by Adam Hartung | May 30, 2017 | Innovation, Lifecycle

Last week Microsoft announced its new Surface Pro 5 tablet would be available June 15. Did you miss it? Do you care?

Do you remember when it was a big deal that a major tech company released a new, or upgraded, device? Does it seem like increasingly nobody cares?

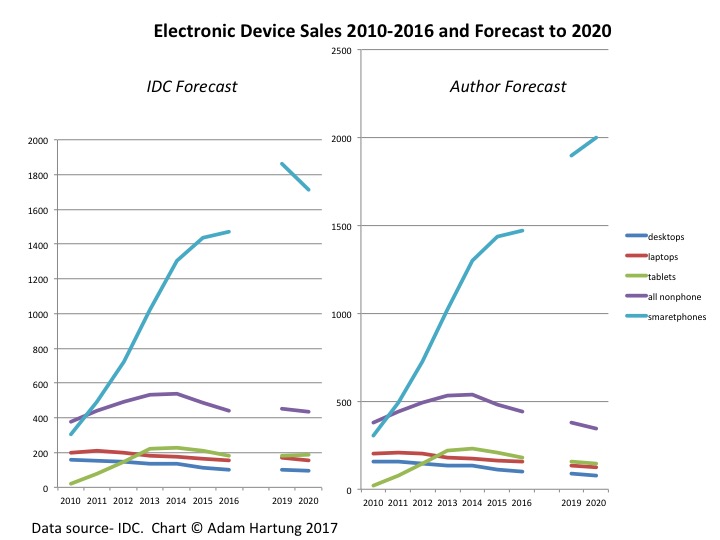

Non-phone device sales are declining, while smartphone sales accelerate

This chart compares IDC sales data, and forecasts, with adjustments to the forecast made by the author. The adjustments offer a fix to IDC’s historical underestimates of PC and tablet sales declines, while simultaneously underestimating sales growth in smartphones.

Since 2010 people are buying fewer desktops and laptops. And after tablet sales ramped up through 2013, tablet purchases have declined precipitously as well. Meanwhile, since 2014 sales of smartphones have doubled, or more, sales of all non-phone devices. And it’s also pretty clear that these trends show no signs of changing.

Why such a stark market shift? After all desktop and laptop sales grew consistently for some 3 decades. Why are they in such decline? And why did the tablet market make such a rapid up, then down movement? It seems pretty clear that people have determined they no longer need large internal hard drives to work locally, nor big keyboards and big screens of non-phone devices. Instead, they can do so much with a phone that this device is becoming the only one they need.

Today a new desktop starts at $350-$400. Laptops start as low as $180, and pretty powerful ones can be had for $500-$700. Tablets also start at about$180, and the newest Microsoft Surface 5 costs $800. Smartphones too start at about $150, and top of the line are $600-$800. So the purchase decision today is not based on price. All devices are more-or-less affordable, and with a range of capabilities that makes price not the determining factor.

Smartphones let most people do most of what they need to do

Every month the Internet-of-Things (IoT) is putting more data in the cloud. And developers are figuring out how to access that data from a smartphone. And smartphone apps are making it increasingly easy to find data, and interact with it, without doing a lot of typing. And without doing a lot of local processing like was commonplace on PCs. Instead, people access the data – whether it is financial information, customer sales and order data, inventory, delivery schedules, plant performance, equipment performance, maintenance specs, throughput, other operating data, web-based news, weather, etc. — via their phone. And they are able to analyze the data with apps they either buy, or that their companies have built or purchased, that don’t rely on an office suite.

Additionally, people are eschewing the old forms of connecting — like email, which benefits from a keyboard — for a combination of texting and social media sites. Why type a lot of words when a picture and a couple of emojis can do the trick?

And nobody listens to CD-based, or watches DVD-based, entertainment any longer. They either stream it live from an app like Pandora, Spotify, StreamUp, Ustream, GoGo or Facebook Live, or they download it from the cloud onto their phone.

To obtain additional insight into just how prevalent this shift to smartphones has become look beyond the USA. According to IDC there are about 1.8 billion smartphone users globally. China has nearly 600M users, and India has over 300 million users — so they account for at least half the market today. And those markets are growing by far the fastest, increasing purchases every quarter in the range of 15-25% more than previous years.

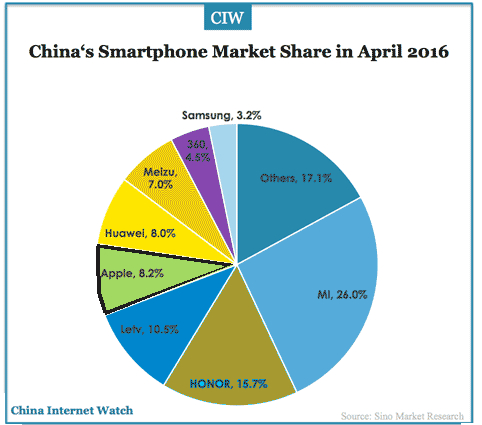

Chinese manufacturers are rapidly catching up to Apple and Samsung – there will be losers

Clayton Christensen often discusses how technology developers “overshoot” user needs. Early market leaders keep developing enhancements long after their products do all people want, producing upgrades that offer little user benefit. And that has happened with PCs and most tablets. They simply do more than people need today, due to the capabilities of the cloud, IoT and apps. Thus, in markets like China and India we see the rapid uptake of smartphones, while demand for PCs, laptops and tablets languish. People just don’t need those capabilities when the smartphone does what they want — and provides greater levels of portability and 24×7 access, which are benefits greatly treasured.

And that is why companies like Microsoft, Dell and HP really have to worry. Their “core” products such as Windows, Office, PCs, laptops and tablets are getting smaller. And these companies are barely marginal competitors in the high growth sales of smartphones and apps. As the market shifts, where will their revenues originate? Cloud services, versus Amazon AWS? Game consoles?

Even Apple and Samsung have reasons to worry. In China Apple has 8.4% market share, while Samsung has 6%. But the Chinese suppliers Oppo, Vivo, Huawei and Xiaomi have 58.4%. And as 2016 ended Chinese manufacturers, including Lenovo, OnePlus and Gionee, were grabbing over 50% of the Indian market, while Samsung has about 20% and Apple is yet to participate. How long will Apple and Samsung dominate the global market as these Chinese manufacturers grow, and increase product development?

When looking at trends it’s easy to lose track of the forest while focusing on individual trees. Don’t become mired in the differences, and specs, comparing laptops, hybrids, tablets and smartphones. Recognize the big shift is away from all devices other than smartphones, which are constantly increasing their capabilities as cloud services and IoT grows. So buy what suits your, and your company’s, needs — without “overbuying” because capabilities just keep improving. And keep your eyes on new, emerging competitors because they have Apple and Samsung in their sites.

by Adam Hartung | Oct 4, 2011 | Current Affairs, Defend & Extend, Film, In the Rapids, Innovation, Leadership, Television, Transparency, Web/Tech

Reed Hastings, the CEO of Netflix, has long been considered a pretty good CEO. In January, 2009 his approval ranking, from Glassdoor, was an astounding 93%. In January, 2010 he was still on the top 25 list, with a 75% approval rating. And it's not surprising, given that he had happy employees, happy customers, and with Netflix's successful trashing of Blockbuster the company's stock had risen dramaticall,y leading to very happy investors.

But that was before Mr. Hastings made a series of changes in July and September. First Netflix raised the price on DVD rentals, and on packages that had DVD rentals and streaming download, by about $$6/month. Not a big increase in dollar terms, but it was a 60% jump, and it caught a lot of media attention (New York Times article). Many customers were seriously upset, and in September Netflix let investors know it had lost about 4% of its streaming subscribers, and possibly as many as 5% of its DVD subscribers (Daily Mail).

No investor wants that kind of customer news from a growth company, and the stock price went into a nosedive. The decline was augmented when the CEO announced Netflix was splitting into 2 companies. Netflix would focus on streaming video, and Quikster would focus on DVDs. Nobody understood the price changes – or why the company split – and investors quickly concluded Netflix was a company out of control and likely to flame out, ruined by its own tactics in competition with Amazon, et.al.

(Source: Yahoo Finance 3 October, 2011)

(Source: Yahoo Finance 3 October, 2011)

This has to be about the worst company communication disaster by a market leader in a very, very long time. TVWeek.com said Netflix, and Reed Hastings, exhibited the most self-destructive behavior in 2011 – beyond even the Charlie Sheen fiasco! With everything going its way, why, oh why, did the company raise prices and split? Not even the vaunted New York Times could figure it out.

But let's take a moment to compare Netflix with another company having recent valuation troubles – Kodak.

Kodak invented home photography, leading it to tremendous wealth as amature film sales soared for seveal decades. But last week Kodak announced it was about out of cash, and was reaching into its revolving credit line for some $160million to pay bills. This latest financial machination reinforced to investors that film sales aren't what they used to be, and Kodak is in big trouble – possibly facing bankruptcy. Kodak's stock is down some 80% this year, from $6 to $1 – and quite a decline from the near $80 price it had in the late 1990s.

(Source: Yahoo Finance 10-3-2011)

Why Kodak declined was well described in Forbes. Despite its cash flow and company strengths, Kodak never succeeded beyond its original camera film business. Heck, Kodak invented digital photography, but licensed the technology to others as it rabidly pursued defending film sales. Because Kodak couldn't adapt to the market shift, it now is probably going to fail.

And that is why it is worth revisiting Netflix. Although things were poorly explained, and certainly customers were not handled well, last quarter's events are the right move for investors in the shifting at-home video entertainment business:

- DVD sales are going the direction of CD's and audio cassettes. Meaning down. It is important Netflix reap the maximum value out of its strong DVD position in order to fund growth in new markets. For the market leader to raise prices in low growth markets in order to maximize value is a classic strategic step. Netflix should be lauded for taking action to maximize value, rather than trying to defend and extend a business that will most likely disappear faster than any of us anticipate – especially as smart TVs come along.

- It is in Netflix's best interest to promote customer transition to streaming. Netflix is the current leader in streaming, and the profits are better there. Raising DVD prices helps promote customer shifting to the new technology, and is good for Netflix as long as customers don't change to a competitor.

- Although Netflix is currently the leader in streaming it has serious competition from Hulu, Amazon, Apple and others. It needs to build up its customer base rapidly, before people go to competitors, and it needs to fund its streaming business in order to obtain more content. Not only to negotiate with more movie and TV suppliers, but to keep funding its exclusive content like the new Lillyhammer series (more at GigaOm.com). Content is critical to maintaining leadership, and that requires both customers and cash.

- Netflix cannot afford to muddy up its streaming strategy by trying to defend, and protect, its DVD business. Splitting the two businesses allows leaders of each to undertake strategies to maximize sales and profits. Quikster will be able to fight Wal-Mart and Redbox as hard as possible, and Netflix can focus attention on growing streaming. Again, this is a great strategic move to make sure Netflix transitions from its old DVD business into streaming, and doesn't end up like an accelerated Kodak story.

Historically, companies that don't shift with markets end up in big trouble. AB Dick and Multigraphics owned small offset printing, but were crushed when Xerox brought out xerography. Then, afater inventing desktop publishing at Xerox PARC, Xerox was crushed by the market shift from copiers to desktop printers – a shift Xerox created. Pan Am, now receiving attention due to the much hyped TV series launch, failed when it could not make the shift to deregulation. Digital Equipment could not make the shift to PCs. Kodak missed the shift from film to digital. Most failed companies are the result of management's inability to transition with a market shift. Trying to defend and extend the old marketplace is guaranteed to fail.

Today markets shift incredibly fast. The actions at Netflix were explained poorly, and perhaps taken so fast and early that leadership's intentions were hard for anyone to understand. The resulting market cap decline is an unmitigated disaster, and the CEO should be ashamed of his performance. Yet, the actions taken were necessary – and probably the smartest moves Netflix could take to position itself for long-term success.

Perhaps Netflix will fall further. Short-term price predictions are a suckers game. But for long-term investors, now that the value has cratered, give Netflix strong consideration. It is still the leader in DVD and streaming. It has an enormous customer base, and looks like the exodus has stopped. It is now well organized to compete effectively, and seek maximum future growth and value. With a better PR firm, good advertising and ongoing content enhancements Netflix has the opportunity to pull out of this communication nightmare and produce stellar returns.

by Adam Hartung | Sep 22, 2010 | Current Affairs, Defend & Extend, Film, In the Whirlpool, Leadership, Lifecycle, Lock-in, Music, Web/Tech

Summary:

- Video retailer Blockbuster (and competitor Hollywood Video) are now bankrupt

- Video rentals/sales are at an all time high – but via digital downloads not DVDs

- Nokia, once the cell phone industry leader, is in deep trouble and risk of failure

- Yet mobile use (calls, texts, internet access, email) is at an all time high

- These companies are victims of locking-in to old business models, and missing a market shift

- Commitment to defending your old business can cause failure, even when participating in high growth markets, if you don’t anticipate, embrace and participate in market shifts

- Lock-in is deadly. It can cause you to ignore a market shift.

According to YahooNews, “Blockbuster Video to File Chapter 11.” In February, Movie Gallery – the owner of primary in-kind competitor Hollywood Video – filed for bankruptcy. It’s now decided to liquidate.

The cause is market shift. Netflix made it possible to rent DVDs without the cost of a store – as has the kiosk competitor Red Box. But everyone knows that is just a stopgap, because Netflix and Hulu are leading us all toward a future where there is no physical product at all. We’ll download the things we want to watch. The market is shifting from physical items – video cassettes then DVDs – to downloads. And both Blockbuster and Hollywood Video missed the shift.

Blockbuster (or Hollywood) could have gotten into on-line renting, or kiosks, like its competition. It even could have used profits to be an early developer of downloadable movies. Nothing stopped Blockbuster from investing in YouTube. Except it’s commitment to its Success Formula – as a brick-and-mortar retailer that rented or sold physically reproduced entertainment. Lock-in. And for that commitment to its historical Success Formula the investors now will get a great big goose egg – and employees will get to be laid off – and the thousands of landlords will be left in the lurch, unprepared.

As predictable as Blockbuster was, we can be equally sure about the future of former powerhouse Nokia. Details are provided in the BusinessWeek.com article “How Nokia Fell from Grace.” As the cell phone business exploded in the 1990s Nokia was a big winner. Revenues grew fivefold between 1996 and 2001 as people around the globe gobbled up the new devices. Another example of the fact that when you enter a high growth market you don’t have to be good – just in the right market at the right time.

But the cell phone business has become the mobile device business. And Nokia didn’t anticipate, prepare for or participate in the market shift. From market dominance, it has become an also-ran. The article author blames the failure, and decline, on complacent management. Weak explanation. You can be sure the leadership and management at Nokia was doing all it possibly could to Defend & Extend its cell phone business. The problem is that D&E management doesn’t work when customers simply walk away to a new technology. It may take a few years, and government subsidies may extend Nokia’s life even longer, but Nokia has about as much chance of surviving its market shift as Blockbuster did.

When companies stumble management sees the problems. They know results are faltering. But for decades management has been trained to think that the proper response is to “knuckle down, cut costs, defend the current business at all cost.” Yet, there are more movies rented now than ever – and Blockbuster is failing despite enormous market growth. There are more mobile telephony minutes, text messages, remote emails and mobile internet searches than ever in history – yet Nokia is doing remarkably poorly. It’s not a market problem, it’s a problem of Lock-in to a solution that is now outdated. When the old supplier didn’t give the market what it wanted, the customers went elsewhere. And unwillingness to go with them has left these companies in tatters.

These markets are growing, yet the purveyors of old solutions are failing primarily because they stuck to defending their old business too long. They did not embrace the market shift, and cannibalize historical product sales to enter the new, higher growth markets. Because they chose to protect their “core,” they failed. New victims of Lock-in.

by Adam Hartung | Apr 20, 2009 | Current Affairs, Defend & Extend, Film, General, In the Swamp, Leadership, Lock-in, Television

How do you pick a movie to see – whether at the theatre or at home? The movie studios think you pick movies by what you see on TV ads, according to the Los Angeles Times "Studios struggle to rein in marketing costs."

I remember the old days when my friends and I grabbed a newspaper and shopped the ads looking for a flick to go see. And we were influenced by television ads as well. But, as time went by, we started asking each other, "Is that movie any good, or are all the best parts in the ad?" (Admit it, you've asked that question too.) Then we found out we could get sneak peaks from shows like "Siskel & Ebert at the movies," so one of us would try to watch that and see if we liked the longer scenes. And we didn't ever agree with the critics, but we could listen to hear if they described a movie we would like. Now, not only myself but my sons follow the same routine. Only we go to the internet looking for a YouTube! clip, and for reviews from all kinds of people – not just critics. Mostly when we see a TV ad we hit the mute button.

Everywhere, businesses are still wasting money on old business notions. For movie studios, they keep trying to get people to watch a big budget by advertising the thing. (To death. Until nobody watches the ad any more because they have it memorized. And get angry that the ad keeps showing.) But even the above article admits that studios know this isn't the best way any more. With the internet around, we all listen less to advertisements, and gain access to more real input. From web sites, or Twitter, or friends on Facebook, or colleagues on Linked-in. We watch a lot less TV, and what we watch is more targeted to our interest and available on cable. Or we download our TV from the web using Hulu.com. Yet, the studios are so Locked-in to their outdated Success Formula that they keep spending money on TV ads – even though they know the value isn't there any more.

So why do the studios spend so much on advertising? Because they always have. That's Lock-in. Lacking a better idea, a better plan, a better approach that would really reach out to potential viewers they keep doing what they know how to do, even as they question whether or not they should do it! The industrial era concept was "I spent a fortune making this movie, and distributing it into theatres, so I better not stop now. Keep spending money to advertise it, create awareness, and get people into the theatres." The studios see movie making as an industrial enterprise, where those who spend the most have the greatest chance of winning. Spend a lot to make, spend to distribute, spend to advertise. To industrial era thinkers, all this spending creates entry barriers that defends their business.

And that's why movie studios struggle. It's unclear how well those ideas ever worked for filmmaking – because we all saw our share of blockbuster bombs and remember the "American Graffiti" or "Blair Witch Project" that was cheap and good. But for sure we all know the world has now permanently shifted. Today, small budget movies like "Slum Dog Millionaire" can be made (offshore in that case – but not necessarily) quite well. The pool of new actors, writers, directors, cinematographers and editors keeps growing – driving production quality up and cost down. And distribution can be via DVD – or web download – between low cost and free. A movie doesn't even have to be shown in a theatre for it to be commercially successful any more. And any filmmaker can promote her product on the internet, building a word of mouth driving popularity and sales.

From filmmaking to recordings to short programs to books, the market has shifted. Things don't have to be big budget to be good. The old status quo police, like Mr. Goldwyn or Mr. Meyer, simply have far less role. Digitization and globalization means that you don't need film for movies – or paper for books. Thus, democratizing the production, as well as sales, of "media" products. Thus the old media companies are struggling (publishers, filmmakers, magazines, newspapers and recording studios) because they no longer have the "entry barriers" they can Defend to allow their old Success Formulas to produce above average returns. And they never will again. The world has changed, and the market has permanently shifted.

Is your business still spending money on things that don't matter? Does your approach to the market, your Success Formula dictate spending on advertising, salespeople, PR, external analysts, paid reviewers or others that really don't make nearly as much difference any more? When will you change your approach? The movie studios are preparing to spend hundreds of millions of dollars on summer ad promotions for new movies. Is this necessary, given that the downturn has increased the demand for escapist entertainment? Is your business doing the same?

If you want to cut your cost, you shouldn't cut 5% or 10% across the board. That won't help your Success Formula meet market needs better. Instead, you need to understand market shifts and cut 90% from things that no longer matter – or that have diminishing value. Quit doing the things you do because you always did them, and make sure you do the things you need to do. You want to be the next "Slumdog Millionaire" not the next "Ishtar." You want to be Apple, not Motorola. You want to be Google, not Tribune Corporation. Spend money on what pays off, not what you've always spent it on.