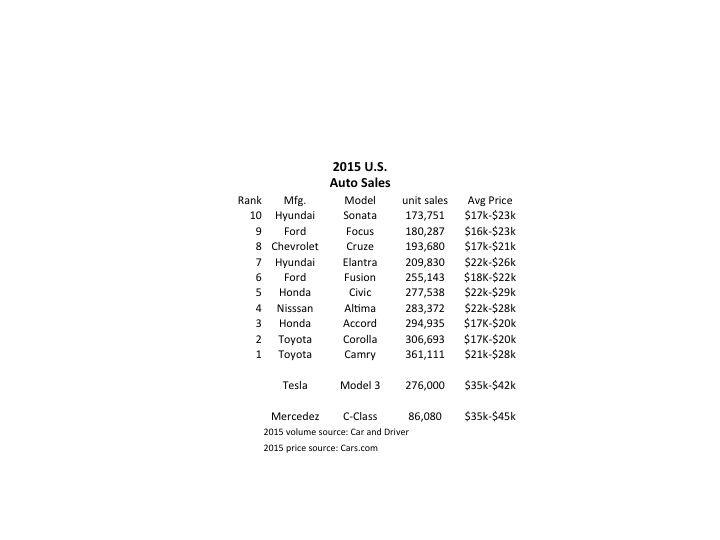

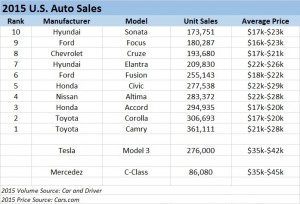

Tesla started taking orders for the Model 3 last week, and the results were remarkable. In 24 hours the company took $1,000 deposits for 198,000 vehicles. By end of Saturday the $1,000 deposits topped 276,000 units. And for a car not expected to be available in any sort of volume until 2017. Compare that with the top selling autos in the U.S. in 2015:

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]

Even more astonishing is the average selling price. Note that top 10 cars are not highly priced, mostly in the $17,000 to $25,000 price range. But the Tesla is base priced at $35,000, and expected with options to sell closer to $42,000. That is almost twice as expensive as the typical top 10 selling auto in the U.S.

Tesla has historically been selling much more expensive cars, the Model S being its big seller in 2015. So if we classify Tesla as a “luxury” brand and compare it to like-priced Mercedes Benz C-Class autos we see the volumes are, again, remarkable. In under 1 week the Model 3 took orders for 3 times the volume of all C-Class vehicles sold in the U.S. in 2015.

Although this has surprised a large number of people, the signs were all pointing to something extraordinary happening. The Tesla Model S sold 50,000 vehicles in 2015 at an average price of $70,000 to $80,000. That is the same number of the Mercedes E-Class autos, which are priced much lower in the $50,000 range. And if you compare to the top line Mercedes S-Class, which is only slightly more expensive at an average $90,0000, the Model S sold over 2 times the 22,000 units Mercedes sold. And while other manufacturers are happy with single digit percentage volume growth, in Q4 Tesla shipments were 75% greater in 2015 than 2014.

In other words, people like this brand, like these cars and are buying them in unprecedented numbers. They are willing to plunk down deposits months, possibly years, in advance of delivery. And they are paying the highest prices ever for cars sold in these volumes. And demand clearly outstrips supply.

Yet, Tesla is not without detractors. From the beginning some analysts have said that high prices would relegate the brand to a small niche of customers. But by outselling all other manufacturers in its price point, Tesla has demonstrated its cars are clearly not a niche market. Likewise many analysts argued that electric cars were dependent on high gasoline prices so that “economic buyers” could justify higher prices. Yet, as gasoline prices have declined to prices not seen for nearly a decade Tesla sales keep going up. Clearly Tesla demand is based on more than just economic analysis of petroleum prices.

People really like, and want, Tesla cars. Even if the prices are higher, and if gasoline prices are low.

Which leads us to the beauty of sales growth. When products tap an under- or unfilled need they frequently far outsell projections. Think about the iPod, iPhone and iPad. There is naturally concern about scaling up production. Will the money be there? Can the capacity come online fast enough?

Of course, of all the problems in business this is one every leader should want. It is certainly a lot more fun to worry about selling too much rather than selling too little. Especially when you are commanding a significant price premium for your product, and thus can be sure that demand is not an artificial, price-induced variance.

With rare exceptions, investors understand the value of high sales at high prices. When gross margins are good, and capacity is low, then it is time to expand capacity because good returns are in the future. The Model 3 release projects a backlog of almost $12B. Booked orders at that level are extremely rare. Further, short-term those orders have produced nearly $300million of short-term cash. Thus, it is a great time for an additional equity offering, possibly augmented with bond sales, to invest rapidly in expansion. Problematic, yes. Insolvable, highly unlikely.

On the face of it Tesla appears to be another car company. But something much more significant is afoot. This sales level, at these prices, when the underlying economics of use seem to be moving in the opposite direction indicates that Tesla has tapped into an unmet need. It’s products are impressing a large number of people, and they are buying at premium prices. Based on recent orders Tesla is vastly outselling competitive electric automobiles made by competitors, all of whom are much bigger and better resourced. And those are all the signs of a real Game Changer.

Many people equate spending on R&D with investing in innovation. The logic goes that R&D spending is lab spending, and out of labs come innovations. Hence, those that spend a lot on R&D are innovative.

That is faulty logic.

This chart shows R&D spending from the top 20 companies in 2011:

Think of your own list of companies that are providing innovations which change your work, or life. Would you include Apple? Amazon? Facebook? Google? Genentech? (Here's the link to Fast Company's 50 most innovative for 2012). Note that none of these companies appear on the list of top R&D spenders.

On the other hand, as you look at the big spender list some things might be apparent:

Microsoft is #5, spending $9B and nearly 13% of revenue. Yet, for this money in 2012 the world received updates to their aging operating system and office automation software. Both of which failed to register favorable reviews by industry gurus, and are considered far from innovative. And Nokia, which is so floundering some consider it a likely bankruptcy candidate soon, is #7! Despite spending nearly $8B on R&D Nokia is now completely reliant on Microsoft if it is to even survive.

Autos make up a big part of the group. Toyota, GM, Volkswagen, Honda and Daimler are all on the list, spending a whopping $36B. Yet, even though they give us improvements nobody considers them (especially GM) very innovative. That award would go to little Tesla Motors. Or maybe Tata Motors in India.

Pharmaceuticals make up the dominant industry. Novartis, Roche, Pfizer, Merck, Johnson & Johnson, Sanofi, GlaxoSmithKline and AstraZeneca are all here – spending a cumulative $54B! Yet, they have all failed to give the world any incredible new drugs, all have profit struggles, and the industry is rife with discussions about weak product pipelines. The future of modern medicine increasingly is shifting to genetic solutions, biologics and more specific alternatives to the historical drug regimes from these aging pharma R&D programs.

Do you see the obvious pattern? Most big R&D spenders are not really seeking innovations. They are spending money on historical programs, following historical patterns and trying to defend and extend the historical business. In other words, they are spending vast sums attempting to sustain (or recapture) historical success. And, as the list shows, largely doing a pretty lousy job of it.

If you were given $10,000 to invest would you select these top 20 R&D spenders – or would you look for other, more innovative companies. From a profitability, rate of return and trend perspective, most of these companies look weak – or downright horrible.

Innovators don't focus on what they spend, but where they spend it.

The companies most known for innovation don't keep spending money year after year on their old business. Instead of digging deeper into what they already know, they invest laterally. They spend money putting the pieces together in new, unique ways. They try to find new solutions to old problems, using new – even fringe – technologies. They try to develop disruptive solutions that actually change the marketplace, rather than trying to make something that already exists better, faster or cheaper.

Lots of people like to think there is "scale" in research. Bigger is better. What's more important, for investors, is that there is "diminishing returns." The more you research an area the more you have to spend to find anything new. The costs keep escalating, as the gains shrink. After investing for a while, continuing to research an area is not a good investment (although it may be very intellectually interesting.)

Most of the companies on this list would be smarter to scrap their existing R&D programs, cut the budget in half (at least,) and then invest it somewhere very different. Instead of looking deeper, they need to look wider – broader. They need to investigate alternative solutions, rather than more of the same. They need to be putting more money on fringe opportunities, and a lot less into the core.

Until they do, few on this list are very good investment bets. You'll do better investing like, and in, the real innovators.

When you go after competitors, does it more resemble a gladiator war – or a David vs. Goliath battle? The answer will likely determine your profitability. As a company, and as an investor.

After they achieve some success, most companies fall into a success formula – constantly tyring to improve execution. And if the market is growing quickly, this can work out OK. But eventually, competitors figure out how to copy your formula, and as growth slows many will catch you. Just think about how easily long distance companies caught the monopolist AT&T after deregulation. Or how quickly many competitors have been able to match Dell’s supply chain costs in PCs. Or how quickly dollar retailers – and even chains like Target – have been able to match the low prices at Wal-Mart.

These competitors end up in a gladiator war. They swing their price cuts, extended terms and other promotional weapons, leaving each other very bloody as they battle for sales and market share. Often, one or more competitors end up dead – like the old AT&T. Or Compaq. Or Circuit City. These gladiator wars are not a good thing for investors, because resources are chewed up in all the fighting, leaving no gains for higher dividends – nor any stock price appreciation. Like we’ve seen at Wal-Mart and Dell.

The old story of David and Goliath gives us a different approach. Instead of going “toe-to-toe” in battle, David came at the fight from a different direction – adopting his sling to throw stones while he remained safely out of Goliath’s reach. After enough peppering, he wore down the giant and eventually popped him in the head.

And that’s how much smarter people compete.

When everyone was keen on retail stores to rent DVDs, Netflix avoided the gladiator war with Blockbuster by using mail delivery.

While United, American, Continental, Delta, etc. fought each other toe-to-toe for customers in the hub-and-spoke airline wars (none making any money by the way) Southwest ferried people cheaply between smaller airports on direct flights. Southwest has made more money than all the “major” airlines combined.

While Hertz, Avis, National, Thrifty, etc. spent billions competing for rental car customers at airports Enterprise went into the local communities with small offices, and now has twice their revenues and much higher profitability.

When internet popularity started growing in the 1990s Netscape traded axe hits wtih Microsoft and was destroyed. Another browser pioneer, Spyglass, transitioned from PCs to avoid Microsoft, and started making browsers for mobile phones, TVs and other devices creating billions for investors.

While GM, Ford and Chrysler were in a grinding battle for auto customers, spending billions on new models and sales programs, Honda brought to market small motorcycles and very practical, reliable small cars. Honda is now very profitable in several major markets, while the old gladiators struggle to survive.

As an investor, we should avoid buying stocks of companies, and management teams that allow themselves to be drug into gladiator wars. No matter what promises they make to succeed, their success is uncertain, and will be costly to obtain. What’s worse, they could win the gladiator war only to find themselves facing David – after they are exhausted and resources are spent!

Research in Motion became embroiled in battles with traditional cell phone manufacturers like Nokia and Ericdson, and now is late to the smartphone app market – and with dwindling resources.

Motorola fought the gladiator war trying to keep Razr phones competitive, only to completely miss its early lead in smartphones. Now it has limited resources to develop its Android smart phone line.

Is it smart for Google to take on a gladiator war in social media against Facebook, when it doesn’t seem to have any special tool for the battle? What will this cost, while it simultaneously fights Apple in Android wars and Microsoft for Chrome sales?

On the other hand, it’s smart to invest in companies that enter growth markets, but have a new approach to drive customer conversion. For example, Zip Car rents autos by the hour for urban users. Most cars are very high mileage, which appeals to customers, but they also are pretty inexpensive to buy. Their approach doesn’t take-on the traditional car rental company, but is growing quite handily.

This same logic applies to internal company investments as well. Far too often the corporate reource allocation process is designed to fight a gladiator war. Constantly spending to do more of the same. Projects become over-funded to fight battles considered “necessity,” while new projects are unfunded despite having the opportunity for much higher rates of return.

In 2000, Apple could have chosen to keep pouring money into the Mac. Instead it radically cut spending, reduced Mac platforms, and started looking for new markets where it could bring in new solutions. IPods, iTunes, IPhones, iPads and iCloud are now driving growth for the company – all new approaches that avoided gladiator battles with old market competitors. Very profitable growth. Apple has enough cash on hand to buy every phone maker, except Samsung – or Apple could buy Dell – if it wanted to. Apple’s market cap is worth more than Microsoft and Intel combined.

If you want to make more money, it’s best to avoid gladiator wars. They are great spectator events – but terrible places to be a participant. Instead, set your organization to find new ways of competing, and invest where you are doing what competitors are not. That will earn the greatest rate of return.

“Blame Piles Up in Tribune Cos. 2007 Buyout” is the Chicago Tribune headline. After months of research the bankruptcy judge has released a court ordered report on the transaction that left Tribune Corporation insolvent. Apparently, lots of people were aware that ad demand was falling like a stone. And that there was little hope it would recover. But selling executives shopped for a valuation company until they found one willing to say that management’s projections were plausible. Of course, they weren’t. The transition from print to digital was well along, and the projections were never going to happen.

What’s more startling is the hubris of Sam Zell to close the deal. Apparently he too had doubts about the forecasts, but he went ahead and borrowed all that money to close. That he would ignore all the market signals, and plenty of opportunities to obtain outsider input on the likely continued demise of newspaper ads, shows he wanted to close. He wanted to control Tribune Corporation. Even if it would cost him $300m.

Success Formulas are very powerful. And successful entrepreneurs often have them so locked-in that there’s no other consideration. Success, and personal fortunes, causes them to ignore external data, and external opinions, when they fly in the face of their historical Success Formula. They want to apply it to a new business, and they are ready to go! So damn the torpedos! Full speed ahead!

It’s too bad that our hero worship of successful entrepreneurs too often leaves them insufficiently challenged. Unfortunately, a lot of people got hurt in the calamity that is now the Tribune Corporation bankruptcy. Employees have lost pay, benefits and jobs. Chicagoans have seen the paper get even smaller, and the amount of local news coverage decline. And the city’s reputation has certainly not benefited.

As much as people despise consultants, it would seem that Mr. Zell would have been a lot smarter to ask some bright strategists what the future was for the newspaper before abetting the close of such an onerous, and destructive, transaction. Outsiders, including consultants, are valuable at pointing out the range of potential outcomes – not just the one that fits your Success Formula. That’s why successful organizations use outsiders to help develop scenarios and study competitors, as well as design Disruptions and establish White Space projects. Outsiders can help overcome Lock-in to historical assumptions, biases, prejudice and viewpoints in order to reduce failures and improve success.

And this is some advice hopefully Leonard Riggio will heed. “Barnes & Noble Considering Sale of Company; Possible Buyers Include Founder Leonard Riggio” is the Chicago Tribune headline. Barnes & Noble as an acquisition looks a lot like Tribune did 3 years ago. Product sales (printed books) are in a free-fall as people choose alternative products – especially digital books and journals. Books themselves are struggling to avoid obsolescence as digital publishing makes shorter format more valuable in many instances. Brick and mortar shops focused on printed material – from bookstores to magazine/news stands – have been failing for 10 years – and in fact overall brick and mortar retail across the board has declined the last 4 years as internet retailing has grown. The leading competitor (Amazon) has led the transition to digital, and is competing with an enormously successful tech company (Apple) for the future of digital publishing. Barnes & Noble may have a fledgling product, but it’s about as competitive as a junior leaguer compared to someone on the Yankees!

The Success Formula of Barnes & Noble, as created by the original founder, is obsolete. And B&N is not in the game for where the marketplace is headed. Just because he knew the business once, years ago, gives the founder no leg-up on resurrecting the company. Contrarily, his background is a decided negative as he’s likely to attempt a “throwback” strategy. Since the world goes forward, never backward, those simply don’t work. We could expect lots of store closings, layoffs and inventory reductions – but the future of publishing has radically changed and will continue doing so, and B&N has little input on that outcome. Amazon, Apple and Google (the largest purveyor of digital words through its search engine) are the giants in this game and B&N will get crushed.

And the city of Milwaukee should consider hiring some consultants, as should Harley Davidson. “In Quest for Lower Cost Harley-Davidson Considers Leaving Milwaukee after 107 years” reports Chicago Tribune. Harley would like subsidies, from its workers (unions) as well as the city and state, to keep from moving its factories. But Harley’s problems are far worse than hourly wages for plant workers, and everyone needs to be careful not to get sucked into a Tribune Corp. deal of trying to save a floundering ship.

Harley Davidson’s product has been largely unchanged for a very long time. Despite all the hoopla about tattooed customers, for 30 years competitors Honda, Suzuki, Kawasaki and Yamaha have been innovating and running circles around Harley. Their businesses have grown. Not only by dramatically expanding their motorcycle products, but adding ATVs, snowmobiles, boat engines, automobiles, electric generators, yard equipment and a raft of other products (Honda even makes a commercial airplane!) They have brought in millions of new customers, while Harley’s customer base is eroding – largely dying off as the average age of buyers has risen to well over 50!!

While competitors have pushed forward with new technology and products, and developed new markets and customers, Harley has tried standing still. So, its now an historical anachronism. Interesting to look at, and with some intriguing niches, but not really important to the industry. Should Harley disappear nobody in the motorcycle business will really notice, because almost every competitor now has a Harley-inspired v-twin motorcycle they can sell. Few people realize that most dealers make more money selling jackets and other Harley-Licensed gear/apparel than motorcycles! Harley’s days have been numbered since they let the v-Rod, a motorcycle with a Porsche engine, languish in dealer showrooms – allowing their “customers” to keep them locked-in to aging technology at ever rising prices (they typical Harley prices for over 2x the price of a comparable Japanese produced motorcycle.) Harley should have paid more attention to competitors a long time ago (instead of deriding them as “rice burners”) and a lot less attention to those very loyal – but diminishing in numbers – dealers and end-use customers.

All 3 of these companies, Tribune, Barnes & Noble and Harley-Davidson have great pasts. But the risk is thinking that means anything about the future. Tribune was fatally harmed by adding debt to a company that needed to refocus on new internet markets, then continuing to try to keep the old Success Formula operating. Barnes & Noble is the last prominent brick and mortar book retailer, but there is little reason to think there will be a need for them in just 5 years. And Harley-Davidson every year appeals to a smaller group of buyers in a niche market with aged technology and a tiring brand. In all cases, caveat emptor! (Let the buyer beware!) Before accepting any management forecasts, it would be a good idea to get some external opinions!

"From the day we start kindergarten we fear the teacher's call to our

parents saying, "Hello Mr. and Mrs. Smith. I'm sorry to tell you that

Mary has been disruptive in class." We are taught, trained and

indoctrinated to go along and get along, to not disrupt. In fact we're

constantly told to seek harmony. But in business that can destroy your

entire value."

That's the first paragraph from my Forbes.com column, posted today,"To Succeed You Must Seriously Disrupt." Companies that don't Disrupt remain Locked-in to Success Formulas with declining value until all hope is lost – just look at Sun Microsystems. Although Chairman Scott McNealy was famous for his Disruptive corporate behavior – he was unwilling to tolerate disruptions from his own organization to the company business model. In 10 years Sun went from $200B market cap to out of business.

Now Toyota is struggling because it wouldn't Disrupt. Meanwhile Honda is doing much better than most, because it is willing to Disrupt. Listen to the 40 second video on Disruptions, and read the article so you can see the need for Disruption and adopt in your business!

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]

Remarkably, the Model 3 would rank as the 6th best selling vehicle all of last year! And with just a few more orders, it will likely make the top 5 – or possibly top 3! And those are orders placed in just one week, versus an entire year of sales for the other models. And every buyer is putting up a $1,000 deposit, something none of the buyers of top 10 cars did as they purchased product widely available in inventory. [Update 7 April – Tesla reports sales exceed 325,000, which would make the Model 3 the second best selling car in the USA for the entire year 2015 – accomplished in less than one week.]