald’s Growth Stall. The company had 7 straight months of revenue declines, and leadership was predicting the trend would continue. Using data from several thousand companies across more than 3 decades, companies in a Growth Stall are unable to maintain a mere 2% growth rate 93% of the time. 55% fall into a consistent revenue decline of more than 2%. 20% drop into a negative 6%/year revenue slide. 69% of Growth Stalled companies will lose at least half their market capitalization in just a few years. 95% will lose more than 25% of their market value. So it is a long-term concern when any company hits a Growth Stall.

A new CEO was hired, and he implemented several changes. He implemented all-day breakfast, and multiple new promotions. He also closed 700 stores in 2015, and 500 in 2016. And he announced the company would move its headquarters from suburban Oakbrook to downtown Chicago, IL. While doing something, none of these actions addressed the fundamental problem of customers switching to competitive options that meet modern consumer food trends far better than McDonald’s.

A new CEO was hired, and he implemented several changes. He implemented all-day breakfast, and multiple new promotions. He also closed 700 stores in 2015, and 500 in 2016. And he announced the company would move its headquarters from suburban Oakbrook to downtown Chicago, IL. While doing something, none of these actions addressed the fundamental problem of customers switching to competitive options that meet modern consumer food trends far better than McDonald’s.

McDonald’s stock languished around $94/share from 8/2014 through 8/2015 – but then broke out to $112 in 2 months on investor hopes for a turnaround. At the time I warned investors not to follow the herd, because there was nothing to indicate that trends had changed – and McDonald’s still had not altered its business in any meaningful way to address the new market realities.

Yet, hopes remained high and the stock peaked at $130 in May, 2016. But since then, the lack of incremental revenue growth has become obvious again. Customers are switching from lunch food to breakfast food, and often switching to lower priced items – but these are almost wholly existing customers. Not new, incremental customers. Thus, the company trumpets small gains in revenue per store (recall, the number of stores were cut) but the growth is less than the predicted 2%. The only incremental growth is in China and Russia, 2 markets known for unpredictable leadership. The stock has now fallen back to $120.

Given that the realization is growing as to the McDonald’s inability to fundamentally change its business competitively, the prognosis is not good that a turnaround will really happen. Instead, the common pattern emerges of investors hoping that the Growth Stall was a “blip,” and will be easily reversed. They think the business is fundamentally sound, and a little management “tweaking” will fix everything. Small changes will lead to the classic hockey-stick forecast of higher future growth. So the stock pops up on short-term news, only to fall back when reality sets in that the long-term doesn’t look so good.

Unfortunately, Apple’s Q3 2016 results (reported yesterday) clearly show the company is now in its own Growth Stall. Revenues were down 11% vs. last year (YOY or year-over-year,) and EPS (earnings per share) were down 23% YOY. 2 consecutive quarters of either defines a Growth Stall, and Apple hit both. Further evidence of a Growth Stall exists in iPhone unit sales declining 15% YOY, iPad unit sales off 9% YOY, Mac unit sales down 11% YOY and “other products” revenue down 16% YOY.

This was not unanticipated. Apple started communicating growth concerns in January, causing its stock to tank. And in April, revealing Q2 results, the company not only verified its first down quarter, but predicted Q3 would be soft. From its peak in May, 2015 of $132 to its low in May, 2016 of $90, Apple’s valuation fell a whopping 32%! One could say it met the valuation prediction of a Growth Stall already – and incredibly quickly!

But now analysts are ready to say “the worst is behind it” for Apple investors. They are cheering results that beat expectations, even though they are clearly very poor compared to last year. Analysts are hoping that a new, lower baseline is being set for investors that only look backward 52 weeks, and the stock price will move up on additional company share repurchases, a successful iPhone 7 launch, higher sales in emerging countries like India, and more app revenue as the installed base grows – all leading to a higher P/E (price/earnings) multiple. The stock improved 7% on the latest news.

So far, Apple still has not addressed its big problem. What will be the next product or solution that will replace “core” iPhone and iPad revenues? Increasingly competitors are making smartphones far cheaper that are “good enough,” especially in markets like China. And iPhone/iPad product improvements are no longer as powerful as before, causing new product releases to be less exciting. And products like Apple Watch, Apple Pay, Apple TV and IBeacon are not “moving the needle” on revenues nearly enough. And while experienced companies like HBO, Netflix and Amazon grow their expanding content creation, Apple has said it is growing its original content offerings by buying the exclusive rights to “Carpool Karaoke“ – yet this is very small compared to the revenue growth needs created by slowing “core” products.

Like McDonald’s stock, Apple’s stock is likely to move upward short-term. Investor hopes are hard to kill. Long-term investors will hold their stock, waiting to see if something good emerges. Traders will buy, based upon beating analyst expectations or technical analysis of price movements. Or just belief that the P/E will expand closer to tech industry norms. But long-term, unless the fundamental need for new products that fulfill customer trends – as the iPad, iPhone and iPod did for mobile – it is unclear how Apple’s valuation grows.

by Adam Hartung | May 20, 2016 | E-Commerce, Investing, Retail, Trends

WalMart announced 1st quarter results on Thursday, and the stock jumped almost 10% on news sales were up versus last year. It was only $1.1B on $115B, about 1%, but it was UP! Same store sales were also up 1%, but analysts pointed out that was largely due to lower prices to hold competitors at bay.

While investors cheered the news, at the higher valuation WalMart is still only worth what it was in June, 2012 (just under $70/share.) From then through August, 2015 WalMart traded at a higher valuation – peaking at $90 in January, 2015. Subsequent fears of slower sales had driven the stock down to $56.50 by November, 2015. So this is a recovery for crestfallen investors the last year, but far from new valuation highs.

Unfortunately, this is likely to be just a blip up in a longer-term ongoing valuation decline for WalMart. And that value will be captured by those who understand the most important, undeniable trend in retail.

(c) AdamHartung.com Data Sources: Yahoo Finance and www.trend-stock-analysis-on.net

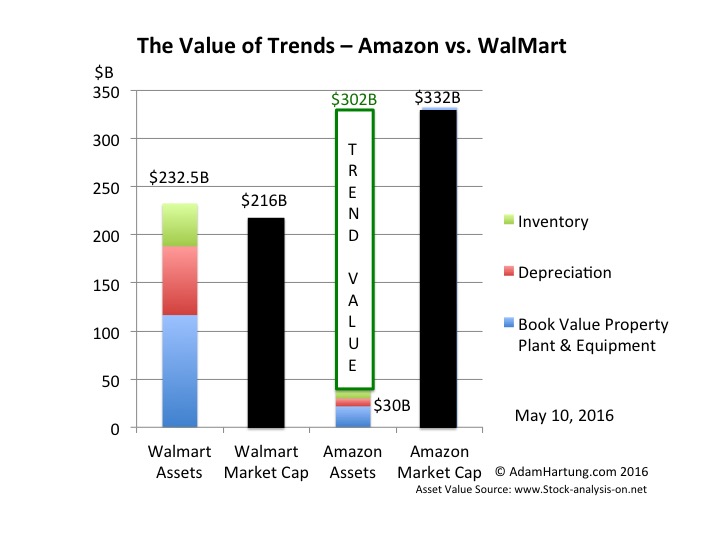

Although the numbers for WalMart’s valuation are a bit better than when the associated chart was completed last week, as you can see WalMart’s assets are greater than the company’s total valuation. This is because the return on its assets, today and projected, are so low that WalMart must borrow money in order to make them overall worthwhile. And the fact that on the balance sheet, at book value, the assets appear to be some $50B lower due to depreciation, and the difference be cost and market value.

This is because WalMart competes almost entirely in the intensely competitive and asset-dense market of traditional brick-and-mortar retail. This requires a lot of land, buildings, shelves and inventory. And that market is barely growing. Maybe 1-2%/year.

Compare t his with Amazon. Amazon has about $30B of assets. Yet its valuation is over $330B. So Amazon captures an extra value of $300B by competing in the asset sparse market of on-line retailing where it needs little land, few buildings, far less shelving and a lot less inventory. And it is competing in a market the Commerce Department says is growing at 15%/year.

The trend to on-line sales is extremely important, as it has entirely different customer acquisition and retention requirements, and very different ways of competing. Amazon understands those trends, and continues to lead its rivals. Today on-line retail is 10.5% of all non-restaurant, non-bar retail. And that 15% growth rate accounts for 60% of ALL the growth in this retail segment. Amazon keeps advancing, growing as fast (or faster) than the industry average, especially in key categories. Meanwhile, despite its vast resources and best efforts WalMart admitted its on-line sales growth is only 7% – half the segment growth rate – and its growth is decelerating.

By understanding this one trend – a very big, important, powerful trend – Amazon captures more value than the current value of ALL the Walmart stores, distribution centers and their contents. With all those assets WalMart can only convince investors it is worth about $200B. With about 13% of the assets used by WalMart, Amazon convinces investors it is worth 33% more than WalMart – over $330B. That’s $300B of value created just by knowing where the market is headed, and how to deliver for customers in that future market.

Yes, Amazon has other businesses, such as AWS cloud services and tech products in tablets, smartphones and smart speakers. But these too (some not nearly as successful as others, mind you) are very much on trends. WalMart once dominated retail technology with its massive computer systems and enormous databases. But WalMart limited itself to using its technology to defend & extend its core traditional retail business via store forecasts, optimized distribution and extensive pricing schemes. Amazon is monetizing its technology prowess by, again, leveraging trends and making its services and products available to others.

How does this apply to you? When someone asks “If you could have anything you want, what would you ask for?” most of us would start with health, happiness, peace and similar intangibles for us, our families and mankind. But if forced to make a tangible selection, we would ask for an asset. Buildings, equipment, cash. Yet, as WalMart and Amazon show us, those assets are only as valuable as what you do with them. And thus, it is more valuable to understand the trends, and how to use assets wisely for greatest value, than it is to own a pile of assets.

So the really important question is “Do you know what trends are going to be important to your business, and are you implementing a strategy to leverage those key trends?” If you are trying to protect your assets, you will likely be overwhelmed by the trend leader. But if you really understand the trends and are ready to act on them, you could be the one to capture the most value in your marketplace, and likely without adding a lot more costly assets.

by Adam Hartung | Mar 30, 2016 | In the Whirlpool, Leadership, Lifecycle, Web/Tech

Starboard Value last week sent a letter to Yahoo’s Board of Directors announcing its intention to ask shareholders to replace the entire Board. That is why Starboard is called an “activist” fund. It is not shy about seeking action at the Board level to change the direction of a company – by changing the CEO, seeking downsizings and reogranizations, changing dividend policy, seeking share buybacks, recommending asset sales, or changing other resource allocations. They are different than other large investors, such as pension funds or mutual funds, who purchase lots of a company’s equity but don’t seek to overtly change the direction, and management, of a company.

Activists have been around a long time. And for years, they were despised. Carl Icahn made himself famous by buying company shares, then pressuring management into decisions which damaged the company long-term while he made money fast. For example, he bought TWA shares then pushed the company to add huge additional debt and repurchase equity (including buying his position via something called “green mail”) in order to short-term push up the earnings per share. This made Icahn billions, but ended up killing the company.

Similarly, Mr. Icahn bought a big position in Motorola right after it successfully launched the RAZR phone. He pushed the board to shut down expensive R&D and product development to improve short-term earnings. Then borrow a lot of money to repurchase shares, improving earnings per share but making the company over-leveraged. He then sold out and split with his cash. But Motorola never launched another successful phone, the technology changed, and Motorola had to sell its cell phone business (that pioneered the industry) in order to pay off debt and avoid bankruptcy. Motorola is now a fragment of its former self, and no longer relevant in the tech marketplace.

So now you understand why many people hate activists. They are famous for

- cutting long-term investments on new products leaving future sales pipelines weakened,

- selling assets to increase cash while driving down margins as vendors take more,

- selling whole businesses to raise cash but leave the company smaller and less competitive,

- cutting headcount to improve short-term earnings but leaving management and employees decimated and overworked,

- increasing debt massively to repurchase shares, but leaving the company financially vulnerable to the slightest problem,

- doing pretty much anything to make the short-term look better with no concern for long-term viability.

Yet, they keep buying shares, and they have defenders among shareholders. Many big investors say that activists are the only way shareholders can do anything about lousy management teams that fail to deliver, and Boards of Directors that let management be lazy and ineffective.

Which takes us to Yahoo. Yahoo was an internet advertising pioneer. Yet, for several years Yahoo has been eclipsed by competitors from Google to Facebook and even Microsoft that have grown their user base and revenues as Yahoo has shrunk. In the 4 years since becoming CEO Marissa Mayer has watched Yahoo’s revenues stagnate or decline in all core sectors, while its costs have increased – thus deteriorating margins. And to prop up the stock price she sold Alibaba shares, the only asset at Yahoo increasing in value, and used the proceeds to purchase Yahoo shares. There are very, very few defenders of Ms. Mayer in the investment community, or in the company, and increasingly even the Board of Directors is at odds with her leadership.

Which takes us to Yahoo. Yahoo was an internet advertising pioneer. Yet, for several years Yahoo has been eclipsed by competitors from Google to Facebook and even Microsoft that have grown their user base and revenues as Yahoo has shrunk. In the 4 years since becoming CEO Marissa Mayer has watched Yahoo’s revenues stagnate or decline in all core sectors, while its costs have increased – thus deteriorating margins. And to prop up the stock price she sold Alibaba shares, the only asset at Yahoo increasing in value, and used the proceeds to purchase Yahoo shares. There are very, very few defenders of Ms. Mayer in the investment community, or in the company, and increasingly even the Board of Directors is at odds with her leadership.

The biggest event in digital marketing is the Digital Content NewFronts in New York City this time every year. Big digital platforms spend heavily to promote themselves and their content to big advertisers. But in the last year Yahoo closed several verticals, and discontinued original programming efforts taking a $42M charge. It also shut is online video hub, Screen. Smaller, and less competitive than ever, Yahoo this year has cut its spending and customer acquisition efforts at NewFronts, a decision sure to make it even harder to reverse its declining fortunes. Not pleasant news to investors.

And Yahoo keeps going down in value. Looking at the market the value of Yahoo and Alibaba, and the Alibaba shares held in Yahoo, the theoretical value of Yahoo’s core business is now zero. But that is an oversimplification. Potential buyers have valued the business at $6B, while management has said it is worth $10B. Only in 2008 Ballmer-led Microsoft made an offer to buy it for $45B! That’s value destruction to the amount of $35B-$39B!

Yet management and the Board remains removed from the impact of that value destruction. And the risk remains that Yahoo leadership will continue selling off Alibaba value to keep the other businesses alive, thus bleeding additional investor value out of the company. There are reports that CEO Mayer never took seriously the threat of an activist involving himself in changing the company, and removing her as CEO. Ensconced in the CEO’s office there was apparently little concern about shareholder value while she remained fixated on Quixotic efforts to compete with much better positioned, growing and more profitable competitors Google and Facebook. Losing customers, losing sales, and losing margin as her efforts proved reasonable fruitless amidst product line shutdowns, bad acquisitions, layoffs and questionable micro-management decisions like eliminating work from home policies.

There appear to be real buyers interested in Yahoo. There are those who think they can create value out of what is left. And they will give the Yahoo shareholders something for the opportunity to take over those business lines. Some want it as part of a bigger business, such as Verizon, and others see independent routes. Even Microsoft is reportedly interested in funding a purchase of Yahoo’s core. But there is no sign that management, or the Board, are moving quickly to redirect the company.

And that is why Starboard Value wants to change the Board of Directors. If they won’t make changes, then Starboard will make changes. And investors, long weary of existing leadership and its inability to take positive action, see Starboard’s activism as the best way to unlock what value remains in Yahoo for them. After years of mismanagement and underperformance what else should investors do?

Activists are easy to pick at, but they play a vital role in forcing management teams and Boards of Directors to face up to market challenges and internal weaknesses. In cases like Yahoo the activist investor is the last remaining player to try and save the company from weak leadership.

by Adam Hartung | Feb 24, 2014 | Current Affairs, Defend & Extend, In the Rapids, Leadership, Transparency, Web/Tech

Facebook is acquiring WhatsApp, a company with at most $300M revenues, and 55 employees, for $19billion. That’s billion – with a “b.” An astonishing figure that is second only to HP’s acquisition of market leader Compaq, which had substantial revenues and profits, as tech acquisitions. $19B is 13 times Facebook’s (not WhatsApp’s) entire 2013 net income – and almost 2.5 times Facebook’s (again, not WhatsApp’s) 2013 gross revenues!

On the mere face of it this valuation should make the most dispassionate analyst swoon. In today’s world very established, successful companies sell for far, far lower valuations. Apple is valued at about 13 times earnings. Microsoft about 14 times earnings. Google 33 times. These are small fractions of the nearly infinite P/E placed on WhatsApp.

But there is a leadership lesson offered here by CEO Zuckerberg’s team that is well worth learning.

Irrelevancy can happen remarkably quickly. True in any industry, but especially in digital technology. Examples: Research-in-Motion/Blackberry. Motorola. Dell. HP all lost relevancy in months and are struggling. (For those who want non-tech examples think of Circuit City, Best Buy, Sears, JCPenney, Abercrombie and Fitch.) Each of these companies was an industry leader that lust its luster, most of its customers, a big chunk of its employees and much of its market valuation in months when the company missed a market shift.

Although leadership knew what it had historically done to sell products profitably, in a very short time market trends reduced the value of the company’s historical success formula leaving investors, as well as management, wondering how it was going to compete.

Facebook is not immune to changing market trends. Although it has been the benchmark for social media, it only achieved that goal after annihilating early leader MySpace. And although Facebook was built by youthful folks, trends away from using laptops and toward mobile devices have challenged the Facebook platform. Simultaneously, changing communication requirements have altered the use, and impact, of things like images, photos, charts and text. All of these have the potential impact of slowly (or not so slowly) eroding the value (which is noticably lofty) of Facebook.

Most leaders address these kinds of challenges by launching new products to leverage the trend. And Facebook did just that. Facebook not only worked on making the platform more mobile friendly, but developed its own platform apps for photos and texting and all kinds of new features.

But, and this is critical, external companies did a better job. Two years ago Instagram emerged as a leader in image sharing. And WhatsApp has developed a superior answer for messaging.

Historically leadership usually said “we need to find a way to beat these new guys.” They would make it hard to integrate new solutions with their dominant platform in an effort to block growth. They would spend huge amounts on marketing and branding to try overcoming the emerging leader. Often they filed intellectual property litigation in an effort to cause short-term business interuption and threaten viability. They might even try hiring the emerging company’s tech leader away to stop development.

All of these actions were efforts to defend & extend the early leader’s market position. Even though the market is shifting, and trends are developing externally from the company, leadership will tend to look inside for an answer. It will often ignore the trend, disparage the competition, keep promising improvements to its historical products and services and blanket the media with PR as to its stated superiority.

But, as that list (above) of companies that lost relevancy demonstrates, this rarely works. In a highly interconnected, fast-paced, globally competitive marketplace customers go where they want. Quickly. Often leaving the early leader with a management team (and Board of Directors) scratching its head and wondering how it lost so much market position, and value, so quickly.

Hand it to Mr. Zuckerberg’s team. Instead of ignoring trends in its effort to defend & extend its early lead, they reached out and brought the leader to them. $1B for Instagram was a big investment, especially so close to launching an IPO. But, it kept Facebook relevant in mobile platforms and imaging.

And making a nosebleed-creating $19B deal for WhatsApp focuses on maintaining relevancy as well. WhatsApp already processes almost as many messages as the entire telecom industry. It has 450million users with 70% active daily, which is already 60% the size of Facebook’s daily user community (550million.) By bringing these people into the Facebook corporate family it assures the company of continued relevancy as the market shifts. It doesn’t matter if these are the same people, or different people. The issue is that it keeps Facebook relevant, rather than losing relevance to a competitor.

How will this all be monetized into $19B? The second brilliant leadership call by Facebook is to not answer that question.

Facebook didn’t know how to monetize its early leadership in users, but management knew it had to find a way. Now the company has grown from almost no revenues in 2008 to almost $8B in just 5 years. (Does your company have a plan to add $8B/year of organic revenue growth by 2019?)

So just as Facebook had to find its revenue model (which it is still exploring,) Zuckerberg’s team allows the leadership of Instagram and WhatsApp to remain independent, operating in their own White Space, to grow their user base and learn how to monetize what is an extraordinarily large group of happy folks. When looking to grow in new markets, and you find a team with the skills to understand the trends, it is independence rather than integration that makes the most sense organizationally.

Thirdly, back to that valuation issue. $19B is a huge amount of money. Unless you don’t really spend $19B. Facebook has the blessed ability to print its own. Private money that it can use for such acquisitions. As long as Facebook has a very high market valuation it can make acquisitions with shares, rather than real money.

In the case of both Instagram and WhatsApp the acquisition is being made in a mix of cash, Facebook stock and restricted Facebook stock for employees. The latter two of these three items are not real money. They are simply pieces of paper giving claims to ownership of Facebook, which itself is valued at 22 times 2013 revenue and 116 times 2013 earnings. The price of those shares are all based on expectations; expectations which now require the performance of Instagram and WhatsApp to make happen.

By making acquisitions with Facebook shares the leadership team is able to link the newly acquired managers to the same overall goals as Facebook, while offering an extremely high price but without actually having to raise any money – or spend all that money.

All companies risk of becoming irrelevant. New technologies, customer behavior patterns, regulations, inventions and innovations constantly challenge old success formulas. Most leaders fall into a pattern of trying to defend & extend their old business in the face of market shifts, hastening the fall into irrelevancy. Or they try to acquire a new business, then integrate it into the old business which strips away the new business value and leads, inevitably, to irrelevancy.

The leaders of Facebook are giving us a lesson in an alternative approach. (1) Recognize the market shift. Accept it. If there is a better solution, rush toward it rather than ignoring it. (2) Bring it into the company, and leave it independent. Eschew integration and efforts to find “synergy.” (You never know, in 3 years the company may need to be renamed WhatsApp to reflect a new market paradigm.) (3) And as long as you can convince investors that you are maintaining your relevancy use your highly valued stock as currency to keep the company moving forward.

These are 3 great lessons for all leadership teams. And I continue to think Facebook is the one stock to own in 2014.

by Adam Hartung | Dec 15, 2010 | Current Affairs, In the Swamp, Leadership, Openness, Television, Web/Tech

Summary:

- Business leaders are honored for creating profitable growth

- Those who create the greatest growth disrupt the status quo and change the way things are done – such as Zuckerberg and Jobs

- Too many CEOs act as caretakers, overlooking growth

- Caretakers watch value decline

- Under Welch, GE dramatically grew and he was Time’s Person of the Year

- Under Immelt, GE has contracted

- Too many CEOs are like Immelt. They need to either change, or be replaced

It’s that time of year when magazines like to honor folks for major accomplishments. This year, Time’s Person of the Year is Mark Zuckerberg, honored for leading Facebook and its dramatic change in social behavior amongst so many people. Marketwatch.com selected Steve Jobs as its CEO of the Decade – an honor several journals gave him last year!

There is of course a bias in these selections. Most journals highly favor CEOs that drive up their stock price! For example, Ed Zander was CEO of the year in 2004 for his “turnaround” at Motorola – and within 2 years he was fired and Motorola was facing possible bankruptcy. Obviously his “quick fix” (getting the RAZR out the door with a big marketing push) didn’t pan out so well over time. We’ll have to see if Alan Mulallly deserves to be CEO of the Year at Marketwatch, since it appears his selection has more to do with not letting Ford go bankrupt – like competitors GM and Chrysler – and thus reaping the benefits of customers who wanted to buy domestic but feared any other selection. Whether Ford’s “turnaround” will be a winner, or another Zander/Motorola, we’ll know better in a couple of years.

One fellow who isn’t on anybody’s list is Jeff Immelt at General Electric. His predecessor was. Given that

- GE is the oldest company on the DJIA (Dow Jones Industrial Average)

- GE is one of the most widely held of all corporations

- GE is one of the largest American corporations in revenues and employees

- GE is in a plethora of businesses, globally

- Mr. Immelt is paid several million dollars per year to lead GE

It is worthwhile to think about why he’s not on this list – whether he should be – and if not, whether he should keep his job!

Since Immelt took the helm at GE, the value has actually declined. He’s not likely to win any awards given that sort of performance. Amidst the financial crisis, he had to make a very sweet deal with Berkshire Hathaway to invest cash (via preferred shares) in order to keep GE out of bankruptcy court – a deal that has enriched Mr. Buffett’s company at the expense of GE. GE has exited several businesses, such as its current effort to unload NBC via a deal with Comcast, but it has not created (or bought) a single exciting, noteworthy growth business! GE has become a smaller, lower growth company that narrowly diverted bankruptcy. That isn’t exactly a ringing endorsement for honors!

Yes, GE has developed a nice positive cash flow, which will allow it to repurchase the preferred shares from Berkshire (Marketwatch “GE to Buy Back Buffett’s Preferreds Next Year.”) But what is Mr. Immelt doing to create future shareholder value? His plan to make a few acquisitions, pay some higher dividends (suspended when the company faltered) and repurchase equity offers shareholders very little as a way to generate high rates of return! Why would anyone want to own GE? Nobody expects the company to be a growth leader in 2012, or 2015. With its current businesses, and strategy, there is no reason to expect GE to produce double digit earnings growth – or double its equity within any reasonable investing horizon.

There’s more to being a CEO than being a “caretaker.” Mr. Immelt’s predecessor, Jack Welch, created enormous value for shareholders. Mr. Welch was willing to disurpt the GE status quo. In fact, he intentionally worked at it! He made sure business leaders were constantly challenged to find new markets, create new products, expand into new businesses, leverage new technologies and generate growth! Mr. Welch was willing to take GE into growth markets, give leaders permission to create new Success Formulas, and invest in whatever it took to profitably grow revenues. During the Welch era, competitors quaked at the thought of GE entering their markets because things were always shaken up – and GE changed the game in order to create higher rates of return. During the Welch era investors received amongst the highest rate of return on any common stock! GE value multiplied many-fold, making pensioners (invested in the stock) and employees quite wealthy – even as employment expanded dramatically. That’s why Mr. Welch was Time’s Person of the Year in 2000 — and for many the CEO of the previous decade.

Mr. Immelt, on the other hand, has done nothing to benefit any of his constituencies. Like far too many CEOs, he took a much less aggressive stance toward growth. He has been unwilling to challenge and disrupt existing leaders, or promote aggressive market disruptions through the GE business units. He has not invested in White Space projects that could continue the massive expansion started during the Welch era. To the contrary, he has moved much more slowly, and focused more on selling businesses than growing them. He has resorted to trying to protect GE – rather than keep it moving forward. As a result, the company has retrenched and actually become less interesting, less valuable and less clearly able to produce returns or create new jobs!

Mr. Immelt certainly has his apologists, and seems to securely have the support of his Board of Directors. But we should question this. It actually has an impact on the American economy (and that of several other countries) when the CEO of a company as large as GE loses the ability to create growth. The malaise of the American economy can be directly tied to CEOs who are operating just like Mr. Immelt: doing almost nothing to create new markets, new sources of revenue, new jobs. Many business journalists like to say the government doesn’t create revenue, or jobs. So who will create them when corporate leaders are as feckless as Mr. Immelt? Especially when they control such vast resources!

Congratulations to Mr. Zuckerberg and Mr. Jobs (and Mr. Hastings of Netflix who was named Fortune magazine’s CEO of the Year.) They have created substantial new revenues, profits, cash flow and return for investors. Their company’s employees, suppliers, customers and investors have all benefitted from their leadership. By disrupting the way their company’s operated they pushed into new markets, and demonstrated how in any economy it is possible to create success. Caretakers they are not, so like Mr. Welch each deserves its recent accolades.

And for all those CEOs out there who are behaving as caretakers – for all who are resting on past company laurels – for all who have watched their company value decline – for those who think it’s OK to not grow – for those who blame the economy, or government, or competitors, or customers or their industry for their inability to grow —- well, you either need to learn from these recently honored CEOs and dramatically change direction, or you should be fired.