by Adam Hartung | May 15, 2016 | In the Swamp, Investing, real estate, Retail

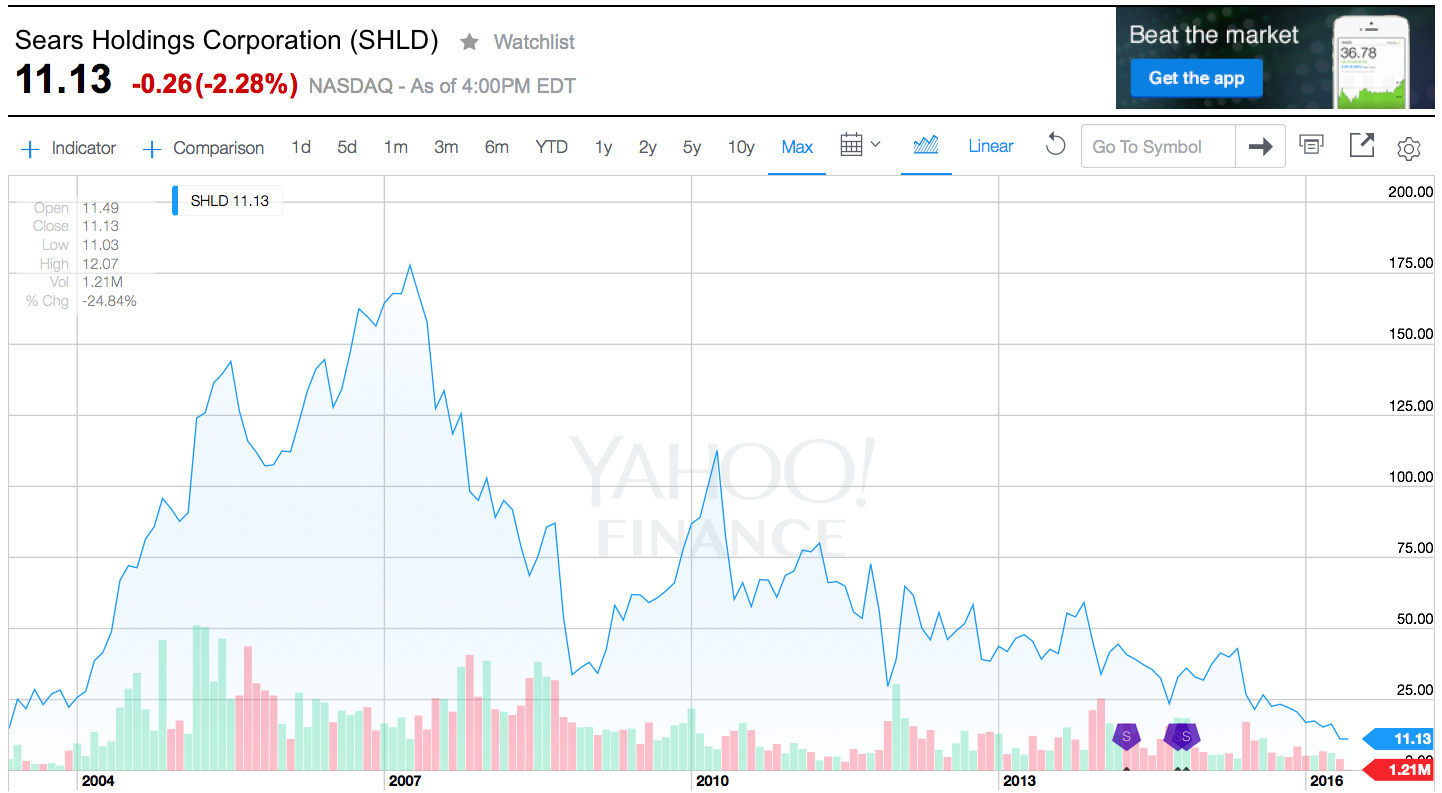

Last week Sears announced sales and earnings. And once again, the news was all bad. The stock closed at a record, all time low. One chart pretty much sums up the story, as investors are now realizing bankruptcy is the most likely outcome.

Chart Source: Yahoo Finance 5/13/16

Quick Rundown: In January, 2002 Kmart is headed for bankruptcy. Ed Lampert, CEO of hedge fund ESL, starts buying the bonds. He takes control of the company, makes himself Chairman, and rapidly moves through proceedings. On May 1, 2003, KMart begins trading again. The shares trade for just under $15 (for this column all prices are adjusted for any equity transactions, as reflected in the chart.)

Lampert quickly starts hacking away costs and closing stores. Revenues tumble, but so do costs, and earnings rise. By November, 2004 the stock has risen to $90. Lampert owns 53% of Kmart, and 15% of Sears. Lampert hires a new CEO for Kmart, and quickly announces his intention to buy all of slow growing, financially troubled Sears.

In March, 2005 Sears shareholders approve the deal. The stock trades for $126. Analysts praise the deal, saying Lampert has “the Midas touch” for cutting costs. Pumped by most analysts, and none moreso than Jim Cramer of “Mad Money” fame (Lampert’s former roommate,) in 2 years the stock soars to $178 by April, 2007. So far Lampert has done nothing to create value but relentlessly cut costs via massive layoffs, big inventory reductions, delayed payments to suppliers and store closures.

Homebuilding falls off a cliff as real estate values tumble, and the Great Recession begins. Retailers are creamed by investors, and appliance sales dependent Sears crashes to $33.76 in 18 months. On hopes that a recovering economy will raise all boats, the stock recovers over the next 18 months to $113 by April, 2010. But sales per store keep declining, even as the number of stores shrinks. Revenues fall faster than costs, and the stock falls to $43.73 by January, 2013 when Lampert appoints himself CEO. In just under 2.5 years with Lampert as CEO and Chairman the company’s sales keep falling, more stores are closed or sold, and the stock finds an all-time low of $11.13 – 25% lower than when Lampert took KMart public almost exactly 13 years ago – and 94% off its highs.

What happened?

Sears became a retailing juggernaut via innovation. When general stores were small and often far between, and stocking inventory was precious, Sears invented mail order catalogues. Over time almost every home in America was receiving 1, or several, catalogues every year. They were a major source of purchases, especially by people living in non-urban communities. Then Sears realized it could open massive stores to sell all those things in its catalogue, and the company pioneered very large, well stocked stores where customers could buy everything from clothes to tools to appliances to guns. As malls came along, Sears was again a pioneer “anchoring” many malls and obtaining lower cost space due to the company’s ability to draw in customers for other retailers.

To help customers buy more Sears created customer installment loans. If a young couple couldn’t afford a stove for their new home they could buy it on terms, paying $10 or $15 a month, long before credit cards existed. The more people bought on their revolving credit line, and the more they paid Sears, the more Sears increased their credit limit. Sears was the “go to” place for cash strapped consumers. (Eventually, this became what we now call the Discover card.)

In 1930 Sears expanded the Allstate tire line to include selling auto insurance – and consumers could not only maintain their car at Sears they could insure it as well. As its customers grew older and more wealthy, many needed help with financia advice so in 1981 Sears bought Dean Witter and made it possible for customers to figure out a retirement plan while waiting for their tires to be replaced and their car insurance to update.

To put it mildly, Sears was the most innovative retailer of all time. Until the internet came along. Focused on its big stores, and its breadth of products and services, Sears kept trying to sell more stuff through those stores, and to those same customers. Internet retailing seemed insignificantly small, and unappealing. Heck, leadership had discontinued the famous catalogues in 1993 to stop store cannibalization and push people into locations where the company could promote more products and services. Focusing on its core customers shopping in its core retail locations, Sears leadership simply ignored upstarts like Amazon.com and figured its old success formula would last forever.

But they were wrong. The traditional Sears market was niched up across big box retailers like Best Buy, clothiers like Kohls, tool stores like Home Depot, parts retailers like AutoZone, and soft goods stores like Bed, Bath & Beyond. The original need for “one stop shopping” had been overtaken by specialty retailers with wider selection, and often better pricing. And customers now had credit cards that worked in all stores. Meanwhile, for those who wanted to shop for many things from home the internet had taken over where the catalogue once began. Leaving Sears’ market “hollowed out.” While KMart was simply overwhelmed by the vast expansion of WalMart.

What should Lampert have done?

There was no way a cost cutting strategy would save KMart or Sears. All the trends were going against the company. Sears was destined to keep losing customers, and sales, unless it moved onto trends. Lampert needed to innovate. He needed to rapidly adopt the trends. Instead, he kept cutting costs. But revenues fell even faster, and the result was huge paper losses and an outpouring of cash.

To gain more insight, take a look at Jeff Bezos. But rather than harp on Amazon.com’s growth, look instead at the leadership he has provided to The Washington Post since acquiring it just over 2 years ago. Mr. Bezos did not try to be a better newspaper operator. He didn’t involve himself in editorial decisions. Nor did he focus on how to drive more subscriptions, or sell more advertising to traditional customers. None of those initiatives had helped any newspaper the last decade, and they wouldn’t help The Washington Post to become a more relevant, viable and profitable company. Newspapers are a dying business, and Bezos could not change that fact.

Mr. Bezos focused on trends, and what was needed to make The Washington Post grow. Media is under change, and that change is being created by technology. Streaming content, live content, user generated content, 24×7 content posting (vs. deadlines,) user response tracking, readers interactivity, social media connectivity, mobile access and mobile content — these are the trends impacting media today. So that was where he had leadership focus. The Washington Post had to transition from a “newspaper” company to a “media and technology company.”

So Mr. Bezos pushed for hiring more engineers – a lot more engineers – to build apps and tools for readers to interact with the company. And the use of modern media tools like headline testing. As a result, in October, 2015 The Washington Post had more unique web visitors than the vaunted New York Times. And its lead is growing. And while other newspapers are cutting staff, or going out of business, the Post is adding writers, editors and engineers. In a declining newspaper market The Washington Post is growing because it is using trends to transform itself into a company readers (and advertisers) value.

CEO Lampert could have chosen to transform Sears Holdings. But he did not. He became a very, very active “hands on” manager. He micro-managed costs, with no sense of important trends in retail. He kept trying to take cash out, when he needed to invest in transformation. He should have sold the real estate very early, sensing that retail was moving on-line. He should have sold outdated brands under intense competitive pressure, such as Kenmore, to a segment supplier like Best Buy. He then should have invested that money in technology. Sears should have been a leader in shopping apps, supplier storefronts, and direct-to-customer distribution. Focused entirely on defending Sears’ core, Lampert missed the market shift and destroyed all the value which initially existed in the great retail merger he created.

Impact?

Every company must understand critical trends, and how they will apply to their business. Nobody can hope to succeed by just protecting the core business, as it can be made obsolete very, very quickly. And nobody can hope to change a trend. It is more important than ever that organizations spend far less time focused on what they did, and spend a lot more time thinking about what they need to do next. Planning needs to shift from deep numerical analysis of the past, and a lot more in-depth discussion about technology trends and how they will impact their business in the next 1, 3 and 5 years.

Sears Holdings was a 13 year ride. Investor hope that Lampert could cut costs enough to make Sears and KMart profitable again drove the stock very high. But the reality that this strategy was impossible finally drove the value lower than when the journey started. The debacle has ruined 2 companies, thousands of employees’ careers, many shopping mall operators, many suppliers, many communities, and since 2007 thousands of investor’s gains. Four years up, then 9 years down. It happened a lot faster than anyone would have imagined in 2003 or 2004. But it did.

And it could happen to you. Invert your strategic planning time. Spend 80% on trends and scenario planning, and 20% on historical analysis. It might save your business.

by Adam Hartung | Feb 12, 2015 | Current Affairs, Disruptions, Innovation, Leadership, Web/Tech

Despite huge fanfare at launch, after a few brief months Google Glass is no longer on the market. The Amazon Fire Phone was also launched to great hype, yet sales flopped and the company recently took a $170M write off on inventory.

Fortune mercilessly blamed Fire Phone’s failure on CEO Jeff Bezos. The magazine blamed him for micromanaging the design while overspending on development, manufacturing and marketing. To Fortune the product was fatally flawed, and had no chance of success according to the article.

Similarly, the New York Times blasted Google co-founder and company leader Sergie Brin for the failure of Glass. He was held responsible for over-exposing the product at launch while not listening to his own design team.

Both these articles make the common mistake of blaming failed new products on (1) the product itself, and (2) some high level leader that was a complete dunce. In these stories, like many others of failed products, a leader that had demonstrated keen insight, and was credited with brilliant work and decision-making, simply “went stupid” and blew it. Really?

Unfortunately there are a lot of new products that fail. Such simplistic explanations do not help business leaders avoid a future product flop. But there are common lessons to these stories from which innovators, and marketers, can learn in order to do better in the future. Especially when the new products are marketplace disrupters; or as they are often called, “game changers.”

Do you remember Segway? The two wheeled transportation device came on the market with incredible fanfare in 2002. It was heralded as a game changer in how we all would mobilize. Founders predicted sales would explode to 10,000 units per week, and the company would reach $1B in sales faster than ever in history. But that didn’t happen. Instead the company sold less than 10,000 units in its first 2 years, and less than 24,000 units in its first 4 years. What was initially a “really, really cool product” ended up a dud.

There were a lot of companies that experimented with Segways. The U.S. Postal Service tested Segways for letter carriers. Police tested using them in Chicago, Philadelphia and D.C., gas companies tested them for Pennsylvania meter readers, and Chicago’s fire department tested them for paramedics in congested city center. But none of these led to major sales. Segway became relegated to niche (like urban sightseeing) and absurd (like Segway polo) uses.

Segway tried to be a general purpose product. But no disruptive product ever succeeds with that sort of marketing. As famed innovation guru Clayton Christensen tells everyone, when you launch a new product you have to find a set of unmet needs, and position the new product to fulfill that unmet need better than anything else. You must have a very clear focus on the product’s initial use, and work extremely hard to make sure the product does the necessary job brilliantly to fulfill the unmet need.

Nobody inherently needed a Segway. Everyone was getting around by foot, bicycle, motorcycle and car just fine. Segway failed because it did not focus on any one application, and develop that market as it enhanced and improved the product. Selling 100 Segways to 20 different uses was an inherently bad decision. What Segway needed to do was sell 100 units to a single, or at most 2, applications.

Segway leadership should have studied the needs deeply, and focused all aspects of the product, distribution, promotion, training, communications and pricing for that single (or 2) markets. By winning over users in the initial market Segway could have made those initial users very loyal, outspoken customers who would recommend the product again and again – even at a $4,000 price.

Segway should have pioneered an initial application market that could grow. Only after that could Segway turn to a second market. The first market could have been using Segway as a golfer’s cart, or as a walking assist for the elderly/infirm, or as a transport device for meter readers. If Segway had really focused on one initial market, developed for those needs, and won that market it would have started a step-wise program toward more applications and success. By thinking the general market would figure out how to use its product, and someone else would develop applications for specific market needs, Segway’s leaders missed the opportunity to truly disrupt one market and start the path toward wider success.

The Fire Phone had a great opportunity to grow which it missed. The Fire Phone had several features making it great for on-line shopping. But the launch team did not focus, focus, focus on this application. They did not keep developing apps, databases and ways of using the product for retailing so that avid shoppers found the Fire Phone superior for their needs. Instead the Fire Phone was launched as a mass-market device. Its retail attributes were largely lost in comparisons with other general purpose smartphones.

The Fire Phone had a great opportunity to grow which it missed. The Fire Phone had several features making it great for on-line shopping. But the launch team did not focus, focus, focus on this application. They did not keep developing apps, databases and ways of using the product for retailing so that avid shoppers found the Fire Phone superior for their needs. Instead the Fire Phone was launched as a mass-market device. Its retail attributes were largely lost in comparisons with other general purpose smartphones.

People already had Apple iPhones, Samsung Galaxy phones and Google Nexus phones. Simultaneously, Microsoft was pushing for new customers to use Nokia and HTC Windows phones. There were plenty of smartphones on the market. Another smartphone wasn’t needed – unless it fulfilled the unmet needs of some select market so well that those specific users would say “if you do …. and you need…. then you MUST have a FirePhone.” By not focusing like a laser on some specific application – some specific set of unmet needs – the “cool” features of the Fire Phone simply weren’t very valuable and the product was easy for people to pass by. Which almost everyone did, waiting for the iPhone 6 launch.

This was the same problem launching Google Glass. Glass really caught the imagination of many tech reviewers. Everyone I knew who put on Glass said it was really cool. But there wasn’t any one thing Glass did so well that large numbers of folks said “I have to have Glass.” There wasn’t any need that Glass fulfilled so well that a segment bought Glass, used it and became religious about wearing Glass all the time. And Google didn’t improve the product in specific ways for a single market application so that users from that market would be attracted to buy Glass. In the end, by trying to be a “cool tool” for everyone Glass ended up being something nobody really needed. Exactly like Segway.

Microsoft recently launched its Hololens. Again, a pretty cool gadget. But, exactly what is the target market for Hololens? If Microsoft proceeds down the road of “a cool tool that will redefine computing,” Hololens will likely end up with the same fate as Glass, Segway and Fire Phone. Hololens marketing and development teams have to find the ONE application (maybe 2) that will drive initial sales, cater to that application with enhancements and improvements to meet those specific needs, and create an initial loyal user base. Only after that can Hololens build future applications and markets to grow sales (perhaps explosively) and push Microsoft into a market leading position.

Microsoft recently launched its Hololens. Again, a pretty cool gadget. But, exactly what is the target market for Hololens? If Microsoft proceeds down the road of “a cool tool that will redefine computing,” Hololens will likely end up with the same fate as Glass, Segway and Fire Phone. Hololens marketing and development teams have to find the ONE application (maybe 2) that will drive initial sales, cater to that application with enhancements and improvements to meet those specific needs, and create an initial loyal user base. Only after that can Hololens build future applications and markets to grow sales (perhaps explosively) and push Microsoft into a market leading position.

All companies have opportunities to innovate and disrupt their markets. Most fail at this. Most innovations are thrown at customers hoping they will buy, and then simply dropped when sales don’t meet expectations. Most leaders forget that customers already have a way of getting their jobs done, so they aren’t running around asking for a new innovation. For an innovation to succeed launchers must identify the unmet needs of an application, and then dedicate their innovation to meeting those unmet needs. By building a base of customers (one at a time) upon which to grow the innovation’s sales you can position both the new product and the company as market leaders.

by Adam Hartung | Aug 6, 2013 | Current Affairs, Defend & Extend, In the Swamp, Innovation, Leadership

Jeff Bezos, founder of Amazon worth $25.2B just paid $250 million to become sole owner of The Washington Post.

Some think the recent rash of of billionaires buying newspapers is simply rich folks buying themselves trophies. Probably true in some instances – and that benefits no one. Just look at how Sam Zell ruined The Chicago Tribune and Los Angeles Times. Or Rupert Murdoch's less than stellar performance owning The Wall Street Journal. It's hard to be excited about a financially astute commodities manager, like John Henry, buying The Boston Globe – as it has all the earmarks of someone simply jumping in where angels fear to tread.

These companies lost their way long ago. For decades they defined themselves as newspaper companies. They linked everything about what they did to printing a daily paper. The service they provided, which was a mix of hard news and entertainment reporting, was lost in the productization of that service into a print deliverable.

So when people started to look for news and entertainment on-line, these companies chose to ignore the trend. They continued to believe that readers would always want the product – the paper – rather than the service. And they allowed themselves to remain fixated on old processes and outdated business models long after the market shifted.

The leaders ignored the fact that advertisers could obtain much more directed placement at targets, at far lower cost, on-line than through the broad-based, general ads placed in newspapers. And that consumers could get a much faster, and cheaper, sale via eBay, CraigsList or Vehix.com than via overpriced classified ads.

Newspaper leadership kept trying to defend their "core" business of collecting news for daily publication in a paper format. They kept trying to defend their local advertising base. Even though every month more people abandoned them for an on-line format. Not one major newspaper headmast made a strong commitment to go on-line. None tried to be #1 in news dissemination via the web, or take a leadership role in associating ad placement with news and entertainment.

They could have addressed the market shift, and changed their approach and delivery. But they did not.

Money manager Mr. Henry has done a good job of turning the Boston Red Sox into a profitable institution. But there is nothing in common between the Red Sox, for which you can grow the fan base, bring people to the ballpark and sell viewing rights, and The Boston Globe. The former is unique. The latter is obsolete. Yes, the New York Times company paid $1.1B for the Globe in 1993, but that doesn't mean it's worth $70M today. Given its revenue and cost structure, as a newspaper it is probably worth nothing.

But, we all still want news. Nobody wants the information infrastructure collecting what we need to know to crumble. Nobody wants journalism to die. But it is unreasonable to expect business people to keep investing in newspapers just to fulfill a public good. Even Mr. Zell abandoned that idea.

Thus, we need the news, as a service, to be transformed into a new, profitable enterprise. Somehow these organizations have to abandon the old ways of doing things, including print and paper distribution, and transform to meet modern needs. The 6 year revenue slide at Washington Post has to stop, and instead of thinking about survival company leadership needs to focus on how to thrive with a new, profitable business model.

And that's why we all should be glad Jeff Bezos bought The Washington Post. As head of Amazon.com The Harvard Business Review ranked him the second best performing CEO of the last decade. CNNMoney.com named him Business Person of the Year 2012, and called him "the ultimate disruptor."

By not doing what everyone else did, breaking all the rules of traditional retail, Mr. Bezos built Amazon.com into a $61B general merchandise retailer in 20 years. When publishers refused to create electronic books he led Amazon into competing with its suppliers by becoming a publisher. When Microsoft wouldn't produce an e-reader, retailer and publisher Amazon.com jumped into the intensely competitive world of personal electroncs creating and launching Kindle. And then upped the stakes against competitors by enhancing that into Kindle Fire. And when traditional IT suppliers like HP and Dell were slow to help small (or any) business move toward cloud computing Amazon launched its own network services to help the market shift.

Mr. Bezos' language regarding his intentions post acquisition are quite telling, "change… is essential… with or without new ownership….need to invent…need to experiment."

And that is exactly what the news industry needs today. Today's leaders are HuffingtonPost.com, Marketwatch.com and other web sites with wildly different business models than traditional paper media. WaPo success will require transforming a dying company, tied to an old success formula, into a trend-aligned organization that give people what they want, when they want it, at a profit.

And it's hard to think of someone better experienced, or skilled, than Jeff Bezos to provide that kind of leadership. With just a little imagination we can imagine some rapid moves:

- distribution of all content via Kindle style eReaders, rather than print. Along with dramatically increasing the cost of paper subscriptions and daily paper delivery

- Instead of a "one size fits all" general purpose daily paper, packaging news into more fitting targeted products. Sports stories on sports sites. Business stories on business sites. Deeper, longer stories into ebooks available for $.99 purchase. And repackaging of stories that cover longer time spans into electronic short-books for purchase.

- Packaging content into Facebook locations for targeted readers. Tying ads into these social media sites, and promoting ad sales for small, local businesses to the Facebook sites.

- Or creating an ala carte approach to buying various news and entertainment in an iTunes or Netflix style environment (or on those sites)

- Robustly attracting readers via connecting content with social media, including Twitter, to meet modern needs for immediacy, headline knowledge and links to deeper stories — with sales of ads onto social media

- Tying electronic coupons, and buy-it-now capabilities to ads linked to appropriate content

- Retargeting advertising sales from general purpose to targeted delivery at specific readers, with robust packages of on-line coupons, links to specials and fast, impulse purchase capability

- Increased use of bloggers and ad hoc writers to supplement staff in order to offer opinions and insights quickly, but at lower cost.

- Changes in compensation linked to page views and readership, just as revenue is linked to same.

We've watched a raft of newspapers and magazines disappear. This has not been a failure of journalism, but rather a failure of business leaders to address shifting markets and transform old organizations to meet modern needs. It's not a quality problem, but rather a failure of strategy to adapt to shifting markets. And that's a lesson every business leaders needs to note, because today, as I wrote in April, 2012, every company has to behave like a tech company!

Doing more of the same, cutting costs and rich egos won't fix a newspaper. Only the willingness to experiment and find new solutions which transform these organizations into something very different, well beyond print, will work. Let's hope Mr. Bezos brings the same zest for addressing these challenges and aligning with market needs he brought to Amazon. To a large extent, the future of news and "freedom of the press" may well depend upon it.

by Adam Hartung | Dec 10, 2012 | Current Affairs, Defend & Extend, In the Whirlpool, Leadership, Lifecycle, Television

Remember when almost everyone read a daily newspaper?

Newspaper readership peaked around 2000. Since then printed media has declined, as readers shifted on-line. Magazines have folded, and newspapers have disappeared, quit printing, dramatically cut page numbers and even more dramatically cut staff.

Amazingly, almost no major print publisher prepared for this, even though the trend was becoming clear in the late 1990s.

Newspapers are no longer a viable business. While industry revenue grew for

almost 2 centuries, it collapsed in a mere decade.

Chart Source: BusinessInsider.com

This market shift created clear winners, and losers. On-line news sites like Marketwatch and HuffingtonPost were clear winners. Losers were traditional newspaper companies such as Tribune Corporation, Gannett, McClatchey, Dow Jones and even the New York Times Company. And investors in these companies either saw their values soar, or practically disintegrate.

In 2012 it is equally clear that television is on the brink of a major transition. Fewer people are content to have their entertainment programmed for them when they can program it themselves on-line. Even though the number of television channels has exploded with pervasive cable access, the time spent watching television is not growing. While simultaneously the amount of time people spend looking at mobile internet displays (tablets, smartphones and laptops) is growing at double digit rates.

Chart Source: Silicone Alley Insider Chart of the Day 12/5/12

It would be easy to act like newspaper defenders and pretend that television as we've known it will not change. But that would be, at best, naive. Just look around at broadband access, the use of mobile devices, the convenience of mobile and the number of people that don't even watch traditional TV any more (especially younger people) and the trend is clear. One-way preprogrammed advertising laden television is not a sustainable business.

So, now is the time to prepare. And change your business to align with impending new realities.

Losers, and winners, will be varied – and not entirely obvious. Firstly, a look at those trying to maintain the status quo, and likely to lose the most.

Giant consumer goods and retail companies benefitted from the domination of television. Only huge companies like P&G, Kraft, GM and Target could afford to lay out billions of dollars for television ads to build, and defend, a brand. But what advantage will they have when TV budgets no longer control brand building? They will become extremely vulnerable to more innovative companies that have better products and move on fast lifecycles. Their size, hierarchy and arcane business practices will lead to huge problems. Imagine a raft of new Hostess Brands experiences.

Even as the trends have started changing these companies have continued pumping billions into the traditional TV networks as they spend to defend their brand position. This has driven up the value of companies like CBS, Comcast (owns NBC) and Disney (owns ABC) over the last 3 years substantially. But don't expect that to last forever. Or even a few more years.

Just like newspaper ad spending fell off a cliff when it was clear the eyeballs were no longer there, expect the same for television ad spending. As giant advertisers find the cost of television harder and harder to justify their outlays will eventually take the kind of cliff dive observed in the chart (above) for newspaper advertising. Already some consumer goods and ad agency executives are alluding to the fact that the rate of return on traditional TV is becoming sketchy.

So far, we've seen little at the companies which own TV networks to demonstrate they are prepared for the floor to fall out of their revenue stream. While some have positions in a few internet production and delivery companies, most are clearly still doing their best to defend & extend the old business – just like newspaper owners did. Just as newspapers never found a way to replace the print ad dollars, these television companies look very much like businesses that have no apparent solution for future growth. I would not want my 401K invested in any major network company.

And there will be winners.

For smaller businesses, there has never been a better time to compete. A company as small as Tesla or Fisker can now create a brand on-line at a fraction of the old cost. And that brand can be as powerful as Ford, and potentially a lot more trendy. There are very low entry barriers for on-line brand building using not only ad words and web page display ads, but also using social media to build loyal followers who use and promote a brand. What was once considered a niche can become well known almost overnight simply by applying the new dynamics of reaching customers on-line, and increasingly via mobile. Look at the success of Toms Shoes.

Zappos and Amazon have shown that with almost no television ads they can create powerhouse retail brands. The new retailers do not compete just on price, but are able to offer selection, availability and customer service at levels unachievable by traditional brick-and-mortar retailers. They can suggest products and prices of things you're likely to need, even before you realize you need them. They can educate better, and faster, than most retail store employees. And they can offer great prices due to less overhead, along with the convenience of shipping the product right into your home.

And as people quit watching preprogrammed TV, where will they go for content? Anybody streaming will have an advantage – so think Netflix (which recently contracted for all the Disney content,) Amazon, Pandora, Spotify and even AOL. But, this will also benefit those companies providing content access such as Apple TV, Google TV, YouTube (owned by Google) to offer content channels and the increasingly omnipresent Facebook will deliver up not only friends, but content — and ads.

As for content creation, the deep pockets of traditional TV production companies will likely disappear along with their ability to control distribution. That means fewer big-budget productions as risk goes up without revenue assurances.

But that means even more ability for newer, smaller companies to create competitive content seeking audiences. Where once a very clever, hard working Seth McFarlane (creator of Family Guy) had to hardscrabble with networks to achieve distribution, and live in fear of a single person controlling his destiny, in the future these creative people will be able to own their content and capture the value directly as they build a direct audience. A phenomenon like George Lucas will be more achievable than ever before as what might look like chaos during transition will migrate to a much more competitive world where audiences, rather than network executives, will decide what content wins – and loses.

So, with due respects to Don McLean, will today be the day TV Died? We will only know in historical context. Nobody predicted newspapers had peaked in 2000, but it was clear the internet was changing news consumption behavior. And we don't know if TV viewership will begin its rapid decline in 2013, or in a couple more years. But the inevitable change is clear – we just don't know exactly when.

So it would be foolish to not think that the industry is going to change dramatically. And the impact on advertising will be even more profound, much more profound, than it was in print. And that will have an even more profound impact on American society – and how business is done.

What are you doing to prepare?

by Adam Hartung | Jul 8, 2011 | Books, Current Affairs, In the Rapids, Leadership, Lifecycle, Openness, Transparency, Web/Tech, Weblogs

Evolution doesn’t happen like we think. It’s not slow and gradual (like line A, below.) Things don’t go from one level of performance slowly to the next level in a nice continuous way. Rather, evolutionary change happens brutally fast. Usually the potential for change is building for a long time, but then there is some event – some environmental shift (visually depcted as B, below) – and the old is made obsolete while the new grows aggressively. Economists call this “punctuated equilibrium.” Everyone was on an old equilibrium, then they quickly shift to something new establishing a new equilibrium.

Momentum has been building for change in publishing for several years. Books are heavy, a pain to carry and often a pain to buy. Now eReaders, tablets and web downloads have changed the environment. And in June J.K. Rowling, author of those famous Harry Potter books, opened her new web site as the location to exclusively sell Harry Potter e-books (see TheWeek.com “How Pottermore Will Revolutionized Publishing.”)

Momentum has been building for change in publishing for several years. Books are heavy, a pain to carry and often a pain to buy. Now eReaders, tablets and web downloads have changed the environment. And in June J.K. Rowling, author of those famous Harry Potter books, opened her new web site as the location to exclusively sell Harry Potter e-books (see TheWeek.com “How Pottermore Will Revolutionized Publishing.”)

Ms. Rowling has realized that the market has shifted, the old equilibrium is gone, and she can be part of the new one. She’ll let the dinosaur-ish publisher handle physical books, especially since Amazon has already shown us that physical books are a smaller market than ebooks. Going forward she doesn’t need the publisher, or the bookstore (not even Amazon) to capture the value of her series. She’s jumping to the new equilibrium.

And that’s why I’m encouraged about AOL these days. Since acquiring The Huffington Post company, things are changing at AOL. According to Forbes writer Jeff Bercovici, in “AOL After the Honeymoon,” AOL’s big slide down in users has begun to reverse direction. Many were surprised to learn, as the FinancialPost.com recently headlined, “Huffington Post Outstrips NYT Web Traffic in May.”

Source: BusinessInsider.com

The old equilibrium in news publishing is obsolete. Those trying to maintain it keep failing, as recently headlined on PaidContent.org “Citing Weak Economy, Gannett Turns to Job Cuts, Furloughs.” Nobody should own a traditional publisher, that business is not viable.

But Forbes reports that Ms. Huffington has been given real White Space at AOL. She has permission to do what she needs to do to succeed, unbridled by past AOL business practices. That has included hiring a stable of the best talent in editing, at high pay packages, during this time when everyone else is cutting jobs and pay for journalists. This sort of behavior is anethema to the historically metric-driven “AOL Way,” which was very industrial management. That sort of permission is rarely given to an acquisition, but key to making it an engine for turn-around.

And HuffPo is being given the resources to implement a new model. Where HuffPo was something like 70 journalists, AOL is now cranking out content from some 2,000 journalists and editors! More than The Washington Post or The Wall Street Journal. Ms. Huffington, as the new leader, is less about “managing for results” looking at history, and more about identifying market needs then filling them. By giving people what they want Huffington Post is accumulating readers – which leads to display ad revenue. Which, as my last blog reported, is the fastest growing area in on-line advertising

Where the people are, you can find advertsing. As people are shift away from newspapers, toward the web, advertising dollars are following. Internet now trails only television for ad dollars – and is likely to be #1 soon:

Chart source: Business Insider

So now we can see a route for AOL to succeed. As traditional AOL subscribers disappear – which is likely to accelerate – AOL is building out an on-line publishing environment which can generate ad revenue. And that’s how AOL can survive the market shift. To use an old marketing term, AOL can “jump the curve” from its declining business to a growing one.

This is by no means a given to succeed. AOL has to move very quickly to create the new revenues. Subscribers and traditional AOL ad revenues are falling precipitously.

Source: Forbes.com

But, HuffPo is the engine that can take AOL from its dying business to a new one. Just like we want Harry Potter digitally, and are happy to obtain it from Ms. Rowlings directly, we want information digitally – and free – and from someone who can get it to us. HuffPo is now winning the battle for on-line readers against traditional media companies. And it is expanding, announced just this week on MediaPost.com “HuffPo Debuts in the UK.” Just as the News Corp UK tabloid, News of the World, dies (The Guardian – “James Murdoch’s News of the World Closure is the Shrewdest of Surrenders.“)

News Corp. once had a shot at jumping the curve with its big investment in MySpace. But leadership wouldn’t give MySpace permission and resources to do whatever it needed to do to grow. Instead, by applying “professional management” it limited MySpace’s future and allowed Facebook to end-run it. Too much energy was spent on maintaining old practices – which led to disaster. And that’s the risk at AOL – will it really keep giving HuffPo permission to do what it needs to do, and the resources to make it happen? Will it stick to letting Ms. Huffington build her empire, and focus on the product and its market fit rather than short-term revenues? If so, this really could be a great story for investors.

So far, it’s looking very good indeed.