Do you have any idea how powerful AOL and Yahoo once were, and how much they were once worth? Do you know how much shareholder value has been destroyed in these 2 companies in just 20 years? $221 Billion of destroyed wealth.

AOL pioneered the web as we know it today. Long before wireless, or broadband, there was “dial up service.” For young readers, that meant using a physical modem to connect your computer to a land-line telephone in order to literally dial up a connection to an internet service provider. AOL pioneered using the internet, and was the #1 connection with almost the entire marketplace. The phrase that made AOL famous back then was when you connected to AOL and it gave us the now iconic “You’ve got mail.” After connecting America, in 2000 AOL merged with Time Warner media in a deal valuing AOL at $111B.

Yahoo pioneered giving internet users news. It accumulated news from around the world on Sports, Economy and many other topics, making the news available to readers for free because it sold ads to pay the bills. In 2000 a publicly traded Yahoo was valued at $125B.

So in 2000, amidst a very extended NASDAQ internet hype, AOL and Yahoo were valued at $226B.

This week Verizon agreed to sell the two companies to a private equity firm for $5B. That’s a loss in value of $221B in 21 years.

How does a loss of this magnitude happen? A lot of focusing on tactics, ignoring market trends and failing to adapt the company strategy to meet changing competitive dynamics. Broadband and wireless eventually made dial-up irrelevant. And despite buying some media company to try and add new content to AOL, it lost all meaning. Time Warner spun it out to the public at a value of $3.5B in 2009.

Then, Verizon thought it could build a proprietary content company to get more Verizon customers so it bought AOL in 2015 for $4.4B. Only, nobody needed another content provider by then. Google served up general content just fine, Facebook gave us content we looked at frequently, and specialized content sites like Finance (Marketwatch) and Sports (ESPN) made it impossible that late in the game to launch a general purpose content accumulator and reposter. It was a strategy for 2005, not 2015. Meanwhile, Yahoo made one tactical decision after another to shore up its old model that didn’t work. Google became vastly better at search, and vastly better at delivering content. Tactical oriented CEOs Carol Bartz and Marissa Mayer had no strategy to meet emerging needs of the 2010 decade and beyond – leading Yahoo into complete irrelevancy.

Undeterred, the Verizon owned AOL bought Yahoo in 2017 for $4.5B. After all, it seemed cheap compared to its once $125B value – right? The idea was to merge the two companies, create “cost synergies” and “scale” in users to sell more advertising. Only, neither platform had enough original content to stop the user bleed to other sites. Netflix and Google’s YouTube took everyone who wanted new content away, and there was nothing left for AOL/Yahoo to deliver. It became the internal combustion engine repair shop in a world full of EVs

Now, after spending $9.9B on the entities plus much more in acquisitions, Verizon is selling both entities to Apollo Global Management private equity for $5B – a loss of $4.4B. And Apollo thinks this is a good deal because “a high tide raises all boats” and it will win merely because the world is increasingly using the internet. Really? More people are using the web, and more often, but they’ve already shown not via AOL nor Yahoo. Facebook, Instagram, Google, Pinterest, Twitter, and a raft of other sites are gaining the traffic. What was once irrelevant remains irrelevant.

It is crucial to understand why these to GIANTS of the internet are now part of history’s dustbin. While they pioneered the market, gaining huge revenues, share and valuation, they did NOT keep their eyes on disruptive innovators who could change the market they pioneered. Broadband killed dial-up, and because AOL moved too late it died. Google overtook search, delivering more content faster and better, and Yahoo simply waited too long to react. Not unlike how Research in Motion (Blackberry) failed to see the “app wave” in mobile coming and lost its enormous lead in mobile phones to Apple and Samsung. All thought their strength in pioneering was enough – and failed to keep their eyes on external trends and new market shifts that would change competition.

I wrote a raft of columns about the mistakes made by these company CEOs from 2009 through 2017 – constantly telling readers not to buy the stocks (just search the blogs my website adamhartung.com for AOL or Yahoo.) It is extremely rare for a corporation locked into its business model and cost cutting to adjust to a rapidly shifting market. When a company does so – like Jobs turned around Apple and Nadella at Microsoft – it is the exception to be well applauded. But that is very, very rare.

And this is NOT what PE companies do. They aren’t visionary investors who put in lots of money to change companies. They cut costs, streamline operations, and add debt to get their investment back. Apollo is no different. It has no vision of the internet future that will slow Facebook, Apple, Netflix, Alphabet/Google or even Amazon. It has purchased two irrelevant brands with outdated business models, no new technology, no new market approaches and no new insight to future unmet needs. There is no doubt Apollo will not turn these around. Apollo will unload this newest Yahoo! over-leveraged to a public debt market dominated by pension funds and it will soon enough file bankruptcy, finishing the coffin.

Do you think you could turn these around? First, are you ready to turn around your own business? Are you focused on how market shifts, happening today, will change your market? Are you seeing trends, and changing your business model and technology to adjust? Are you building a business around future scenarios you’ve created to compete in 2025 and beyond with different competitors offering different solutions? Or are you relying on past strengths to carry you through the future? If you’re planning with your eyes firmly in the rear view mirror I highly recommend you learn the lesson from AOL and Yahoo – that approach will not work.

Do you know your Value Proposition? Can you clearly state that Value Proposition without any linkage to your Value Delivery System? If not, you better get on that pretty fast. Otherwise, you’re very likely to end up like encyclopedias and newspaper companies. Or you’ll develop a neat technology that’s the next Segway. It’s always know your customer and their needs first, then create the solution. Don’t be a solution looking for an application. Hopefully Uber and Aurora will both now start heading in the right directions.

Did you see the trends, and were you expecting the changes that would happen to your demand? It IS possible to use trends to make good forecasts, and prepare for big market shifts. If you don’t have time to do it, perhaps you should contact us, Spark Partners. We track hundreds of trends, and are experts at developing scenarios applied to your business to help you make better decisions.

TRENDS MATTER. If you align with trends your business can do GREAT! Are you aligned with trends? What are the threats and opportunities in your strategy and markets? Do you need an outsider to assess what you don’t know you don’t know? You’ll be surprised how valuable an inexpensive assessment can be for your future business. Click for Assessment info.Or, to keep up on trends, subscribe to our weekly podcasts and posts on trends and how they will affect the world of business at www.SparkPartners.com

Give us a call or send an email. Adam@sparkpartners.com 847-726-8465.

Few businesses fail in a fiery, quick downfall. Most linger along for years, not really mattering to anyone – including customers, suppliers or even investors. They exist, but they aren’t relevant.

When a company is relevant customers are eager for new product releases, and excited to talk to salespeople. Media want to report on the company, its products and its leaders. Investors want to hear about what the company will do next to drive revenues and increase profits.

But when a company loses relevancy, that all disappears. Customers quit paying attention to new products, and salespeople are not given the time of day. The company begs for coverage of its press releases, but few media outlets pay attention because writing about that company produces few readers, or advertisers. Investors lose hope for big gains, and start looking for ways to sell the stock or debt without taking too big a loss, or further depressing valuations.

In short, when a company loses relevancy it is on the downward slope to failure. It may take a long time, but lacking market relevancy the company has practically no hope of increasing revenues or profits, or of creating many new and exciting jobs, or of being a great customer for suppliers. Losing relevancy means the company is headed out of business, it’s just a matter of time. Think Howard Johnson’s, ToysRUs, Sears, Radio Shack, Palm, Hostess, Samsonite, Pierre Cardin, Woolworth’s, International Harvester, Zenith, Sony, Rand McNally, Encyclopedia Britannica, DEC — you get the point.

Many people may not be aware that Microsoft made an exclusive deal with the NFL to provide Surface tablets for coaches and players to use during games, replacing photographs, paper and clipboards for reviewing on-field activities and developing plays. The goal was to up the prestige of Surface, improve its “cool” factor, while showing capabilities that might encourage more developers to write apps for the product and more businesses to buy it.

But things could not have gone worse during the NFL’s launch. Because over and again, announcers kept calling the Surface tablets iPads. Announcers saw the tablet format and simply assumed these were iPads. Or, worse, they did not realize there was any tablet other than the iPad. As more and more announcers made this blunder it became increasingly clear that Apple not only invented the modern tablet marketplace, but that it’s brand completely dominates the mindset of users and potential buyers. iPad has become synonymous with tablet for most people.

In a powerful way, this demonstrates the lack of relevancy Microsoft now has in the personal technology marketplace. Fewer and fewer people are buying PCs as they rely increasingly on mobile devices. Practically nobody cares any more about new releases of Windows or Office. In fact, the American Customer Satisfaction Index reported people think Apple is now considered the best PC maker (the Macintosh.) HP was near the bottom of the list, with Dell, Acer and Toshiba not faring much better.

There are many people who cannot imagine a world without Microsoft. And the vast majority of people would think that predicting Microsoft’s demise is considerably premature given its size and cash hoard. But, that looks backward at what Microsoft was, and the assets it previously created, rather than looking forward.

The complete lack of relevancy was exposed last week when Blackberry launched its new Passport phone alongside Apple’s iPhone 6 actions. While the press was full of articles about the new iPhone, were you even aware of Blackberry’s most recent effort? Did you recall seeing press coverage? Did you read any product reviews? And while Apple was selling record numbers, Blackberry analysts were wondering if the Passport could find a niche with “nostalgic customers” that would sell enough units to keep the company’s hardware unit alive. Reviewers now compare Passport to the market standard, which is the iPhone – and still complain that its use of apps is “confusing.” In a world where most people use their own smartphone, the only reason most people could think of to use a Passport was if their employer told them they were forced to.

Like with Radio Shack, most people have to be reminded that Blackberry still exists. In just a few years Blackberry’s loss of relevancy has made the company and its products a backwater. Now it is quite clear that Microsoft is entering a similar situation. Windows 8 was a weak launch and did nothing to slow the shift to mobile. Microsoft missed the mobile market, and its mobile products are achieving no traction. Even where it has an exclusive use, such as this NFL application, people don’t recognize its products and assume they are the products of the market leader. Microsoft really has become irrelevant in its historical “core” personal technology market – and that should scare its employees and investors a lot.

Can you believe it has been only 12 years since Apple introduced the iPod? Since then Apple’s value has risen from about $11 (January, 2001) to over $500 (today) – an astounding 45X increase.

With all that success it is easy to forget that it was not a “gimme” that the iPod would succeed. At that time Sony dominated the personal music world with its Walkman hardware products and massive distribution through consumer electronics chains such as Best Buy, and broad-line retailers like Wal-Mart. Additionally, Sony had its own CD label, from its acquisition of Columbia Records (renamed CBS Records,) producing music. Sony’s leadership looked impenetrable.

But, despite all the data pointing to Sony’s inevitable long-term domination, Apple launched the iPod. Derided as lacking CD quality, due to MP3’s compression algorithms, industry leaders felt that nobody wanted MP3 products. Sony said it tried MP3, but customers didn’t want it.

All the iPod had going for it was a trend. Millions of people had downloaded MP3 songs from Napster. Napster was illegal, and users knew it. Some heavy users were even prosecuted. But, worse, the site was riddled with viruses creating havoc with all users as they downloaded hundreds of millions of songs.

Eventually Napster was closed by the government for widespread copyright infreingement. Sony, et.al., felt the threat of low-priced MP3 music was gone, as people would keep buying $20 CDs. But Apple’s new iPod provided mobility in a way that was previously unattainable. Combined with legal downloads, including the emerging Apple Store, meant people could buy music at lower prices, buy only what they wanted and literally listen to it anywhere, remarkably conveniently.

The forecasted “numbers” did not predict Apple’s iPod success. If anything, good analysis led experts to expect the iPod to be a limited success, or possibly failure. (Interestingly, all predictions by experts such as IDC and Gartner for iPhone and iPad sales dramatically underestimated their success, as well – more later.) It was leadership at Apple (led by the returned Steve Jobs) that recognized the trend toward mobility was more important than historical sales analysis, and the new product would not only sell well but change the game on historical leaders.

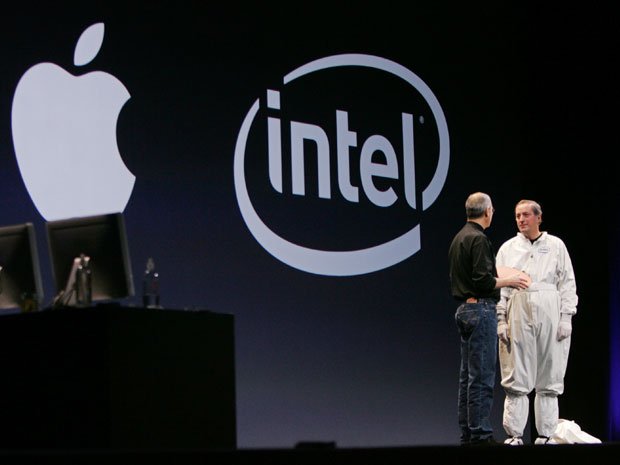

Which takes us to the mistake Intel made by focusing on “the numbers” when given the opportunity to build chips for the iPhone. Intel was a very successful company, making key components for all Microsoft PCs (the famous WinTel [for Windows+Intel] platform) as well as the Macintosh. So when Apple asked Intel to make new processors for its mobile iPhone, Intel’s leaders looked at the history of what it cost to make chips, and the most likely future volumes. When told Apple’s price target, Intel’s leaders decided they would pass. “The numbers” said it didn’t make sense.

Uh oh. The cost and volume estimates were wrong. Intel made its assessments expecting PCs to remain strong indefinitely, and its costs and prices to remain consistent based on historical trends. Intel used hard, engineering and MBA-style analysis to build forecasts based on models of the past. Intel’s leaders did not anticipate that the new mobile trend, which had decimated Sony’s profits in music as the iPod took off, would have the same impact on future sales of new phones (and eventually tablets) running very thin apps.

Harvard innovation guru Clayton Christensen tells audiences that we have complete knowledge about the past. And absolutely no knowledge about the future. Those who love numbers and analysis can wallow in reams and reams of historical information. Today we love the “Big Data” movement which uses the world’s most powerful computers to rip through unbelievable quantities of historical data to look for links in an effort to more accurately predict the future. We take comfort in thinking the future will look like the past, and if we just study the past hard enough we can have a very predictible future.

But that isn’t the way the business world works. Business markets are incredibly dynamic, subject to multiple variables all changing simultaneously. Chaos Theory lecturers love telling us how a butterfly flapping its wings in China can cause severe thunderstorms in America’s midwest. In business, small trends can suddenly blossom, becoming major trends; trends which are easily missed, or overlooked, possibly as “rounding errors” by planners fixated on past markets and historical trends.

Markets shift – and do so much, much faster than we anticipate. Old winners can drop remarkably fast, while new competitors that adopt the trends become “game changers” that capture the market growth.

In 2000 Apple was the “Mac” company. Pretty much a one-product company in a niche market. And Apple could easily have kept trying to defend & extend that niche, with ever more problems as Wintel products improved.

But by understanding the emerging mobility trend leadership changed Apple’s investment portfolio to capture the new trend. First was the iPod, a product wholly outside the “core strengths” of Apple and requiring new engineering, new distribution and new branding. And a product few people wanted, and industry leaders rejected.

Then Apple’s leaders showed this talent again, by launching the iPhone in a market where it had no history, and was dominated by Motorola and RIMM/BlackBerry. Where, again, analysts and industry leaders felt the product was unlikely to succeed because it lacked a keyboard interface, was priced too high and had no “enterprise” resources. The incumbents focused on their past success to predict the future, rather than understanding trends and how they can change a market.

Then Apple did it again. Years after Microsoft attempted to launch a tablet, and gave up, Apple built on the mobility trend to launch the iPad. Analysts again said the product would have limited acceptance. Looking at history, market leaders claimed the iPad was a product lacking usability due to insufficient office productivity software and enterprise integration. The numbers just did not support the notion of investing in a tablet.

Anyone can analyze numbers. And today, we have more numbers than ever. But, numbers analysis without insight can be devastating. Understanding the past, in grave detail, and with insight as to what used to work, can lead to incredibly bad decisions. Because what really matters is vision. Vision to understand how trends – even small trends – can make an enormous difference leading to major market shifts — often before there is much, if any, data.

Microsoft needed a great Christmas season. After years of product stagnation, and a big market shift toward mobile devices from PCs, Microsoft's future relied on the company seeing customers demonstrate they were ready to jump in heavily for Windows8 products – including the new Surface tablet.

Looking deeper, for the 4th quarter PC sales declined by almost 5% according to Gartner research, and by almost 6.5% according to IDC. Both groups no longer expect a rebound in PC shipments, as they believe homes will no longer have more than 1 PC due to the mobile device penetration – the market where Surface and Win8 phones have failed to make any significant impact or move beyond a tiny market share. Users increasingly see the complexity of shifting to Win8 as not worth the effort; and if a switch is to be made consumer and businesses now favor iOS and Android.

These trends mean nothing short of the ruin of Microsoft. Microsoft makes more than 75% of its profits from Windows and Office. Less than 25% comes from its vaunted servers and tools. And Microsoft makes nothing from its xBox/Kinect entertainment division, while losing vast sums on-line (negative $350M-$750M/quarter). No matter how much anyone likes the non-Windows Microsoft products, without the historical Windows/Office sales and profits Microsoft is not sustainable.

So what can we expect at Microsoft:

Ballmer has committed to fight to the death in his effort to defend & extend Windows. So expect death as resources are poured into the unwinnable battle to convert users from iOS and Android.

As resources are poured out of the company in the Quixotic effort to prolong Windows/Office, any hope of future dividends falls to zero.

Expect enormous layoffs over the next 3 years. Something like 50-60%, or more, of employees will go away.

Expect closure of the long-suffering on-line division in order to conserve resources.

The entertainment division will be spun off, sold to someone like Sony or even Barnes & Noble, or dramatically reduced in size. Unable to make a profit it will increasingly be seen as a distraction to the battle for saving Windows – and Microsoft leadership has long shown they have no idea how to profitably grow this business unit.

As more and more of the market shifts to competitive cloud businesses Apple, Amazon and others will grow significantly. Microsoft, losing its user base, will demonstrate its inability to build a new business in the cloud, mimicking its historical experiences with Zune (mobile music) and Microsoft mobile phones. Microsoft server and tool sales will suffer, creating a much more difficult profit environment for the sole remaining profitable division.

Missing the market shift to mobile has already forever tarnished the Microsoft brand. No longer is Microsoft seen as a leader, and instead it is rapidly losing market relevancy as people look to Apple, Google, Amazon, Samsung, Facebook and others for leadership. The declining sales, and lack of customer interest will lead to a tailspin at Microsoft not unlike what happened to RIM. Cash will be burned in what Microsoft will consider an "epic" struggle to save the "core of the company."

But failure is already inevitable. At this stage, not even a new CEO can save Microsoft. Steve Ballmer played "Bet the Company" on the long-delayed release of Win8, losing the chance to refocus Microsoft on other growing divisions with greater chance of success. Unfortunately, the other players already had enough chips to simply bid Microsoft out of the mobile game – and Microsoft's ante is now long gone – without holding a hand even remotely able to turn around the product situation.

Game over. Ballmer loses. And if you keep your money invested in Microsoft it will disappear along with the company.

We've become so used to reading about reorganizations, layoffs and cost cutting that most people just accept such leadership decisions as "best practice." No matter the company, or industry, it has become conventional wisdom to believe cost cutting is a good thing.

As a reporter recently asked me regarding about layoffs at Yahoo, "Isn't it always smart to cut heads when your profits fall?" Of course not. Have the layoffs at Yahoo in any way made it a better, more successful company able to compete with Google, Microsoft, Facebook and Apple? Given the radical need for innovation, layoffs have only hurt Yahoo more – and made it more likely to end up like RIM (Research in Motion.)

But like believing in a flat world, blood letting to cure disease and that meteorites are spit up out of the ground – this is just another conventional wisdom that is untrue; and desperately needs to be challenged. Cost reductions are killing most companies, not helping them.

Take for example Sara Lee. Sara Lee was once a great, growing company. Its consumer brands were well known, considered premium products and commanded a price premium at retail.

The death spiral at Sara Lee began in 2006. "Professional managers" from top-ranked MBA schools started "improving earnings" with an ongoing program of reorganizations and cost reductions. Largely under the leadership of the much-vaunted Brenda Barnes, none of these cost reductions improved revenues. And the stock price went nowhere.

With each passing year Sara Lee sold parts of the business, such as Hanes, under the disguise of "seeking focus." With each sale a one-time gain was booked, and more people were laid off as the reorganizations continued. Profits remained OK, but the company was actually shrinking – rather than growing.

To prop up the stock price all avaiable cash was used to buy back stock, which helped maximize executive compensation but really did nothing for investors. R&D was eliminated, as was new product development and any new product launches. Instead Sara Lee kept selling more businesses, reorganizing, cutting costs — and buying its own shares. Until finally, after Ms. Barnes left due to an unfortunate stroke, Sara Lee was so small it had nothing left to sell.

So the company decided to split into two parts! Magically, it's like pushing the reset button. What was Sara Lee is now an even smaller Hillshire Brands. All that poor track record of sales, profits and equity value goes POOF as the symbol SLE disappears, and investors are left following HSH – which has only traded for about 2 days! No more looking at that long history of bad performance, it isn't on Bloomberg or Marketwatch or Yahoo. Like the name Sara Lee, the history vanishes.

Well, "if you can't dazzle 'em with brilliance you baffle 'em with bull**it" W.C. Fields once said.

Cost cuts don't work because they don't compound. If I lay off the head of Brand Marketing this year I promise to save $300,000 and improve the Profit & Loss Statement (P&L) by that amount. So a one time improvement. Now – ignoring the fact that the head of branding probably did a number of things to grow revenue – the problem becomes, what do you do the next year? You can't lay off the Brand V.P. again to save that $300,000 twice. Further, if you want to improve the P&L by $450,000 this time you actually have to find 2 Directors to lay off!

Shooting your own troops in order to manage a smaller army rarely wins battles.

Cost cuts are one-time, and are impossible to duplicate. Following this route leads any company toward being much smaller. Like Sara Lee. From a once great company with revenues in the $10s of billions, the new Hillshire Brands isn't even an S&P 500 company (it was replaced by Monster Beverage.) And how can any investor obtain a great return on investment from a company that's shrinking?

What does create a great company? Growth! Unlike cost cutting, if a company launches a new product it can sell $300,000 the first year. If it meets unmet needs, and is a more effective solution, then the product can attract new customers and sell $600,000 the second year. And then $900,000 or maybe $1.2M the third year. (And even add jobs!)

If you are very good at creating and launching products that meet needs, you can create billions of dollars in new revenue. Like Apple with the iPhone and iPad. Or Facebook. Or Groupon. These companies are growing revenues extremely fast because they have products that meet needs. They aren't trying to "save the P&L."

And revenue growth creates "compound returns." Unlike the cost savings which are one time, each dollar of revenue produces cash flow which can be invested in more sales and delivery which can generate even more cash flow. So if growth is 20% and you invest $1,000 in year one, that can become $1,200 in year two, then $1,440 in year three, $1,728 in year four and $2,070 in year five. Each year you receive 20% not only on the $1,000 you invested, but on returns from the previous years!

By compounding year after year, at20% investor money doubles in 5 years. That's why the most important term for investing is CAGR – Compound Annual Growth Rate. Even a small improvement in this number, from say 9% to 11%, has very important meaning. Because it "compounds" year after year. You don't have to add to your investment – merely allowing it to support growth produces very, very handsome returns. The higher the CAGR the better.

Something no cost cutting program can possibly due. Ever.

So, what is the future of Hillshire Brands? According to the CEO, interviewed Sunday for the Chicago Tribune, the company's historically poor performance could be blamed on —– wait —– insufficient focus. Alas, Sara Lee's problem was obviously too much sales! Well, good thing they've been solving that problem.

Of course, having too many brands led to too much lateral thinking and not enough really deep focus on meat. So now that all they need to think about is meat, he expects innovation will be much improved. Right. Now that HSH is a "meat focused meals" company, and the objective is to add innovation to meat, they are considering such radical dietary improvements for our fat-laden, overcaloried American society as adding curry powder to the frozen meatloaf.

Not exactly the iPhone.

To create future growth the first act the new CEO took to push growth was —- wait —– cutting staff by $100million over the next 3 years. Really. He will solve the "analysis paralysis" which seems to concern him as head of this much smaller company because there won't be anyone around to do the analysis, nor to discuss it and certainly not to disagree with the CEO's decisions. Perhaps meat loaf egg rolls will be next.

All reorganizations and cost reductions point to leadership's failure to create growth. Every time. Staff reductions say to investors, employees, suppliers and customers "I have no idea how to add profitable revenue to this company. I really have no clue how to put these people to work productively – even if they are really good people. I have no choice but to cut these jobs, because we desperately need to make the profits look better in order to prop up the stock price short term; even if it kills our chances of developing new products, creating new markets and making superior rates of return for investors long term."

Hillshire's CEO may do very well for himself, and his fellow executives. Assuredly they have compensation plans tied to stock price, and golden parachutes if they leave. HSH is now so small that it is a likely purchase by a more successful company. By further gutting the organization Hillshire's CEO can reduce staff to a minimum, making the acquisition appear easier for a large company. This would allow a premium payment upon acquisition, providing millions to the executives as options pay out and golden parachutes enact.

And it might give a return to the shareholders. If the ongoing slaughter finds a buyer. Otherwise investors will see the stock crater as it heads to bankruptcy. Like RIM and Yahoo. So flip a coin. But that's called gambling, not investing.

What investors need is CAGR. Not cost cutting and reorganizations. And as I've said since 2006 – you don't want to own Sara Lee; even if it's now called Hillshire Brands.