This week, to almost no fanfare, a Microsoft Vice President issued a statement saying that Windows 10X (planned for 2019) would not ship in 2021. In fact, it would never ship. The technology enhancements would be integrated into existing Windows, and other products. While this gained little press, it is great news for customers and investors.

CEO Satya Nadella has officially changed the course of Microsoft. Under former CEO Ballmer the behemoth kept pouring money into Windows and Office. While the world was moving from PCs and PC servers to mobile devices and the cloud, Ballmer just kept pouring billions into old products. His slavish insistence on trying to defend & extend an old “core product line,” which every year was losing importance as PC sales slowed, was killing Microsoft — leading me to call Mr. Ballmer the worst CEO in America (my Forbes column that was by far the most read of any I ever penned.) After more than a decade as CEO, Ballmer had spent a lot of Microsoft money on new versions of its ancient product and bad acquisitions like Skype and Nokia, but he entirely missed the market shift in his customer base. In my blog post, “Microsoft, What Next?”, I described the challenges ahead to pull Microsoft out of the Growth Stall.

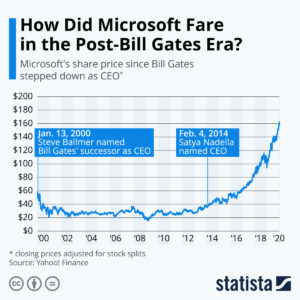

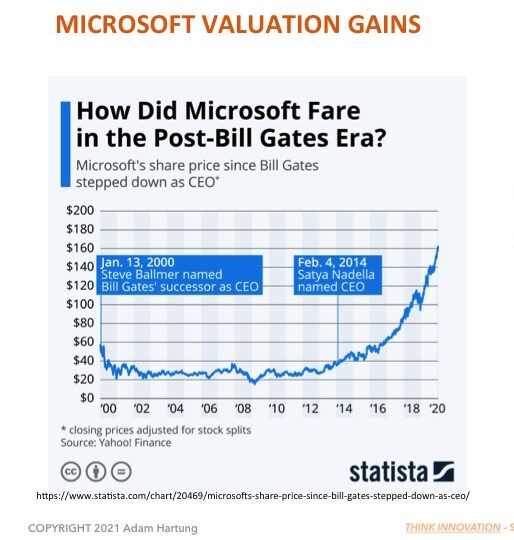

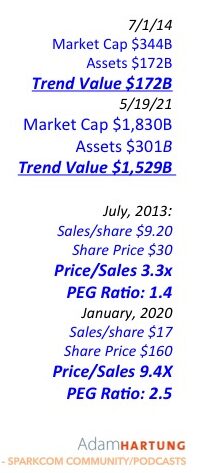

This chart shows just how much Microsoft has changed since Nadella took over. During Ballmer’s 13+ year leadership Microsoft’s valuation barely budged. (From left to small blue box.) But, Nadella rapidly shifted investments from Windows and Office to software as a service and cloud computing. (Graph rapidly increases.) That radical redirection enlivened both sales and earnings – and the company’s future growth prospects. In short, where the company had been locked-in to defending & extending its past, Nadella redirected the company onto trends. By doing so, he improved sales per/share 85%, the price/sales ratio from 3.3x to 9.4x, and the PEG ratio from 1.4 to 2.5. The company’s “trend value” (market cap increase over assets due to aligning with trends) since Nadella took charge has grown from $172 billion to a staggering $1.53 trillion!!! Now that is wealth creation!!!

In the years leading up to Ballmer’s firing I was a very loud critic of Microsoft. In multiple Forbes columns, (republished as blogs on my web site) I pushed for his ouster. But even more importantly I gave the company little hope of long term viability. By over-investing in outdated products it seemed most likely Microsoft would go the way of Hostess Baking, Sears, DEC and Sun Microsystems – irrelevant leading to failure. I rabidly recommended not owning Microsoft.

Microsoft Stock 2014-2021

The Impossible Just Takes a little Longer…

But Nadella achieved the improbable. Much like Jobs when he retook the reigns at Apple, Nadella quit looking (and investing) in the rear view mirror. Like Jobs, he dropped investing in PC’s. Instead he focused on the future, and where Jobs invested in mobility, Nadella has invested in the cloud. Very few companies make this kind of radical shift in resourcing projects, even when it is the obviously right thing to do. And Nadella deserves the credit for making this radical change in Microsoft, saving the company from near-oblivion while creating a very viable, valuable company in a short time. Where once I saw a company heading for infamy, now Microsoft shows all signs of leadership toward the next technology wave and longevity. Quietly saying the company has no plans for a new Windows version, which nobody cares about anyway, is a tremendous demonstration of looking forward rather than backward.

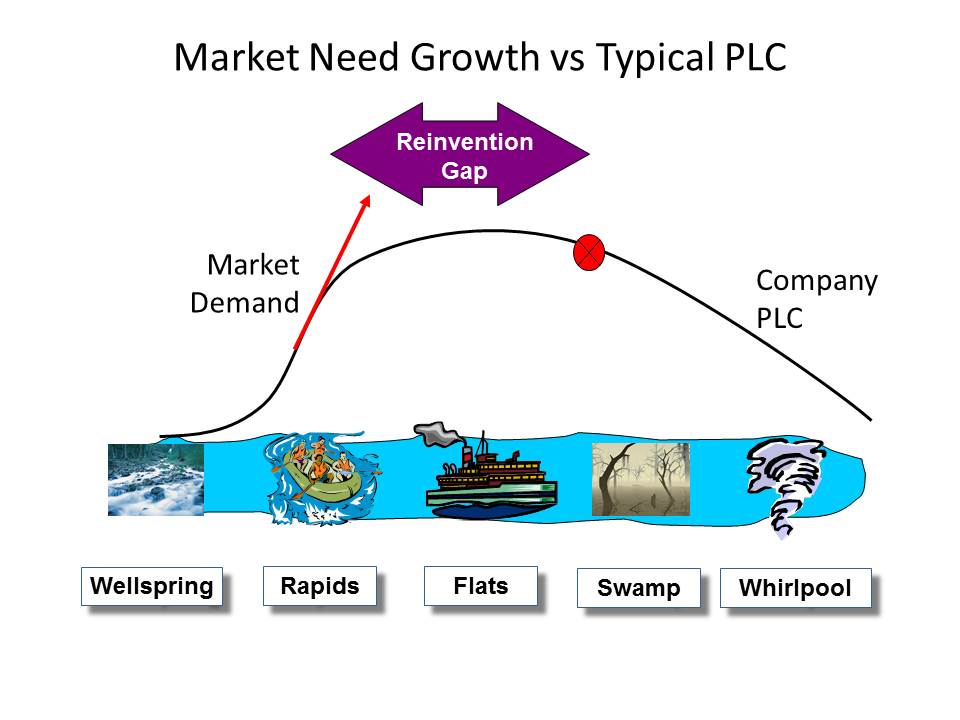

Jump the Re-Invention Gap

Do you have the insight to know when you’re company is over-investing in past solutions as markets shift? Are you like Ballmer, always making the next version of what once made you great, or are you like CEO Nadella – ready to unload your past focus in order to seek future growth? Are you letting market trends guide your investing and solution development, allowing you to de-invest in outdated technologies and products? Like Reed Hastings at Netflix, do you see the need to pivot? Netflix changed from an outdated business model (shipping DVDs and tapes) to a new model (streaming) in order to keep your company viable, and an industry leader. You must be if you want to thrive in the rapidly changing competitive marketplace of the 2020’s.

Did you see the trends, and were you expecting the changes that would happen to your demand? It IS possible to use trends to make good forecasts, and prepare for big market shifts. If you don’t have time to do it, perhaps you should contact us, Spark Partners. We track hundreds of trends, and are experts at developing scenarios applied to your business to help you make better decisions.

TRENDS MATTER. If you align with trends your business can do GREAT! Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business. Click for Assessment info.Or, to keep up on trends, subscribe to our weekly podcasts and posts on trends and how they will affect the world of business at www.SparkPartners.com

Give us a call or send an email. Adam@sparkpartners.com 847-726-8465.

People who follow my speaking and writing – including my over 400 Forbes columns – know that I preach the importance of growth. Successful organizations are agile – and agility is the sum of learning + adaptability. Smart organizations are constantly looking externally, gathering data, learning about markets and shifts – then structured to adopt those learnings into their business model and adapt the organization to new market needs.

Steve Ballmer was the antithesis of agility. For his entire career he knew only that Windows and Office made all the money at Microsoft. So he kept investing in Windows and Office. He failed at everything else. False starts in phones, tablets, gaming – products came and went like ice cream cones on a hot August day. Ballmer laughed at the very notion of the iPhone ever being successful – while simultaneously throwing away $7.2B buying Nokia. Then there was $8.5B buying Skype. $400M buying the Borders Nook. Those were ridiculous acquisitions that just wasted shareholder money. To Ballmer, Microsoft’s future relied on maintaining Windows and Office.

It was not hard to identify Steve Ballmer as the worst CEO in America in 2012. When Ballmer took over Microsoft it was worth $60/share. He drove that value down to $20. And the company valuation was almost unchanged his entire 14 years as CEO. He remained locked-in to trying to Defend & Extend PC sales, and it did Microsoft no good. But when the Board replaced Ballmer with Nadella the company moved quickly into growth in gaming, and especially cloud services. In just 6 years Nadella has improved the company’s value by 400%!!!

Success is NOT about defending the past. Success IS about growth. Don’t be locked in to what worked before. Focus on what markets want and need – learn how to understand these needs – and then adapt to giving customers new solutions. Don’t make the mistakes of Ballmer – be a Nadella to lead your organization into growth opportunities!

The Only Surprise At GE Was That Anyone Was Surprised

GE Sign in Schenectady, NY- Hearst Newspapers

General Electric announced quarterly results this week, and and they were pretty bad. Profits were nowhere near expectations, and the company lowered expectations for the year. Cash flow was also disappointing, not even strong enough to cover the dividend. Now analysts are really negative on company prospects, and most expect the dividend to be cut.

In other words, CEO Flannery continues the strategy of making GE smaller, and a less hospitable workplace, that his predecessor Immelt started implementing 16 years ago. That’s the strategy that has seen GE lose ~45% of its value since Immelt took the top job, and lose over 60% of its value since peaking at $60 in 2000. So far, GE just keeps shrinking in size, and value, and leadership gives no indication it has a plan to grow GE revenues and profits in future markets building on major market trends.

What’s most surprising is that people seem surprised by the horrible current performance, and surprised that GE is in such terrible condition. All the way back in December, 2010 this column highlighted selections for CEO of the year, and CEO of the decade, and in doing so pointed out that GE’s Immelt was on nobody’s list. Even though his predecessor, Jack Welch, was widely lauded.

Immelt inherited one of America’s strongest, fastest growing and most valuable companies. But in the first few years of his leadership the company completely failed to maintain Welch’s gains, and under Immelt’s mismanagement nearly went bankrupt by not preparing for the near-collapse of financial services in the Great Recession. It was obvious then that Immelt was trying to be a “caretaker” of GE, a “steward” of its history. But he was not an effective leader with plans for a growing future, and competitors were beating up GE in all markets. Even upstarts like Facebook, and its CEO Mark Zuckerberg, were far outperforming the stagnating, declining GE.

By May, 2012 it was impossible to miss the mismanagement at GE. This column selected CEO Immelt as the 4th worst CEO of all publicly traded American companies (beaten in badness by Mike Duke of WalMart who was pushed out during allegations of international bribery and fraud, Ed Lampert of Sears who has now completely destroyed the once great retailer, and Steve Ballmer of Microsoft who over-invested in Windows and Office while missing every major tech development of the last 15 years before being forced out by the board.) By 2012 it was time for the Board of Directors to take action and replace Immelt. But few investors amplified this column’s cries for change, and quiet complacency set in as people simply expected GE to perform better. Just because it was GE, it appeared, as there were no signs the company understood market trends and how to ignite growth.

Of course, performance did not improve at GE. By April, 2015 GE was the victim of a total leadership failure. The company was not developing any major new trends, and Immelt’s focus was on unraveling old businesses, mostly via sales to external parties, in order to increase cash. And the cash was used for share buybacks and dividends, rather than investing in growth. A slow, and badly implemented, liquidation of one of America’s oldest, and greatest, companies was underway.

Which made GE a target for activist investors, and Trian Funds took up the challenge, investing $1.5B in GE stock and taking a seat on the GE board. Finally, it was time for action. Immelt was pushed out and Flannery was put in, and dramatic cuts and re-organizations led the discussions. Current appearances indicate GE will be significantly dismantled, assets will be sold, and in short order GE will look nothing like the great company it once was.

But, the question remains, why did things have to become so bad before the board took action? Why were people surprised? Why didn’t Jim Cramer scream for a leadership housecleaning 7, 5 or 3 years ago? Why didn’t shareholders vote against CEO compensation plans on the “say-on-pay” measures, exerting their voice to change a lackluster board that was allowing an incompetent CEO to remain in the job? Why wasn’t the pension fund, constantly whittling away at retiree benefits, forcing change? Why were so many people, so many leaders, so quiet about what was an obvious business failure? A failure that needed to be addressed, first and foremost, by replacing the CEO?

So GE’s stock value has taken a big hit of late. And now people seem surprised by the admission of how bad things really are. What’s really surprising is that people are surprised. This was not hard to see coming.

Michael Dell has put together a hedge fund, one of his largest suppliers and some debt money to take his company, Dell, Inc. private. There are large investors threatening to sue, claiming the price isn't high enough. While they are wrangling, small investors should consider this privatization manna from heaven, take the new, higher price and run to invest elsewhere – thankful you're getting more than the company is worth.

In the 1990s everybody thought Dell was an incredible company. With literally no innovation a young fellow built an enormously large, profitable company using other people's money, and technology. Dell jumped into the PC business as it was born. Suppliers were making the important bits, and looking for "partners" to build boxes. Dell realized he could let other people invest in microprocessor, memory, disk drive, operating system and application software development. All he had to do was put the pieces together.

Dell was the rare example of a company that was built on nothing more than execution. By marketing hard, selling hard, buying smart and building cheap Dell could produce a product for which demand was skyrocketing. Every year brought out new advancements from suppliers Dell could package up and sell as the latest, greatest model. All Dell had to do was stay focused on its "core" PC market, avoid distractions, and win at execution. Heck, everyone was going to make money building and selling PCs. How much you made boiled down to how hard you worked. It wasn't about strategy or innovation – just execution.

Dell's business worked for one simple reason. Everybody wanted PCs. More than one. And everybody wanted bigger, more powerful PCs as they came available. Market demand exploded as the PC became part of everything companies, and people, do. As long as demand was growing, Dell was growing. And with clever execution – primarily focused on speed (sell, build, deliver, get the cash before the supplier has to be paid) – Dell became a multi-billion dollar company, and its founder a billionaire with no college degree, and no claim to being a technology genius.

But, the market shifted. As this column has pointed out many times, demand for PCs went flat – never to return to previous growth rates. Users have moved to mobile devices such as smartphones and tablets, while corporate IT is transitioning from PC servers to cloud services. iPad sales now nearly match all of Dell's sales. Dell might well be the world's best PC maker, but when people don't want PCs that doesn't matter any more.

Market watchers knew this. That's why Dell's stock took a long ride from its lofty value on the rapids of growth to the recent distinctly low value as it slipped into the whirlpool of failure.

If you think adding debt to Dell will save it from the market shift, just look at how well that strategy worked for fixing Tribune Corporation. A Sam Zell led LBO took over the company claiming he had plans for a new future, as advertisers shifted away from newspapers. Bankruptcy came soon enough, employee pensions were wiped out, massive layoffs undertaken and 4 years of legal fighting followed to see if there was any plan that would keep the company afloat. Debt never fixes a failing company, and Dell knows that. Dell has no answer to changing market demand away from PCs.

Now the buzzards are circling. HP has been caught in a rush to destruction ever since CEO Fiorina decided to buy Compaq and gut the HP R&D in an effort to follow Dell's wild revenue ride. Only massive cost cutting by the following CEO Hurd kept HP alive, wiping out any remnants of innovation. Now HP has a dismal future. But it hopes that as the PC market shrinks the elimination of one competitor, Dell, will give newest CEO Whitman more time to somehow find something HP can do besides follow Dell into bankruptcy court.

Watching as its execution-oriented ecosystem manufacturers are struggling, supplier Microsoft is pulling out its wallet to try and extend the timeline. Plundering its $85B war chest, Microsoft keeps adding features, with acquisitions such as Skype, that consume cash while offering no returns – or even strong reasons for people to stop the transition to tablets.

Additionally it keeps putting up money for companies that it hopes will build end-user products on its software, such as its $500M investment in Barnes & Noble's Nook and now putting $2B into Dell. $85B is a lot of money, but how much more will Microsoft have to spend to keep HP alive – or money losing Acer – or Lenovo? A billion here, a billion there and pretty soon it adds up to a lot of money! Not counting losses in its own entertainmnet and on-line divisions. The transition to mobile devices is permanent and Microsoft has arrived at the game incredibly late – and with products that simply cannot obtain better than mixed reviews.

The lesson to learn is that management, and investors, take a big risk when they focus on execution. Without innovation, organizations become reliant on vendors who may, or may not, stay ahead of market transitions. When an organization fails to be an innovator, someone who creates its own game changers, and instead tries to succeed by being the best at execution eventually market shifts will kill it. It is not a question of if, but when.

Being the world's best PC maker is no better than being the world's best maker of white bread (Hostess) or the world's best maker of photographic film (Kodak) or the world's best 5 and dime retailer (Woolworth's) or the world's best manufacturer of bicycles (Schwinn) or cold rolled steel (Bethlehem Steel.) Being able to execute – even execute really, really well – is not a long-term viable strategy. Eventually, innovation will create market shifts that will kill you.

Microsoft needed a great Christmas season. After years of product stagnation, and a big market shift toward mobile devices from PCs, Microsoft's future relied on the company seeing customers demonstrate they were ready to jump in heavily for Windows8 products – including the new Surface tablet.

Looking deeper, for the 4th quarter PC sales declined by almost 5% according to Gartner research, and by almost 6.5% according to IDC. Both groups no longer expect a rebound in PC shipments, as they believe homes will no longer have more than 1 PC due to the mobile device penetration – the market where Surface and Win8 phones have failed to make any significant impact or move beyond a tiny market share. Users increasingly see the complexity of shifting to Win8 as not worth the effort; and if a switch is to be made consumer and businesses now favor iOS and Android.

These trends mean nothing short of the ruin of Microsoft. Microsoft makes more than 75% of its profits from Windows and Office. Less than 25% comes from its vaunted servers and tools. And Microsoft makes nothing from its xBox/Kinect entertainment division, while losing vast sums on-line (negative $350M-$750M/quarter). No matter how much anyone likes the non-Windows Microsoft products, without the historical Windows/Office sales and profits Microsoft is not sustainable.

So what can we expect at Microsoft:

Ballmer has committed to fight to the death in his effort to defend & extend Windows. So expect death as resources are poured into the unwinnable battle to convert users from iOS and Android.

As resources are poured out of the company in the Quixotic effort to prolong Windows/Office, any hope of future dividends falls to zero.

Expect enormous layoffs over the next 3 years. Something like 50-60%, or more, of employees will go away.

Expect closure of the long-suffering on-line division in order to conserve resources.

The entertainment division will be spun off, sold to someone like Sony or even Barnes & Noble, or dramatically reduced in size. Unable to make a profit it will increasingly be seen as a distraction to the battle for saving Windows – and Microsoft leadership has long shown they have no idea how to profitably grow this business unit.

As more and more of the market shifts to competitive cloud businesses Apple, Amazon and others will grow significantly. Microsoft, losing its user base, will demonstrate its inability to build a new business in the cloud, mimicking its historical experiences with Zune (mobile music) and Microsoft mobile phones. Microsoft server and tool sales will suffer, creating a much more difficult profit environment for the sole remaining profitable division.

Missing the market shift to mobile has already forever tarnished the Microsoft brand. No longer is Microsoft seen as a leader, and instead it is rapidly losing market relevancy as people look to Apple, Google, Amazon, Samsung, Facebook and others for leadership. The declining sales, and lack of customer interest will lead to a tailspin at Microsoft not unlike what happened to RIM. Cash will be burned in what Microsoft will consider an "epic" struggle to save the "core of the company."

But failure is already inevitable. At this stage, not even a new CEO can save Microsoft. Steve Ballmer played "Bet the Company" on the long-delayed release of Win8, losing the chance to refocus Microsoft on other growing divisions with greater chance of success. Unfortunately, the other players already had enough chips to simply bid Microsoft out of the mobile game – and Microsoft's ante is now long gone – without holding a hand even remotely able to turn around the product situation.

Game over. Ballmer loses. And if you keep your money invested in Microsoft it will disappear along with the company.

This chart shows just how much Microsoft has changed since Nadella took over. During Ballmer’s 13+ year leadership Microsoft’s valuation barely budged. (From left to small blue box.) But, Nadella rapidly shifted investments from Windows and Office to software as a service and cloud computing. (Graph rapidly increases.) That radical redirection enlivened both sales and earnings – and the company’s future growth prospects. In short, where the company had been locked-in to defending & extending its past, Nadella redirected the company onto trends. By doing so, he improved sales per/share 85%, the price/sales ratio from 3.3x to 9.4x, and the PEG ratio from 1.4 to 2.5. The company’s “trend value” (market cap increase over assets due to aligning with trends) since Nadella took charge has grown from $172 billion to a staggering $1.53 trillion!!! Now that is wealth creation!!!

This chart shows just how much Microsoft has changed since Nadella took over. During Ballmer’s 13+ year leadership Microsoft’s valuation barely budged. (From left to small blue box.) But, Nadella rapidly shifted investments from Windows and Office to software as a service and cloud computing. (Graph rapidly increases.) That radical redirection enlivened both sales and earnings – and the company’s future growth prospects. In short, where the company had been locked-in to defending & extending its past, Nadella redirected the company onto trends. By doing so, he improved sales per/share 85%, the price/sales ratio from 3.3x to 9.4x, and the PEG ratio from 1.4 to 2.5. The company’s “trend value” (market cap increase over assets due to aligning with trends) since Nadella took charge has grown from $172 billion to a staggering $1.53 trillion!!! Now that is wealth creation!!!

Do you have the insight to know when you’re company is over-investing in past solutions as markets shift? Are you like Ballmer, always making the next version of what once made you great, or are you like CEO Nadella – ready to unload your past focus in order to seek future growth? Are you letting market trends guide your investing and solution development, allowing you to de-invest in outdated technologies and products? Like Reed Hastings at Netflix, do you see the need to pivot? Netflix changed from an outdated business model (shipping DVDs and tapes) to a new model (streaming) in order to keep your company viable, and an industry leader. You must be if you want to thrive in the rapidly changing competitive marketplace of the 2020’s.

Do you have the insight to know when you’re company is over-investing in past solutions as markets shift? Are you like Ballmer, always making the next version of what once made you great, or are you like CEO Nadella – ready to unload your past focus in order to seek future growth? Are you letting market trends guide your investing and solution development, allowing you to de-invest in outdated technologies and products? Like Reed Hastings at Netflix, do you see the need to pivot? Netflix changed from an outdated business model (shipping DVDs and tapes) to a new model (streaming) in order to keep your company viable, and an industry leader. You must be if you want to thrive in the rapidly changing competitive marketplace of the 2020’s.