by Adam Hartung | May 15, 2016 | In the Swamp, Investing, real estate, Retail

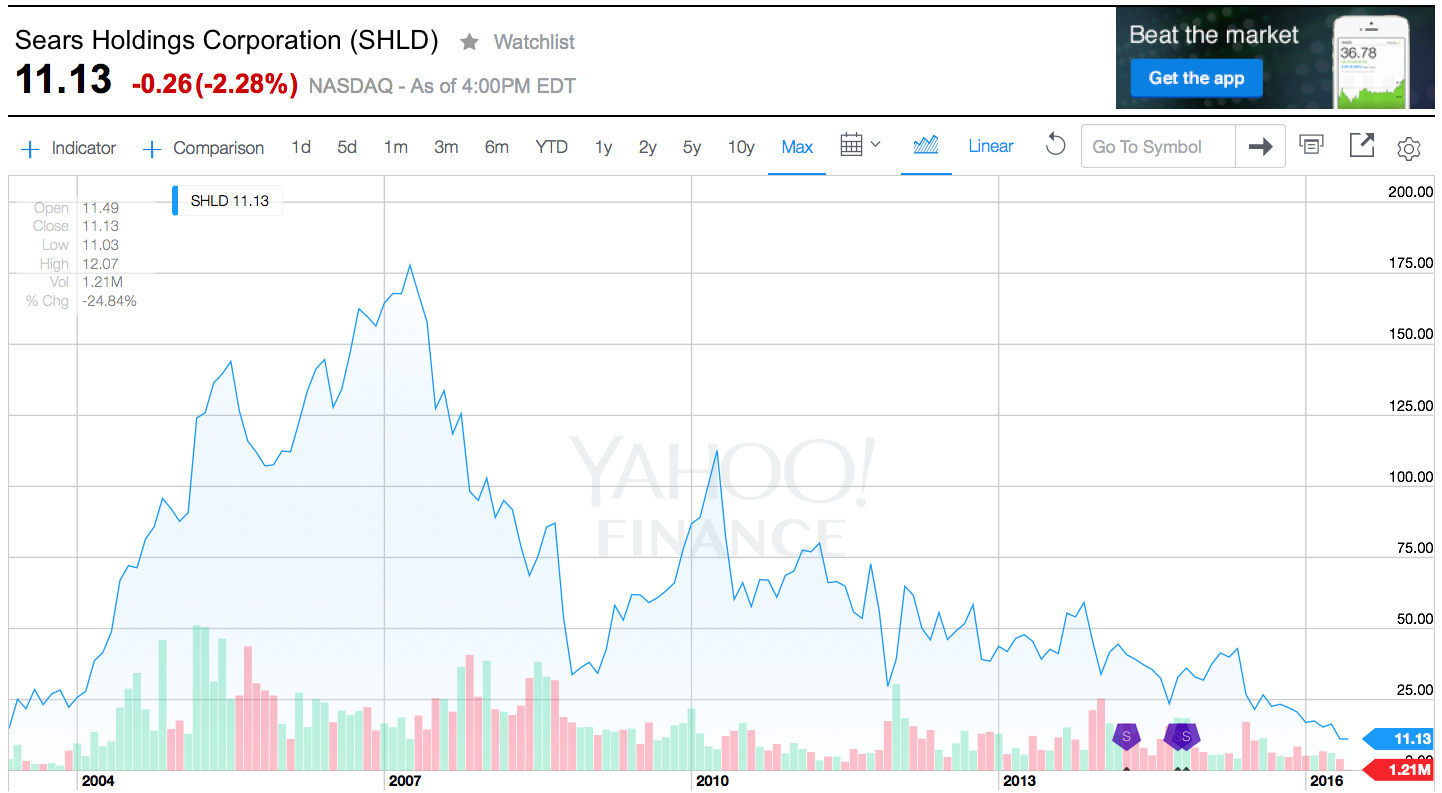

Last week Sears announced sales and earnings. And once again, the news was all bad. The stock closed at a record, all time low. One chart pretty much sums up the story, as investors are now realizing bankruptcy is the most likely outcome.

Chart Source: Yahoo Finance 5/13/16

Quick Rundown: In January, 2002 Kmart is headed for bankruptcy. Ed Lampert, CEO of hedge fund ESL, starts buying the bonds. He takes control of the company, makes himself Chairman, and rapidly moves through proceedings. On May 1, 2003, KMart begins trading again. The shares trade for just under $15 (for this column all prices are adjusted for any equity transactions, as reflected in the chart.)

Lampert quickly starts hacking away costs and closing stores. Revenues tumble, but so do costs, and earnings rise. By November, 2004 the stock has risen to $90. Lampert owns 53% of Kmart, and 15% of Sears. Lampert hires a new CEO for Kmart, and quickly announces his intention to buy all of slow growing, financially troubled Sears.

In March, 2005 Sears shareholders approve the deal. The stock trades for $126. Analysts praise the deal, saying Lampert has “the Midas touch” for cutting costs. Pumped by most analysts, and none moreso than Jim Cramer of “Mad Money” fame (Lampert’s former roommate,) in 2 years the stock soars to $178 by April, 2007. So far Lampert has done nothing to create value but relentlessly cut costs via massive layoffs, big inventory reductions, delayed payments to suppliers and store closures.

Homebuilding falls off a cliff as real estate values tumble, and the Great Recession begins. Retailers are creamed by investors, and appliance sales dependent Sears crashes to $33.76 in 18 months. On hopes that a recovering economy will raise all boats, the stock recovers over the next 18 months to $113 by April, 2010. But sales per store keep declining, even as the number of stores shrinks. Revenues fall faster than costs, and the stock falls to $43.73 by January, 2013 when Lampert appoints himself CEO. In just under 2.5 years with Lampert as CEO and Chairman the company’s sales keep falling, more stores are closed or sold, and the stock finds an all-time low of $11.13 – 25% lower than when Lampert took KMart public almost exactly 13 years ago – and 94% off its highs.

What happened?

Sears became a retailing juggernaut via innovation. When general stores were small and often far between, and stocking inventory was precious, Sears invented mail order catalogues. Over time almost every home in America was receiving 1, or several, catalogues every year. They were a major source of purchases, especially by people living in non-urban communities. Then Sears realized it could open massive stores to sell all those things in its catalogue, and the company pioneered very large, well stocked stores where customers could buy everything from clothes to tools to appliances to guns. As malls came along, Sears was again a pioneer “anchoring” many malls and obtaining lower cost space due to the company’s ability to draw in customers for other retailers.

To help customers buy more Sears created customer installment loans. If a young couple couldn’t afford a stove for their new home they could buy it on terms, paying $10 or $15 a month, long before credit cards existed. The more people bought on their revolving credit line, and the more they paid Sears, the more Sears increased their credit limit. Sears was the “go to” place for cash strapped consumers. (Eventually, this became what we now call the Discover card.)

In 1930 Sears expanded the Allstate tire line to include selling auto insurance – and consumers could not only maintain their car at Sears they could insure it as well. As its customers grew older and more wealthy, many needed help with financia advice so in 1981 Sears bought Dean Witter and made it possible for customers to figure out a retirement plan while waiting for their tires to be replaced and their car insurance to update.

To put it mildly, Sears was the most innovative retailer of all time. Until the internet came along. Focused on its big stores, and its breadth of products and services, Sears kept trying to sell more stuff through those stores, and to those same customers. Internet retailing seemed insignificantly small, and unappealing. Heck, leadership had discontinued the famous catalogues in 1993 to stop store cannibalization and push people into locations where the company could promote more products and services. Focusing on its core customers shopping in its core retail locations, Sears leadership simply ignored upstarts like Amazon.com and figured its old success formula would last forever.

But they were wrong. The traditional Sears market was niched up across big box retailers like Best Buy, clothiers like Kohls, tool stores like Home Depot, parts retailers like AutoZone, and soft goods stores like Bed, Bath & Beyond. The original need for “one stop shopping” had been overtaken by specialty retailers with wider selection, and often better pricing. And customers now had credit cards that worked in all stores. Meanwhile, for those who wanted to shop for many things from home the internet had taken over where the catalogue once began. Leaving Sears’ market “hollowed out.” While KMart was simply overwhelmed by the vast expansion of WalMart.

What should Lampert have done?

There was no way a cost cutting strategy would save KMart or Sears. All the trends were going against the company. Sears was destined to keep losing customers, and sales, unless it moved onto trends. Lampert needed to innovate. He needed to rapidly adopt the trends. Instead, he kept cutting costs. But revenues fell even faster, and the result was huge paper losses and an outpouring of cash.

To gain more insight, take a look at Jeff Bezos. But rather than harp on Amazon.com’s growth, look instead at the leadership he has provided to The Washington Post since acquiring it just over 2 years ago. Mr. Bezos did not try to be a better newspaper operator. He didn’t involve himself in editorial decisions. Nor did he focus on how to drive more subscriptions, or sell more advertising to traditional customers. None of those initiatives had helped any newspaper the last decade, and they wouldn’t help The Washington Post to become a more relevant, viable and profitable company. Newspapers are a dying business, and Bezos could not change that fact.

Mr. Bezos focused on trends, and what was needed to make The Washington Post grow. Media is under change, and that change is being created by technology. Streaming content, live content, user generated content, 24×7 content posting (vs. deadlines,) user response tracking, readers interactivity, social media connectivity, mobile access and mobile content — these are the trends impacting media today. So that was where he had leadership focus. The Washington Post had to transition from a “newspaper” company to a “media and technology company.”

So Mr. Bezos pushed for hiring more engineers – a lot more engineers – to build apps and tools for readers to interact with the company. And the use of modern media tools like headline testing. As a result, in October, 2015 The Washington Post had more unique web visitors than the vaunted New York Times. And its lead is growing. And while other newspapers are cutting staff, or going out of business, the Post is adding writers, editors and engineers. In a declining newspaper market The Washington Post is growing because it is using trends to transform itself into a company readers (and advertisers) value.

CEO Lampert could have chosen to transform Sears Holdings. But he did not. He became a very, very active “hands on” manager. He micro-managed costs, with no sense of important trends in retail. He kept trying to take cash out, when he needed to invest in transformation. He should have sold the real estate very early, sensing that retail was moving on-line. He should have sold outdated brands under intense competitive pressure, such as Kenmore, to a segment supplier like Best Buy. He then should have invested that money in technology. Sears should have been a leader in shopping apps, supplier storefronts, and direct-to-customer distribution. Focused entirely on defending Sears’ core, Lampert missed the market shift and destroyed all the value which initially existed in the great retail merger he created.

Impact?

Every company must understand critical trends, and how they will apply to their business. Nobody can hope to succeed by just protecting the core business, as it can be made obsolete very, very quickly. And nobody can hope to change a trend. It is more important than ever that organizations spend far less time focused on what they did, and spend a lot more time thinking about what they need to do next. Planning needs to shift from deep numerical analysis of the past, and a lot more in-depth discussion about technology trends and how they will impact their business in the next 1, 3 and 5 years.

Sears Holdings was a 13 year ride. Investor hope that Lampert could cut costs enough to make Sears and KMart profitable again drove the stock very high. But the reality that this strategy was impossible finally drove the value lower than when the journey started. The debacle has ruined 2 companies, thousands of employees’ careers, many shopping mall operators, many suppliers, many communities, and since 2007 thousands of investor’s gains. Four years up, then 9 years down. It happened a lot faster than anyone would have imagined in 2003 or 2004. But it did.

And it could happen to you. Invert your strategic planning time. Spend 80% on trends and scenario planning, and 20% on historical analysis. It might save your business.

by Adam Hartung | Jul 10, 2013 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Television

Tribune Corporation finally emerged from a 4 year bankruptcy on the last day of 2012. Before the ink hardly dried on the documents, leadership has decided to triple company debt to double up the number of TV stations. Oh my, some people just never learn.

The media industry is now over a decade into a significant shift. Since the 1990s internet access has changed expectations for how fast, easily and flexibly we acquire entertainment and news. The result has been a dramatic decline in printed magazine and newspaper reading, while on-line reading has skyrocketed. Simultaneously, we're now seeing that on-line streaming is making a change in how people acquire what they listen to (formerly radio based) and watch (formerly television-based.)

Unfortunately, Tribune – like most media industry companies – consistently missed these shifts and underestimated both the speed of the shift and its impact. And leadership still seems unable to understand future scenarios that will be far different from today.

In 2000 newspaper people thought they had "moats" around their markets. The big newspaper in most towns controlled the market for classified ads for things like job postings and used car sales. Classified ads represented about a third of newspaper revenues, and 40% of profits. Simultaneously display advertising for newspapers was considered a cash cow. Every theatre would advertise their movies, every car dealer their cars and every realtor their home listings. Tribune leadership felt like this was "untouchable" profitability for the LA Times and Chicago Tribune that had no competition and unending revenue growth.

So in 2000 Tribune spent $8B to buy Times-Mirror, owner of the Los

Angeles Times. Unfortunately, this huge investment (75% over market

price at the time, by the way) was made just as people were preparing to

shift away from newspapers. Craigslist, eBay and other user sites killed the market for classified ads. Simultaneously movie companies, auto companies and realtors all realized they could reach more people, with more information, cheaper on-line than by paying for newspaper ads.

These web sites all existed before the acquisition, but Tribune leadership ignored the trend. As one company executive said to me "CraigsList!! You think that's competition for a newspaper? Craigslist is for hookers! Nobody would ever put a job listing on Craigslist." Like his compadres running newspapers nationwide, the new competitors and trends toward on-line were dismissed with simplistic statements and broad generalizations that things would never change.

The floor fell out from under advertising revenues in newspapers in the 2000s. There was no way Times-Mirror would ever be worth a fraction of what Tribune paid. Debt used to help pay for the acquisition limited the options for Tribune as cost cutting gutted the organization.

Then, in 2007 Sam Zell bailed out management by putting together a leveraged buyout to acquire Tribune company. Saying that he read 3 newspapers every day, he believed people would never stop reading newspapers. Like a lot of leaders, Mr. Zell had more money than understanding of trends and shifting markets. He added a few billion dollars more debt to Tribune. By the end of 2008 Tribune was unable to meet its debt obligations, and filed for bankruptcy.

Now, new leadership has control of Tribune. They are splitting the company in two, seperating the print and broadcast businesses. The hope is to sell the newspapers, for which they believe there are 40 potential buyers. Even though profits continued falling, from $156M to $89M, in just the last year. Why anyone would buy newspaper companies, which are clearly buggy whip manufacturers, is wholly unclear. But hope springs eternal!

The new stand-alone Tribune Broadcasting company has decided to go all-in on a deal to borrow $2.7B and buy 19 additional local television stations raising total under their control to 42.

Let's see, what's the market trend in entertainment and news? Where once we were limited to local radio and television stations for most content, now we can acquire almost anything we want – from music to TV, movies, documentaries or news – via the internet. Rather than being subjected to what some programming executive decides to give us, we can select what we want, when we want it, and simply stream it to our laptop, tablet, smartphone, or even our large-screen TV.

A long time ago content was controlled by distribution. There was no reason to create news stories or radio programs or video unless you had access to distribution. Obviously, that made distribution – owning newspapers, radio and TV stations – valuable.

But today distribution is free, and everywhere. Almost every American has access to all the news and entertainment they want from the internet. Either free, or for bite-size prices that aren't too high. Today the value is in the content, not distribution.

In the last 2 years the number of homes without a classical TV connection (the cable) has doubled. Sure, it's only 5% of homes now. But the trend is pretty clear. Even homes that have cable are increasingly not watching it as they turn to more and more streaming video. Instead of watching a 30 minute program once per week, people are starting to watch 8 or 10 half hour episodes back to back. And when they want to watch those episodes, where they want to watch them.

While it might be easy for Tribune to ignore Hulu, Netflix and Amazon, the trend is very clear. The need for broadcast stations like NBC or WGN or Food Network to create content is declining as we access content more directly, from more sources. And the need to have content delivered to our home by a local affiliate station is becoming, well, an anachronism.

Yet, Tribune's new TV-oriented leadership is doubling down on its bet for local TV's future. Ignoring all the trends, they are borrowing more money to buy more assets that show all signs of becoming about as valuable whaling ships. It's a big, dumb bet. Similar to overpaying for Times-Mirror. Some leaders just seem destined to never learn.

by Adam Hartung | May 25, 2011 | Defend & Extend, Disruptions, In the Swamp, Innovation, Leadership, Lock-in, Openness, Transparency, Web/Tech

Nobody admits to being the innovation killer in a company. But we know they exist. Some these folks “dinosaurs that won’t change.” Others blame “the nay-saying ‘Dr. No’ middle managers.” But when you meet these people, they won’t admit to being innovation killers. They believe, deep in their hearts as well as in their everyday actions, that they are doing the right thing for the business. And that’s because they’ve been chosen, and reinforced, to be the Status Quo Police.

When a company starts it has no norms. But as it succeeds, in order to grow quickly it develops a series of “key success factors” that help it continue growing. In order to grow faster, managers – often in functional roles – are assigned the task of making sure the key success factors are unwaveringly supported. Consistency becomes more important than creativity. And these managers are reinforced, supported, even bonused for their ability to make sure they maintain the status quo. Even if the market has shifted, they don’t shift. They reinforce doing things according to the rules. Just consider:

Quality – Who can argue with the need to have quality? Total Quality Management (TQM,) Continuous Improvement (CI,) and Six Sigma programs all have been glorified by companies hoping to improve product or service quality. If you’re trying to fix a broken product, or process, these work pretty well at helping everyone do their job better.

But these programs live with the mantra “if you can’t measure it, you can’t improve it. Measure everything that’s important.” If you’re innovating, what do you measure? If you’re in a new technology, or manufacturing process, how do you know what you really need to do right? If you’re in a new market, how do you know the key metric for sales success? Is it number of customers called, time with customers, number of customer surveys, recommendation scores, lost sales reports? When you’re trying to do something new, a lot of what you do is respond quickly to instant feedback – whether it’s good feedback or bad.

The key to success isn’t to have critical metrics and measure performance on a graph, but rather to learn from everything you do – and usually to change. Quality people hate this, and can only stand in the way of trying anything new because you don’t know what to measure, or what constitutes a “good” measure. Don’t ever forget that Motorola pretty much invented Six Sigma, and what happened to them in the mobile phone business they pioneered?

Finance. All businesses exist to make money, so who can argue with “show me the numbers. Give me a business plan that shows me how you’re going to make money.” When your’e making an incremental investment to an existing asset or process, this is pretty good advice.

But when you’re innovating, what you don’t know far exceeds what you know. You don’t know how to meet unment needs. You don’t know the market size, the price that people will pay, the first year’s volume (much less year 5,) the direct cost at various volumes, the indirect cost, the cost of marketing to obtain customer attention, the number of sales calls it will take to land a sale, how many solution revisions will be necessary to finally put out the “right” solution, or how sales will ramp up quarterly from nothing. So to create a business plan, you have to guess.

And, oh boy, then it gets ugly. “Where did this number come from? That one? How did you determine that?” It’s not long until the poor business plan writer is ridden out of the meeting on a rail. He has no money to investigate the market, so he can’t obtain any “real” numbers, so the business plan process leads to ongoing investment in the old business, while innovation simply stalls.

Under Akia Morita Sony was a great innovator. But then an MBA skilled in finance took over the top spot. What once was the #1 electronics innovator in the globe has become, well, let’s say they aren’t Apple.

Legal – No company wants to be sued, or take on unnecessary risk. And when you’re selling something, lawyers are pretty good at evaluating the risk in that business, and lowering the risk. While making sure that all the compliance issues are met in order to keep regulators – and other lawyers – out of the business.

But when you’re starting something new, everything looks risky. Customers can sue you for any reason. Suppliers can sue you for not taking product, or using it incorrectly. The technology could fail, or have negative use repercussions. Reguators can question your safety standards, or claims to customers.

From a legal point of view, you’re best to never do anything new. The less new things you do, the less likely you are to make a mistake. So legal’s great at putting up roadblocks to make sure they protect the company from lawsuits, by making sure nothing really new happens. The old General Motors had plenty of lawyers making sure their cars were never too risky – or interesting.

R&D or Product Development – Who doesn’t think it’s good to be a leader in a specific technology? Technology advances have proven invaluable for companies in industries from computers to pharmaceuticals to tractors and even services like on-line banking. Thus R&D and Product Development wants to make sure investments advance the state of the technology upon which the company was built.

But all technologies become obsolete. Or, at least unprofitable. Innovators are frequently on the front end of adopting new technologies. But if they have to obtain buy-in from product development to obtain staffing or money they’ll be at the end of a never-ending line of projects to sustain the existing development trend. You don’t have to look much further than Microsoft to find a company that is great at pouring money into the PC platform (some $9B, 16% of revenue in 2009,) while the market moves faster each year to mobile devices and entertainment (Apple spent 1/8th the Microsoft budget in 2009.)

Sales, Marketing & Distribution – When you want to protect sales to existing customers, or maybe increase them by 5%, then doing more of what you’ve always done is smart. So money is spent to put more salespeople on key accounts, add more money to the advertising budget for the most successful (or most profitable) existing products. There are more rules about using the brand than lighters at a smoker’s convention. And it’s heresy to recommend endangering the distribution channel that has so successfully helped increase sales.

But innovators regularly need to behave differently. They need to sell to different people – Xerox sold to secretaries while printing press manufacturers sold to printers. The “brand” may well represent a bygone era, and be of no value to someone launching a new product; are you eager to buy a Zenith electronic device? Sprucing up the brand, or even launching something new, may well be a requirement for a new solution to be taken seriously.

And often, to be successful, a new solution needs to cut through the old, high-cost distribution system directly to customers if it is to succeed. Pre-Gerstner IBM kept adding key account sales people in hopes of keeping IT departments from switching out of mainframes to PCs. Sears avoided the shift to on-line sales successfully – and revenue keeps dropping in the stores.

Information Technology – To make more money you automate more functions. Computers are wonderful for reducing manpower in many tasks. So IT implements and supports “standard solutions” that are cost effective for the historical business. Likewise, they set up all kinds of user rules – like don’t go to Facebook or web sites from work – to keep people focused on productivity. And to make sure historical data is secure and regulations are met.

But innovators don’t have a solution mapped out, and all that automated functionality is an enormously expensive headache. When being creative, more time is spent looking for something new than trying to work faster, or harder, so access to more external information is required. Since the solution isn’t developed, there’s precious little to worry about keeping secure. Innovators need to use new tools, and have flexibility to discover advantageous ways to use them, that are far beyond the bounds of IT’s comfort zone.

Newspapers are loaded with automated systems to collect and edit news, to enter display ads, and to “Make up” the printed page fast and cheap. They have automated systems for classified advertising sales and billing, and for display ad billing. And systems to manage subscribers. That technology isn’t very helpful now, however, as newspapers go bankrupt. Now the most critical IT skills are pumping news to the internet in real-time, and managing on-line ads distributed to web users that don’t have subscriptions.

Human Resources – Growth pushes companies toward tighter job descriptions with clear standards for “the kinds of people that succeed around here.” When you want to hire people to be productive at an existing job, HR has the procedures to define the role, find the people and hire them at the most efficient cost. And they can develop a systematic compensation plan that treats everyone “fairly” based upon perceived value to the historical business.

But innovators don’t know what kinds of people will be most successful. Often they need folks who think laterally, across lots fo tasks, rather than deeply about something narrow. Often they need people who are from different backgrounds, that are closer to the emerging market than the historical business. And pay has to be related to what these folks can get in the market, not what seems fair through the lens of the historical business. HR is rarely keen to staff up a new business opportunity with a lot of misfits who don’t appreciate their compensation plan – or the rules so carefully created to circumscribe behavior around the old business.

B.Dalton was America’s largest retail book seller when Amazon.com was founded by Jeff Bezos. Jeff knew nothing about books, but he knew the internet. B.Dalton knew about books, and claimed it knew what book buyers wanted. Two years later B.Dalton went bankrupt, and all those book experts became unemployed. Amazon.com now sells a lot more than books, as it ongoingly and rapidly expands its employee skill sets to enter new markets – like publishing and eReaders.

Innovation requires that leaders ATTACK the Status Quo Police. Everything done to efficiently run the old business is irrelevant when it comes to innovation. Functional folks need to be told they can’t force the innovatoirs to conform to old rules, because that’s exactly why the company needs innovation! Only by attacking the old rules, and being willing to allow both diversity and disruption can the business innovate.

Instead of saying “this isn’t how we do things around here” it is critical leaders make sure functional folks are saying “how can I help you innovate?” What was done in the name of “good business” looks backward – not forward. Status Quo cops have to be removed from the scene – kept from stopping innovation dead in its tracks. And if the internal folks can’t be supportive, that means keeping them out of the innovator’s way entirely.

Any company can innovate. Doing so requires recognizing that the Status Quo Police are doing what they were hired to do. Until you take away their clout, attack their role and stop them from forcing conformance to old dictums, the business can’t hope to innovate.

by Adam Hartung | Feb 18, 2011 | Current Affairs, In the Swamp, Innovation, Leadership, Lock-in, Openness, Television, Web/Tech

Business people keep piling onto the innovation and growth bandwagon. PWC just released the results of its 14th annual CEO survey entitled “Growth Reimagined.” Seems like most CEOs are as tired of cost cutting as everyone else, and would really like to start growing again. Therefore, they are looking for innovations to help them improve competitiveness and build new markets. Hooray!

But, haven’t we heard this before? Seems like the output of several such studies – from IBM, IDC and many others – have been saying that business leaders want more innovation and growth for the last several years! Hasn’t this been a consistent mantra all through the last decade? You could get the impression everyone is talking about innovation, and growth, but few seem to be doing much about it!

Rather than search out growth, most businesses are still trying to simply do what their business has done for decades – and marveling at the lack of improved results. David Brooks of the New York Times talks at length in his recent Op Ed piece on the Experience Economy about a controversial book from Tyler Cowen called “The Great Stagnation.” The argument goes that America was blessed with lots of fertile land and abundant water, giving the country a big advantage in the agrarian economy from the 1600s into the 1900s. During the Industrial economy of the 1900s America was again blessed with enormous natural resources (iron ore, minerals, gold, silver, oil, gas and water) as well as navigable rivers, the great lakes and natural low-cost transport routes. A rapidly growing and hard working set of laborers, aided by immigration, provided more fuel for America’s growth as an industrial powerhouse.

But now we’re in the information economy. Those natural resources aren’t the big advantage they once were. Foodstuffs require almost no people for production. And manufacturing is shifting to offshore locations where cheap labor and limited regulations allow for cheaper production. And it’s not clear America would benefit even if it tried maintaining these lower-skilled jobs. Today, value goes to those who know how to create, store, manipulate and use information. And success in this economy has a lot more to do with innovation, and the creation of entirely new products, industries and very different kinds of jobs.

Unfortunately, however, we keep hiring for the last economy. It starts with how Boards of Directors (and management teams) select – incorrectly, it appears – our business leaders. Still thinking like out-of-date industrialists, Scientific American offers us a podcast on how “Creativity Can Lesson a Leader’s Image.” Citing the same study, Knowledge @ Wharton offers us “A Bias Against ‘Quirky’ Why Creative People Can Lose Out on Creative Positions.” While 1,500 CEOs say that creativity is the single most important quality for success today – and studies bear out the greater success of creative, innovative leaders – the study found that when it came to hiring and promoting businesses consistently marked down the creative managers and bypassed them, selecting less creative types!

Our BIAS (Beliefs, Interpretations, Assumptions and Strategies) cause the selection process to pick someone who is seen as less creative. Consider these comments:

- “would you rather have a calm hand on the tiller, or someone who constantly steers the boat?”

- “do you want slow, steady conservatism in control – or irrational exuberance?”

- “do we want consistent execution or big ideas?”

These are all phrases I’ve heard (as you might have as well) for selecting a candidate with a mediocre track record, and very limited creativity, over a candidate with much better results and a flair for creativity to get things done regardless of what the market throws at her. All imply that what’s important to leadership is not making mistakes. Of you just don’t screw up the future will take care of itself. And that’s so industrial economy – so “don’t let the plant blow up.”

That approach simply doesn’t work any more. The Christian Science Monitor reported in “Obama’s Innovation Push: Has U.S. Really Fallen Off the Cutting Edge” that America is already in economic trouble due to our lock-in to out-of-date notions about what creates business success. In the last 2 years America has fallen from first to fourth in the World Economic Forum ranking of global competitivenes. And while America still accounts for 40% of global R&D spending, we rank remarkably low (on all studies below 10th place) on things like public education, math and science skills, national literacy and even internet access! While we’ve poured billions into saving banks, and rebuilding roads (ostensibly hiring asphalt layers) we still have no national internet system, nor a free backbone for access by all budding entrepreneurs!

Ask the question, “If Steve Jobs (or his clone) showed up at our company asking for a job – would we give him one?” Don’t forget, the Apple Board fired Steve Jobs some 20 years ago to give his role to a less creative, but more “professional,” John Scully. Mr. Scully was subsequently fired by the Board for creatively investing too heavily in the innovative Newton – the first PDA – to be replaced by a leadership team willing to jettison this new product market and refocus all attention on the Macintosh. Both CEO change decisions turned out to be horrible for Apple, and it was only after Mr. Jobs returned to the company after nearly 20 years in other businesses that its fortunes reblossomed when the company replaced outdated industrial management philosophies with innovation. But, oh-so-close the company came to complete failure before re-igniting the innovation jets.

Examples of outdated management, with horrific results, abound. Brenda Barnes destroyed shareholder value for 6 years at Sara Lee chasing a centrallized focus and cost reductions – leaving the company with no future other than break-up and acquisition. GE’s fortunes have dropped dramatically as Mr. Immelt turned away from the rabid efforts at innovation and growth under Welch and toward more cautious investments and reliance on a set of core markets – including financial services. After once dominating the mobile phone industry the best Motorola’s leadership has been able to do lately is split the company in two, hoping as a divided business leadership can do better than it did as a single entity. Even a big winner like Home Depot has struggled to innovate and grow as it remained dedicated to its traditional business. Once a darling of industry, the supply chain focused Dell has lost its growth and value as a raft of new MBA leaders – mostly recruited from consultancy Bain & Company – have kept applying traditional industrial management with its cost curves and economy-of-scale illogic to a market racked by the introduction of new products such as smartphones and tablets.

Meanwhile, leaders that foster and implement innovation have shown how to be successful this last decade. Jeff Bezos has transformed retailing and publishing simultaneously by introducing a raft of innovations, including the Kindle. Google’s value soared as its founders and new CEO redefined the way people obtain news – and the ads supporting what people read. The entire “social media” marketplace is now taking viewers, and ad dollars, from traditional media bringing the limelight to CEOs at Facebook, Twitter and Linked-in. While newspaper companies like Tribune Corp., NYT, Dow Jones and Washington Post have faltered, pop publisher Arianna Huffington created $315M of value by hiring a group of bloggers to populate the on-line news tabloid Huffington Post. And Apple is close to becoming the world’s most valuable publicly traded company on the backs of new product innovations.

But, asking again, would your company hire the leaders of these companies? Would it hire the Vice-President’s, Directors and Managers? Or would you consider them too avant-garde? Even President Obama washed out his commitment to jobs growth when he selected Mr. Immelt to head his committee – demonstrating a complete lack of understanding what it takes to grow – to innovate – in today’s intensely competitive information economy. Where he should have begged, on hands and knees, for Eric Schmidt of Google to show us the way to information nirvana he picked, well, an old-line industrialist.

Until we start promoting innovators we won’t have any innovation. We must understand that America’s successful history doesn’t guarantee it’s successful future. Competing on bits, rather than brawn or natural resources, requires creativity to recognize opportunities, develop them and implement new solutions rapidly. It requires adaptability to deal with new technologies, new business models and new competitors. It requires an understanding of innovation and how to learn while doing. Amerca has these leaders. We just need to give them the positions and chance to succeed!

by Adam Hartung | Jan 5, 2011 | Defend & Extend, In the Rapids, In the Swamp, Leadership, Lock-in, Openness

Summary:

- Business planning systems are designed to defend historical markets

- Rapidly shifting markets makes it impossible to grow by defense alone

- Growth requires understanding what customers want, and creating new solutions that most likely aren’t part of the current business

- You can’t grow if you don’t plan to grow, but to plan for growth you have to shift resources from traditional planning into scenario planning

- High growth companies like Virgin, Apple and Google plan to fulfill future needs, not defend & extend past practicess

Imagine you see a pile of hay. Above it is a sign flashing “find the needle.” That achievement would be hard. Change the sign to “find the hay” and suddenly achieving the goal becomes much easier. So, as the comedian Bill Engvall might ask, what’s your sign? Unfortunately, most businesses plan for 2011, and beyond, using the first sign. Very few do planning using the latter. Most businesses won’t grow, because they simply don’t know how to plan for growth!!

Most businesses start planning with “I’m in the horseshoe (for example) business. My market isn’t growing, and there is more capacity than demand. How can I grow?” For these people, their sign is “find the needle.”

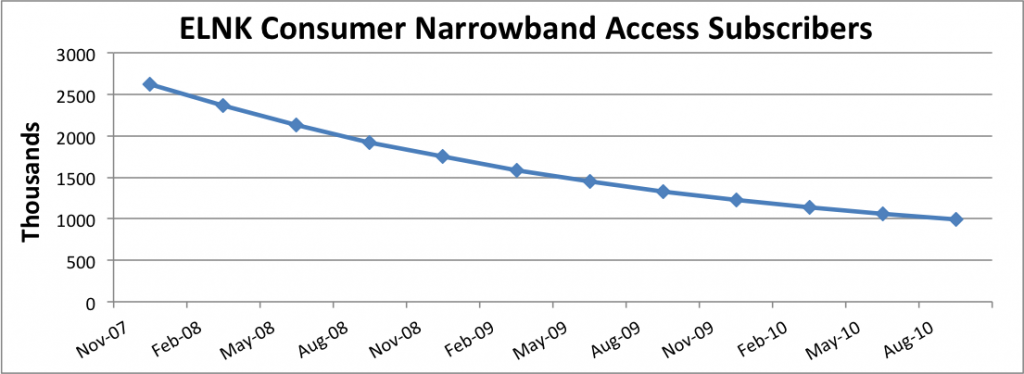

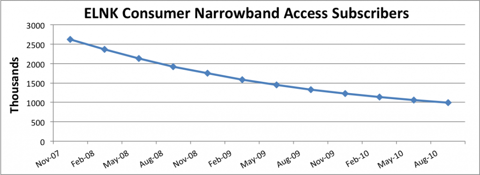

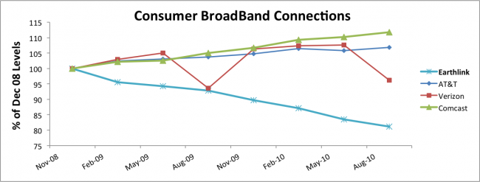

Take for example Earthlink. The company’s growth looked like a rocket ship in the early internet days as people by the millions signed up for dial-up service. But along came broadband, and the market for dial up died – never to return. Earthlink has no hope of growing as long as it thinks of itself as a dial-up company

Chart at SeekingAlpha.com author Ananthan Thangavel

Despite the absolute certainty that the market is shrinking, at this point almost all business planners will develop plans to defend this dying business as long as possible. Despite the impossibility of achieving good returns, there will be a plethora of actions to try and keep serving all the way to the very last customer. Just look at how AOL has invested millions trying to defend its dying internet access busiuness. Reality is, the company that walks away – gives up- is the smartest. There’s no way to make money as oversupply keeps too many companies spending too much to service too few customers.

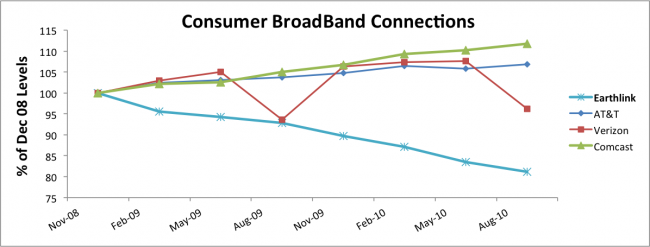

The next step for most planners is to attempt extending the business into something adjacent. For example, Earthlink would say “let’s invest in Broadband. We’ll hang onto customers as they want to switch, and maybe pick up a few customers.” But this completely ignores the fact that competitors already have a substantial lead. Competitors have learned the technology, and the marketplace. They are growing, and have no intention of giving up any room to a new competitor.

Chart at SeekingAlpha.com author Ananthan Thangavel

Planning systems are designed to keep the business doing more of what it always did, or possibly extending the business into adjacent markets after returns have faltered. Planning systems have no way of recognizing when a business, or market, has become obsolete. And practically never do they recognize the power of exsting competitors when looking at adjacent markets. As a result, the planning system produces no growth plans, leading 2011 to end with the self-fulfilling prophecy that the plan predicted – little or no growth.

The future for Earthlink is pretty grim. As it is for most companies that plan based upon history, trying to Defend & Extend their historical markets. In the highly dynamic, global marketplaces of 2011 trying to find growth by remaining focused on the past is like looking for the needle in a haystack. Maybe there’s something in there – but it’s not likely – and it’s even a lot less likely you’ll find it – and if you did, the cost of finding it will almost assuredly be greater than the value.

Alternatively, why not use planning resources to find, and develop, growth markets. Instead of looking at what you did (as in the past tense) try to figure out what you should do. Rather than studying past products, customers and markets, why not develop scenarios about the future that give you insight to what people will want to buy in 2011, 2012 and beyond? Rather than looking for needles, why not go explore the hay?

Newspapers kept focusing on declining subscriptions, when they should have been studying Craig’s List, eBay, Vehix.com and other on-line environments to learn the future of advertising. Had Tribune company poured its resources into its early internet investments, such as cars.com and careerbuilder.com, rather than trying to defend its traditional newspapers, it may well have avoided bankruptcy. But rather than looking to the future when doing its planning, and understanding that on-line news was going to explode, Tribune kept looking for the needle (cost cuts, layoffs, outsourcing, etc.) to save the old success formula.

Direct mail companies and Sunday insert printers have continued looking for ways to defend & extend their coupon printing business – despite the fact that nobody reads junk mail or uses printed coupons. Several have failed, and larger companies have merged trying to find “synergies” and more cost cuts. Simultaneously a 28 year old music major from Nothwestern university starts figuring out how to help companies acquire new customers by offering email coupons, and within 2 years his company, Groupon, is valued at around $6B. There’s nothing that stopped coupon powerhouse Advo from being Groupon, except that its planning system was devoted to finding the needle, while Groupon’s leaders decided to go play in the hay.

Hallmark and American Greetings want us to buy birthday and holiday cards for various occasions – in a world where almost nobody mails cards any longer. As they keep trying to defend their old business, and extend it into a few new opportunities for on-line cards, Twitter captures the wave of instant communications by offering everyone 140 character ways to communicate. Because Twitter is out where the growth is, the company raises $200M giving it a value of $3.7B.

Nothing stops any business from being anything it wants to be. But as most enter 2011 they will use their planning resources, including all those management meetings and hours of forms completion, to do nothing more than re-examine the historical business. Most will devolve into trying to figure out how to do more with less. As future forecasts look grim, or perhaps cautiously optimistic (based on a lot of things going right – like a mysterious pick-up in demand) there will be much nashing of teeth – and meetings looking for a needle that can be offered to employees and investors as a hope for rising future value.

Smart companies get out of that rut. They focus their planning on the future. What do customers want, and how can we give them what they want? How can we create whole new markets. Apple was a PC company, but by exploring mobility it became a provider of MP3 consumer electronics, downloadable music, a mobile device and app supplier and the early winner in cloud accessing tablets. Google has moved from a search engine to a powerhouse ad placement company and is pushing the edges of growth in mobile computing as well as several other markets. Virgin started as a distributor of long-playing vinyl record albums, but by exploring what customers really wanted it has become an international airline, cell phone company, international lender and space travel pioneer (to mention just a few of its businesses.)

You can grow in 2011, but to do so you need to shed the old planning system (and its resource wasting processes) and get serious about scenario planning. Focus on the future, not the past.