Toys R Us filed for bankruptcy this week. And the obvious response was “another retailer slaughtered by Amazon and on-line retailing.” But this conclusion comes short of describing why Toys R Us leadership did not do the obvious things to keep Toys R Us relevant.

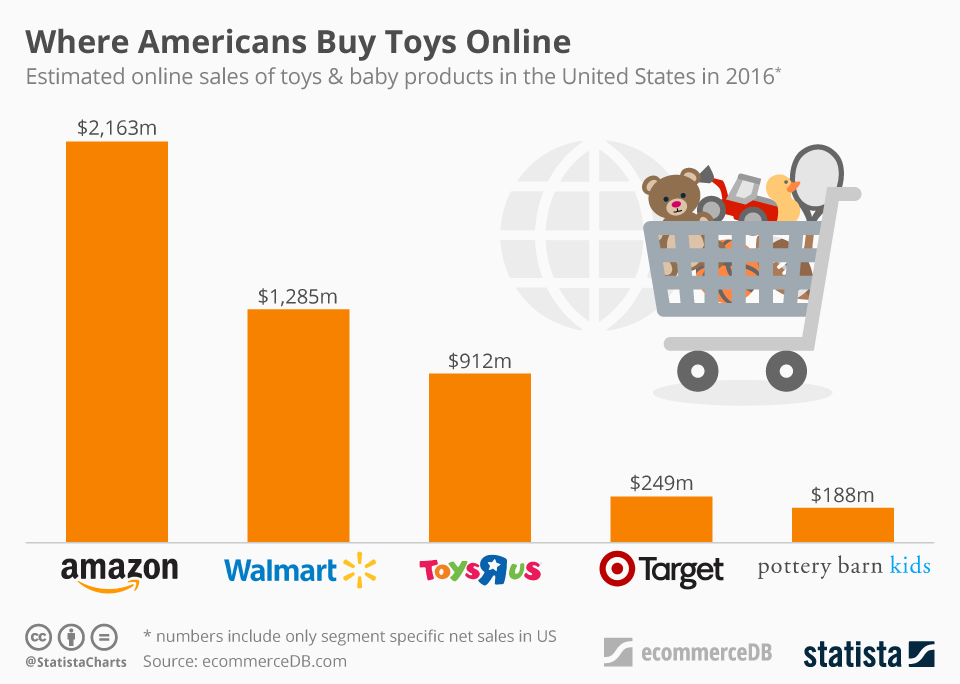

Amazon and WalMart both eclipsed Toys R Us in toy retail sales. Chart courtesy of Felix Richter, Statista

Everyone, and I mean everyone, knew over the last decade that customers were buying more stuff on-line, including toys. And everyone also knew that WalMart was pushing extremely hard to keep customers going to their stores by offering products like toys at low prices. And, it was clear that customers were shifting to buying more toys from both these retailers. If this was so obvious to everyone, why didn’t Toys R Us leadership do something? After all, Toys R Us is a multi-billion dollar revenue company.

The LBO

It was over 30 years ago when financiers discovered they could buy a company, sell off some assets and otherwise increase the company’s cash, then convince banks and bondholders to load the company with debt. These financiers would then pull out the cash for themselves, and leave the company with a ton of debt. The LBO (leveraged buy out) was born, invented by investment bankers like KKR (named for founders Kohlberg, Kravis & Roberts.) They would use a small bit of private equity, and then use the company’s own assets to raise debt money (leverage) to buy the company. By “restructuring” the company to a lower cost of operations, usually with draconian reductions, they would increase cash flow to make higher debt repayments. Then they would either take the money out directly, or take the company public where they could sell their shares, and make themselves rich. This form of deal making birthed what we now call the Private Equity business.

In 2005, KKR and Bain Capital (which included former Presidential candidate Mitt Romney) bought Toys R Us for about $6.6billion, plus assuming just under $1B of debt, for a total valuation of $7.5billion. But the private equity guys didn’t buy the company with equity. They only put in $1.3billion, and used the company’s assets to raise $5.3billion in additional debt, making total debt a whopping $6.2B. Total debt was now a remarkable 82.7% of total capital! At the time of the deal interest rates on that debt were around 7.25%, creating a cash outflow of $450million/year just to pay interest on the loans. At the time Toys R Us was barely making a profit of 2% – so the debt was double company net profits.

Debt led to bad management decisions and ultimately bankruptcy of the U.S. company

The biggest assumption behind a debt-financed takeover is that the company can cut costs to improve cash flow and thus pay the interest. But behind that assumption is an even bigger assumption. That the marketplace won’t change dramatically. The KKR and Bain Capital leaders assumed they could shrink Toys R Us in a way that would lower operating costs. They also assumed they could sell some under-utilized assets to raise cash. They did not assume they would need contingency money if competition, and the marketplace, changed in some unplanned way.

eCommerce was pretty new in 2005. Amazon was an $8.5 billion company, but it didn’t make any profits and very few predicted then it would become today’s $100 billion behemoth. Because the financiers didn’t anticipate a big market shift to ecommerce, they focused on the war with Walmart and Target. Their plans were to lower operating costs, close some stores that were underperforming, license some offshore stores, and sell some assets (like real estate owned or leases) to raise cash and repay the debt.

But they weren’t prepared to take on another, entirely different competitor on-line. As Amazon’s growth affected all retailers, Toys R Us simply did not have the resources to fight the traditional discount and dollar brick-and-mortar retailers, and build a major on-line presence, and keep paying that debt. While it is easy to sit on the sidelines and say that Toys R Us should have spent more money building its on-line presence in order to remain relevant, the fact is that the deal in 2005 left the company with insufficient cash flow to do so. Regardless of what leadership might have wanted to do, simply keeping the lights on was a tough challenge when having to pay out so much cash to bondholders.

And the investors simply did not expect that the growth of on-line retailing would stall traditional retail stores, thus creating a major loss of value for retail real estate. U.S. retail real estate value had increased in value for decades. The assumption was that the real estate, whether owned or leased, would continue to go up in value. Real estate was a “hard” asset that KKR and Bain Capital could bank on for raising cash to repay the debt. But as on-line retail grew, and traditional retail declined, America became “over stored” with far too much retail space. Prices were shattered in many markets, and it was not possible for Toys R Us to sell those assets for a gain that would meet the debt obligations.

With $400 million of debt coming due next year, Toys R Us simply doesn’t have the cash flow, or assets, to repay those bondholders

Old assumptions about finance are a big problem for companies today. Assumptions about “leveraging” hard assets, and intangibles like brand value, are no longer true. Competitors emerge, markets change, and old assets can lose value very fast. Assumptions about business model stability are no longer true, as new competitors using newer technology create new ways to sell, and often at lower cost than was ever expected. Assumptions about customer loyalty, and market share stability, are no longer true as new competitors appeal to customers differently and cause big shifts in buying behavior very fast. The speed with which technology, competitors, markets and customers shift now requires companies have the funds available to invest in change.

This story isn’t just about debt. The very popular activity of “returning money to shareholders by repurchasing stock” is a terrible idea. Stock repurchases do not make a company more valuable, nor a stronger competitor. Instead they burn through cash to reduce the company’s capitalization, and manipulate ratios like EPS (earnings per share) and P/E (price/earnings) multiple. Stock repurchases hurt companies, and make them less competitive. Good companies return money to shareholders by investing in growth, which raises sales, profits and increases the stock price making the company truly more valuable.

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

Toys R Us isn’t a story about Amazon, or eCommerce, taking out another retailer

The important part of the Toys R Us story is realizing that the wrong financial decisions can doom your organization. You can have a great vision, and even great ideas about new ways to compete. But if you don’t have the money to invest in growth, it won’t happen. If leaders don’t have the money to spend on new projects and new markets, because they’re sending it all to bondholders or using it to repurchase shares in hopes of propping up a stock price, eventually there will be a market shift that will doom the old business model and leave it unable to compete.

To succeed today leaders need the money to invest in change, and they have to constantly invest it in change, or their companies will lose relevancy and end up like Toys R Us, Radio Shack, Circuit City, Aeropostale, The Limited, Payless Shoes, Gander Mountain, Golfsmith, Sports Authority, Borders Books and the great, original American retailer A&P.

On April 15 Zebra Technologies announced its planned acquisition of Motorola’s Enterprise Device Business. This was remarkable because it represented a major strategic shift for Zebra, and one that would take a massive investment in products and technologies which were wholly new to the company. A gutsy play to make Zebra more relevant in its B-2-B business as interest in its “core” bar code business was declining due to generic competition.

Last week the acquisition was completed. In an example of Jonah swallowing the whale, Zebra added $2.5B to annual revenues on its old base of $1B (2.5x incremental revenue,) an additional 4,500 employees joined its staff of 2,500 and 69 new facilities were added. Gulp.

As CEO Anders Gustafsson told me, “after the deal was agreed to I felt like the dog that caught the car. ”

Fortunately Zebra has a plan, and it is all around growth. Acquisitions led by private equity firms, hedge funds or leveraged buyout partners are usually quick to describe the “synergies” planned for after the acquisition. Synergy is a code word for massive cost cutting (usually meaning large layoffs,) selling off assets (from buildings to product lines and intellectual property rights) and shutting down what the buyers call “marginal” businesses. This always makes the company smaller, weaker and less likely to survive as the new investors focus on pulling out cash and selling the remnants to some large corporation.

There is no growth plan.

But Zebra has publicly announced that after this $3.25B investment they plan only $150M of savings over 2 years. Which means Zebra’s management team intends to grow what they bought, not decimate it. What a novel, or perhaps throwback, idea.

Minimal cost cutting reflects a deal, as CEO Gustafsson told me, “envisioned by management, not by bankers.”

Zebra’s management knew the company was frequently pitching for new work in partnership with Motorola. The two weren’t competitors, but rather two companies working to move their clients forward. But in a disorganized, unplanned way because they were two totally different companies. Zebra’s team recognized that if this became one unit, better planning for clients, the products could work better together, the solutions more directly target customer needs and it would be possible to slingshot forward ahead of competitors to grow revenues.

As CEO since 2007, Anders Gustafsson had pushed a strategy which could grow Zebra, and move the company outside its historical core business of bar code printers and readers. The leadership considered buying Symbol Technology, but wasn’t ready and watched it go to Motorola.

Then Zebra’s team knuckled down on their strategy work. CEO Gustafsson spelled out for me the 3 trends which were identified to build upon:

Mobility would continue to be a secular growth trend. And business customers needed products with capabilities beyond the generic smart phone. For example, the kind of integrated data entry and printing device used at a remote rental car return. These devices drive business productivity, and customers hunger for such solutions.

From the days of RFID, where Zebra was an early player, had emerged automatic data capture – which became what now is commonly called “The Internet of Things” – and this trend too had far to extend. By connecting the physical and digital worlds, in markets like retail inventory management, big productivity boosts were possible in formerly moribund work that added cost but little value.

Cloud-based (SaaS and growth of lightweight apps) ecosystems were going to provide fast growth environments. Client need for capability at the employee’s (or their customer’s) fingertips would grow, and those people (think distributors, value added resellers [VARs]) who build solutions will create apps, accessible via the cloud, to rapidly drive customer productivity.

With this groundwork, the management team developed future scenarios in which it became increasingly clear the value in merging together with Motorola devices to accelerate growth. According to CEO Gustafsson, “it would bring more digital voice to the Zebra physical voice. It would allow for more complete product offerings which would fulfill critical, macro customer trends.”

But, to pull this off required selling the Board of Directors. They are ultimately responsible for company investments, and this was – as described above – a “whopper.”

The CEO’s team spent a lot of time refining the message, to be clear about the benefits of this transaction. Rather than pitching the idea to the Board, they offered it as an opportunity to accelerate strategy implementation. Expecting a wide range of reactions, they were not surprised when some Directors thought this was “phenomenal” while others thought it was “fraught with risk.”

So management agreed to work with the Board to undertake a thorough due diligence process, over many weeks (or months it turned out) to ask all the questions. A key executive, who was a bit skeptical in her own right, took on the role of the “black hat” leader. Her job was to challenge the many ideas offered, and to be a chronic skeptic; to not let the team become enraptured with the idea and thereby sell themselves on success too early, and/or not consider risks thoroughly enough. By persistently undertaking analysis, education led the Board to agree that management’s strategy had merit, and this deal would be a breakout for Zebra.

Next came completing financing. This was a big deal. And the only way to make it happen was for Zebra to take on far more debt than ever in the company’s history. But, the good news was that interest rates are at record low levels, so the cost was manageable.

Zebra’s leadership patiently met with bankers and investors to overview the market strategy, the future scenarios and their plans for the new company. They over and again demonstrated the soundness of their strategy, and the cash flow ability to service the debt. Zebra had been a smaller, stable company. The debt added more dynamism, as did the much greater revenues. The requirement was to decide if the strategy was soundly based on trends, and had a high likelihood of success. Quickly enough, the large shareholders agreed with the path forward, and the financing was fully committed.

Now that the acquisition is complete we will all watch carefully to see if the growth machine this leadership team created brings to market the solutions customers want, so Zebra can generate the revenue and profits investors want. If it does, it will be a big win for not only investors but Zebra’s employees, suppliers and the communities in which Zebra operates.

The obvious question has to be, why didn’t Motorola do this deal? After all, they were the whale. It would have been much easier for people to understand Motorola buying Zebra than the gutsy deal which ultimately happened.

Answering this question requires a lot more thought about history. In 2006 Motorola had launched the Razr phone and was an industry darling. Newly minted CEO Ed Zander started partnering with Google and Apple rather than developing proprietary solutions like Razr. Carl Icahn soon showed up as an activist investor intent on restructuring the company and pulling out more cash. Quickly then-CEO Ed Zander was pushed out the door. New leadership came in, and Motorola’s new product introductions disappeared.

Under pressure from Mr. Icahn, Motorola started shrinking under direction of the new CEO. R&D and product development went through many cuts. New product launches simply were delayed, and died. The cellular phone business began losing money as RIM brought to market Blackberry and stole the enterprise show. Year after year the focus was on how to raise cash at Motorola, not how to grow.

But left in Icahn’s wake was a culture of cut and shred, rather than invest. After 90 years of invention, from Army 2-way radios to police radios, from AM car radios to home televisions, the inventor analog and digital cell towers and phones, there was no more innovation at Motorola. Motorola had become a company where the leaders, and Board, only thought about how to raise cash – not deploy it effectively within the corporation. There was very little talk about how to create new markets, but plenty about how to retrench to ever smaller “core” markets with no sales growth and declining margins. In September of this year long-term CEO Greg Brown showed no insight for what the company can become, but offered plenty of thoughts on defending tax inversions and took the mantle as apologist for CEOs who use financial machinations to confuse investors.

Investors today should cheer the leadership, in management and on the Board, at Zebra. Rather than thinking small, they thought big. Rather than bragging about their past, they figured out what future they could create. Rather than looking at their limits, they looked at the possibilities. Rather than giving up in the face of objections, they studied the challenges until they had answers. Rather than remaining stuck in their old status quo, they found the courage to become something new.

Tribune Corporation finally emerged from a 4 year bankruptcy on the last day of 2012. Before the ink hardly dried on the documents, leadership has decided to triple company debt to double up the number of TV stations. Oh my, some people just never learn.

The media industry is now over a decade into a significant shift. Since the 1990s internet access has changed expectations for how fast, easily and flexibly we acquire entertainment and news. The result has been a dramatic decline in printed magazine and newspaper reading, while on-line reading has skyrocketed. Simultaneously, we're now seeing that on-line streaming is making a change in how people acquire what they listen to (formerly radio based) and watch (formerly television-based.)

Unfortunately, Tribune – like most media industry companies – consistently missed these shifts and underestimated both the speed of the shift and its impact. And leadership still seems unable to understand future scenarios that will be far different from today.

In 2000 newspaper people thought they had "moats" around their markets. The big newspaper in most towns controlled the market for classified ads for things like job postings and used car sales. Classified ads represented about a third of newspaper revenues, and 40% of profits. Simultaneously display advertising for newspapers was considered a cash cow. Every theatre would advertise their movies, every car dealer their cars and every realtor their home listings. Tribune leadership felt like this was "untouchable" profitability for the LA Times and Chicago Tribune that had no competition and unending revenue growth.

So in 2000 Tribune spent $8B to buy Times-Mirror, owner of the Los

Angeles Times. Unfortunately, this huge investment (75% over market

price at the time, by the way) was made just as people were preparing to

shift away from newspapers. Craigslist, eBay and other user sites killed the market for classified ads. Simultaneously movie companies, auto companies and realtors all realized they could reach more people, with more information, cheaper on-line than by paying for newspaper ads.

These web sites all existed before the acquisition, but Tribune leadership ignored the trend. As one company executive said to me "CraigsList!! You think that's competition for a newspaper? Craigslist is for hookers! Nobody would ever put a job listing on Craigslist." Like his compadres running newspapers nationwide, the new competitors and trends toward on-line were dismissed with simplistic statements and broad generalizations that things would never change.

The floor fell out from under advertising revenues in newspapers in the 2000s. There was no way Times-Mirror would ever be worth a fraction of what Tribune paid. Debt used to help pay for the acquisition limited the options for Tribune as cost cutting gutted the organization.

Then, in 2007 Sam Zell bailed out management by putting together a leveraged buyout to acquire Tribune company. Saying that he read 3 newspapers every day, he believed people would never stop reading newspapers. Like a lot of leaders, Mr. Zell had more money than understanding of trends and shifting markets. He added a few billion dollars more debt to Tribune. By the end of 2008 Tribune was unable to meet its debt obligations, and filed for bankruptcy.

Now, new leadership has control of Tribune. They are splitting the company in two, seperating the print and broadcast businesses. The hope is to sell the newspapers, for which they believe there are 40 potential buyers. Even though profits continued falling, from $156M to $89M, in just the last year. Why anyone would buy newspaper companies, which are clearly buggy whip manufacturers, is wholly unclear. But hope springs eternal!

Let's see, what's the market trend in entertainment and news? Where once we were limited to local radio and television stations for most content, now we can acquire almost anything we want – from music to TV, movies, documentaries or news – via the internet. Rather than being subjected to what some programming executive decides to give us, we can select what we want, when we want it, and simply stream it to our laptop, tablet, smartphone, or even our large-screen TV.

A long time ago content was controlled by distribution. There was no reason to create news stories or radio programs or video unless you had access to distribution. Obviously, that made distribution – owning newspapers, radio and TV stations – valuable.

But today distribution is free, and everywhere. Almost every American has access to all the news and entertainment they want from the internet. Either free, or for bite-size prices that aren't too high. Today the value is in the content, not distribution.

While it might be easy for Tribune to ignore Hulu, Netflix and Amazon, the trend is very clear. The need for broadcast stations like NBC or WGN or Food Network to create content is declining as we access content more directly, from more sources. And the need to have content delivered to our home by a local affiliate station is becoming, well, an anachronism.

Yet, Tribune's new TV-oriented leadership is doubling down on its bet for local TV's future. Ignoring all the trends, they are borrowing more money to buy more assets that show all signs of becoming about as valuable whaling ships. It's a big, dumb bet. Similar to overpaying for Times-Mirror. Some leaders just seem destined to never learn.

Michael Dell has put together a hedge fund, one of his largest suppliers and some debt money to take his company, Dell, Inc. private. There are large investors threatening to sue, claiming the price isn't high enough. While they are wrangling, small investors should consider this privatization manna from heaven, take the new, higher price and run to invest elsewhere – thankful you're getting more than the company is worth.

In the 1990s everybody thought Dell was an incredible company. With literally no innovation a young fellow built an enormously large, profitable company using other people's money, and technology. Dell jumped into the PC business as it was born. Suppliers were making the important bits, and looking for "partners" to build boxes. Dell realized he could let other people invest in microprocessor, memory, disk drive, operating system and application software development. All he had to do was put the pieces together.

Dell was the rare example of a company that was built on nothing more than execution. By marketing hard, selling hard, buying smart and building cheap Dell could produce a product for which demand was skyrocketing. Every year brought out new advancements from suppliers Dell could package up and sell as the latest, greatest model. All Dell had to do was stay focused on its "core" PC market, avoid distractions, and win at execution. Heck, everyone was going to make money building and selling PCs. How much you made boiled down to how hard you worked. It wasn't about strategy or innovation – just execution.

Dell's business worked for one simple reason. Everybody wanted PCs. More than one. And everybody wanted bigger, more powerful PCs as they came available. Market demand exploded as the PC became part of everything companies, and people, do. As long as demand was growing, Dell was growing. And with clever execution – primarily focused on speed (sell, build, deliver, get the cash before the supplier has to be paid) – Dell became a multi-billion dollar company, and its founder a billionaire with no college degree, and no claim to being a technology genius.

But, the market shifted. As this column has pointed out many times, demand for PCs went flat – never to return to previous growth rates. Users have moved to mobile devices such as smartphones and tablets, while corporate IT is transitioning from PC servers to cloud services. iPad sales now nearly match all of Dell's sales. Dell might well be the world's best PC maker, but when people don't want PCs that doesn't matter any more.

Market watchers knew this. That's why Dell's stock took a long ride from its lofty value on the rapids of growth to the recent distinctly low value as it slipped into the whirlpool of failure.

If you think adding debt to Dell will save it from the market shift, just look at how well that strategy worked for fixing Tribune Corporation. A Sam Zell led LBO took over the company claiming he had plans for a new future, as advertisers shifted away from newspapers. Bankruptcy came soon enough, employee pensions were wiped out, massive layoffs undertaken and 4 years of legal fighting followed to see if there was any plan that would keep the company afloat. Debt never fixes a failing company, and Dell knows that. Dell has no answer to changing market demand away from PCs.

Now the buzzards are circling. HP has been caught in a rush to destruction ever since CEO Fiorina decided to buy Compaq and gut the HP R&D in an effort to follow Dell's wild revenue ride. Only massive cost cutting by the following CEO Hurd kept HP alive, wiping out any remnants of innovation. Now HP has a dismal future. But it hopes that as the PC market shrinks the elimination of one competitor, Dell, will give newest CEO Whitman more time to somehow find something HP can do besides follow Dell into bankruptcy court.

Watching as its execution-oriented ecosystem manufacturers are struggling, supplier Microsoft is pulling out its wallet to try and extend the timeline. Plundering its $85B war chest, Microsoft keeps adding features, with acquisitions such as Skype, that consume cash while offering no returns – or even strong reasons for people to stop the transition to tablets.

Additionally it keeps putting up money for companies that it hopes will build end-user products on its software, such as its $500M investment in Barnes & Noble's Nook and now putting $2B into Dell. $85B is a lot of money, but how much more will Microsoft have to spend to keep HP alive – or money losing Acer – or Lenovo? A billion here, a billion there and pretty soon it adds up to a lot of money! Not counting losses in its own entertainmnet and on-line divisions. The transition to mobile devices is permanent and Microsoft has arrived at the game incredibly late – and with products that simply cannot obtain better than mixed reviews.

The lesson to learn is that management, and investors, take a big risk when they focus on execution. Without innovation, organizations become reliant on vendors who may, or may not, stay ahead of market transitions. When an organization fails to be an innovator, someone who creates its own game changers, and instead tries to succeed by being the best at execution eventually market shifts will kill it. It is not a question of if, but when.

Being the world's best PC maker is no better than being the world's best maker of white bread (Hostess) or the world's best maker of photographic film (Kodak) or the world's best 5 and dime retailer (Woolworth's) or the world's best manufacturer of bicycles (Schwinn) or cold rolled steel (Bethlehem Steel.) Being able to execute – even execute really, really well – is not a long-term viable strategy. Eventually, innovation will create market shifts that will kill you.