by Adam Hartung | Nov 25, 2015 | Innovation, Leadership, Transparency

No. You’re not seeing things. These are goats in trees.

These goats love the fruit growing on argon trees west of Marrakesh, Morocco. They don’t care so much for the nut inside, so they spit it out. People gather those nuts and make them into argon oil highly valued for food and in beauty products.

I was startled by these goats. It was, at the very least, mentally disruptive. As I thought about the experience, I realized there were leadership lessons to be learned from these tree climbing goats:

- These goats don’t chase low hanging fruit. What they want is up in the trees, and the challenge did not stop them. It takes extraordinary measures to accomplish what they want, but they invested in the effort to be extraordinary. Once they learned to climb trees, something they easily could say was “not their core strength,” they left behind what was on the ground for the riches of success. These goats prove that if what you want is in the trees, you have to go for it. One should not settle for less. No leader should stay so focused on the past that they can’t figure out new ways to compete, and succeed.

- Once they became known for doing extraordinary things, people flocked to be next to these goats. People want to be near goats that are unusual, and in some way better than other goats. By seeking the extraordinary, and accomplishing the extraordinary, these goats merely need to “do their thing” and people are attracted to them. People will feed these goats, and even pay their shepherds to be next to them and take photos. Being extraordinary creates a winning situation that feeds on itself, creating additional wins – including attracting people to you.

- Because of their willingness to do something extraordinary, these goats have control over their shepherds. In a real way, the shepherds need the goats much more than the goats need the shepherds. The power wielded by tree climbing goats is not from being brutal, or micromanaging, or being “charismatic.” They simply developed their power via their willingness to do something extraordinary — something their shepherds will not do. Something most people will not do. Simultaneously, the goats share their wealth with the shepherds. While they receive lots of their favorite foods, the shepherds receive payments. The goats have a symbiotic, sharing relationship with their handlers, and the people who visit and feed them, where everyone wins.

Here’s the bottom line:

No matter what you are doing, strive for the extraordinary. You are not limited by “core strengths,” nor your past. If you can visualize a goal you can seek that goal and you can work to accomplish that goal. You can be extraordinary if you are willing to break out of your old self-definition and try. These goats didn’t become successful tree climbers in one day, but by accomplishing their goal over time they became quite extraordinary.

It is good to be extraordinary. Don’t just go for the low-hanging fruit, or what is easy. Innovate. Be disruptive. The path may not be easy, or obvious, but the payoff can be as extraordinary as the accomplishment.

So what’s stopping you from being extraordinary? What locks you in to your definition of your old “self?” What goal can you set, and work to accomplish, that will set you apart and demonstrate you are extraordinary, and a leader someone should admire?

by Adam Hartung | Oct 5, 2015 | Current Affairs, In the Rapids, Innovation, Leadership, Web/Tech

Twitter’s Board decided in July to oust the CEO, Dick Costolo, due to frustration over company profits. As I wrote at the time, Twitter had continued to add members, at a rate comparable to its social media competition. And it had grown revenues, while remaining the industry leader in revenue per active user.

But the concern was a lack of profits. Oh my, if rapid revenue growth but weak profits were a reason to fire a CEO, how does Jeff Bezos keep his job?

Anyway, Mr. Costolo was replaced by an original founder and former Twitter CEO Jack Dorsey on an interim basis. Four months later, after failing in its effort to find a suitable full-time CEO, the Board has made Mr. Dorsey the permanent CEO. While he simultaneously remains full time CEO of Square, a mobile payments processing company.

As I said in my last column on this subject, investors better beware.

Facebook is tearing up the social media market. It has grown to be not only #1 in active monthly users, but at 1.5B monthly active users (MSUs) the site has 5 times the number of users that Twitter has. By adding a slew of new features and functions Facebook has become more valuable to its users – and advertisers.

According to Statista, simultaneously Facebook has grown Facebook Messenger to 700M MSUs, acquired WhatsApp with 800M MSUs and Instagram with 400M MSUs. By constantly expanding the ecosphere Facebook now has 3.4B MSUs – over 10 times the number of Twitter. Facebook is so dominant that even muscular Google, with all its resources, abandoned its efforts to compete with the juggernaut by killing Google+ (which had 300M MSUs) earlier in 2015.

Twitter had great organic growth numbers, but unlike competitors it does not dominate any particular category of social media. Linked in, with only 100M MSUs dominates business networking, and bosts a user base that skews older and more professional. Pinterest and Instagram are battling it out for leadership in photo sharing. But it is unclear how one would describe a social growth category that Twitter dominates.

I actively use Twitter. But among my peers I am the exception. When I ask people over 40 if they use Twitter I regularly hear “I don’t get it. It all looks completely chaotic. Why would I want to follow people on Twitter, and why would I want to post.” This sounds a lot like what people said of Facebook and Linked in 5 years ago. But those companies found their connection with users and people now “get it.”

So the question is whether Mr. Dorsey will make Twitter into a site that is ubiquitous, at least for one category. Can he make the product so useful that users can’t live without it, and that continues drawing in massive new numbers of users?

Twitter has not changed much at all since it was founded. It still depends on users to sign on, start tweeting, and search out others a user wants to follow. And that means follow for some reason other than that person is a celebrity or politician that simply can’t stop spouting off. The Twitter user has to hunt for like minded individuals, find a way to connect with folks who are informative to their needs and then create a dialogue — and all with pretty much the same character limits and shrunken link technology available many years ago.

Apple floundered as a manufacturer of niche PCs. The returning CEO, Steve Jobs, resurrected the company by putting all his money on mobile. It wasn’t an improved Mac that turned around Apple, but rather the launch of the iPod and iTunes, followed by the iPhone and the iPad. The way Apple stole the thunder from previously dominant Microsoft was by creating new products built on the mobile trend that led to explosive growth.

Mr. Costolo left Twitter in far better shape than Apple was in when Mr. Jobs retook the reins. But will Mr. Dorsey be able to launch a series of new products that can create an Apple-like growth explosion?

Square, where Mr. Dorsey ostensibly spends half his time, is preparing to go public. But, even though it is currently considered by many the leader in its marketplace, Square is looking down the barrel of ApplePay – a technology on every iPhone that could make it obsolete. Then there’s also Google Wallet that is on all the other smartphones. Plus well funded outfits like PayPal and Mastercard. Square will need a very competent, capable and visionary CEO to guide its development competing with these – and other – well funded and powerful companies. Square will need to add features, functions and benefits if it is create long-term value.

A lot of new products are needed by two relatively small companies in short order if they are to survive. Success will not happen by cutting costs in either. It will require intensive product development with very rapid product cycles that bring in millions upon millions of new users.

Twitter was once a disruptive innovator. Now it is hard to recognize any innovation at Twitter. Does Mr. Dorsey get it? And if he does, can he do it? And do it twice, simultaneously?

by Adam Hartung | Sep 22, 2015 | Current Affairs, Disruptions, In the Rapids, Innovation

A recent analyst took a look at the impact of electric vehicles (EVs) on the demand for oil, and concluded that they did not matter. In a market of 95million barrels per day production, electric cars made a difference of 25,000 to 70,000 barrels of lost consumption; ~.05%.

You can’t argue with his arithmetic. So far, they haven’t made any difference.

But then he goes on to say they won’t matter for another decade. He forecasts electric vehicle sales grow 5-fold in one decade, which sounds enormous. That is almost 20% growth year over year for 10 consecutive years. Admittedly, that sounds really, really big. Yet, at 1.5million units/year this would still be only 5% of cars sold, and thus still not a material impact on the demand for gasoline.

But then he goes on to say they won’t matter for another decade. He forecasts electric vehicle sales grow 5-fold in one decade, which sounds enormous. That is almost 20% growth year over year for 10 consecutive years. Admittedly, that sounds really, really big. Yet, at 1.5million units/year this would still be only 5% of cars sold, and thus still not a material impact on the demand for gasoline.

This sounds so logical. And one can’t argue with his arithmetic.

But one can argue with the key assumption, and that is the growth rate.

Do you remember owning a Walkman? Listening to compact discs? That was the most common way to listen to music about a decade ago. Now you use your phone, and nobody has a walkman.

Remember watching movies on DVDs? Remember going to Blockbuster, et.al. to rent a DVD? That was common just a decade ago. Now you likely have shelved the DVD player, lost track of your DVD collection and stream all your entertainment. Bluckbuster, infamously, went bankrupt.

Do you remember when you never left home without your laptop? That was the primary tool for digital connectivity just 6 years ago. Now almost everyone in the developed world (and coming close in the developing) carries a smartphone and/or tablet and the laptop sits idle. Sales for laptops have declined for 5 years, and a lot faster than all the computer experts predicted.

Markets that did not exist for mobile products 10 years ago are now huge. Way beyond anyone’s expectations. Apple alone has sold over 48million mobile devices in just 3 months (Q3 2015.) And replacing CDs, Apple’s iTunes was downloading 21million songs per day in 2013 (surely more by now) reaching about 2billion per quarter. Netflix now has over 65million subscribers. On average they stream 1.5hours of content/day – so about 1 feature length movie. In other words, 5.85billion streamed movies per quarter.

What has happened to old leaders as this happened? Sony hasn’t made money in 6 years. Motorola has almost disappeared. CD and DVD departments have disappeared from stores, bankrupting Circuit City and Blockbuster, and putting a world of hurt on survivors like Best Buy.

The point? When markets shift, they often shift a lot faster than anyone predicts. 20%/year growth is nothing. Growth can be 100% per quarter. And the winners benefit unbelievably well, while losers fall farther and faster than we imagine.

Tesla was barely an up-and-comer in 2012 when I said they would far outperform GM, Ford and Toyota. The famous Bob Lutz, a long-term widely heralded auto industry veteran chastised me in his own column “Tesla Beating Detroit – That’s Just Nonsense.”

Mr. Lutz said I was comparing a high-end restaurant to McDonald’s, Wendy’s and Pizza Hut, and I was foolish because the latter were much savvier and capable than the former. He should have used as his comparison Chipotle, which I predicted would be a huge winner in 2011. Those who followed my advice would have made more money owning Chipotle than any of the companies Mr. Lutz preferred.

The point? Market shifts are never predicted by incumbents, or those who watch history. The rate of change when it happens is so explosive it would appear impossible to achieve, and far more impossible to sustain. The trends shift, and one market is rapidly displaced by another.

While GM, Ford and Toyota struggle to maintain their mediocrity, Tesla is winning “best car” awards one after another – even “breaking” Consumer Reports review system by winning 103 points out of a maximum 100, the independent reviewer liked the car so much. Tesla keeps selling 100% of its production, even at its +$100K price point.

So could the market for EVs wildly grow? BMW has announced it will make all models available as electrics within 10 years, as it anticipates a wholesale market shift by consumers promoted by stricter environmental regulations. Petroleum powered car sales will take a nosedive.

The International Energy Agency (IEA) points out that EVs are just .08% of all cars today. And of the 665,000 on the road, almost 40% are in the USA, where they represent little more than a rounding error in market share. But there are smaller markets where EV sales have strong share, such as 12% in Norway and 5% in the Netherlands.

So what happens if Tesla’s new lower priced cars, and international expansion, creates a sea change like the iPod, iPhone and iPad? What happens if people can’t get enough of EVs? What happens if international markets take off, due to tougher regulations and higher petrol costs? What happens if people start thinking of electric cars as mainstream, and gasoline cars as old technology — like two-way radios, VCRs, DVD players, low-definition picture tube TVs, land line telephones, fax machines, etc?

What if demand for electric cars starts doubling each quarter, and grows to 35% or 50% of the market in 10 years? If so, what happens to Tesla? Apple was a nearly bankrupt, also ran, tiny market share company in 2000 before it made the world “i-crazy.” Now it is the most valuable publicly traded company in the world.

Already awash in the greatest oil inventory ever, crude prices are down about 60% in the last year. Oil companies have already laid-off 50,000 employees. More cuts are planned, and defaults expected to accelerate as oil companies declare bankruptcy.

It is not hard to imagine that if EVs really take off amidst a major market shift, oil companies will definitely see a precipitous decline in demand that happens much faster than anticipated.

To little Tesla, which sold only 1,500 cars in 2010 could very well be positioned to make an enormous difference in our lives, and dramatically change the fortunes of its shareholders — while throwing a world of hurt on a huge company like Exxon (which was the most valuable company in the world until Apple unseated it.)

[Note: I want to thank Andreas de Vries for inspiring this column and assisting its research. Andreas consults on Strategy Management in the Oil & Gas industry, and currently works for a major NOC in the Gulf.]

by Adam Hartung | Aug 27, 2015 | In the Rapids, Innovation, Investing, Leadership, Web/Tech

As market volatility reached new highs this week, CNBC began talking about something called “FANG Investing.” Most commentators showed great displeasure in the fact that prior to the recent downturn high growth companies such as Facebook, Amazon, Netflix and Google (FANG) had performed much better than all the major market indices. And, in the short burst of recent recovery these companies again seemed to be doing much better.

Coined by “CNBC Mad Money” host Jim Cramer, he felt that FANG investing was bad for investors. He said he preferred seeing a much larger group of companies would go up in value, thus representing a much more stable marketplace.

Coined by “CNBC Mad Money” host Jim Cramer, he felt that FANG investing was bad for investors. He said he preferred seeing a much larger group of companies would go up in value, thus representing a much more stable marketplace.

Sound like Wall Street gobblygook? Good. Because as an individual investor why should you care about a stable market? What you should care about is your individual investments going up in value. And if yours go up and all others go down what difference does it make?

Most financial advisers today actually confuse investors much more than help them. And nowhere is this more true than when discussing risk. All financial advisers (brokers in the old days) ask how much risk you want as an investor. If you’re smart you say “none.” Why would you want any risk? You want to make money.

Only this is the wrong answer, because most investors don’t understand the question – because the financial adviser’s definition of risk is nothing like yours.

To a broker investment risk is this bizarre term called “beta,” created by economists. They defined risk as the degree to which a stock does not move with the market index. If the S&P down 5%, and the stock goes down 5%, then they see no difference between the stock and the “market” so they say it has no risk. If the S&P goes up 3% and the stock goes up 3%, again, no risk.

But if a stock trades based on its own investor expectation, and does not track the market index, then it is considered “high beta” and your broker will say it is “high risk.” So let’s look at Apple the last 5 years. If you had put all your money into Apple 5 years ago you would be up over 200% – over 4x. Had you bought the S&P 500 Index you would be up 80%. Clearly, investing in Apple would have been better. But your adviser would say that is “high risk.” Why? Because Apple did not move with the S&P. It did much better. It is therefore considered high beta, and high risk.

You buy that?

Thus, brokers keep advising investors buy funds of various kinds. Because the investors says she wants low risk, they try to make sure her returns mirror the indices. But it begs the question, why don’t you just buy an electronic traded fund (ETF) that mirrors the S&P or Dow, and quit paying those fund fees and broker fees? If their approach is designed to have you do no better than the average, why not stop the fees and invest in those things which will exactly give you the average?

Anyway, what individual investors want is high returns. And that has nothing to do with market indices or how a stock moves compares to an index. It has to do with growth.

Growth is a wonderful thing. When a company grows it can write off big mistakes and nobody cares. It can overpay employees, give them free massages and lunches, and nobody cares. It can trade some of its stock for a tiny company, implying that company is worth a vast amount, in order to obtain new products it can push to its customers, and nobody cares. Growth hides a multitude of sins, and provides investors with the opportunity for higher valuations.

On the other hand, nobody ever cost cut a company into prosperity. Layoffs, killing products, shutting down businesses and selling assets does not create revenue growth. It causes the company to shrink, and the valuation to decline.

That’s why it is lower risk to invest in FANG stocks than those so-called low-risk portfolios. Companies like Facebook, Amazon, Netflix, Google — and Apple, EMC, Ultimate Software, Tesla and Qualcomm just to name a few others — are growing. They are firmly tied to technologies and products that are meeting emerging needs, and they know their customers. They are doing things that increase long-term value.

McDonald’s was a big winner for investors in the 1960s and 1970s as fast food exploded with the baby boomer generation. But as the market shifted McDonald’s sold off its investments in trend-linked brands Boston Market and Chipotle. Now its revenue has stalled, and its value is in decline as it shuts stores and lays off employees.

Thirty years ago GE tied its plans to trends in medical technology, financial services and media, and it grew tremendously making fortunes for its investors. In the last decade it has made massive layoffs, shut down businesses and sold off its appliance, financial services and media businesses. It is now smaller, and its valuation is smaller.

Caterpillar tied itself to the massive infrastructure growth in Asia and India, and it grew. But as that growth slowed it did not move into new businesses, so its revenues stalled. Now its value is declining as it lays off employees and shuts down business units.

Risk is tied to the business and its future expectations. Not how a stock moves compared to an index. That’s why investing in high growth companies tied to trends is actually lower risk than buying a basket of stocks — even when that basket is an index like DIA or SPY. Why should you own the low-or no-growth dogs when you don’t have to? How is it lower risk to invest in a struggling McDonald’s, GE or Caterpillar or some basket that contains them than investing in companies demonstrating tremendous revenue growth?

Good fishermen go where the fish are. Literally. Anybody can cast out a line and hope. But good fisherman know where the fish are, and that’s where they invest their bait. As an investor, don’t try to fish the ocean (the index.) Be smart, and put your money where the fish are. Invest in companies that leverage trends, and you’ll lower your risk of investment failure while opening the door to superior returns.

by Adam Hartung | Aug 6, 2015 | In the Rapids, Innovation, Leadership, Web/Tech

Would you like to triple your revenue next year? And have plans to keep tripling it – or more – every year into the future?

Of course you would. But is your business positioned for such explosive growth? Are you in growth markets, creating new products with new technologies that meet unmet needs and have the potential to completely change your business? Or are you stuck doing the same thing you’ve always done, a litle better, faster and cheaper in hopes you can just maintain your position?

If you’re constantly looking at your “core” markets and solutions, and you know those aren’t going to grow fast, what keeps you from changing to make your company a high growth winner?

First, most people don’t try. Leaders say it all the time, “I’m so busy running a business I don’t have time to chase rainbows. Sure technology is changing, but I don’t understand it, nor know how to use it. I’m better off investing in what I know than trying to chase trends.” That’s often followed by dragging out the old saw, usually attributed to Warren Buffet, of “don’t invest in what you don’t know – and I don’t know anything about trends.” The comfort, and ease, of repeating what you’ve always done allows lethargy to set in – so you keep doing more and more of what you’ve always done, over and again, hoping for a different result. It’s been attributed to Albert Einstein that such behavior is the very definition of insanity.

Everyone is busy. We live in a “culture of busy.” Years of layoffs and cost reductions have left most leaders simply struggling to keep up with making and selling last year’s solution. Constant busy-ness becomes a convenient excuse to not take the time to look at trends, evaluate new opportunities or consider doing things entirely differently. Busy, busy, busy – until someone knocks your business off its blocks and then you have all kinds of time on your hands.

For those who overcome these 2 built-in biases, the opportunities today are extra-ordinary. It is possible to slingshot into leadership positions with new solutions, literally from out of nowhere. If you take the time and try. Listen, and just do it – to steal from a popular ad campaign.

ikeGPS was started in 2003 as a government/military funded products research company. Focusing on the technology of lasers and cameras, they won contracts to develop and prototype new solutions with technology mostly buried in universities and labs. It was a good business, made money for the founders, and was intellectually stimulating. If not growing very fast or showing much potential of growing.

Eventually ikeGPS started making products with lasers and cameras for finding physical assets. This turned out to be quite beneficial for electric utilities, which have to maintain some 200,000 power poles in the U.S alone. EPC (Engineering, Procurement and Construction) companies like Black & Veatch, Bechtel. Burns & McDonel , FMC and Foster Wheeler had a need to find big physical things, then measure their size and location between each other and major points. For utility company suppliers like GE laser cameras for asset location were a handy, if slow growing business. Good, solid, reliable revenues, but not something that was going to create a $100M company.

So the Managing Director, Glenn Milnes, and Chief Marketing Officer, Jeff Ross, set about to see what they could do to become a $100M business. Not because anything in their history said they could do so. Rather because they wanted to make their company a bigger, faster growing and lot more valuable entity.

The first thing they identified was the trend to mobile devices. They noticed darn near everyone has one, and they were using them for all kinds of interesting things. There were thousands and thousands of apps, but none that really took advantage of the cameras to do much measuring, or integrated lasers. While they didn’t know anything about mobile operating systems, or much about the kinds of cameras in mobile phones or the software used for popular mobile camera uses – they could see a trend.

What if they could take their knowledge about lasers and cameras and figure out how to make mobile phones a lot more powerful? Could they apply what they knew into markets where they had no experience, using technologies with which they had no experience? Would it work, or waste their time? If it worked, what would they make? If they made something, who would buy it?

Despite these great questions, they wanted ikeGPS to grow, and they decided to take the cash flow from their solid, but low growth historical business and plow it into development of a new product. So they took to internal company brainstorming to see what they might do. And they came up with the very clever idea of making an add-on device that construction workers, like concrete installers, pavers, carpenters, masons and such, could use with their mobile phones to replace tape measures. Something that would be simple, easy to use, work with the phones in their pockets and be a lot more accurate than decades-old technology.

So they went to the lab and built it. They started design in October, 2013, and a year later they had a product ready to launch. – Spike! They took it to social media, Google adwords, all the low-cost ad tools available to small business today. They also went to industry trade shows, bought some ads in industry trade magazines and ads on industry specific sites. Things were OK, but it was a slow slog.

So they went to the lab and built it. They started design in October, 2013, and a year later they had a product ready to launch. – Spike! They took it to social media, Google adwords, all the low-cost ad tools available to small business today. They also went to industry trade shows, bought some ads in industry trade magazines and ads on industry specific sites. Things were OK, but it was a slow slog.

As they were preparing to launch Spike they thought, “why don’t we reach for outsiders to gain some input on this product. Let’s hear what others might have to say.” So they launched a Kickstarter campaign, offering investors the product to try. Via this route they gained the eyes and ears of early adopters.

This was when the surprise happened. The earliest adopters, and biggest fans of laser measuring via mobile devices weren’t in the construction business. They were signage companies. ikeGPS listened to their feedback, and realized they could tweek Spike to be very relevant for folks in signage. The made themselves accessible to these early adopters, and turned a few into fanatical loyalists.

With this early success, they began to downplay construction and seek signage companies. Across 2 months they placed about $20k (not millions, thousands) in ads in the 4 largest publishers to the signage industry. This led to on-line product sales, and smashing reviews.

So then they made overtures to the large franchisors of signage related shops – with retail names like Fast Sign, Sign-o-Rama, Alphagraphics, Speedy Sign, Sign World, etc — in companies like Franchise Services and Alliance Franchise. Within 6 months of launch they had stopped chasing construction customers and were full-tilt developing signage companies, to great success. Even sign supply companies llke Reece Sign saw the benefit of promoting (and even reselling) these new laser camera add-ons for mobile devices to stimulate sales and move sign design and creation into the 21st century.

After making this switch, they initial launch sold 1,200 units at $500/unit retail . But better yet, contracts for promotion and reselling has the company convinced they will blow far beyond their projection of 4,000 units in the first year.But they did not simply forget about construction. The idea was still sound, but clearly the market had not developed. So they asked themselves, “if we listened to sign guys and they told us what to do, could we listen to construction guys for advice?”

They pursued finding out more about construction, and learned the market was dominated by brand names. Few products were bought without a strong brand name – and most products are purchased through the very large home improvement chains such as Home Depot, Lowe’s, Menard’s and others. But that would be a nearly impossible task, at extremely high cost, for little ikeGPS. So they pursued finding a partner which knew the industry.

In early 2015 ideGPS announced that Stanley Black&Decker would brand and sell Spike via traditional retail. The product should be on shelves before the end of year, and substantial additional sales volumes are expected.

In 2013 100% of ikeGPS revenues were in their traditional government/military and utility markets with their bespoke device. In just one year they developed a mobile device, and launched it. In 2015 1/3 or more of their $10.5 estimated revenue will be from Spike, and they expect to at a minimum triple revenues in 2016. And they think that rate of growth is sustainable into future years.

ikeGPS shows that it IS possible to move beyond historical markets and create new products for break-out growth. You aren’t stuck in old businesses with no hope of growth. if you want to grow, and reap the rewards of growth, you can. You have to

- Want to do it

- Take time to do it

- Pay attention to trends, and support obvious trend growth

- Learn about new technologies and how you can apply them. Start with the trend technologies first, then see how to apply something new. Don’t start by trying to push what you know onto another platform. Be ethnocentric in product development, not egocentric.

- Brainstorm how to meet unmet needs

- Listen to early sales results, and go where the need is highest/selling is easiest

- Don’t forget to learn from what did not work, and see if you can overcome early weaknesses.

by Adam Hartung | Jun 7, 2015 | Defend & Extend, In the Swamp, Innovation, Leadership, Transparency

Did you ever notice that Human Resource (HR) practices are designed to lock-in the past rather than grow? A quick tour of what HR does and you quickly see they like to lock-in processes and procedures, insuring consistency but offering no hope of doing something new. And when it comes to hiring, HR is all about finding people that are like existing employees – same school, same degrees, same industry, same background. And HR tries its very hardest to insure conformity amongst employees to historical standard – especially regarding culture.

Several years ago I was leading an innovation workshop for leaders in a company that made nail guns, screw guns, nails and screws. Once a market leader, sales were struggling and profits were nearly nonexistent due to the emergence of competitors from Asia. Some of their biggest distributors were threatening to drop this company’s line altogether unless there were more concessions – which would insure losses.

They liked to call themselves a “fastener company,” which has long been the trend with companies that like to make it sound as if they do more than they actually do.

I asked the simple question “where is the growth in fasteners?” The leaders jumped right in with sales numbers on all their major lines. They were sure that growth was in auto-loading screwguns, and they were hard at work extending this product line. To a person, these folks were sure they new where growth existed.

But I had prepared prior to the meeting. There actually was much higher growth in adhesives. Chemical attachment was more than twice the growth rate of anything in the old nail and screw business. Even loop-and-hook fasteners [popularly referred to by the tradename Velcro(c)] was seeing much greater growth than the old-line mechanical products.

They looked at me blank-faced. “What does that have to do with us?” the head of sales finally asked. The CEO and everyone else nodded in agreement.

I pointed out to them they said they were in the fastener business. Not the nail and screw business. The nail and screw business had become a bloody fight, and it was not going to get any better. Why not move into faster growing, less competitive products?

Competitors were making lots of battery powered and air powered tools beyond nail guns and screw guns, and their much deeper product lines gave them much higher favorability with retail merchandisers and professional tool distributors. Plus, competitor R&D into batteries was already showing they could produce more powerful and longer-lasting tools than my client. In a few major retailers competitors already had earned the position of “category leader” recommending the shelf space and layout for ALL competitors, giving them a distinct advantage.

This company had become myopic, and did not even realize it. The people were so much alike that they could finish each others sentences. They liked working together, and had built a tightly knit culture. The HR head was very proud of his ability to keep the company so harmonious.

Only, it was about to go bankrupt. Lacking diversity in background, they were unable to see beyond their locked-in business model. And there sure wasn’t anyone who would “rock the boat” by admitting competitors were outflanking them, or bringing up “wild ideas” for new markets or products.

According to the New York Times 80% of hiring is done based on “cultural fit.” Which means we hire people we want to hang out with. Which almost always means people that are a lot like ourselves. Regardless of what we really need in our company. Thus companies end up looking, thinking and acting very homogenously.

It is common amongst management authors and keynote speakers to talk about creating “high-performance teams.” The vaunted Jim Collins in “Good to Great” uses the metaphor of a company as a bus. Every company should have a “core” and every employee should be single-mindedly driving that “core.” He says that it is the role of good leaders to get everyone on the bus to “core.” Anyone who isn’t 100% aligned – well, throw them off the bus (literally, fire them.)

We see this phenomenon in nepotism. Where a founder, CEO or Chairperson who succeeds uses their leadership position to promote relatives into high positions.

Wal-Mart’s Board of Directors, for example, recently elected the former Chairman’s son-in-law to the position of Chairman. He appears accomplished, but today Wal-Mart’s problem is Amazon and other on-line retail. Wal-Mart desperately needs outside thinking so it can move beyond its traditional brick-and-mortar business model, not someone who’s indoctrinated in the past.

The Reputation Institute just completed its survey of the most reputable retailers in the USA. Top of the list was Amazon, for the third straight year. Wal-Mart wasn’t even in the top 10, despite being the largest U.S. retailer by a considerable margin. Wal-Mart needs someone at the top much more like Jeff Bezos than someone who comes from the family.

Despite what HR often says, it is incredibly important to have high levels of diversity. It’s the only way to avoid becoming myopic, and finding yourself with “best practices” that don’t matter as competitors overwhelm your market.

Despite what HR often says, it is incredibly important to have high levels of diversity. It’s the only way to avoid becoming myopic, and finding yourself with “best practices” that don’t matter as competitors overwhelm your market.

Ever wonder why so many CEOs turn to layoffs when competitors cause sales and/or profits to stall? They are trying to preserve the business model, and everyone reporting to them is doing the same thing. Instead of looking for creative ways to grow the business – often requiring a very different business model – everyone is stuck in roles, processes and culture tied to the old model. As everyone talks to each other there is no “outsider” able to point out obvious problems and the need for change.

In 2011, while he was still CEO, I wrote a column titled “Why Steve Jobs Couldn’t Find a Job Today.” The premise was pretty simple. Steve Jobs was not obsessed with “cultural fit,” nor was he a person who shied away from conflict. He obsessed about results. But no HR person would consider a young Steve Jobs as a manager in their company. He would be considered too much trouble.

Yet, Steve Jobs was able to take a nearly dead Macintosh company and turn it into a leader in mobile products. Clearly, a person very talented in market sensing and identifying new solutions that fit trends. And a person willing to move toward the trend, rather than obsess about defending and extending the past.

Does your organization’s HR insure you would seek out, recruit and hire Steve Jobs, or Jeff Bezos? Or are you looking for good “cultural fit” and someone who knows “how to operate within that role.” Do you look for those who spot and respond to trends, or those with a history related to how your industry or business has always operated? Do you seek people who ask uncomfortable questions, and propose uncomfortable solutions – or seek people who won’t make waves?

Does your organization’s HR insure you would seek out, recruit and hire Steve Jobs, or Jeff Bezos? Or are you looking for good “cultural fit” and someone who knows “how to operate within that role.” Do you look for those who spot and respond to trends, or those with a history related to how your industry or business has always operated? Do you seek people who ask uncomfortable questions, and propose uncomfortable solutions – or seek people who won’t make waves?

Too many organizations suffer failure simply because they lack diversity. They lack diversity in geographic sales, markets, products and services – and when competition shifts sales stall and they fall into a slow death spiral.

And this all starts with insufficient diversity amongst the people. Too much “cultural fit” and not enough focus on what’s really needed to keep the organization aligned with customers in a fast-changing world. If you don’t have the right people around you, in the discussion, then you’re highly unlikely to develop the right solution for any problem. In fact, you’re highly unlikely to even ask the right question.

by Adam Hartung | Apr 30, 2015 | Current Affairs, Defend & Extend, In the Rapids, Innovation, Leadership, Web/Tech

Last week saw another slew of quarterly earnings releases. For long term investors, who hold stocks for years rather than months, these provide the opportunity to look at trends, then compare and contrast companies to determine what should be in their portfolio. It is worthwhile to compare the trends supporting the valuations of market leaders Google and Facebook.

Google once again reported higher sales and profits. And that is a good thing. But, once again, the price of Google’s primary product declined. Revenues increased because volume gains exceeded the price decline, which indicates that the market for internet ads keeps growing. But this makes 15 straight quarters of price declines for Google. Due to this long series of small declines, the average price of Google’s ads (cost per click) has declined 70%* since Q3 2011!

Google once again reported higher sales and profits. And that is a good thing. But, once again, the price of Google’s primary product declined. Revenues increased because volume gains exceeded the price decline, which indicates that the market for internet ads keeps growing. But this makes 15 straight quarters of price declines for Google. Due to this long series of small declines, the average price of Google’s ads (cost per click) has declined 70%* since Q3 2011!

While this is a miraculous example of what economists call demand elasticity, one has to wonder how long growth will continue to outpace price degradation. At some point the marginal growth in demand may not equal the marginal decline in pricing. Should that happen, revenues will start going down rather than up.

Part of what drives this price/growth effect has been the creation of programmatic ad buying, which allows Google to place more ads in more specific locations for advertisers via such automated products as AdMob, AdExchange and DoubleClick Bid Manager. But such computerized ad buying relies on ever more content going onto the web, as well as ever more consumption by internet users.

Further, Google’s revenues are almost entirely search-based advertising, and Google dominates this category. But this is largely a PC-related sale. Today 67.5% of Google ad revenue is from PC searches, while only 32.5% is from mobile searches. Due to this revenue skew, and the fact that people do more mobile interaction via apps, messaging apps and social media than browser, search ad growth has fallen considerably. What was a 24% year over year growth rate in Q1 2012 has dropped to more like 15% for the last 8 quarters.

So while the market today is growing, and Google is making more money, it is possible to see that the growth is slowing. And Google’s efforts to create mobile ad sales outside of search has largely failed, as witnessed by the recent death of Google+ as competition for Twitter or Facebook. It is the market shift, to mobile, which creates the greatest threat to Google’s ability to grow; certainly at historical rates.

Simultaneously, Facebook’s announcements showed just how strongly it is continuing to dominate both social media and mobile, and thus generate higher revenues and profits with outstanding growth. The #1 site for social media and messenger apps is Facebook, by quite a large margin. But, Facebook’s 2014 acquisition of What’sApp is now #2. WhatsApp has doubled its monthly active users (MAUs) just since the acquisition, and now reaches 800million. Growth is clearly accelerating, as this is from a standing start in 2011.

Facebook Messenger at #3, just behind WhatsApp. And #5 is Instagram, another Facebook acquisition. Altogether 4 of the top 5 sites, and the ones with greatest growth on mobile, are Facebook. And they total over 3billion MAUs, growing at over 300million new MAUs/month. Thus Facebook has already emerged as the dominant force, with the most users, in the fast-growing, accelerating, mobile and app sectors. (Just as Google did in internet search a decade ago, beating out companies like Yahoo, Ask Jeeves, etc.)

Google is moving rapidly to monetize this user base. From nothing in early 2012, Facebook’s mobile revenue is now $2.5B/quarter and represents 67% of global revenue (the inverse of Google’s revenues.) Further, Facebook is now taking its own programmatic ad buying tool, Atlas, to advertisers in direct competition with Google. Only Atlas places ads on both social media and internet browser pages – a one-two marketing punch Google has not yet cracked.

Google’s $17.3B Q1 2015 revenue is 30 times the revenue of Facebook. There is no doubt Google is growing, and generating enormous profits. But, for long-term investors, growth is slowing and there is reason to be concerned about the long term growth prospects of Google as the market shifts toward more social and more mobile. Google has failed to build any substantial revenues outside of search, and has had some notable failures recently outside its core markets (Google + and Google Glass.) Just how long Google will continue growing, and just how fast the market will shift is unclear. Technology markets have shown the ability to shift a lot faster than many people expected, leaving some painful losers in their wake (Dell, HP, Sun Microsystems, Yahoo, etc.)

Meanwhile, Facebook is squarely positioned as the leader, without much competition, in the next wave of market growth. Facebook is monetizing all things social and mobile at a rapid clip, and wisely using acquisitions to increase its strength. As these markets continue on their well established trends it is hard to be anything other than significantly optimistic for Facebook long-term.

* 1x .93 x .88 x .84 x .85 x .94 x .96 x .94 x .93 x .89 x .91 x .94 x .98 x .97 x .95 x .93 = .295

by Adam Hartung | Apr 25, 2015 | Defend & Extend, Food and Drink, In the Rapids, In the Swamp, Innovation, Leadership, Transparency

If you don’t drink gin you may not know the brand Tanqueray, a product owned by Diageo. But Tanqueray has been around for almost 190 years, going back to the days when London Dry Gin was first created. Today Tanqueray is one of the most dominant gin brands in the world, and the leading brand in the USA.

But gin is not a growth category. And Tanqueray, despite its great product heritage and strong brand position, has almost no growth prospects.

But gin is not a growth category. And Tanqueray, despite its great product heritage and strong brand position, has almost no growth prospects.

Any product that doesn’t grow sales cannot generate profits to spend on brand maintenance. Firstly, if due to nothing more than inflation, costs always go up over time. It takes rising sales to offset higher costs. Additionally, small competitors can niche the market with new products, cutting into leader sales. And competitors will undercut the leader’s price to steal volume/share in a stagnant market, causing margin erosion.

Category growth stalls are usually linked to substitute products stealing share in a larger definition of the marketplace. For example sales of laptop/desktop PCs stalled because people are now substituting tablets and smartphones. The personal technology market is growing, but it is in the newer product category stealing sales from the older product category.

This is true for gin sales, because older drinkers – who dominate today’s gin market – are drinking less spirits, and literally dying from old age. In the overall spirits market, younger liquor drinkers have preferred vodkas and flavored vodkas which are “smoother,” sweeter, and perceived as “lighter.”

So, what is a brand manager to do? Simply let trends obsolete their product line? Milk their category and give up money for investing somewhere else?

That may sound fine at a corporate level, where category portfolios can be managed by corporate vice presidents. But if you’re a brand manager and you want to become a future V.P., managing declining product sales will not get you into that promotion. And defending market share with price cuts, rebates and deals will cut into margin, ruin the brand position and likely kill your marketing career.

Keith Scott is the Senior Brand Manager for Tanqueray, and his team has chosen to regain product growth by using sustaining innovations in a smart way to attract new customers into the gin category. They are looking beyond the currently dwindling historical customer base of London Dry Gin drinkers, and working to attract new customers which will generate category growth and incremental Tanqueray sales. He’s looking to build the brand, and the category, rather than get into a price war.

Building on demographic trends, Tanqueray’s brand management is targeting spirit drinkers from 28-38. Three new Tanqueray brand extensions are being positioned for greatest appeal to increasingly adult tastes, while offering sophistication and linkage to one of the longest and strongest spirits brands.

#1 – Tanqueray Rangpur is a highly citrus-flavored gin taking a direct assault on flavored vodkas. Although still very much a gin, with its specific herb-based taste, Rangpur adds a hefty, and uniquely flavored, dose of lime. This makes for a fast, easy to prepare gin and tonic or lime-based gimlet – 2 classic cocktails that have their roots in England but have been popular in the US since before prohibition. And, in defense of the brand, Rangpur is priced about 10-20% higher than London Dry.

#1 – Tanqueray Rangpur is a highly citrus-flavored gin taking a direct assault on flavored vodkas. Although still very much a gin, with its specific herb-based taste, Rangpur adds a hefty, and uniquely flavored, dose of lime. This makes for a fast, easy to prepare gin and tonic or lime-based gimlet – 2 classic cocktails that have their roots in England but have been popular in the US since before prohibition. And, in defense of the brand, Rangpur is priced about 10-20% higher than London Dry.

#2 – Tanqueray Old Tom and Tanqueray Milacca appeal to the demographic that loves specialty, crafted products. The “craft” product movement has grown dramatically, and nowhere more powerfully than amongst 28-42 year old beer drinkers. Old Tom and Milacca leverage this trend. Both are “retro” products, harkening to gins over 100 years ago. They are made in small batches and have limited availability. They are targeted at the consumer that wants something new, unique, unusual and yet tied to old world notions of hand-made production and high quality. These craft products are priced 25-35% higher than traditional London Dry.

#2 – Tanqueray Old Tom and Tanqueray Milacca appeal to the demographic that loves specialty, crafted products. The “craft” product movement has grown dramatically, and nowhere more powerfully than amongst 28-42 year old beer drinkers. Old Tom and Milacca leverage this trend. Both are “retro” products, harkening to gins over 100 years ago. They are made in small batches and have limited availability. They are targeted at the consumer that wants something new, unique, unusual and yet tied to old world notions of hand-made production and high quality. These craft products are priced 25-35% higher than traditional London Dry.

#3 – Tanqueray No. 10 is a “super-premium” product pointed at the customer who wants to project maximum sophistication and wealth. No 10 uses a special manufacturing process creating a uniquely smooth and slightly citrus flavor. But this process loses 40% of the product to “tailings” compared to the industry standard 10% loss. No. 10 is the high-end defense of the Tanqueray brand (a “top shelf” product as its known in the industry) priced 75-90% higher than London Dry.

No. 10 is being promoted with “invitation only” events being held in major U.S. cities such as New York, Chicago and Atlanta. No. 10 “trunk events” bring in some of the hottest, newest designers to showcase the latest in apparel trends, accompanied by hot, new musical talent. No. 10 is associated with the sophistication of super-premium brands – individualized and rare products – in a members-only environment. Targeted at the primary demographic of 28-38, No. 10 events are designed to lure these consumers to this product they otherwise might overlook .

Rather than addressing their gin category growth stall with price cuts and other sales incentives, which would lead to brand erosion, price erosion, and margin erosion, the Tanqueray brand team is leveraging trends to bring new consumers to their category and generate profitable growth. These innovative brand extensions actually build brand value while leveraging identifiable market trends. Notice that all these sustaining innovations are actually priced higher than the highest volume London Dry core product, thus augmenting price – and hopefully margin.

Too often leaders see their market stagnate and use that as an excuse lower expectations and accept sales decline. They don’t look beyond their core market for new customers and sources of growth. They react to competition with the blunt axe of pricing actions, seeking to maintain volume as margins erode and competition intensifies. This accelerates product genericization, and kills brand value.

The Tanqueray brand team demonstrates how critical sustaining innovation can be for maintaining growth at all levels of an organization. Even the level of a single product or brand. They are using sustaining innovations to lure in new customers and grow the brand umbrella, while growing the category and achieving desired price realization. This is a lesson many brands, and companies, should emulate.

by Adam Hartung | Apr 9, 2015 | Current Affairs, Defend & Extend, Innovation, Leadership

This week a self-driving car built by Delphi of England completed a 9 day trip from San Francisco to New York City. The car traveled 3,400 miles, and was fully automated for 99% of the trip.

Attention has again focused on self-driving cars. There are a handful of players entering the market today, including Apple. But the most famous company by far is Google, which has put over 700,000 autonomous miles on its vehicles since pioneering the concept after winning a DARPA challenge to build a functioning prototype in 2005. In fact, we’re so used to hearing about the Google self-driving car that many of have stopped asking “Why Google? They aren’t in the auto business.”

Of course the idea of a self-driving auto is as old as the Jetson’s (and if you don’t know who the Jetson’s are you are, that was a long time ago.) And nobody should be surprised to hear that prototypes have been on the drawing board for 5 decades. But I bet you didn’t know that DuPont was once seriously engaged in such development.

In 1986 DuPont was America’s largest and most noteworthy chemical company. The company was a pioneer in petrochemicals, and was considered the company that brought the world plastic – at a time when plastic was considered a great, new invention. A leader in films of all sorts, DuPont leadership saw the opportunity for electronics to replace film in applications such as printing (where films were used in high volume for platemaking and proofing) and healthcare (where xRays and MRIs were a large film users.) They conceived of a future time when computers and monitors – digitial products – could replace analog film, and they chose to create a new business unit called Electronic Imaging to pioneer developing these applications.

As the team started they expanded the definition of Electronic Imaging to include all sorts of applications for digital imaging – and using all kinds of technologies. The breadth of analysis, and product development, included non-destructive parts testing, infrared uses such as heads-up displays and inventory identification, and radar applications. Which led the team to using a radar for automating an automobile.

In 1987 DuPont invested in a small company out of San Diego that accomplished something never done before. Using a phased-array radar hooked up to the brakes of a van, they were able to have the car recognize objects in front of the van, calculate in real time the distance between the van and these forward objects, calculate the relative speed of both objects (whether one or both were stationary or moving) and then apply braking in order to maintain a safe distance. If the forward object stopped, then the van would come to a complete stop.

This was all done with discreet componentry, and the team realized future success required developing more specific electronics, including specialized integrated chips that could operate faster and be more error-free. So they drove the prototype from San Diego to Wilmington, DE with a person behind the wheel, but relying as much as possible on the automated system to do all braking. The team collected data on location, speed, weather, traffic conditions, and many other items during the journey and prepared to take the project forward, planning to eventually build a module which could be installed in vehicles as small as cars or as large as 18-wheelers, with enough intelligence to adjust for different vehicle designs and applications (in order to calibrate for different braking distances.)

Net/net they had a working prototype. The product was expected to reduce the number of accidents by assisting drivers with braking. Multi-car pile-ups would become a thing of the past. And this device could potentially allow for better traffic flow because automated braking would reduce – maybe eliminate! – rear-end collisions. This wasn’t a self-driving car, but it was self-braking car, which would be a first step toward the sort of Jetson’s-esque vision the young team imagined.

What happened?

It didn’t take long for the older, “wiser” leadership to shut down the project. Even though several executives participated in a controlled demonstration of the prototype in an enclosed DuPont parking lot, the conclusion was that this project demonstrated just how off-track the new Electronic Imaging Department had become, and that it was clear folks needed to be reigned in and budgets cut:

- This clearly had nothing to do with film or replacing film. DuPont was a chemical company, and to the extent it had any interest in electronics it was where they were applied to potentially cannibalize film sales. Products which were not closely aligned with historical products were simply not to be pursued.

- DuPont had no history in radar, analogue electronics or development of integrated circuits. Yes, DuPont had an Electronics Department, but they sold film for solder masking and other applications of semiconductor and electronics manufacturing. DuPont was a chemical company, not a computer company or electronics company and this division was not going to change this situation.

- This product was seen as carrying too much liability risk. What if it failed? What if the car ran over a child? The auto industry was seen as litigious, and DuPont had no interest in a product that could have the kind of liability this one would generate. Yes, there was an Auto Department, but it sold films for safety glass, plastic sheets used for molding inside panels, and surface coatings which could be painted on the inside and/or outside of the vehicle. But those did not have the kind of failure possibility of this active radar device. [“By the way” the vice-Chairman asked “could that radar fry someone’s innards at a crosswalk?”]

- The market is too limited. Who would really want an automatic braking system? Given what it might cost, only the most expensive cars could install it, and only the wealthiest customers could afford it. This product was destined for niche use, at best, and would never have widespread installation.

Poof, away went the automatic automobile braking project. Once this dagger had been thrown, within just a few months everything that wasn’t printing or medical – in fact anything that wasn’t tied to printing films, xRays and MRI – was gone. Within 2 years leadership decided that for some variant of the 4 issues above the entire Electronic Imaging division was a bad idea. DuPont would be better served if it stuck to its core business, and if it spent money defending and extending film sales rather than trying to cannibalize them.

DuPont liked competing in the oceans where it had long competed. Venturing beyond those oceans was simply too risky. Today, 25 years later, DuPont is about 1/3 the size it was when its leaders launched the ill-fated Electronic Imaging division.

Google obviously has a different way of looking at the opportunity for automating automobile operation. Since winning the DARPA competition Google has spent a goodly sum building and testing ways to automate driving. And it has even gone so far as lobbying to make self-driving cars legal, which they now are in 4 states. Pessimists remain, but every quarter more people are thinking that self-driving cars will be here sooner than we might have imagined. This week’s cross-country achievement fuels speculation that the reality could be just around the corner.

Google seems happy to compete in new oceans. It dominates search, where its share is attacked every day by the likes of Yahoo and Microsoft. But simultaneously Google has invested far outside its core market, including software for PCs (Chrome) and mobile devices (Android), hardware (Nexus phones), media (Blogger, YouTube), payments (Wallet) and even self-driving cars. To what extent these, and dozens of other non-core products/services, will pay off for investors is yet to be determined. But at least Google’s leadership is able to overcome the desire to restrict the company’s options and look for future markets.

Which kind of organization is yours? Do you find reasons to kill new projects, or are you willing to experiment at creating new markets which might create dramatic growth?

by Adam Hartung | Apr 2, 2015 | Current Affairs, Defend & Extend, In the Rapids, Innovation, Leadership, Web/Tech

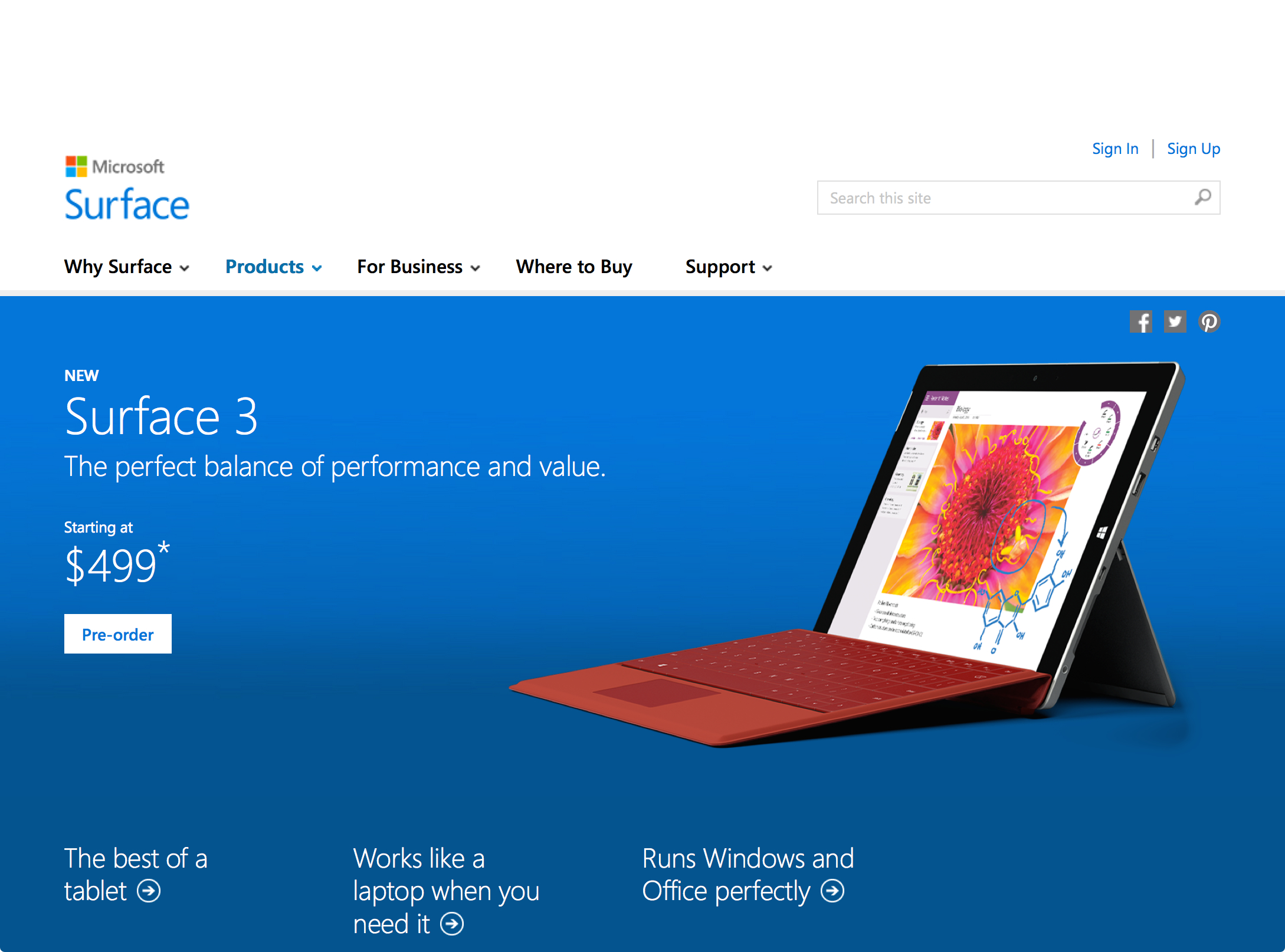

Microsoft launched its new Surface 3 this week, and it has been gathering rave reviews. Many analysts think its combination of a full Windows OS (not the slimmed down RT version on previous Surface tablets,) thinness and ability to operate as both a tablet and a PC make it a great product for business. And at $499 it is cheaper than any tablet from market pioneer Apple.

Meanwhile Apple keeps promoting the new Apple Watch, which was debuted last month and is scheduled to release April 24. It is a new product in a market segment (wearables) which has had very little development, and very few competitive products. While there is a lot of hoopla, there are also a lot of skeptics who wonder why anyone would buy an Apple Watch. And these skeptics worry Apple’s Watch risks diverting the company’s focus away from profitable tablet sales as competitors hone their offerings.

Looking at these launches gives a lot of insight into how these two companies think, and the way they compete. One clearly lives in red oceans, the other focuses on blue oceans.

Blue Ocean Strategy (Chan Kim and Renee Mauborgne) was released in 2005 by Harvard Business School Press. It became a huge best-seller, and remains popular today. The thesis is that most companies focus on competing against rivals for share in existing markets. Competition intensifies, features blossom, prices decline and the marketplace loses margin as competitors rush to sell cheaper products in order to maintain share. In this competitively intense ocean segments are niched and products are commoditized turning the water red (either the red ink of losses, or the blood of flailing competitors, choose your preferred metaphor.)

On the other hand, companies can choose to avoid this margin-eroding competitive intensity by choosing to put less energy into red oceans, and instead pioneer blue oceans – markets largely untapped by competition. By focusing beyond existing market demands companies can identify unmet needs (needs beyond lower price or incremental product improvements) and then innovate new solutions which create far more profitable uncontested markets – blue oceans.

Obviously, the authors are not big fans of operational excellence and a focus on execution, but instead see more value for shareholders and employees from innovation and new market development.

If we look at the new Surface 3 we see what looks to be a very good product. Certainly a product which is competitive. The Surface 3 has great specifications, a lot of adaptability and meets many user needs – and it is available at what appears to be a favorable price when compared with iPads.

But …. it is being launched into a very, very red ocean.

The market for inexpensive personal computing devices is filled with a lot of products. Don’t forget that before we had tablets we had netbooks. Low cost, scaled back yet very useful Microsoft-based PCs which can be purchased at prices that are less than half the cost of a Surface 3. And although Surface 3 can be used as a tablet, the number of apps is a fraction of competitive iOS and Android products – and the developer community has not yet embraced creating new apps for Windows tablets. So Surface 3 is more than a netbook, but also a lot more expensive.

Additionally, the market has Chromebooks which are low-cost devices using Google Chrome which give most of the capability users need, plus extensive internet/cloud application access at prices less than a third that of Surface 3. In fact, amidst the Microsoft and Apple announcements Google announced it was releasing a new ChromeBit stick which could be plugged into any monitor, then work with any Bluetooth enabled keyboard and mouse, to turn your TV into a computer. And this is expected to sell for as little as $100 – or maybe less!

This is classic red ocean behavior. The market is being fragmented into things that work as PCs, things that work as tablets (meaning run apps instead of applications,) things that deliver the functionality of one or the other but without traditional hardware, and things that are a hybrid of both. And prices are plummeting. Intense competition, multiple suppliers and eroding margins.

Ouch. The “winners” in this market will undoubtedly generate sales. But, will they make decent profits? At low initial prices, and software that is either deeply discounted or free (Google’s cloud-based MSOffice competitive products are free, and buyers of Surface 3 receive 1 year free of MS365 Office in the cloud, as well as free upgrade to Windows 10,) it is far from obvious how profitable these products will be.

Amidst this intense competition for sales of tablets and other low-end devices, Apple seems to be completely focused on selling a product that not many people seem to want. At least not yet. In one of the quirkier product launch messages that’s been used, Apple is saying it developed the Apple Watch because its other innovative product line – the iPhone – “is ruining your life.”

Apple is saying that its leaders have looked into the future, and they think today’s technology is going to move onto our bodies. Become far more personal. More interactive, more knowledgeable about its owner, and more capable of being helpful without being an interruption. They see a future where we don’t need a keyboard, mouse or other artificial interface to connect to technology that improves our productivity.

Right. That is easy to discount. Apple’s leaders are betting on a vision. Not a market. They could be right. Or they could be wrong. They want us to trust them. Meanwhile, if tablet sales falter….. if Surface 3 and ChromeBit do steal the “low end” – or some other segment – of the tablet market…..if smartphone sales slip….. if other “forward looking” products like ApplePay and iBeacon don’t catch on……

This week we see two companies fundamentally different methods of competing. Microsoft thinks in relation to its historical core markets, and engaging in bloody battles to win share. Microsoft looks at existing markets – in this case tablets – and thinks about what it has to do to win sales/share at all cost. Microsoft is a red ocean competitor.

Apple, on the other hand, pioneers new markets. Nobody needed an iPod… folks were happy enough with Sony Walkman and Discman. Everybody loved their Razr phones and Blackberries… until Apple gave them an iPhone and an armload of apps. Netbook sales were skyrocketing until iPads came along providing greater mobility and a different way of getting the job done.

Apple’s success has not been built upon defending historical markets. Rather, it has pioneered new markets that made existing markets obsolete. Its success has never looked obvious. Contrarily, many of its products looked quite underwhelming when launched. Questionable. And it has cannibalized its own products as it brought out new ones (remember when iPods were so new there was the iPod mini, iPod nano and iPod Touch? After 5 years of declining iPod sale Apple has stopped reporting them.) Apple avoids red oceans, and prefers to develop blue ones.

Which company will be more successful in 2020? Time will tell. But, since 2000 Apple has gone from nearly bankrupt to the most valuable publicly traded company in the USA. Since 1/1/2001 Microsoft has gone up 32% in value. Apple has risen 8,000%. While most of us prefer the competition in red oceans, so far Apple has demonstrated what Blue Ocean Strategy authors claimed, that it is more profitable to find blue oceans. And they’ve shown us they can do it.