by Adam Hartung | Nov 7, 2016 | Advertising, Election, Marketing

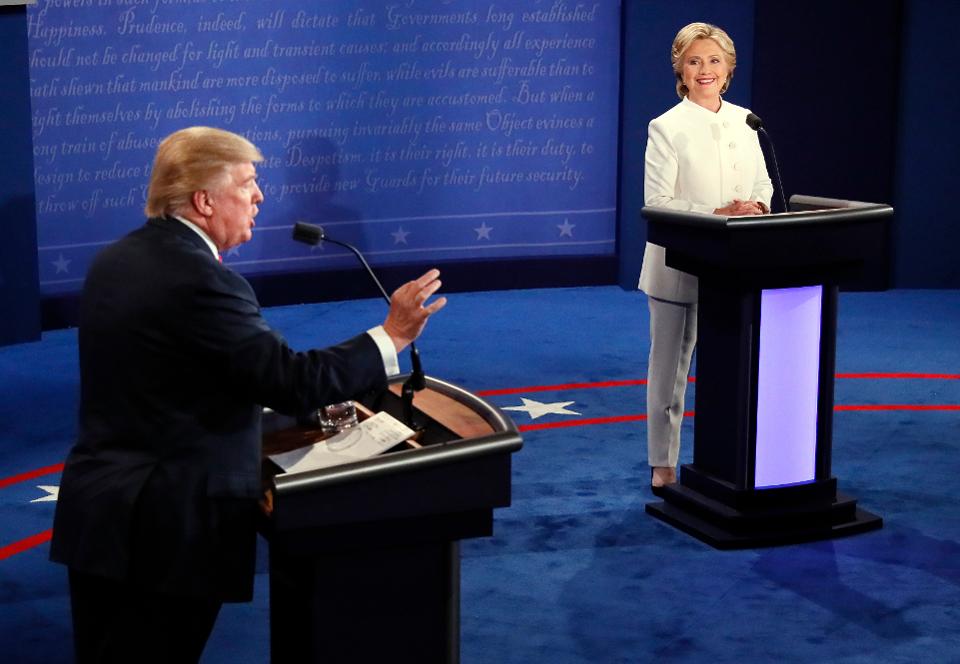

Republican presidential nominee Donald Trump debates Democratic presidential nominee Hillary Clinton during the third presidential debate. (Mark Ralston/Pool via AP)

Whoever wins tomorrow’s election, their success will have a lot to do with how they marketed their campaign. And in many ways, selling a candidate is not different from selling anything else.

Do you remember the “four Ps of marketing” from Marketing 101? They are product, price, place and promotion. Every newbie is taught not to overly rely on any one, and greatest success comes from a well planned use of all four.

Product: The candidates are about the same age and health. And while they represent very different parties, both have spent less time talking about what a great president they would be, and a lot more on what a terrible product the other candidate is. Message after message has denigrated the other, to the point where we hear most of the electorate is now less than happy with both.

Most marketers know that negative marketing is risky, because it tends to tar all products with similar negatives. Greatest sales happen when you convince people your product is superior in its own right – not just compared to alternatives. Barack Obama figured this out in both previous elections, and he was able to convince the majority of people he would be a good president. Unfortunately, in this election the competitive attacks have cancelled each other out, and neither candidate has a majority of people liking them. An opportunity lost by both candidates to make their product more appealing, and thus bringing out more people to vote for them based on policies and the core of how their presidency would make voters happy.

Price: One could say that the tax policies of Hillary Clinton make her a more expensive candidate than Donald Trump. However, the long-term cost of the debt increase from Trump means that the price of his presidency will be costlier than Clinton. Let’s just be practical and say that neither candidate has positioned themselves as the candidate better for everyone’s pocketbook.

Again, an opportunity lost. Ronald Reagan did a superb job of positioning himself as being good for people’s pocketbooks, and it helped him unseat Jimmy Carter. Barack Obama made hay out of the economic crisis as Republican George Bush left office, helping him convince voters that he would be far better for their pocketbooks – via job creation – than his opponent.

Place: This is all about “get out the vote.” Here the advantage clearly goes to Clinton. Candidate Clinton has done a superb job of building a “machine” that has turned out a record number of Democrats to early vote. And she has worked diligently with her party to make sure local support exists across the country to help take people to the polls, and encourage voting on election day. By making sure her constituents make it to vote, she will likely do far better at collecting votes than her opponent.

Additionally, candidate Clinton is not only campaigning, but she has a two former presidents campaigning for her, a sitting first lady, a sitting vice president and her key opponent from the primaries. This breadth of support, canvasing across multiple states, further puts her message into voters ears right before the election, and encourages people to go vote for her tomorrow. Her large fundraising, and ability to offer funds to down-ticket candidates, has helped make sure her message was clear at the local level.

On the other hand, candidate Trump is walking a nearly singular path, with precious little party support. While he swept the primaries, he has not built a strong machine to make sure that those beyond the party faithful – those who are undecided or independent – are going to make it to the voting booth to help him be elected. It is one thing to excite people about your product, it is another to make sure people actually invest the resources to obtain it.

In Trump’s case the advertising has been relentless, but the local machine support to turn out registered party voters, and everyone else who might enjoy his candidacy, is quite weak. One reason candidate Trump keeps saying the election is “rigged” is because he’s now realizing he failed to put in place the distribution system to get his voters to the ballot box.

Further, those who are helping candidate Trump secure his message are few and far between. Outside of family members there are few making the case to get out the vote. Despite two living former Republican presidents and one vice president available, none is helping him be elected. Likewise, despite a large number of primary opponents, most of which pledged their support for whoever won the primary, there is only one (Chris Christie) that has been a notable advocate for candidate Trump.

And the party itself has not been mobilized to get out the vote for candidate Trump. His personal wealth has allowed Trump to implement a credible campaign. But his inability, or unwillingness, to raise lots of money to invest in down-ticket races has meant he has not garnered support from other candidates running for Congress, Senate, governorships, etc. to promote his message at a more local level.

For months we have been inundated with polls. But on election day it is not someone calling your house to hear for whom you might vote. Rather, people have to leave their houses, make time in their busy days and go to the election booth – then stand in line and vote. Mr. Trump has not done the sort of job one would expect for building the support necessary to make sure voters turn out for him.

Promotion: This might be where the two marketing programs most differ.

Candidate Trump has relied on advertising. Years ago marketing programs often relied on huge ad budgets to build a brand. Companies quickly learned that if you spent a lot on advertising you could drown out a competitive message, and bring your brand to the forefront. Simply on the basis of a big ad spend, heavily reliant on television, success was once possible. And the Trump campaign has used advertising like a soap company launching a new brand. Lots and lots and lots of advertising.

Notably, there has been little use of digital, internet and mobile advertising. Little use of social media to build trends and increase brand effectiveness. The candidate himself has gone almost entirely against modern thinking about social, mobile and internet marketing by unleashing tweets which have been simultaneously shocking, and often opposed to the brand message the advertising set out to create. While entertaining, this has not met even the minimum standards of modern marketing.

Candidate Clinton has matched candidate Trump in television and other traditional media advertising. Thus, her candidacy has not been overwhelmed by competitive spending While most people are likely tired of the ads from both candidates, it is clear that when it comes to traditional ad programs Clinton’s marketing has met the competitive level necessary to neutralize any possible Trump advantage.

But internet, mobile and social marketing has been much more successful for Clinton. Barack Obama did a splendid job of using these tools to mobilize young and minority voters in previous elections. This sort of marketing often touches people much closer, and has a greater “one-on-one” appeal, even if it is a modified “one-to-many.” And the Clinton campaign has lifted those guidelines, perhaps not as effectively as the Obama campaigns, to convert Sanders constituents to her as well as independents and undecideds.

The Trump campaign relied almost wholly on advertising, and an effort at achieving greater public relations via outrageous messaging. This has kept the candidate squarely in the public eye. But every marketer will tell you that it is not possible to build high commitment for your product with advertising alone. It takes an ability to touch people on a more personal, closer to home basis. It is critical now, more than for many years, to create identification with local issues within the home and workplace, and often reinforce social relationships.

At this, the Trump campaign has been out of step with modern marketing, and overly reliant on tools that were more effective in the ’80s and ’90s. Thus his appeal outside of European heritage, Christian, white and mostly male voter groups has struggled.

The Clinton campaign’s use of these tools has spread her base considerably wider. She has been able to connect with minorities, women, people of color, people of different religions and other groups much more effectively. In tune with demographic trends in America, this greatly enhances her opportunity to obtain the largest share of market. Tied to a superior placement campaign (to get out the vote,) this use of modern tools gives her a significant advantage.

These two campaigns have lessons for all business leaders. Too often we rely on product alone to think we will succeed. But product is only part of successfully luring buyers. You also have to make sure your product is in the right place, accessible to the most people, at time of purchase.

And today budget is only a part of good promotion, because effective use of social, mobile and internet marketing tools can help you connect with your targets more closely, and more personally. New promotion tools can expand your base, identify new target markets, develop strengths in niche groups and achieve greater loyalty at lower cost.

In history, there are almost no great campaigns that were won just because a product was superior. Nor because a product was cheaper. And despite some great ad lines (“Where’s the beef?” or “Plop, plop, fizz, fizz oh what a relief it is”) advertising has limited ability to actually make a product successful. Those that win build a marketing program using all four Ps most effectively to build on trends and excite customers.

by Adam Hartung | Feb 5, 2013 | Current Affairs, Food and Drink, Innovation, Leadership, Sports, Television

Reading reviews of Super Bowl ads I was struck by two observations:

- The reviewers got the value of most ads backwards

- They missed the most important ad of all – on Twitter

Super Bowl ads cost $1M+ to make. Then they cost $2M+ to air. So it is an expensive proposition. This isn't fine art, like a Picasso, with a long shelf life to create a rate of return. These ads need to pay off fast. They need to build the brand with existing and/or new customers to drive sales and make back that money now.

So let's start with one of the best reviewed ads – Chrysler's "God Made a Farmer". Reviewers liked the home-spun approach of using a dead conservative radio commentator voicing over pictures of farmers in pick-ups. Unfortunately, from a rate of return perspective my bet is this ad will end up near the very bottom.

- Firstly, the 50 year trend is to urbanization. In 1900 9 out of 10 Americans had something to do with agriculture. Now it is fewer than 1 in 20. Trucks are used for lots of things, but farming makes up a small percentage. It has been a full generation since most 2nd generation Americans had anything to do with a farm. Showing people using a product in ways that almost nobody uses it, and with a message most of your target market doesn't even recognize, leaves most people confused rather than ready to buy.

- Secondly, first generation Americans are changing the demographics of America quickly. First generation Americans (can I say immigrant?) proved large enough, and powerful enough, to play a spoiler role in Mitt Romney's run for the Presidency. To them, farming in America has no history, appeal or meaning to their lives.

- Thirdly, no one under the age of 35 has any idea who Paul Harvey is. Perhaps Chrysler could have used Bill O'Reilly and achieved its message mission. But as it was, there were two of us +50 people who spent 5 minutes trying to tell the group watching the game at my home who Paul Harvey even was – and why he was being quoted.

A 24 year old boy watching the game with me in suburban Chicago listened to my explanation about Paul Harvey and farming. He drives a Ford F-250 4×4 pick-up. After I finished he looked me square in the eyes and said "Swing, and a miss." And that's what I'd say to Chrysler. Whoever made this ad had more money than market research and common sense.

Simultaneously, reviewers hated GoDaddy.com's "Perfect Match, Bar Rafieli's Big Kiss." This portrayed a very stereotypical engineer enjoying a long kiss with a pretty girl – referring to how the company's products well serve client needs. Reviewers found the ad in bad taste. My bet is this ad will have immediate payback for GoDaddy.com

Have you ever heard of the monstrously successful situation comedy "The Big Bang Theory?" At just about any time you can find this in reruns on at least one, if not more than one, cable channel. The show is so successful that to pull people viewers to its Monday night schedule CBS actually chose to rerun "Big Bang" episodes amidst new episodes of its other programs in January. The show thrives on the tension of male technical professionals seeking to solve the age old question of how a man can appeal to desirable ladies. Politically correct or not, the show is successful because it is a timeless message. Most boys want to be liked by girls.

Today the world of people who have technical, or quasi-technical jobs, is HUGE. GoDaddy's target audience of people buying, and servicing, web domains just happens to be mostly male under-40 men with technical or quasi-technical backgrounds. This little, tasteless demonstration may have upset the high ethics of ad execs (or has "Mad Men" unraveled that myth?) but to its target group this ad was pure gold. And same for GoDaddy.com.

But most importantly, none of these ads will have the payback of 9 words a marketer tweeted when the lights went out at the game. Because it had blown a huge wad of money on a traditional game ad the Oreo brand folks at Mondelez were watching the game with their media agency 360i. Thinking quickly the creatives came up with an idea, and the brand guys approved it – so out went the tweet from Oreo Cookies "No problem. You can still dunk in the dark."

"Booya" as my young friends say. 10,000 retweets and an entire Monday news cycle devoted to the quick thinking folks who posted this tweet. ROI? Given that the incremental cost was zero, pretty darn high. If I was investing, I'd take the tweet over the video. The equivalent of a kick return for a TD.

The world has changed. We now live in a 24×7, real-time, always-on world. We no longer wait for the weekly magazine for analysis, or the daily newspaper for information. Or even the 11:00 television daily recap. We pick up alerts on our mobile devices constantly. Receive highlights from friends on Facebook and Twitter. We want our information NOW. And those who connect to this new way of living for providing us information are not only accepted, but admired by those thriving on the social networks.

This year's Super Bowl social media postings were triple last year's; over 30million. This is the world of immediate feedback. Immediate discussion. And the place were ads need to be immediate as well. Those who understand this, and connect to it, will succeed. Others, who spend too much to make and then distribute ads on traditional media, will not. Just as newspaper ads have lost of their relevance – TV ads are destined for the same conclusion.

The good news is that Mondelez and its Oreos team was ready, and willing, to take advantage. Where were most of the other advertisers? Audi, VW and P&G's Tide also jumped in. But of all those millions spent on once-run ads, these major corporate advertisers – and their extremely highly paid ad agencies – were absent. When the easy money was to be made, they simply weren't there. Off drinking beer and watching the game when they should have been working!

Today we learned Twitter is buying Bluefin to make its information on who is tweeting, about what, in real time even better. This will be helpful for any smart advertiser. And not just the multi-billion dollar giants. The good news is anyone, anywhere in any size company can play in this real-time, on-line social media world. You don't have to be huge, or rich.

Where were you when the lights went out? Were you taking advantage of what we may later call a "once in a lifetime" opportunity?

Where will you be the next time? Are you ready to invest in the new world of social media advertising? Or are you stuck spending too much to come in too late?

by Adam Hartung | May 25, 2011 | Defend & Extend, Disruptions, In the Swamp, Innovation, Leadership, Lock-in, Openness, Transparency, Web/Tech

Nobody admits to being the innovation killer in a company. But we know they exist. Some these folks “dinosaurs that won’t change.” Others blame “the nay-saying ‘Dr. No’ middle managers.” But when you meet these people, they won’t admit to being innovation killers. They believe, deep in their hearts as well as in their everyday actions, that they are doing the right thing for the business. And that’s because they’ve been chosen, and reinforced, to be the Status Quo Police.

When a company starts it has no norms. But as it succeeds, in order to grow quickly it develops a series of “key success factors” that help it continue growing. In order to grow faster, managers – often in functional roles – are assigned the task of making sure the key success factors are unwaveringly supported. Consistency becomes more important than creativity. And these managers are reinforced, supported, even bonused for their ability to make sure they maintain the status quo. Even if the market has shifted, they don’t shift. They reinforce doing things according to the rules. Just consider:

Quality – Who can argue with the need to have quality? Total Quality Management (TQM,) Continuous Improvement (CI,) and Six Sigma programs all have been glorified by companies hoping to improve product or service quality. If you’re trying to fix a broken product, or process, these work pretty well at helping everyone do their job better.

But these programs live with the mantra “if you can’t measure it, you can’t improve it. Measure everything that’s important.” If you’re innovating, what do you measure? If you’re in a new technology, or manufacturing process, how do you know what you really need to do right? If you’re in a new market, how do you know the key metric for sales success? Is it number of customers called, time with customers, number of customer surveys, recommendation scores, lost sales reports? When you’re trying to do something new, a lot of what you do is respond quickly to instant feedback – whether it’s good feedback or bad.

The key to success isn’t to have critical metrics and measure performance on a graph, but rather to learn from everything you do – and usually to change. Quality people hate this, and can only stand in the way of trying anything new because you don’t know what to measure, or what constitutes a “good” measure. Don’t ever forget that Motorola pretty much invented Six Sigma, and what happened to them in the mobile phone business they pioneered?

Finance. All businesses exist to make money, so who can argue with “show me the numbers. Give me a business plan that shows me how you’re going to make money.” When your’e making an incremental investment to an existing asset or process, this is pretty good advice.

But when you’re innovating, what you don’t know far exceeds what you know. You don’t know how to meet unment needs. You don’t know the market size, the price that people will pay, the first year’s volume (much less year 5,) the direct cost at various volumes, the indirect cost, the cost of marketing to obtain customer attention, the number of sales calls it will take to land a sale, how many solution revisions will be necessary to finally put out the “right” solution, or how sales will ramp up quarterly from nothing. So to create a business plan, you have to guess.

And, oh boy, then it gets ugly. “Where did this number come from? That one? How did you determine that?” It’s not long until the poor business plan writer is ridden out of the meeting on a rail. He has no money to investigate the market, so he can’t obtain any “real” numbers, so the business plan process leads to ongoing investment in the old business, while innovation simply stalls.

Under Akia Morita Sony was a great innovator. But then an MBA skilled in finance took over the top spot. What once was the #1 electronics innovator in the globe has become, well, let’s say they aren’t Apple.

Legal – No company wants to be sued, or take on unnecessary risk. And when you’re selling something, lawyers are pretty good at evaluating the risk in that business, and lowering the risk. While making sure that all the compliance issues are met in order to keep regulators – and other lawyers – out of the business.

But when you’re starting something new, everything looks risky. Customers can sue you for any reason. Suppliers can sue you for not taking product, or using it incorrectly. The technology could fail, or have negative use repercussions. Reguators can question your safety standards, or claims to customers.

From a legal point of view, you’re best to never do anything new. The less new things you do, the less likely you are to make a mistake. So legal’s great at putting up roadblocks to make sure they protect the company from lawsuits, by making sure nothing really new happens. The old General Motors had plenty of lawyers making sure their cars were never too risky – or interesting.

R&D or Product Development – Who doesn’t think it’s good to be a leader in a specific technology? Technology advances have proven invaluable for companies in industries from computers to pharmaceuticals to tractors and even services like on-line banking. Thus R&D and Product Development wants to make sure investments advance the state of the technology upon which the company was built.

But all technologies become obsolete. Or, at least unprofitable. Innovators are frequently on the front end of adopting new technologies. But if they have to obtain buy-in from product development to obtain staffing or money they’ll be at the end of a never-ending line of projects to sustain the existing development trend. You don’t have to look much further than Microsoft to find a company that is great at pouring money into the PC platform (some $9B, 16% of revenue in 2009,) while the market moves faster each year to mobile devices and entertainment (Apple spent 1/8th the Microsoft budget in 2009.)

Sales, Marketing & Distribution – When you want to protect sales to existing customers, or maybe increase them by 5%, then doing more of what you’ve always done is smart. So money is spent to put more salespeople on key accounts, add more money to the advertising budget for the most successful (or most profitable) existing products. There are more rules about using the brand than lighters at a smoker’s convention. And it’s heresy to recommend endangering the distribution channel that has so successfully helped increase sales.

But innovators regularly need to behave differently. They need to sell to different people – Xerox sold to secretaries while printing press manufacturers sold to printers. The “brand” may well represent a bygone era, and be of no value to someone launching a new product; are you eager to buy a Zenith electronic device? Sprucing up the brand, or even launching something new, may well be a requirement for a new solution to be taken seriously.

And often, to be successful, a new solution needs to cut through the old, high-cost distribution system directly to customers if it is to succeed. Pre-Gerstner IBM kept adding key account sales people in hopes of keeping IT departments from switching out of mainframes to PCs. Sears avoided the shift to on-line sales successfully – and revenue keeps dropping in the stores.

Information Technology – To make more money you automate more functions. Computers are wonderful for reducing manpower in many tasks. So IT implements and supports “standard solutions” that are cost effective for the historical business. Likewise, they set up all kinds of user rules – like don’t go to Facebook or web sites from work – to keep people focused on productivity. And to make sure historical data is secure and regulations are met.

But innovators don’t have a solution mapped out, and all that automated functionality is an enormously expensive headache. When being creative, more time is spent looking for something new than trying to work faster, or harder, so access to more external information is required. Since the solution isn’t developed, there’s precious little to worry about keeping secure. Innovators need to use new tools, and have flexibility to discover advantageous ways to use them, that are far beyond the bounds of IT’s comfort zone.

Newspapers are loaded with automated systems to collect and edit news, to enter display ads, and to “Make up” the printed page fast and cheap. They have automated systems for classified advertising sales and billing, and for display ad billing. And systems to manage subscribers. That technology isn’t very helpful now, however, as newspapers go bankrupt. Now the most critical IT skills are pumping news to the internet in real-time, and managing on-line ads distributed to web users that don’t have subscriptions.

Human Resources – Growth pushes companies toward tighter job descriptions with clear standards for “the kinds of people that succeed around here.” When you want to hire people to be productive at an existing job, HR has the procedures to define the role, find the people and hire them at the most efficient cost. And they can develop a systematic compensation plan that treats everyone “fairly” based upon perceived value to the historical business.

But innovators don’t know what kinds of people will be most successful. Often they need folks who think laterally, across lots fo tasks, rather than deeply about something narrow. Often they need people who are from different backgrounds, that are closer to the emerging market than the historical business. And pay has to be related to what these folks can get in the market, not what seems fair through the lens of the historical business. HR is rarely keen to staff up a new business opportunity with a lot of misfits who don’t appreciate their compensation plan – or the rules so carefully created to circumscribe behavior around the old business.

B.Dalton was America’s largest retail book seller when Amazon.com was founded by Jeff Bezos. Jeff knew nothing about books, but he knew the internet. B.Dalton knew about books, and claimed it knew what book buyers wanted. Two years later B.Dalton went bankrupt, and all those book experts became unemployed. Amazon.com now sells a lot more than books, as it ongoingly and rapidly expands its employee skill sets to enter new markets – like publishing and eReaders.

Innovation requires that leaders ATTACK the Status Quo Police. Everything done to efficiently run the old business is irrelevant when it comes to innovation. Functional folks need to be told they can’t force the innovatoirs to conform to old rules, because that’s exactly why the company needs innovation! Only by attacking the old rules, and being willing to allow both diversity and disruption can the business innovate.

Instead of saying “this isn’t how we do things around here” it is critical leaders make sure functional folks are saying “how can I help you innovate?” What was done in the name of “good business” looks backward – not forward. Status Quo cops have to be removed from the scene – kept from stopping innovation dead in its tracks. And if the internal folks can’t be supportive, that means keeping them out of the innovator’s way entirely.

Any company can innovate. Doing so requires recognizing that the Status Quo Police are doing what they were hired to do. Until you take away their clout, attack their role and stop them from forcing conformance to old dictums, the business can’t hope to innovate.

by Adam Hartung | Mar 4, 2011 | Current Affairs, In the Rapids, Innovation, Leadership, Openness, Television, Web/Tech

My high school physics teacher spent a week teaching students how to use a slide rule. I asked him, "why can't we just use calculators?" At the time a slide rule was about $2, and a calculator was $300. The minimum wage was $1.14/hour. He responded that slide rules had been around a long time, and you never knew if you'd have access to a calculator. To the day he retired he insisted on using, and teaching, slide rule use. Needless to say, by then plenty of folks were ready to see him go. Too bad for his students he stayed as long as he did, because that was a week they could have spent learning physics, and other important materials. Ignoring the new tool, and its advantages, was a wasteful decision that hurt him and his customers.

Yet, I am amazed at how few people are using today's new tools for business, and marketing. At a small business Board meeting this week the head of marketing presented his roll-out of the boldest campaign ever in the business's history. His promotion plan was centered around traditional PR, supplemented with radio and billboard ads. I asked for his social media campaign, and after he confirmed I was serious he said he had a manager working on that. I asked if he had a facebook page ready, the videos on YouTube, a linked-in program ready to run against targets and his twitter communications established, including hash tags? He said if those things were important somebody had to be working on them. Two weeks from roll-out and he wasn't giving them any personal consideration.

I then asked the roughly 20 attendees, all but one of which were over 40, some questions:

- How many of you use skype at least once/month? Answer – 5%

- How many of you have a facebook page and check it daily? A – 15%

- How many of you check twitter daily? A – 5% Tweet at least 5 times/week? A – none

- How many own and use a tablet? A – 10%

- How many of you have a smartphone on which you've downloaded at least 10 apps? A – 10%

- How many of you carry a laptop? A – 100%

- Who knows the #1 company for new hires in Chicago in 2010? Answer – 5% (GroupOn)

- Who has used a Groupon coupon? Answer – 30%

Slide rule users.

New tools are here, and adopters will be the winners. If you still think we're a nation of laptop users, you need to think again. Laptop usage declined 20% in the last 2 years, to 2006 levels, as people have adopted easier to use technology

Chart Source: Silicon Alley Insider of BusinessInsider.com

If you are trying to pump out ads the new medium is mobile – not television, radio, outdoor or even web sites. Have you tested the look and feel of your web site on popular mobile devices? Do you know if new users to your business are even able to access your information from a mobile device?

And, it's more likely a customer will hear about you, and obtain a review of your product or service, via Facebook than vai the web! A CNet.com article asks the leading question "Will Facebook Replace Company Web Sites?" Want to understand the importance of Facebook, check out these same month comparisons:

- Starbucks: Facebook likes – 21.1M, site visits – 1.8M

- Coca-Cola: Facebook likes – 20.5M, site visits – .3M

- Oreo: Facebook likes – 10.1M, site visits – .3M

Yes, these are consumer products. But if you don't think the first place a potential customer looks for information on your business is Facebook, whether it's financial services, business insurance, catering or blow-molded plastic housings you need to think again. The use of facebook is simply exploding.

According to Business Insider, by the end of December, 2010 Facebook apps were downloaded to iPhones at a rate exceeding 500,000/day as the total shot to nearly 60million! Meanwhile the Facebook app downloads to Android devices grew to over 20million! Blackberry Facebook users has reached 27million, bringing the total by end of 2010 to well over 100M – just on smartphones! In September, 2010 Facebook became the #1 most time spent on the internet, passing combined time on all Google and all Yahoo sites! With over 500million users, Facebook isn't just kids checking on their friends any longer. When somebody wants a first peak at your business, odds are great it will be done over a smartphone and likely via a Facebook referral!

Chart Source: Silicon Alley Insider at Business Insider

As fast as smartphone usage has grown, tablet usage is on the precipice of explosion. Tablet sales will be 6 times (or more) notebook sales in just a few years! The second most popular product will be, of course, continued sales of advanced smartphones as the two new platforms overtake the traditional laptop. So what's your budgeted spend on mobile devices, mobile apps and mobile marketing?

Chart Source: Silicon Alley Insider of Business Insider

And in the effort to attract new customers, if you think the route will be newspapers, radio, TV, billboards, or direct mail – think again. Digital local deal delivery is projected to grow at least 45%/year through 2015 creating a market of over $10billion! If you want somebody to know about your product or service, Groupon and its competitors is already taking the lead over older, traditional techniques. By the way, when was the last time you bothered to open that latest Vallasis direct mail package – or did you just throw it immediately in the recycling bin without even a look?

Chart Source: Silicon Alley Insider of Business Insider

So, what is your business doing to leverage these tools? Are your marketing, and technology, plans for 2011 and 2012 still mired in old approaches and technologies? If so, expect to be eclipsed by competitors who more quickly implement these new solutions.

Too often we become comfortable in our old way of doing things. We keep implementing the same way, like the teacher giving slide rule instructions. And that simply wastes resources, and leaves you uncompetitive. The time to use these new solutions was yesterday – and today – and tomorrow – and every day. If you don't have plans to adopt these new solutions, and use them to grow your business, what's your excuse? Is it that much fun using the old slide rule?

by Adam Hartung | Dec 6, 2010 | Current Affairs, Defend & Extend, Disruptions, Food and Drink, Leadership, Lock-in

Summary:

- Business leaders like consistency

- Consistency leads to repetition, sameness, and lower rates of return

- Kraft's product lines are consistent, but without growth

- Kraft's value has been stagnant for 10 years

- Disruptive competitors make higher rates of return, and grow

- Disruptive competitors have higher valuations – just look at Groupon

"Needless consistency is the hobgoblin of small minds" – Ralph Waldo Emerson

That was my first thought when I read the MediaPost.com Marketing Daily article "Kraft Mac & Cheese Gets New, Unified Look." Whether this 80-something year old brand has a "unified" look is wholly uninteresting. I don't care if all varieties have the same picture – and if they do it doesn't make me want to eat more powdered cheese and curved noodles.

In fact, I'm not at all interested in anything about this product line. It is kind of amusing, in an historical way, to note that people (largely children) still eat the stuff which fueled my no-cash college years (much like ramen noodles does for today's college kids.) While there's nothing I particularly dislike about the product, as an investor or marketer there's nothing really to like about it either. Pasta products always do better in a recession, as people look for cheaper belly-fillers (especially for the kid,) so that more is being sold the last couple of years doesn't tell me anything I would not have guessed on my own. That the entire category has grown to only $800M revenue across this 8 decade period only shows that it's a relatively small business with no excitement! Once people feel their finances are on firm footing sales will soon taper off.

Kraft's Mac & Cheese is emblematic of management teams that lock-in on defending and extending old businesses – even though the lack of growth leaves them struggling to grow cash flow and create a decent valuation. Introducing multiple varieties of this product has not produced growth that even matched inflation across the years. Primarily, marketing programs have been designed to try keeping existing customers from buying something else. This most recent Kraft program is designed to encourage adults to try a product they gave up eating many years ago. This is, at best, "foxhole" marketing. Spending money largely just to keep the brand from going away, rather than really expecting any growth. Truly, does anyone think this kind of spending will generate a billion dollar product line in 2011 – or even 2012?

What's wrong with defensive marketing, creating consistency across the product line – across the brand – and across history? It doesn't produce high rates of return. There are lots of pasta products, even lots of brands of mac & cheese. While Kraft's product surely produces a positive margin, multiple competitors and lack of growth means increased spending over time merely leaves the brand producing a marginal rate of return. Incremental ad spending doesn't generate real growth, just a hope of not losing ground. We know people aren't flocking to the store to buy more of the product. New customers aren't being identified, and short-term growth in revenues does not yield the kinds of returns that would enhance valuation and make the world a better place for investors – or employees.

While Kraft is trying to create headlines with more spending in a very tired product, across town in Chicago Groupon has created a $500M revenue business in just 2 years! And new reports from the failed acquisition attempt by Google indicate revenues are likely to reach $2B in 2011 (CNNMoney.com, Fortune, "Google's Groupon Groping Reveals the Shifting Power of the Web World.") Where's Kraft in this kind of growth market? After all, coupons for Kraft products have been in mailers and Sunday inserts for 50 years. Why isn't Kraft putting money into a real growth business, which is producing enormous value while cash flow grows in multiples? While Groupon has created somewhere around $6B of value in 2 years, Kraft's value has only gone sideways for the last decade (chart at Marketwatch.com.)

Kraft has not introduced a new product since — well — DiGiorno. And that's been more than a decade. While the company has big revenues – so did General Motors. The longer a company plays defense, regardless of size, trying to extend its outdated products (and business model) the riskier that business becomes. While big revenues appear to offer some kind of security, we all know that's not true. Not only does competition drive down margins in these older businesses, but newer products make it harder and harder for the old products to compete at all. Eventually, the effort to maintain historical consistency simply allows competitors to completely steal the business away with new products, creating a big revenue drop, or producing such low returns that failure is inevitable.

Lots of business people like consistency. They like consistency in how the brand is executed, or how products are aligned. They like consistency in the technology base, or production capabilities. They like consistency in customers, and markets. They like being consistent with company history – doing what "made the company famous." They like the similarity of doing something again, and again, hoping that consistency will produce good returns.

But consistency is the hobgoblin of small minds. And those who are more clever find ways to change the game. Xerox figured out how to let everyone be a one-button printer, and killed the small printing press manufacturers. HP's desktop printers knocked the growth out of Xerox. Google figured out a better way to find information, and place ads, just about killing newspapers (and magazines.) Apple found a better way to use mobile minutes, taking a big bite out of cell phone manufacturers. Amazon found a better way to sell things, killing off bookstores and putting a world of hurt on many retailers. Netflix found a better way of distributing DVDs and digital movies, sending Blockbuster to bankruptcy. Infosys and Tata found a better way of doing IT services, wiping out PWC and nearly EDS. Hulu (and soon Netflix, Google and Apple) has found a better way of delivering television programming, killing the growth in cable TV. Groupon is finding a better way of delivering coupons, creating huge concerns for direct mail companies. Now tablet makers (like Apple) are demonstrating a better way of working remotely, sending shivers of worry down the valuation of Microsoft. These companies, failed or in jeapardy, were very consistent.

Those who create disruptions show again and again that they can generate growth and above average returns, even in a recession. While those who keep trying to defend and extend their old business are letting consistency drive their behavior – leading to intense competition, genericization, and lower rates of return. Maybe Kraft should spend more money looking for the next food we would all like, rather than consistently trying to convince us we want more Mac & Cheese (or Velveeta).