by Adam Hartung | Feb 15, 2017 | Marketing, Mobile, Retail, Web/Tech

(Photo by Andrew Burton/Getty Images)

Apple’s stock is on a tear. After languishing for well over a year, it is back to record high levels. Once again Apple is the most valuable publicly traded company in America, with a market capitalization exceeding $700 billion. And pretty overwhelmingly, analysts are calling for Apple’s value to continue rising.

But today’s Apple, and the Apple emerging for the future, is absolutely not the Apple which brought investors to this dance. That Apple was all about innovation. That Apple identified big trends – specifically mobile – then created products that turned the trend into enormous markets. The old Apple knew that to create those new markets required an intense devotion to product development, bringing new capabilities to products that opened entirely new markets where needs were previously unmet, and making customers into devotees with really good quality and customer service.

That Apple was built by Steve Jobs. Today’s Apple has been remade by Tim Cook, and it is an entirely different company.

Today’s Apple – the one today’s analysts love – is all about making and selling more iPhones. And treating those iPhone users as a “loyal base” to which they can sell all kinds of apps/services. Today’s Apple is about using the company’s storied position, and brand leadership, to milk more money out of customers that own their devices, and expanding into adjacent markets where the installed base can continue growing.

UBS likes Apple because they think the services business is undervalued. After noting that it today would stand alone as a Fortune 100 company, they expect those services to double in four years. Bernstein notes services today represents 11% of revenue, and should grow at 22% per year. Meanwhile they expect the installed base of iPhones to expand by 27% – largely due to offshore sales – adding further to services growth.

Analysts further like Apple’s likely expansion into India – a previously almost untapped market. CEO Cook has led negotiations to have Foxxcon and Wistron, the current Chinese-based manufacturers, open plants in India for domestic production of iPhones. This expansion into a new geographic market is anticipated to produce tremendous iPhone sales growth. Do you remember when, just before filing for bankruptcy, Krispy Kreme was going to keep up its valuation by expanding into China?

Of course, with so many millions of devices, it is expected that the apps and services to be deployed on those devices will continue growing. Likely exponentially. The iOS developer community has long been one of Apple’s great strengths. Developers like how quickly they can deploy new apps and services to the market via Apple’s sales infrastructure. And with companies the size of IBM dedicated to building enterprise apps for iOS the story heard over and again is about expanding the installed base, then selling the add-ons.

Gee, sounds a lot like the old “razors lead to razor blade sales” strategy – business innovation circa 1966.

Overall, doesn’t this sound a lot like Microsoft? Bill Gates founded a company that revolutionized computing with low-cost software on low-cast hardware that did just about anything you would want. Windows made life easy. Microsoft gave users office automation, databases and all the basic work tools. And when the internet came along Microsoft connected everyone with Internet Explorer – for free! Microsoft created a platform with Windows upon which hordes of developers could build special applications for dedicated markets.

Once this market was created, and pretty much monopolized by Microsoft CEO Gates turned the reigns over to CEO Steve Ballmer. And Mr. Ballmer maximized these advantages. He invested constantly in developing updates to Windows and Office which would continue to insure Microsoft’s market share against emerging competitors like Unix and Linux. The money was so good that over a decade money was poured into gaming, even though that business lost more money than it made in revenue – but who cared? There were occasional investments in products like tablets, hand-helds and phones, but these were merely attractions around the main show. These products came and went and, again, nobody really cared.

Ballmer optimized the gains from Microsoft’s installed base. And a lot – a lot – of money was made doing this. nvestors appreciated the years of ongoing profits, dividends – and even occasional special dividends – as the money poured in. Microsoft was unstoppable in personal computing. The only thing that slowed Microsoft down was the market shift to mobile, which caused the PC market to collapse as unit sales have declined for six straight years (PC sales in 2016 barely managed levels of 2006). But, for a goodly while, it was a great ride!

Today all one hears about at Apple is growing the installed base. Maximizing sales of iPhones. And then selling everyone services. Oh yeah, the Apple Watch came out. Sort of flopped. Nobody really seemed to care much. Not nearly as much as they cared about 2 quarters of sales declines in iPhones. And whatever happened to AppleTV? ApplePay? iBeacons? Beats? Weren’t those supposed to be breakthrough innovations to create new markets? Oh well, nobody seems to much care about those things any longer. Attractions around the main event – iPhones!

So now analysts today aren’t put in the mode of evaluating breakthrough innovations and trying to guess the size of brand new, never before measured markets. That was hard. Now they can be far more predictable forecasting smartphone sales and services revenue, with simulations up and down. And that means they can focus on cash flow. After all, Apple makes more cash than it makes profit! Apple has a $246 billion cash hoard. Most people think Berkshire Hathaway, led by famed investor Warren Buffett, spent $6.6 billion on Apple stock in 2016 because Berkshire sees Apple as a cash generation machine – sort of like a railroad! And if those meetings between CEO Cook and President Trump can yield a tax change allowing repatriation at a low rate then all that cash could lead to a big one time dividend!

And, most likely, the stock will go up. Most likely, a lot. Because for at least a while Apple’s iPhone business is going to be pretty good. And the services business is going to grow. It will be a lot like Microsoft – at least until mobile changed the business. Or, maybe like Xerox giving away copiers to obtain toner sales – until desktop publishing and email cratered the need for copiers and large printers. Or, going all the way back into the 1950s and 60s, when Multigraphics and AB Dick practically gave away small printers to get the ink and plate sales – until xerography crushed that business. Of course you couldn’t go wrong investing in Sears for years, because they had the store locations, they had the brands (Kenmore, Craftsman, et.al.,) they had the credit card services – until Wal-Mart and Amazon changed that game.

You see, that’s the problem with all of these sort of “milk the base” businesses. As the focus shifts to grow the base and add-on sales the company loses sight of customer needs. Innovation declines, then evaporates as everything is poured into maximizing returns from the “core” business. Optimization leads to a focus on costs, and price reductions. Arrogance, based on market leadership, emerges and customer service starts to wane. Quality falters, but is not considered as important because sales are so large.

These changes take time, and the business looks really good as profits and cash flow continue, so it is easy to overlook these cultural and organizational changes, and their potential negative impact. Many applaud cost reductions – remember the glee with which analysts bragged about the cost savings when Dell moved its customer service to India some 20 years ago?

Today we’re hearing more stories about long-term Apple customers who aren’t as happy as they once were.

Genius bar experiences aren’t always great. In a telling AdAge column one long-time Apple user discusses how he had two iPhones fail, and Apple could not replace them leaving the customer with no phone for two weeks – demonstrating a lack of planning for product failures and a lack of concern for customer service. And the same issues were apparent when his corporate Macbook Pro failed. This same corporate customer bemoans design changes that have led to incompatible dongles and jacks, making interoperability problematic even within the Apple line.

Meanwhile, over the last four years Apple has spent lavishly on a new corporate headquarters befitting the country’s most valuable publicly traded company. And Apple leaders have been obsessive about making sure this building is built right! Which sounds well and good, except this was a company that once put customers – and unearthing their hidden needs, wants and wishes – first. Now, a lot of attention is looking inward. Looking at how they are spending all that money from milking the installed base. Putting some of the best managers on building the building – rather than creating new markets.

Who was that retailer that was so successful that it built what was, at the time, the world’s tallest building? Oh yeah, that was Sears.

Markets always shift. Change happens. Today it happens faster than ever in history. And nowhere does change happen faster than in technology and consumer electronics. CEO Cook is leading like CEO Ballmer. He is maximizing the value, and profitability, of the Apple’s core product – the iPhone. And analysts love it. It would be wise to disavow yourself of any thoughts that Apple will be the innovative market creating Jobs/Ives organization it once was.

How long will this be a winning strategy? Your answer to that should determine how long you would like to be an Apple investor. Because some day something new will come along.

by Adam Hartung | Apr 27, 2016 | Food and Drink, In the Rapids, In the Swamp, Retail, Software, Web/Tech

Growth fixes a multitude of sins. If you grow revenues enough (you don’t even need profits, as Amazon has proven) investors will look past a lot of things. With revenue growth high enough, companies can offer employees free meals and massages. Executives and senior managers can fly around in private jets. Companies can build colossal buildings as testaments to their brand, or pay to have thier names on public buildings. R&D budgets can soar, and product launches can fail. Acquisitions are made with no concerns for price. Bonuses can be huge. All is accepted if revenues grow enough.

Just look at Facebook. Today Facebook announced today that for the quarter ended March, 2016 revenues jumped to $5.4B from $3.5B a year ago. Net income tripled to $1.5B from $500M. And the company is basically making all its revenue – 82% – from 1 product, mobile ads. In the last few years Facebook paid enormous premiums to buy WhatsApp and Instagram – but who cares when revenues grow this fast.

Anticipating good news, Facebook’s stock was up a touch today. But once the news came out, after-hours traders pumped the stock to over $118//share, a new all time high. That’s a price/earnings (p/e) multiple of something like 84. With growth like that Facebook’s leadership can do anything it wants.

But, when revenues slide it can become a veritable poop puddle. As Apple found out.

Rumors had swirled that Apple was going to say sales were down. And the stock had struggled to make gains from lows earlier in 2016. When the company’s CEO announced Tuesday that sales were down 13% versus a year ago the stock cratered after-hours, and opened this morning down 10%. Breaking a streak of 51 straight quarters of revenue growth (since 2003) really sent investors fleeing. From trading around $105/share the last 4 days, Apple closed today at ~$97. $40B of equity value was wiped out in 1 day, and the stock trades at a p/e multiple of 10.

The new iPhone 6se outsold projections, iPads beat expectations. First year Apple Watch sales exceeded first year iPhone sales. Mac sales remain much stronger than any other PC manufacturer. Apple iBeacons and Apple Pay continue their march as major technologies in the IoT (Internet of Things) market. And Apple TV keeps growing. There are about 13M users of Apple’s iMusic. There are 1.5M apps on the iTunes store. And the installed base keeps the iTunes store growing. Share buybacks will grow, and the dividend was increased yet again. But, none of that mattered when people heard sales growth had stopped. Now many investors don’t think Apple’s leadership can do anything right.

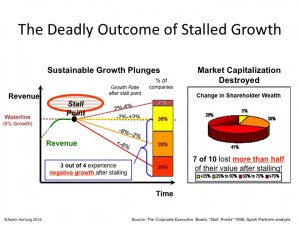

Yet, that was just one quarter. Many companies bounce back from a bad quarter. There is no statistical evidence that one bad quarter is predictive of the next. But we do know that if sales decline versus a year ago for 2 consecutive quarters that is a Growth Stall. And companies that hit a Growth Stall rarely (93% of the time) find a consistent growth path ever again. Regardless of the explanations, Growth Stalls are remarkable predictors of companies that are developing a gap between their offerings, and the marketplace.

Yet, that was just one quarter. Many companies bounce back from a bad quarter. There is no statistical evidence that one bad quarter is predictive of the next. But we do know that if sales decline versus a year ago for 2 consecutive quarters that is a Growth Stall. And companies that hit a Growth Stall rarely (93% of the time) find a consistent growth path ever again. Regardless of the explanations, Growth Stalls are remarkable predictors of companies that are developing a gap between their offerings, and the marketplace.

Which leads us to Chipotle. Chipotle announced that same store sales fell almost 30% in Q1, 2016. That was after a 15% decline in Q4, 2015. And profits turned to losses for the quarter. That is a growth stall. Chipotle shares were $750/share back in early October. Now they are $417 – a drop of over 44%.

Customer illnesses have pointed to a company that grew fast, but apparently didn’t have its act together for safe sourcing of local ingredients, and safe food handling by employees. What seemed like a tactical problem has plagued the company, as more customers became ill in March.

Whether that is all that’s wrong at Chipotle is less clear, however. There is a lot more competition in the fast casual segment than 2 years ago when Chipotle seemed unable to do anything wrong. And although the company stresses healthy food, the calorie count on most portions would add pounds to anyone other than an athlete or construction worker – not exactly in line with current trends toward dieting. What frequently looks like a single problem when a company’s sales dip often turns out to have multiple origins, and regaining growth is nearly always a lot more difficult than leadership expects.

Growth is magical. It allows companies to invest in new products and services, and buoy’s a stock’s value enhancing acquisition ability. It allows for experimentation into new markets, and discovering other growth avenues. But lack of growth is a vital predictor of future performance. Companies without growth find themselves cost cutting and taking actions which often cause valuations to decline.

Right now Facebook is in a wonderful position. Apple has investors rightly concerned. Will next quarter signal a return to growth, or a Growth Stall? And Chipotle has investors heading for the exits, as there is now ample reason to question whether the company will recover its luster of yore.

by Adam Hartung | Aug 29, 2014 | Current Affairs, In the Whirlpool, Leadership

It’s Labor Day, and a time when we naturally think about our jobs.

When it comes to jobs creation, no role is more critical than the CEO. No company will enter into a growth phase, selling more product and expanding employment, unless the CEO agrees. Likewise, no company will shrink, incurring job losses due to layoffs and mass firings, unless the CEO agrees. Both decisions lay at the foot of the CEO, and it is his/her skill that determines whether a company adds jobs, or deletes them.

Over 2 years ago (5 May, 2012) I published “The 5 CEOs Who Should Be Fired.” Not surprisingly, since then employment at all 5 of these companies has lagged economic growth, and in all but one case employment has shrunk. Yet, 3 of these CEOs remain in their jobs – despite lackluster (and in some cases dismal) performance. And all 5 companies are facing significant struggles, if not imminent failure.

#5 – John Chambers at Cisco

In 2012 it was clear that the market shift to public networks and cloud computing was forever changing the use of network equipment which had made Cisco a modern growth story under long-term CEO Chambers. Yet, since that time there has been no clear improvement in Cisco’s fortunes. Despite 2 controversial reorganizations, and 3 rounds of layoffs, Cisco is no better positioned today to grow than it was before.

Increasingly, CEO Chambers’ actions reorganizations and layoffs look like so many machinations to preserve the company’s legacy rather than a clear vision of where the company will grow next. Employee morale has declined, sales growth has lagged and although the stock has rebounded from 2012 lows, it is still at least 10% short of 2010 highs – even as the S&P hits record highs. While his tenure began with a tremendous growth story, today Cisco is at the doorstep of losing relevancy as excitement turns to cloud service providers like Amazon. And the decline in jobs at Cisco is just one sign of the need for new leadership.

#4 Jeff Immelt at General Electric

When CEO Immelt took over for Jack Welch he had some tough shoes to fill. Jack Welch’s tenure marked an explosion in value creation for the last remaining original Dow Jones Industrials component company. Revenues had grown every year, usually in double digits; profits soared, employment grew tremendously and both suppliers and investors gained as the company grew.

But that all stalled under Immelt. GE has failed to develop even one large new market, or position itself as the kind of leading company it was under Welch. Revenues exceeded $150B in 2009 and 2010, yet have declined since. In 2013 revenues dropped to $142B from $145B in 2012. To maintain revenues the company has been forced to continue selling businesses and downsizing employees every year. Total employment in 2014 is now less than in 2012.

Yet, Mr. Immelt continues to keep his job, even though the stock has been a laggard. From the near $60 it peaked at his arrival, the stock faltered. It regained to $40 in 2007, only to plunge to under $10 as the CEO’s over-reliance on financial services nearly bankrupted the once great manufacturing company in the banking crash of 2009. As the company ponders selling its long-standing trademark appliance business, the stock is still less than half its 2007 value, and under 1/3 its all time high. Where are the jobs? Not GE.

#3 Mike Duke at Wal-Mart

Mr. Duke has left Wal-Mart, but not in great shape. Since 2012 the company has been rocked by scandals, as it came to light the company was most likely bribing government officials in Mexico. Meanwhile, it has failed to defend its work practices at the National Labor Relations Board, and remains embattled regarding alleged discrimination of female employees. The company’s employment practices are regularly the target of unions and those supporting a higher minimum wage.

The company has had 6 consecutive quarters of declining traffic, as sales per store continue to lag – demonstrating leadership’s inability to excite people to shop in their stores as growth shifts to dollar stores. The stock was $70 in 2012, and is now only $75.60, even though the S&P 500 is up about 50%. So far smaller format city stores have not generated much attention, and the company remains far behind leader Amazon in on-line sales. WalMart increasingly looks like a giant trapped in its historical house, which is rapidly delapidating.

One big question to ask is who wants to work for WalMart? In 2013 the company threatened to close all its D.C. stores if the city council put through a higher minimum wage. Yet, since then major cities (San Francisco, Chicago, Los Angeles, Seattle, etc.) have either passed, or in the process of passing, local legislation increasing the minimum wage to anywhere from $12.50-$15.00/hour. But there seems no response from WalMart on how it will create profits as its costs rise.

#2 Ed Lampert at Sears

Nine straight quarterly losses. That about says it all for struggling Sears. Since the 5/2012 column the CEO has shuttered several stores, and sales continue dropping at those that remain open. Industry pundits now call Sears irrelevant, and the question is looming whether it will follow Radio Shack into oblivion soon.

CEO Lampert has singlehandedly destroyed the Sears brand, as well as that of its namesake products such as Kenmore and Diehard. He has laid off thousands of employees as he consolidated stores, yet he has been unable to capture any value from the unused real estate. Meanwhile, the leadership team has been the quintessential example of “a revolving door at headquarters.” From about $50/share 5/2012 (well off the peak of $190 in 2007,) the stock has dropped to the mid-$30s which is about where it was in its first year of Lampert leadership (2004.)

Without a doubt, Mr. Lampert has overtaken the reigns as the worst CEO of a large, publicly traded corporation in America (now that Steve Ballmer has resigned – see next item.)

#1 Steve Ballmer at Microsoft

In 2013 Steve Ballmer resigned as CEO of Microsoft. After being replaced, within a year he resigned as a Board member. Both events triggered analyst enthusiasm, and the stock rose.

However, Mr. Ballmer left Microsoft in far worse condition after his decade of leadership. Microsoft missed the market shift to mobile, over-investing in Windows 8 to shore up PC sales and buying Nokia at a premium to try and catch the market. Unfortunately Windows 8 has not been a success, especially in mobile where it has less than 5% share. Surface tablets were written down, and now console sales are declining as gamers go mobile.

As a result the new CEO has been forced to make layoffs in all divisions – most substantially in the mobile handset (formerly Nokia) business – since I positioned Mr. Ballmer as America’s worst CEO in 2012. Job growth appears highly unlikely at Microsoft.

“CEOs – From Makers to Takers”

Forbes colleague Steve Denning has written an excellent column on the transformation of CEOs from those who make businesses, to those who take from businesses. Far too many CEOs focus on personal net worth building, making enormous compensation regardless of company performance. Money is spent on inflated pay, stock buybacks and managing short-term earnings to maximize bonuses. Too often immediate cost savings, such as from outsourcing, drive bad long-term decisions.

CEOs are the ones who determine how our collective national resources are invested. The private economy, which they control, is vastly larger than any spending by the government. Harvard professor William Lazonick details how between 2003 and 2012 CEOs gave back 54% of all earnings in share buybacks (to drive up stock prices short term) and handed out another 37% in dividends. Investors may have gained, but it’s hard to create jobs (and for a nation to prosper) when only 9% of all earnings for a decade go into building new businesses!

There are great CEOs out there. Steve Jobs and his replacement Tim Cook increased revenues and employment dramatically at Apple. Jeff Bezos made Amazon into an enviable growth machine, producing revenues and jobs. These leaders are focused on doing what it takes to grow their companies, and as a result the jobs in America.

It’s just too bad the 5 fellows profiled above have done more to destroy value than create it.

by Adam Hartung | Sep 19, 2013 | Current Affairs, In the Swamp, Innovation, Leadership, Television, Web/Tech

Apple announced the new iPhones recently. And mostly, nobody cared.

Remember when users waited anxiously for new products from Apple? Even the media became addicted to a new round of Apple products every few months. Apple announcements seemed a sure-fire way to excite folks with new possibilities for getting things done in a fast changing world.

But the new iPhones, and the underlying new iPhone software called iOS7, has almost nobody excited.

Instead of the product launches speaking for themselves, the CEO (Tim Cook) and his top product development lieutenants (Jony Ive and Craig Federighi) have been making the media rounds at BloombergBusinessWeek and USAToday telling us that Apple is still a really innovative place. Unfortunately, their words aren't that convincing. Not nearly as convincing as former product launches.

CEO Cook is trying to convince us that Apple's big loss of market share should not be troubling. iPhone owners still use their smartphones more than Android owners, and that's all we should care about. Unfortunately, Apple profits come from unit sales (and app sales) rather than minutes used. So the chronic share loss is quite concerning.

Especially since unit sales are now growing barely in single digits, and revenue growth quarter-over-quarter, which sailed through 2012 in the 50-75% range, have suddenly gone completely flat (less than 1% last quarter.) And margins have plunged from nearly 50% to about 35% – more like 2009 (and briefly in 2010) than what investors had grown accustomed to during Apple's great value rise. The numbers do not align with executive optimism.

For industry aficianados iOS7 is a big deal. Forbes Haydn Shaughnessy does a great job of laying out why Apple will benefit from giving its ecosystem of suppliers a new operating system on which to build enhanced features and functionality. Such product updates will keep many developers writing for the iOS devices, and keep the battle tight with Samsung and others using Google's Android OS while making it ever more difficult for Microsoft to gain Windows8 traction in mobile.

And that is good for Apple. It insures ongoing sales, and ongoing profits. In the slog-through-the-tech-trench-warfare Apple is continuing to bring new guns to the battle, making sure it doesn't get blown up.

But that isn't why Apple became the most valuable publicly traded company in America.

We became addicted to a company that brought us things which were great, even when we didn't know we wanted them – much less think we needed them. We were happy with CDs and Walkmen until we discovered much smaller, lighter iPods and 99cent iTunes. We were happy with our Blackberries until we learned the great benefits of apps, and all the things we could do with a simple smartphone. We were happy working on laptops until we discovered smaller, lighter tablets could accomplish almost everything we couldn't do on our iPhone, while keeping us 24×7 connected to the cloud (that we didn't even know or care about before,) allowing us to leave the laptop at the office.

Now we hear about upgrades. A better operating system (sort of sounds like Microsoft talking, to be honest.) Great for hard core techies, but what do users care? A better Siri; which we aren't yet sure we really like, or trust. A new fingerprint reader which may be better security, but leaves us wondering if it will have Siri-like problems actually working. New cheaper color cases – which don't matter at all unless you are trying to downgrade your product (sounds sort of like P&G trying to convince us that cheaper, less good "Basic" Bounty was an innovation.)

More (upgrades) Better (voice interface, camera capability, security) and Cheaper (plastic cases) is not innovation. It is defending and extending your past success. There's nothing wrong with that, but it doesn't excite us. And it doesn't make your brand something people can't live without. And, while it keeps the battle for sales going, it doesn't grow your margin, or dramatically grow your sales (it has declining marginal returns, in fact.)

And it won't get your stock price from $450-$475/share back to $700.

We all know what we want from Apple. We long for the days when the old CEO would have said "You like Google Glass? Look at this……. This will change the way you work forever!!"

We've been waiting for an Apple TV that let's us bypass clunky remote controls, rapidly find favorite shows and helps us avoid unwanted ads and clutter. But we've been getting a tease of Dick Tracy-esque smart watches.

From the world's #1 tech brand (in market cap – and probably user opinion) we want something disruptive! Something that changes the game on old companies we less than love like Comcast and DirecTV. Something that helps us get rid of annoying problems like expensive and bad electric service, or routers in our basements and bedrooms, or navigation devices in our cars, or thumb drives hooked up to our flat screen TVs —- or doctor visits. We want something Game Changing!

Apple's new CEO seems to be great at the Sustaining Innovation game. And that pretty much assures Apple of at least a few more years of nicely profitable sales. But it won't keep Apple on top of the tech, or market cap, heap. For that Apple needs to bring the market something big. We've waited 2 years, which is an eternity in tech and financial markets. If something doesn't happen soon, Apple investors deserve to be worried, and wary.

by Adam Hartung | Oct 26, 2012 | Current Affairs, Defend & Extend, In the Whirlpool, Innovation, Leadership, Web/Tech

This is an exciting time of year for tech users – which is now all of us. The biggest show is the battle between smartphone and tablet leader Apple – which has announced new products with the iPhone 5 and iPad Mini – and the now flailing, old industry leader Microsoft which is trying to re-ignite its sales with a new tablet, operating system and office productivity suite.

I’m reminded of an old joke. Steve the trucker drives with his pal Alex. Someone at the diner says “Steve, imagine you’re going 60 miles an hour when you start down a hill. You keep gaining speed, nearing 90. Then you realize your brakes are out. Now, you see one quarter mile ahead a turn in the road, because there’s a barricade and beyond that a monster cliff. What do you do?”

Steve smiles and says “Well, I wake up Alex.”

“What? Why?” asks the questioner.

“Because Alex has never seen a wreck like the one we’re about to have.”

Microsoft has played “bet the company” on its Windows 8 launch, updated office suite and accompanied Surface tablet. (More on why it didn’t have to do this later.) Now Microsoft has to do something almost never done in business. The company has to overcome a 3 year lateness to market and upend a multi-billion dollar revenue and brand leader. It must overcome two very successful market pioneers, both of which have massive sales, high growth, very good margins, great cash flow and enormous war chests (Apple has over $100B cash.)

Just on the face of it, the daunting task sounds unlikely to succeed.

But there is far more reason to be skeptical. Apple created these markets with new products about which people had few, if any conceptions. But today customers have strong viewpoints on both what a smartphone and tablet should be like to use – and what they expect from Microsoft. And these two viewpoints are almost diametrically opposed.

Yet Microsoft has tried bridging them in the new product – and in doing so guaranteed the products will do poorly. By trying to please everyone Microsoft, like the Ford Edsel, is going to please almost no one:

- Since the initial product viewing, almost all professional reviewers have said the Surface is neat, but not fantastically so. It is different from iOS and Google’s Android products, but not superior. It has generated very little enthusiasm.

- Tests by average users have shown the products to be non-intuitive. Especially when told they are Microsoft products. So the Apple-based interface intuition doesn’t come through for easy use, nor does historical Microsoft experience. Average users have been confused, and realize they now must learn a 3rd interface – the iOS or Android they have, the old Microsoft they have, and now this new thing. It might as well be Linux for all its similarity to Microsoft.

- For those who were excited about having native office products on a tablet, the products aren’t the same as before – in feel or function. And the question becomes, if you really want the office suite do you really want a tablet or should you be using a laptop? The very issue of trying to use Office on the Surface easily makes people rethink the question, and start to realize that they may have said they wanted this, but it really isn’t the big deal they thought it would be. The tablet and laptop have different uses, and between Surface and Win8 they are seeing learning curve cost maybe isn’t worth it.

- The new Win8 – especially on the tablet – does not support a lot of the “professional” applications written on older Windows versions. Those developers now have to redevelop their code for a new platform – and many won’t work on the new tablet processors.

- Many have been banking on Microsoft winning the “enterprise” market. Selling to CIOs who want to preserve legacy code by offering a Microsoft solution. But they run into two problems. (1) Users now have to learn this 3rd, new interface. If they have a Galaxy tab or iPad they will have to carry another device, and learn how to use it. Do not expect happy employees, or executives, who expressly desire avoiding both these ideas. (2) Not all those old applications (drivers, code, etc) will port to the new platform so easily. This is not a “drop in” solution. It will take IT time and money – while CEOs keep asking “why aren’t you doing this for my iPad?”

All of this adds up to a new product set that is very late to market, yet doesn’t offer anything really new. By trying to defend and extend its Windows and Office history, Microsoft missed the market shift. It has spent several billion dollars trying to come up with something that will excite people. But instead of offering something new to change the market, it has given people something old in a new package. Microsoft they pretty much missed the market altogether.

Everyone knows that PC sales are going to decline. Unfortunately, this launch may well accelerate that decline. Remember how slowly people were willing to switch to Vista? How slowly they adopted Microsoft 7 and Office 2010? There are still millions of users running XP – and even Office XP (Office Professional 2003.) These new products may convince customers that the time and effort to “upgrade” simply means its time to switch.

Microsoft has fallen into a classic problem the Dean of innovation Clayton Christensen discusses. Microsoft long ago overshot the user need for PCs and office automation tools. But instead of focusing on developing new solutions – like Apple did by introducing greater mobility with its i products – Microsoft has diligently, for a decade, continued to dump money into overshooting the user needs for its basic products. They can’t admit to themselves that very, very, very few people are looking for a new spreadsheet or word processing application update. Or a new operating system for their laptop.

These new Microsoft products will NOT cause people to quit the trend to mobile devices. They will not change the trend of corporate users supplying their own devices for work (there’s now even an IT acronym for this movement [BYOD,] and a Wikipedia page.) It will not find a ready, excited market of people wanting to learn yet another interface, especially to use old applications they thought they already new!

It did not have to be this way.

Years ago Microsoft started pouring money into xBox. And although investors can complain about the historical cost, the xBox (and Kinect) are now market leaders in the family room. Honestly, Microsoft already has – especially with new products released this week – what people are hoping they can soon buy from AppleTV or GoogleTV; products that are at best vaporware.

Long-term, there is yet another great battle to be fought. What will be the role of monitors, scattered in homes and bars, and in train stations, lobbies and everywhere else? Who will control the access to monitors which will be used for everything from entertainment (video/music,) to research and gaming. The tablet and smartphones may well die, or mutate dramatically, as the ability to connect via monitors located nearly everywhere using —- xBox?

But, this week all discussion of the new xBox Live and music applications were overshadowed by the CEO’s determination to promote the dying product line around Windows8.

This was simply stupid. Ballmer should be fired.

The PC products should be managed for a cash hoarding transition into a smaller market. Investments should be maximized into the new products that support the next market transition. xBox and Kinect should be held up as game changers, and Microsoft should be repositioned as a leader in the family and conference room; an indespensible product line in an ever-more-connected world.

But that didn’t happen this week. And the CEO keeps heading straight for the cliff. Maybe when he takes the truck over the guard rail he’ll finally be replaced. Investors can only wake up and watch – and hope it happens sooner, rather than later.

UPDATE 16 April, 2019 – Android TV is a new emerging tech that could have a big impact on the overall marketplace. Read more about Android TV here.