by Adam Hartung | May 10, 2016 | Defend & Extend, In the Swamp, Leadership, Lifecycle, Web/Tech

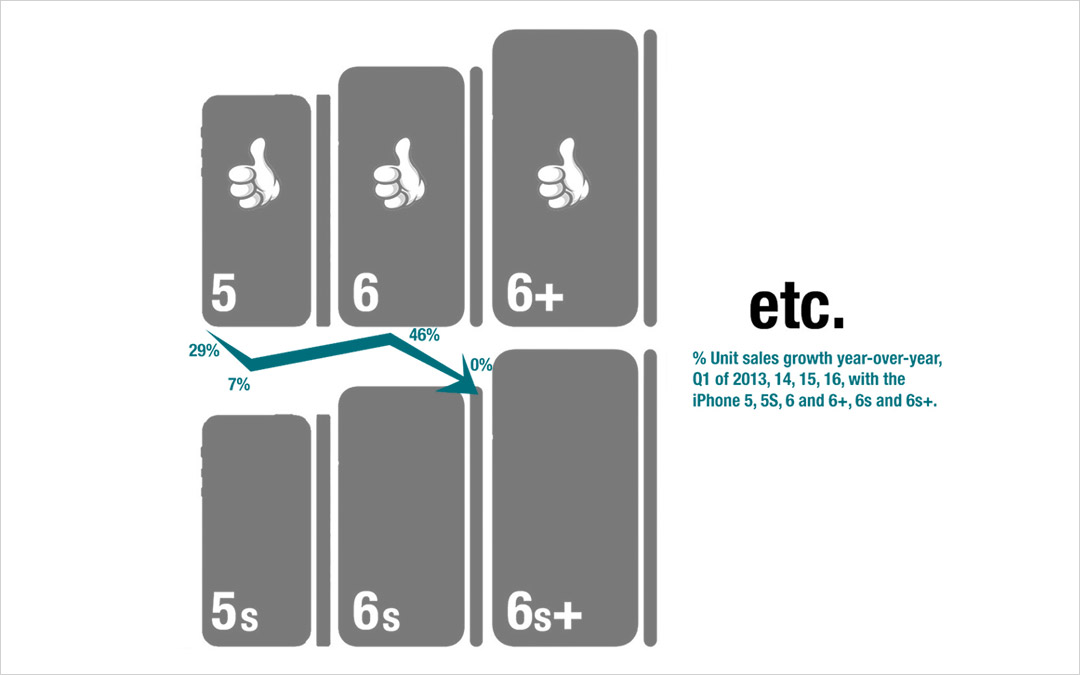

My last column focused on growth, and the risks inherent in a Growth stall. As I mentioned then, Apple will enter a Growth Stall if its revenue declines year-over-year in the current quarter. This forecasts Apple has only a 7% probability of consistently growing just 2%/year in the future.

This usually happens when a company falls into Defend & Extend (D&E) management. D&E management is when the bulk of management attention, and resources, flow into protecting the “core” business by seeking ways to use sustaining innovations (rather than disruptive innovations) to defend current customers and extend into new markets. Unfortunately, this rarely leads to high growth rates, and more often leads to compressed margins as growth stalls. Instead of working on breakout performance products, efforts are focused on ways to make new versions of old products that are marginally better, faster or cheaper.

Using the D&E lens, we can identify what looks like a sea change in Apple’s strategy.

For example, Apple’s CEO has trumpeted the company’s installed base of 1B iPhones, and stated they will be a future money maker. He bragged about the 20% growth in “services,” which are iPhone users taking advantage of Apple Music, iCloud storage, Apps and iTunes. This shows management’s desire to extend sales to its “installed base” with sustaining software innovations. Unfortunately, this 20% growth was a whopping $1.2B last quarter, which was 2.4% of revenues. Not nearly enough to make up for the decline in “core” iPhone, iPad or Mac sales of approximately $9.5B.

Apple has also been talking a lot about selling in China and India. Unfortunately, plans for selling in India were at least delayed, if not thwarted, by a decision on the part of India’s regulators to not allow Apple to sell low cost refurbished iPhones in the country. Fearing this was a cheap way to dispose of e-waste they are pushing Apple to develop a low-cost new iPhone for their market. Either tactic, selling the refurbished products or creating a cheaper version, are efforts at extending the “core” product sales at lower margins, in an effort to defend the historical iPhone business. Neither creates a superior product with new features, functions or benefits – but rather sustains traditional product sales.

Of even greater note was last week’s announcement that Apple inked a partnership with SAP to develop uses for iPhones and iPads built on the SAP ERP (Enterprise Resource Planning) platform. This announcement revealed that SAP would ask developers on its platform to program in Swift in order to support iOS devices, rather than having a PC-first mentality.

This announcement builds on last year’s similar announcement with IBM. Now 2 very large enterprise players are building applications on iOS devices. This extends the iPhone, a product long thought of as great for consumers, deeply into enterprise sales. A market long dominated by Microsoft. With these partnerships Apple is growing its developer community, while circumventing Microsoft’s long-held domain, promoting sales to companies as well as individuals.

And Apple has shown a willingness to help grow this market by introducing the iPhone 6se which is smaller and cheaper in order to obtain more traction with corporate buyers and corporate employees who have been iPhone resistant. This is a classic market extension intended to sustain sales with more applications while making no significant improvements in the “core” product itself.

And Apple’s CEO has said he intends to make more acquisitions – which will surely be done to shore up weaknesses in existing products and extend into new markets. Although Apple has over $200M of cash it can use for acquisitions, unfortunately this tactic can be a very difficult way to actually find new growth. Each would be targeted at some sort of market extension, but like Beats the impact can be hard to find.

Remember, after all revenue gains and losses were summed, Apple’s revenue fell $7.6B last quarter. Let’s look at some favorite analyst acquisition targets to explain:

- Box could be a great acquisition to help bring more enterprise developers to Apple. Box is widely used by enterprises today, and would help grow where iCloud is weak. IBM has already partnered with Box, and is working on applications in areas like financial services. Box is valued at $1.45B, so easily affordable. But it also has only $300M of annual revenue. Clearly Apple would have to unleash an enormous development program to have Box make any meaningful impact in a company with over $500B of revenue. Something akin of Instagram’s growth for Facebook would be required. But where Instagram made Facebook a pic (versus words) site, it is unclear what major change Box would bring to Apple’s product lines.

- Fitbit is considered a good buy in order to put some glamour and growth onto iWatch. Of course, iWatch already had first year sales that exceeded iPhone sales in its first year. But Apple is now so big that all numbers have to be much bigger in order to make any difference. With a valuation of $3.7B Apple could easily afford FitBit. But FitBit has only $1.9B revenue. Given that they are different technologies, it is unclear how FitBit drives iWatch growth in any meaningful way – even if Apple converted 100% of Fitbit users to the iWatch. There would need to be a “killer app” in development at FitBit that would drive $10B-$20B additional annual revenue very quickly for it to have any meaningful impact on Apple.

- GoPro is seen as a way to kick up Apple’s photography capabilities in order to make the iPhone more valuable – or perhaps developing product extensions to drive greater revenue. At a $1.45B valuation, again easily affordable. But with only $1.6B revenue there’s just not much oomph to the Apple top line. Even maximum Apple Store distribution would probably not make an enormous impact. It would take finding some new markets in industry (enterprise) to build on things like IoT to make this a growth engine – but nobody has said GoPro or Apple have any innovations in that direction. And when Amazon tried to build on fancy photography capability with its FirePhone the product was a flop.

- Tesla is seen as the savior for the Apple Car – even though nobody really knows what the latter is supposed to be. Never mind the actual business proposition, some just think Elon Musk is the perfect replacement for the late Steve Jobs. After all the excitement for its products, Tesla is valued at only $28.4B, so again easily affordable by Apple. And the thinking is that Apple would have plenty of cash to invest in much faster growth — although Apple doesn’t invest in manufacturing and has been the king of outsourcing when it comes to actually making its products. But unfortunately, Tesla has only $4B revenue – so even a rapid doubling of Tesla shipments would yield a mere 1.6% increase in Apple’s revenues.

- In a spree, Apple could buy all 4 companies! Current market value is $35B, so even including a market premium $55B-$60B should bring in the lot. There would still be plenty of cash in the bank for growth. But, realize this would add only $8B of annual revenue to the current run rate – barely 25% of what was needed to cover the gap last quarter – and less than 2% incremental growth to the new lower run rate (that magic growth percentage to pull out of a Growth Stall mentioned earlier in this column.)

Such acquisitions would also be problematic because all have P/E (price/earnings) ratios far higher than Apple’s 10.4. FitBit is 24, GoPro is 43, and both Box and Tesla are infinite because they lose money. So all would have a negative impact on earnings per share, which theoretically should lower Apple’s P/E even more.

Acquisitions get the blood pumping for investment bankers and media folks alike – but, truthfully, it is very hard to see an acquisition path that solves Apple’s revenue problem.

All of Apple’s efforts big efforts today are around sustaining innovations to defend & extend current products. No longer do we hear about gee whiz innovations, nor do we hear about growth in market changing products like iBeacons or ApplePay. Today’s discussions are how to rejuvenate sales of products that are several versions old. This may work. Sales may recover via growth in India, or a big pick-up in enterprise as people leave their PCs behind. It could happen, and Apple could avoid its Growth Stall.

But investors have the right to be concerned. Apple can grow by defending and extending the iPhone market only so long. This strategy will certainly affect future margins as prices, on average, decline. In short, investors need to know what will be Apple’s next “big thing,” and when it is likely to emerge. It will take something quite significant for Apple to maintain it’s revenue, and profit, growth.

The good news is that Apple does sell for a lowly P/E of 10 today. That is incredibly low for a company as profitable as Apple, with such a large installed base and so many market extensions – even if its growth has stalled. Even if Apple is caught in the Innovator’s Dilemma (i.e. Clayton Christensen) and shifting its strategy to defending and extending, it is very lowly valued. So the stock could continue to perform well. It just may never reach the P/E of 15 or 20 that is common for its industry peers, and investors envisioned 2 or 3 years ago. Unless there is some new, disruptive innovation in the pipeline not yet revealed to investors.

by Adam Hartung | May 2, 2012 | Defend & Extend, Lock-in, Web/Tech

My latest bi-monthly column for CIO magazine came out in print this week. In it I challenge CIOs to think hard about what made the role successful in the 1970s – then in the 1990s – and how it is transitioning today. Far too many CIOs are locked in on old notions about what made them successful – usually controlling both hardware and software and forcing managers to behave in ways acceptable to IT. But today cloud computing, mobile devices and apps make it possible for many "users" to obviate the IT department entirely – skip the enterprise applications – and find an easy route for their information needs.

I encourage you to click through to the article on CIO.com, or ComputerWorld.com – if you're in IT it should give you something to think about regarding your role. If you are an investor it should give you some new thoughts about what IT companies are worth your money (time to rethink Oracle and SAP, for example.) And if you're a manager it just might embolden you to focus on your needs and fight back on IT solutions that don't work for you.

CIO Mag – http://www.cio.com/article/704934/CIOs_Will_You_Be_Relevant_in_2017_

ComputerWorld – http://www.computerworld.com/s/article/9226722/CIOs_Will_You_Be_Relevant_in_2017_

by Adam Hartung | Aug 24, 2011 | Current Affairs, Defend & Extend, In the Swamp, Innovation, Leadership, Lock-in, Web/Tech

“You’ve got to be kidding me” was the line tennis great John McEnroe made famous. He would yell it at officials when he thought they made a bad decision. I can’t think of a better line to yell at Leo Apotheker after last week’s announcements to shut down the tablet/WebOS business, spin-off (or sell) the PC business and buy Autonomy for $10.2B. Really. You’ve got to be kidding me.

HP has suffered mightily from a string of 3 really lousy CEOs. And, in a real way, they all have the same failing. They were wedded to their history and old-fashioned business notions, drove the company looking in the rear view mirror and were unable to direct HP along major trends toward future markets where the company could profitably grow!

Being fair, Mr. Apotheker inherited a bad situation at HP. His predecessors did a pretty good job of screwing up the company before he arrived. He’s just managing to follow the new HP tradition, and make the company worse.

HP was once an excellent market sensing company that invested in R&D and new product development, creating highly profitable market leading products. HP was one of the first “Silicon Valley” companies, creating enormous shareholder value by making and selling equipment (oscilliscopes for example) for the soon-to-explode computer industry. It was a leader in patent applications, new product launches and being first with products that engineers needed, and wanted.

Then Carly Fiorina decided the smart move in 2001 was to buy Compaq for $25B. Compaq was getting creamed by Dell, so Carly hoped to merge it with HP’s retail PC business and let “scale” create profits. Only, the PC business had long been a commodity industry with competitors competing on cost, and the profits largely going to Intel and Microsoft! The “synergistic” profits didn’t happen, and Carly got fired.

But she paved the way for HPs downfall. She was the first to cut R&D and new product development in favor of seeking market share in largely undifferentiated products. Why file 3,500 patents a year – especially when you were largely becoming a piece-assembly company of other people’s technology? To get the cash for acquisitions, supply chain investments and retail discounts Carly started a whole new tradition of doing less innovation, and spending a lot being a copy-cat.

But in an information economy, where almost all competitors have market access and can achieve highly efficient supply chains at low cost, there was no profit to the volume Carly sought. HP became HPQ – but the price paid was an internal shift away from investing in new markets and innovation, and heading straight toward commoditization and volume! The most valuable liquid in all creation – HP ink – was able to fund a lot of the company’s efforts, but it was rapidly becoming the “golden goose” receiving a paltry amount of feed. And itself entirely off the trend as people kept moving away from printed documents!

Mark Hurd replaced Carly, And he was willing to go her one better. If she was willing to reduce R&D and product development – well he was ready to outright slash it! And all the better, so he could buy other worn out companies with limited profits, declining share and management mis-aligned with market trends – like his 2008 $13.9B acquisition of EDS! Once a great services company, offshore outsourcing and rabid price competition had driven EDS nearly to the point of bankruptcy. It had gone through its own cost slashing, and was a break-even company with almost no growth prospects – leading many analysts to pan the acquisition idea. But Mr. Hurd believed in the old success formula of selling services (gee, it worked 20 years before for IBM, could it work again?) and volume. He simply believed that if he kept adding revenue and cutting cost, surely somewhere in there he’d find a pony!

And patent applications just kept falling. By the end of his cost-cutting reign, the once great R&D department at HP was a ghost of its former self. From 9%+ of revenues on new products, expenditures were down to under 2%! And patent applications had fallen by 2/3rds

Chart Source: AllThingsD.com “Is Innovation Dead at HP?“

The patent decline continued under Mr. Apotheker. The latest CEO intent on implementing an outdated, industrial success formula. But wait, he has committed to going even further! Now, HP will completely evacuate the PC business. Seems the easy answer is to say that consumer businesses simply aren’t profitable (MediaPost.com “Low Margin Consumers Do It Again, This Time to HP“) so HP has to shift its business entirely into the B-2-B realm. Wow, that worked so well for Sun Microsystems.

I guess somebody forgot to tell consumer produccts lacked profits to Apple, Amazon and NetFlix.

There’s no doubt Palm was a dumb acquisition by Mr. Hurd (pay attention Google.) Palm was a leader in PDAs (personal digital assistants,) at one time having over 80% market share! Palm was once as prevalent as RIM Blackberries (ahem.) But Palm did not invest sufficiently in the market shifts to smartphones, and even though it had technology and patents the market shifted away from its “core” and left Palm with outdated technology, products and limited market growth. By the time HP bought Palm it had lost its user base, its techology lead and its relevancy. Mr. Hurd’s ideas that somehow the technology had value without market relevance was another out-of-date industrial thought.

The only mistake Mr. Apotheker made regarding Palm was allowing the Touchpad to go to market at all – he wasted a lot of money and the HP brand by not killing it immediately!

It is pretty clear that the PC business is a waning giant. The remaining question is whether HP can find a buyer! As an investor, who would want a huge business that has marginal profits, declining sales, an extraordinarily dim future, expensive and lethargic suppliers and robust competitors rapidly obsoleting the entire technology? Getting out of PCs isn’t escaping the “consumer” business, because the consumer business is shifting to smartphones and tablets. Those who maintain hope for PCs all think it is the B-2-B market that will keep it alive. Getting out is simply because HP finally realized there just isn’t any profit there.

But, is the answer is to beef up the low-profit “services” business, and move into ERP software sales with a third-tier competitor?

I called Apotheker’s selection as CEO bad in this blog on 5 October, 2010 (HP and Nokia’s Bad CEO Selections). Because it was clear his history as CEO of SAP was not the right background to turn around HP. Today ERP (enterprise resource planning) applications like SAP are being seen for the locked-in, monolithic, buraucracy creating, innovation killing systems they really are. Their intent has always been, and remains, to force companies, functions and employees to replicate previous decisions. Not to learn and do anything new. They are designed to create rigidity, and assist cost cutting – and are antithetical to flexibility, market responsiveness and growth.

But following in the new HP tradition, Mr. Apotheker is reshuffling assets – closing the WebOS business, getting rid of all “consumer” businesses, and buying an ERP company! Imagine that! The former head of SAP is buying an SAP application! Regardless of what creates value in highly dynamic, global markets Mr. Apotheker is implementing what he knows how to do – operate an ERP company that sells “business solutions” while leaving everything else. He just can’t wait to get into the gladiator battle of pitting HP against SAP, Oracle, J.D. Edwards and the slew of other ERP competitors! Even if that market is over-supplied by extremely well funded competitors that have massive investments and enormously large installed client bases!

What HP desperately needs is to connect to the evolving marketplace. Quit looking at the past, and give customers solutions that fit where the market is headed. Customers aren’t moving toward where Apotheker is taking the company.

All 3 of HP’s CEOs have been a testament to just how bad things can go when the CEO is more convinced it is important to do what worked in the past, rather than doing what the market needs. When the CEO is locked-in to old thinking, old market dynamics and old solutions – rather than fixated on understanding trends, future scenarios and the solutions people want and need bad things happen.

There are a raft of unmet needs in the marketplace. For a decade HP has ignored them. Its CEOs have spent their time trying to figure out how to make old solutions work better, faster and cheaper. And in the process they have built large, but not very profitable businesses that are now uninteresting at best and largely at the precipice of failure. They have ignored market shifts in favor of doing more of the same. And the value of HP keeps declining – down 50% this year. For HP to change direction, to increase value, it needs a CEO and leadership team that can understand important trends, fulfill unmet needs and migrate customers to new solutions. HP needs to rediscover innovation.

by Adam Hartung | Jul 28, 2011 | Books, Current Affairs, Defend & Extend, eBooks, In the Rapids, Innovation, Leadership, Television, Web/Tech

“It’s easier to succeed in the Amazon than on the polar tundra” Bruce Henderson, famed founder of The Boston Consulting Group, once told me. “In the arctic resources are few, and there aren’t many ways to compete. You are constantly depleting resources in life-or-death struggles with competitors. Contrarily, in the Amazon there are multiple opportunities to grow, and multiple ways to compete, dramatically increasing your chances for success. You don’t have to fight a battle of survival every day, so you can really grow.”

Today, Amazon(.com) is the place to be. As the financial markets droop, fearful about the economy and America’s debt ceiling “crisis,” Amazon is achieving its highest valuation ever. While the economy, and most companies, struggle to grow, Amazon is hitting record growth:

Source: BusinessInsider.com

Sales are up 50% versus last year! The result of this impressive sales growth has been a remarkable valuation increase – comparable to Apple!

- Since 2009, valuation is up 5.5x

- Over 5 years valuation is up 8x

- Over the last decade Amazon’s value has risen 15x

How did Amazon do this? Not by “sticking to its knitting” or being very careful to manage its “core.” In 2001 Amazon was still largely an on-line book seller.

The company’s impressive growth has come by moving far from its “core” into new markets and new businesses – most far removed from its expertise. Despite its “roots” and “DNA” being in U.S. books and retailing, the company has pioneered off-shore businesses and high-tech products that help customers take advantage of big trends.

Amazon’s earnings release provided insight to its fantastic growth. Almost 50% of revenues lie outside the U.S. Traditional retailers such as WalMart, Target, Kohl’s, Sears, etc. have struggled in foreign markets, and blamed poor performance on weak infrastructure and complex legal/tax issues. But where competitors have seen obstacles, Amazon created opportunity to change the way customers buy, and change the industry using its game-changing technology and capabilities. For its next move, according to Silicon Alley Insider, “Amazon is About to Invade India,” a huge retail market, in an economy growing at over 7%/year, with rising affluence and spendable income – but almost universally overlooked by most retailers due to weak infrastructure and complex distribution.

Amazon’s remarkable growth has occurred even though its “core” business of books has been declining – rather dramatically – the last decade. Book readership declines have driven most independents, and large chains such as B. Dalton and more recently Borders, out of business. But rather than use this as an excuse for weak results, Amazon invested heavily in the trends toward digitization and mobility to launch the wildly successful Kindle e-Reader. Today about half of all Amazon book sales are digital, creating growth where most competitors (hell-bent on trying to defend the old business) have dealt with stagnation and decline.

Amazon did this without a background as a technology company, an electronics company, or a consumer goods company. Additionally, Amazon invested in Kindle – and is now developing a tablet – even as these products cannibalized the historically “core” paper-based book sales. And Amazon has pursued these market shifts, even though these new products create a significant threat to Amazon’s largest traditional suppliers – book publishers.

Rather than trying to defend its old core business, Amazon has invested heavily in trends – even when these investments were in areas where Amazon had no history, capability or expertise!

Amazon has now followed the trends into a leading position delivering profitable “cloud” services. Amazon Web Services (AWS) generated $500M revenue last year, is reportedly up 50% to $750M this year, and will likely hit $1B or more before next year. In addition to simple data storage Amazon offers cloud-based Oracle database services, and even ERP (enterprise resource planning) solutions from SAP. In cloud computing services Amazon now leads historically dominant IT services companies like Accenture, CSC, HP and Dell. By offering solutions that fulfill the emerging trends, rather than competing head-to-head in traditional service areas, Amazon is growing dramatically and avoiding a gladiator war. And capturing big sales and profits as the marketplace explodes.

Amazon created 5,300 U.S. jobs last quarter. Organic revenue growth was 44%. Cash flow increased 25%. All because the company continued expanding into new markets, including not only new retail markets, and digital publishing, but video downloads and television streaming – including making a deal to deliver CBS shows and archive.

Amazon’s willingness to go beyond conventional wisdom has been critical to its success. GeekWire.com gives insight into how Amazon makes these critical resource decisions in “Jeff Bezos on Innovation” (taken from comments at a shareholder meeting June 7, 2011):

- “you just have to place a bet. If you place enough of those bets, and if you place them early enough, none of them are ever betting the company”

- “By the time you are betting the company, it means you haven’t invented for too long”

- “If you invent frequently and are willing to fail, then you never get to the point where you really need to bet the whole company”

- “We are planting more seeds…everything we do will not work…I am never concerned about that”

- “my mind never lets me get in a place where I think we can’t afford to take these bets”

- “A big piece of the story we tell ourselves about who we are, is that we are willing to invent”

If you want to succeed, there are ample lessons at Amazon. Be willing to enter new markets, be willing to experiment and learn, don’t play “bet the company” by waiting too long, and be willing to invest in trends – especially when existing competitors (and suppliers) are hesitant.

by Adam Hartung | Oct 1, 2010 | Current Affairs, Defend & Extend, In the Swamp, Innovation, Leadership, Web/Tech

Summary:

- HP and Nokia have lost the ability to grow organically

- Both need CEOs that can attack old decision-making processes to overcome barriers and move innovation to market much more quickly

- Unfortunately, both companies hired new CEOs who are very weak in these skills

- HP’s new CEO is from SAP – which has been horrible at new product development and introduction

- Nokia’s new CEO is from Microsoft – another failure at developing new markets

- It is unlikely these CEO hires will bring to these companies what is most needed

Leo Apotheker is taking over as CEO of Hewlett Packard today. Formerly he ran SAP. According to MarketWatch.com “HP’s New CEO Has a Lot To Prove,” and investors were less than overwhelmed by the selection, “HP Shares Slip After CEO Appointment.” Rightly so. What was the last exciting new product you can remember from SAP, where Apotheker led the company from 2008 until recently? Well?

SAP is going nowhere good. Its best years are way behind it as the company focuses on defending its installed base and adding new bits to existing products It’s product is amazingly expensive, incredibly hard and expensive to install, and primarily keeps companies from doing anything new. Enterprise software packages are like cement, once you pour them in place nothing can change. They reinforce making the same decision over and over. But increasingly, that kind of management practice is failing. In a fast-changing world software that can take 4 years to install and limits decision-making options doesn’t add to desperately needed organizational agility. And during the last 10 years SAP has done nothing to make its products better linked to the needs of today’s markets.

So why would anyone be excited to see such a leader take over their company? If Apotheker leads HP the way he led SAP investors will see growth decline – not grow. What does this new CEO know about listening carefully to emerging market needs? The move to install SAP in smaller companies hasn’t moved the needle, as SAP remains almost wholly software for stodgy, low-growth, struggly behemoths. What does this CEO know about creating an organization that can moving quickly, create new products and identify market needs to position HP for growth? His experience doesn’t look anything like Steve Jobs, under who’s leadership Apple’s value has increased multi-fold the last decade.

Unfortunately, the same refrain applies at Nokia. Just last week I pointed out in “Another One Bites the Dust” that Nokia was at grave risk of following Blockbuster into bankruptcy court. Although Nokia has 40% worldwide market share in mobile phones, U.S. share has slipped to about 8% this year. In smartphones Nokia has nowhere near the margin of Apple, even though both will sell about the same number of units this year. Nokia once had the lead, but now it is far behind in a market where it has the largest overall share. And that was the problem which befell Motorola – #1 for 3 years early in this decade but now far, far behind competitors in all segments and a very likely candidate for bankruptcy when it spins out a seperate cell phone business.

According to the New York Times in “Nokia’s New Chief Faces a Culture of Complacency” Nokia had a very similar product to the iPhone in 2004 but never took it to market. The internal organization made the new advancement go through several rounds of “review” and the hierarachy simply shot it down in an effort to maintain company focus on the popular, traditional cell phones then being offered. Rather than risk cannibalization, the organization focused on doing more of what it had done well. Eschewing innovation for defending the old products is shown again and again the first step toward disaster. (Would your organization use layers of reviews to kill a new idea in a new market?)

Meanwhile, when an internal Nokia team tried to get approval to launch the smart phones management’s responses sounded like:

- We don’t know much about this technology. The old stuff we do.

- We don’t know how big this new market might be. The old one we do

- We can’t tell if this new product will succeed. Enhanced versions of old products we can predict very accurately.

- We might be too early to market. We know how to sell in the existing market.

Even though Nokia had quite a lead in touch screens, downloadable apps, a good smartphone operating system and even 3-D interfaces, the desire to Defend & Extend the old “core” business overwhelmed any effort to move innovation to market. (By the way, do these comments in any way sound like your company?)

The new CEO, Mr. Elop, is from Microsoft. Again, one of the weakest tech companies out there at launching new products. Microsoft had the smart phone O/S lead just 3 years ago, but lost it to maintain investment in its traditional Windows PC O/S and Office automation software. And again you can ask, exactly how excited have people been with Microsoft’s new products over the last decade? Or you might ask, exactly what new products?

Both HP and Nokia need CEOs ready to attack lock-in to old technologies, old business practices, old hierarchies and old metrics. They need to rejuvenate the companies’ ability to quickly get new products to market, learn and improve. They need experience at early market sensing of unmet needs, and using White Space teams to get products out the door and competitive fast. Both need to overcome traditional management approaches that inhibit growth and move fast to be first into new markets with new products – like Apple and Google.

But in both cases, it appears highly unlikely the Board has hired for what the companies need. Instead, they’ve hired for a stodgy resume. Executive who came from companies that are already in bad positions with limited growth prospects. Exactly NOT what the companies need. We can only hope that somehow both CEOs overcome their historical approaches and rapidly attack existing locked-in decision-making. Otherwise, this will be seen as when investors should have sold their stock and employees should have begun putting resumes on the street!