by Adam Hartung | Jul 14, 2020 | Disruptions, Innovation, Leadership, Marketing, real estate, Retail, Trends

TRENDS: Covid-19 has accelerated a lot of trends. Few more than retail. Oddly some people have taken the view that Covid-19 changed retail. Actually, it didn’t. The pandemic has merely accelerated trends that have been driving industry change for almost two decades.

Back in 2004, Eddie Lampert bought all the bonds of defunct Kmart and used those assets to do a merger with Sears – creating Sears Holdings that encompassed both brands. The day of announcement Chicago Tribune asked for my opinion, and famously I predicted the merger would be a disaster. Clearly both Kmart and Sears were far, far off trends in retail, both were already struggling – and neither had a clue about emerging e-commerce.

Why in 2004 would I predict Sears would fail? The #1 trend in retail was e-commerce, which was all about individualized customer experience, problem solving for customer needs — and only, finally fulfillment. By increasing “scale” – primarily owning a lot more real estate – this new organization would NOT be more competitive. Walmart was already falling behind the growth curve, and everyone in retail was ignoring the elephant in the room – Amazon.com. Loading up on a lot more real estate, more inventory, more employees, more supplier relationships and more community commitments – old ideas about how to succeed related to fulfillment – would hurt more than help. Retail was an industry in transition. All of these factors were boat anchors on future success, which relied on aggressively moving to greater internet use.

Unfortunately, Eddie Lampert as CEO was like most CEOs. He thought success would come from doing more of what worked in the past. Be better, faster, cheaper at what you used to do. In 2011 Sears asked its HQ town (Hoffman Estates) and the state (Illinois) for tax subsidies to keep the HQ there. Sears had built what was once the world’s once tallest building, named the Sears Tower. But many years earlier Sears left, the building was renamed, and Sears was becoming a ghost of itself. I pleaded with government officials to “let Sears go” since the money would be wasted. And it was clear by 2016, that Lampert and his team’s bias toward old retail approaches had only served to hurt Sears more and guarantee its failure. Now – in 2020 – Hoffman Estates has taken the embarrassing act of removing the Sears name from the town’s arena, admitting Sears is washed up.

****

It was with a multi-year observation of trends that I told people in 2/2017 that retail real estate values would crumble . Now mall vacancies are at an 8 year high and 50% of mall department stores will permanently close within a year. We are “over-stored” and nothing will change the fast decline in retail real estate values. Who knows what will happen to all this empty space?

Trends led me in March 2017 to advise investors they should own NO traditional retail equities. Shortly after Sears filed bankruptcy Radio Shack and storied ToysRUs followed. And with the pandemic acting as gasoline fueling change, we’ve now seen the bankruptcies of Neiman Marcus, JCPenney, J Crew, Forever 21, GNC and Chuck e Cheese (but, really, weren’t you a bit surprised the last one was still even in business?) After 3 years of pre-Covid store closings, Industry pundits are finally predicting “record numbers of store closings”. And, after 15 years of predictions, I’m being asked by radio hosts to explain the impact of widespread failures of both local and national retailers ( ). Ignominious ends are abounding in retail. But – it was all very predictable. The trends were obvious years ago. If you were smart, you moved early to avoid asset traps as valuations declined. You also moved early to get on the bandwagon of trend leaders – like Amazon.com – so you too could succeed.

Ignominious ends are abounding in retail. But – it was all very predictable. The trends were obvious years ago. If you were smart, you moved early to avoid asset traps as valuations declined. You also moved early to get on the bandwagon of trend leaders – like Amazon.com – so you too could succeed.

As we move forward, what will happen to your business? Will you build on trends to create a new future where growth abounds? Will you align your strategy with the future so you “skate to where the puck will be?” Or will you – like Sears and so many others – find an ignominious end to your organization? Will the signs change, or will the signs come down? The trends have never been stronger, the markets have never moved faster and the rewards have never been greater. It’s time to plan for the future, and build your strategy on trends (not what worked in the past.)

But don’t lose sight of the lesson. TRENDS MATTER. If you align with trends your business can do GREAT! Like Facebook. But if you don’t pay attention, and you miss a big trend (like demographic inclusion) the pain the market can inflict can be HUGE and FAST. Like Facebook. Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business (https://adamhartung.com/assessments/)

Give us a call or send an email. Adam @Sparkpartners.com

by Adam Hartung | Jun 5, 2018 | Investing, Retail, Strategy, Trends, Web/Tech

The US e-commerce market is just under 10% the size of entire retail market. On the face of it this would indicate that the game is far from over for big traditional retail. After all, how could such a small segment kill profits for such a huge industry based on enormous traditional players?

Yet, Sears – once a Dow Jones component and the world’s most powerful retailer – has announced it will close 100 more stores. The Kmart/Sears chain is now only 894 stores – down from thousands at its peak and 1,275 just last year. Revenue dropped 30% versus a year ago, and quarterly losses of $424M were almost 15% of revenues.

But, that ignores marginal economics. It often doesn’t take a monster change in one factor to have a huge impact on the business model. Let’s say Sales are $100. Less Cost of Goods sold of $75. That leaves a Gross Margin of $25. Selling, General and Administrative costs are 20%, so Operating Income is only $5. The Net Margin before Interest and Taxes is 5%. (BTW, these are the actual percentages of Walmart from 1/31/18.)

Now, in comes a new competitor – like Amazon.com. They have no stores, no store clerks, and minimal inventory due to “e-storefront” selling. So, they are able to lower prices by 5%. That seems pretty small – just a 5% discount compared to typical sales of 20%, 30% even 50% (BOGO) in retail stores. Amazon’s 5% price reduction seems like no big deal to established firms.

But, Walmart has to lower prices by 5% in response, which lowers revenues to $95. But the stores, clerks, inventory, distribution centers and trucks all largely remain. With Cost of Goods Sold still $75, Gross Margin falls to $20. Fixed headquarters costs, general and administrative costs don’t change, so they remain at $20. This leaves Operating Income of …$0.

(For more detailed analysis see “Bigger is Not Always Better – Why Amazon is Worth More than Walmart” from July, 2015.)

How can Walmart survive with no profits? It can’t. To get some margin back, Walmart has to start shutting stores, selling assets, cutting pay, using automation to cut headcount, beating on vendors to offer them better prices. This earns praise as “a low cost operation.” When in fact, this makes Walmart a less competitive company, because it’s footprint and service levels decline, which encourages people to do more shopping on-line. A vicious circle begins of trying to recapture lost profitability, while sales are declining rather than growing.

Walmart was (and is) huge. Even Sears was much bigger than Amazon.com at the beginning. But to compete with Amazon.com both had to lower prices on ALL of their products in ALL of their stores. So the hit to Walmart’s, and Sears’, revenue is a huge number. Though Amazon.com was a much, much smaller company, its impact explodes on the larger competitor P&L’s.

This disruption is felt across the entire industry: ALL traditional retailers are forced to match Amazon and other e-commerce companies, even though there is no way they can cut costs enough to compete. Thus, Toys-R-Us, Radio Shack, Claire’s and Bon-Ton have declared bankruptcy in 2018, and the once great, dominant Sears is on the precipice of extinction.

All of which is good news for Amazon.com investors. Amazon.com has 40% market share of the entire e-commerce business. The fact that e-commerce is only 10% of all retail is great news for Amazon investors. That means there is still an enormously large market of traditional retail available to convert to on-line sales.

The shift to e-commerce will not be stopping, or even slowing. Since January, 2010 the future has been easily predictable for traditional retail’s decline. The next few years will see a transition of an additional $2.5 trillion on-line, which is 5X the size of the existing e-commerce market!

As stores close new competitors will emerge in the e-commerce market. But undoubtedly the big winner will be the company with 40% market share today – Amazon.com. So what will Amazon’s stock be worth when sales are 5x larger (or more) and Amazon can increase profits by making leveraging its infrastructure and slow future investments?

Twenty years ago, Amazon was a retail ant. And retail elephants ignored it. But that was foolish, because Amazon had a different business model with an entirely different cost of operations. And now the elephants are falling fast, due to their inability to adapt to new market conditions and maintain their growth.

_________________________________________________________________________

Author’s Note: In June, 2007 I was asked to predict WalMart’s future. Here are the predictions I made 11 years ago:

- “In 5 years (2012) Walmart would not have succeeded internationally” [True: Mexico, China, Germany all failed]

- “In 5 years (2012) Walmart would no new businesses, and its revenue will be stalled” [True]

- In 5 years (2012) Walmart would be spending more on stock repurchases then investing in its own stores or distribution” [True – and the Walton’s were moving money out of Walmart to other investments]

- “In 10 years (2017) Walmart would take a dramatic act, and make an acquisition” [True: Jet.com]

- “In 10 years (2017 Walmart’s value would not keep up with the stock market” [from 6/2007 to 6/2017 WMT went from $48 to $75 up 56.25%, DIA went from $134 to $180 up 34.3%, AMZN went from $70 to $1,000 up 1,330% or 13.3x]

- “In 30 years (2037) Walmart will only be known as “a once great company, like General Motors”

by Adam Hartung | Mar 6, 2018 | In the Swamp, Investing, Retail, Scenario Planning

On February 20, 2018 Walmart’s stock had its biggest price drop ever. And the second biggest percentage decline ever. Even though same store sales improved, investors sold off the stock in droves. And after a pretty healthy recent valuation run-up.

What happened? Simply put, Walmart said its on-line sales slowed and its cost of operations rose, slowing growth and cramping margins. In other words, even though it bought Jet.com Walmart is still a long, long way from coming close to matching the customer relationship and growth of Amazon.com. And (surprise, surprise) margins in on-line aren’t an easy thing — as Amazon’s thin margins for 15 years have demonstrated.

In other words, this was completely to be expected. Walmart is a behemoth with no adaptability. For decades the company has been focused on how to operate its warehouses and stores, and beat up its suppliers. Management had to be drug, kicking and screaming, into e-commerce. And failing regularly it finally made an acquisition. But to think that Jet.com was going to change WalMart’s business model into a growing, high profit operation any time soon was foolish. Management still wants people in the store, first and foremost, and really doesn’t understand how to do anything else.

All the way back in 2005, I wrote that Walmart was too big to learn, and was unwilling to create white space teams to really explore growing e-commerce (hence the belated Jet-com acquisition.) In 2007, I wrote that calling Walmart a “mature” competitor with huge advantages was the wrong way to view the company already under attack by all the e-commerce players. In July, 2015 Amazon’s market cap exceeded Walmart’s, showing the importance of retail transformation on investor expectations. By February, 2016 there were 10 telltale signs Walmart was in big trouble by a changing retail market. And by October, 2017 it was clear the Waltons were cashing out of Walmart, questioning why any investor should remain holding the stock.

It really is possible to watch trends and predict future markets. And that can lead to good predictions about the fates of companies. The signs were all there that Walmart shouldn’t be going up in value. Hope had too many investors thinking that Walmart was too big to stumble – or fail. But hope is not how you should invest. Not for your portfolio, and not for your business. Walmart should have dedicated huge sums to e-commerce 15 years ago, now it is playing catch up with Amazon.com, and that’s a race it simply won’t win. Are you making the right investment decisions for your business early enough? Or will you stumble like Walmart?

by Adam Hartung | Jan 23, 2018 | Disruptions, Investing, Retail, Trends

Business Insider is projecting a “tsunami” of retail store closings in 2018 — 12,000 (up from 9,000 in 2017.) Also, the expect several more retailers will file bankruptcy, including Sears.

Duh. Nothing surprising about those projections. In mid-2016, Wharton Radio interviewed me about Sears, and I made sure everyone clearly understood I expect it to fail. Soon. In December, 2016 I overviewed Sears’ demise, predicted its inevitable failure, and warned everyone that all traditional retail was going to get a lot smaller. I again recommended dis-investing your portfolio of retail. By March, 2017 the handwriting was so clear I made sure investors knew that there were NO traditional retailers worthy of owning, including Walmart. By October, 2017 I wrote about the Waltons cashing out their Walmart ownership, indicating nobody should be in the stock – or any other retailer.

The trend is unmistakable, and undeniable. The question is – what are you going to do about it? In July, 2015 Amazon became more valuable than Walmart, even though much smaller. I explained why that made sense – because the former is growing and the latter is shrinking. Companies that leverage trends are always worth more. And that fact impacts YOU! As I wrote in February, 2017 the “Amazon Effect” will change not only your investments, but how you shop, the value of retail real estate (and thus all commercial real estate,) employment opportunities for low-skilled workers, property and sales tax revenues for all cities impacting school and infrastructure funding, and all supply chain logistics. These trends are far-reaching, and no business will be untouched.

Don’t just say “oh my, retailers are crumbling” and go to the next web page. You need to make sure your strategy is leveraging the “Amazon Effect” in ways that will help you grow revenues and profits. Because your competition is making plans to use these trends to hurt your business if you don’t make the first move. Need help?

by Adam Hartung | Sep 21, 2017 | Investing, Trends

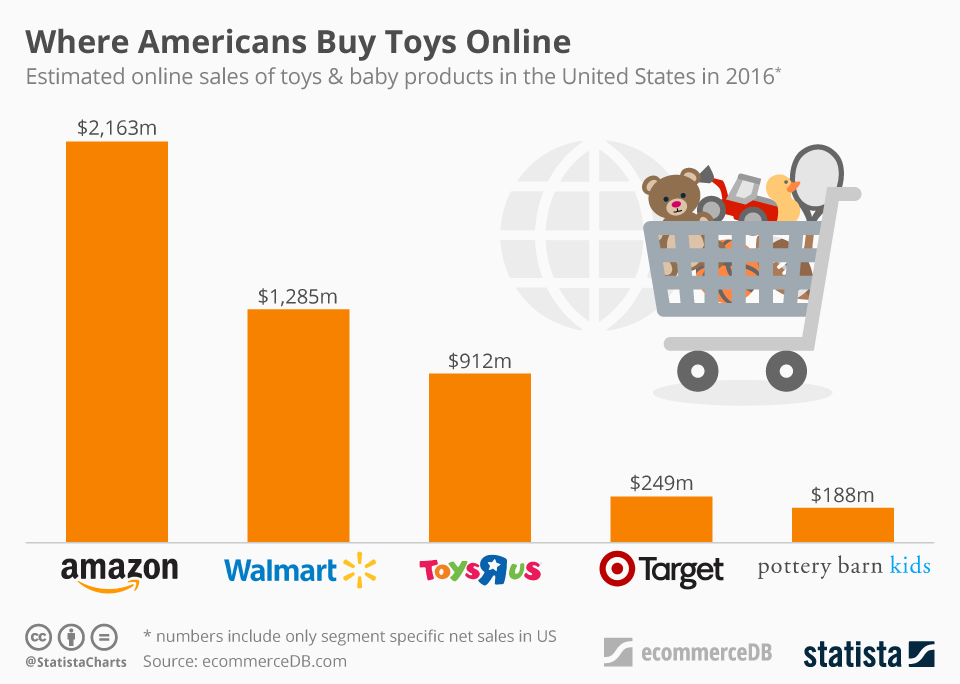

Toys R Us filed for bankruptcy this week. And the obvious response was “another retailer slaughtered by Amazon and on-line retailing.” But this conclusion comes short of describing why Toys R Us leadership did not do the obvious things to keep Toys R Us relevant.

Amazon and WalMart both eclipsed Toys R Us in toy retail sales.

Chart courtesy of Felix Richter, Statista

Everyone, and I mean everyone, knew over the last decade that customers were buying more stuff on-line, including toys. And everyone also knew that WalMart was pushing extremely hard to keep customers going to their stores by offering products like toys at low prices. And, it was clear that customers were shifting to buying more toys from both these retailers. If this was so obvious to everyone, why didn’t Toys R Us leadership do something? After all, Toys R Us is a multi-billion dollar revenue company.

It was over 30 years ago when financiers discovered they could buy a company, sell off some assets and otherwise increase the company’s cash, then convince banks and bondholders to load the company with debt. These financiers would then pull out the cash for themselves, and leave the company with a ton of debt. The LBO (leveraged buy out) was born, invented by investment bankers like KKR (named for founders Kohlberg, Kravis & Roberts.) They would use a small bit of private equity, and then use the company’s own assets to raise debt money (leverage) to buy the company. By “restructuring” the company to a lower cost of operations, usually with draconian reductions, they would increase cash flow to make higher debt repayments. Then they would either take the money out directly, or take the company public where they could sell their shares, and make themselves rich. This form of deal making birthed what we now call the Private Equity business.

In 2005, KKR and Bain Capital (which included former Presidential candidate Mitt Romney) bought Toys R Us for about $6.6billion, plus assuming just under $1B of debt, for a total valuation of $7.5billion. But the private equity guys didn’t buy the company with equity. They only put in $1.3billion, and used the company’s assets to raise $5.3billion in additional debt, making total debt a whopping $6.2B. Total debt was now a remarkable 82.7% of total capital! At the time of the deal interest rates on that debt were around 7.25%, creating a cash outflow of $450million/year just to pay interest on the loans. At the time Toys R Us was barely making a profit of 2% – so the debt was double company net profits.

Debt led to bad management decisions and ultimately bankruptcy of the U.S. company

The biggest assumption behind a debt-financed takeover is that the company can cut costs to improve cash flow and thus pay the interest. But behind that assumption is an even bigger assumption. That the marketplace won’t change dramatically. The KKR and Bain Capital leaders assumed they could shrink Toys R Us in a way that would lower operating costs. They also assumed they could sell some under-utilized assets to raise cash. They did not assume they would need contingency money if competition, and the marketplace, changed in some unplanned way.

eCommerce was pretty new in 2005. Amazon was an $8.5 billion company, but it didn’t make any profits and very few predicted then it would become today’s $100 billion behemoth. Because the financiers didn’t anticipate a big market shift to ecommerce, they focused on the war with Walmart and Target. Their plans were to lower operating costs, close some stores that were underperforming, license some offshore stores, and sell some assets (like real estate owned or leases) to raise cash and repay the debt.

But they weren’t prepared to take on another, entirely different competitor on-line. As Amazon’s growth affected all retailers, Toys R Us simply did not have the resources to fight the traditional discount and dollar brick-and-mortar retailers, and build a major on-line presence, and keep paying that debt. While it is easy to sit on the sidelines and say that Toys R Us should have spent more money building its on-line presence in order to remain relevant, the fact is that the deal in 2005 left the company with insufficient cash flow to do so. Regardless of what leadership might have wanted to do, simply keeping the lights on was a tough challenge when having to pay out so much cash to bondholders.

And the investors simply did not expect that the growth of on-line retailing would stall traditional retail stores, thus creating a major loss of value for retail real estate. U.S. retail real estate value had increased in value for decades. The assumption was that the real estate, whether owned or leased, would continue to go up in value. Real estate was a “hard” asset that KKR and Bain Capital could bank on for raising cash to repay the debt. But as on-line retail grew, and traditional retail declined, America became “over stored” with far too much retail space. Prices were shattered in many markets, and it was not possible for Toys R Us to sell those assets for a gain that would meet the debt obligations.

With $400 million of debt coming due next year, Toys R Us simply doesn’t have the cash flow, or assets, to repay those bondholders

Old assumptions about finance are a big problem for companies today. Assumptions about “leveraging” hard assets, and intangibles like brand value, are no longer true. Competitors emerge, markets change, and old assets can lose value very fast. Assumptions about business model stability are no longer true, as new competitors using newer technology create new ways to sell, and often at lower cost than was ever expected. Assumptions about customer loyalty, and market share stability, are no longer true as new competitors appeal to customers differently and cause big shifts in buying behavior very fast. The speed with which technology, competitors, markets and customers shift now requires companies have the funds available to invest in change.

This story isn’t just about debt. The very popular activity of “returning money to shareholders by repurchasing stock” is a terrible idea. Stock repurchases do not make a company more valuable, nor a stronger competitor. Instead they burn through cash to reduce the company’s capitalization, and manipulate ratios like EPS (earnings per share) and P/E (price/earnings) multiple. Stock repurchases hurt companies, and make them less competitive. Good companies return money to shareholders by investing in growth, which raises sales, profits and increases the stock price making the company truly more valuable.

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

The important part of the Toys R Us story is realizing that the wrong financial decisions can doom your organization. You can have a great vision, and even great ideas about new ways to compete. But if you don’t have the money to invest in growth, it won’t happen. If leaders don’t have the money to spend on new projects and new markets, because they’re sending it all to bondholders or using it to repurchase shares in hopes of propping up a stock price, eventually there will be a market shift that will doom the old business model and leave it unable to compete.

To succeed today leaders need the money to invest in change, and they have to constantly invest it in change, or their companies will lose relevancy and end up like Toys R Us, Radio Shack, Circuit City, Aeropostale, The Limited, Payless Shoes, Gander Mountain, Golfsmith, Sports Authority, Borders Books and the great, original American retailer A&P.

Ignominious ends are abounding in retail. But – it was all very predictable. The trends were obvious years ago. If you were smart, you moved early to avoid asset traps as valuations declined. You also moved early to get on the bandwagon of trend leaders – like Amazon.com – so you too could succeed.

Ignominious ends are abounding in retail. But – it was all very predictable. The trends were obvious years ago. If you were smart, you moved early to avoid asset traps as valuations declined. You also moved early to get on the bandwagon of trend leaders – like Amazon.com – so you too could succeed.