by Adam Hartung | Mar 13, 2018 | Defend & Extend, Growth Stall, Innovation, Investing, Software

In February, Berkshire Hathaway revealed it had dumped its IBM position. Good riddance to a stock that has gone down for 5 years while the S&P went up! What did Buffett do with the money? He loaded up on Apple – making that high-flyer Berkshire’s #1 holding. So, isn’t the smart thing now to buy Apple?

First, don’t confuse your investing goals with Berkshire Hathaway’s. It may seem that everyone has the same objective, to buy stocks that go up. But Berkshire is a very special case. As I pointed out in 2014, we mere mortals can’t invest like Buffett, and shouldn’t try. Berkshire Hathaway has the opportunity to make investments in special situations with tremendous return potential that we don’t have. Berkshire’s investment strategy is to invest where it can create cash to prepare for special situations, or to park money where it can make a decent return, and hopefully generate cash while it waits.

Apple is the #1 most cash-rich company on the planet, and with the new tax laws it can repatriate that cash. This is an opportunity for a “special dividend” to investors, and that is the kind of thing that Buffett loves. He isn’t a venture capitalist looking for a 10x price appreciation. He wants a decent 5% rate of return, and hopefully dividends, so he can grow cash for his special situation opportunities. Apple, the most valuable company on any exchange, is exactly the kind of company where he can place a few billion dollars without driving up the price and let it sit making a solid 5-6%, collect dividends and maybe get a few kickers from things like the cash repatriation.

Second, let’s not forget that Buffett’s IBM buying spree lost money. If he was a great tech investor, he never would have bought IBM. He bought it for the same reason he’s buying Apple, only he was wrong about what was going to happen to IBM as it continued to lose relevancy.

I pointed out in May, 2016 that Apple was showing us all a lot of sustaining innovations, with new rev levels of existing products, but almost no new disruptive innovations. The company that once gave us iPods, iTunes, iPhones and iPads was increasingly relying on the next version of everything to drive sales. Lots of incremental improvement. But little discussion about any breakthrough products, like iBeacon, ApplePay or even the Apple Watch. In a real way, Apple was looking a lot more like the old Microsoft with its Windows and Office fascination than the old Apple.

By October, 2016 Apple hit a Growth Stall. While this may have seemed like “no big deal,” recall that only 7% of the time do companies maintain a 2% growth rate after stalling. Is Apple going to be in that 7%? With the launch of the less-than-overwhelming iPhone X, and the actual drop in iPhone sales in Q4, 2017 it looks increasingly like Apple is on the same road as all other stalled companies.

In the short term Apple has said it is milking its installed base. By constantly bringing out new apps it has raised iTunes sales to over $30B/quarter. And it has a dedicated cadre of developers making over $25B/year creating new apps. So Apple is doing its best to get as much revenue out of that installed base of iPhones as it can, even if device sales slow (or decline.) For Buffett, this is no big deal. After all, he’s parking cash and hoping to get dividends. Milking the base is a cash generation strategy he would love – like a railroad, or Coca-Cola.

But if you’re interested in maintaining high returns in your portfolio, be aware of what’s happening. Apple is changing. It’s not going to falter and fail any time soon. But don’t be lulled by Berkshire’s big purchases into thinking Apple in 2018 is anything like it was in 2012 – or through 2014. Instead, keep your eyes on game changers like Netflix, Tesla and Amazon.

by Adam Hartung | Feb 27, 2018 | Growth Stall, Innovation, Investing, Software

This February, Warren Buffett admitted he had no faith in IBM. After accumulating a huge position, by 4th quarter of 2017 he sold out almost the entire Berkshire Hathaway position. He lost faith in the IBM CEO Virginia (Ginni) Rometty, who talked big about a turnaround, but it never happened.

Mr. Buffett would have been wise to stopped having “faith” long ago. All the way back in May, 2014 I wrote that IBM was not going to be a turnaround. CEO Rommetty was spending ALL its money on share buybacks, rather than growing its business. The Washington Post made IBM the “poster child” for stupid share buybacks, pointing out that spending over $8B on repurchases had maintained earnings-per-share, and propped up the stock price, but giving IBM the largest debt-to-equity ratio of comparable companies.

IBM was already in a Growth Stall, something about which I’ve written often. Once a company stalls, its odds  of growing at 2%/year fall to a mere 7%. But it was clear then that the CEO was more interested in financial machinations, borrowing money to repurchase shares and prop up the stock, rather than actually investing in growing the company. The once great IBM was out of step with the tech market, and had no programs in place to make it an industry leader in the future.

of growing at 2%/year fall to a mere 7%. But it was clear then that the CEO was more interested in financial machinations, borrowing money to repurchase shares and prop up the stock, rather than actually investing in growing the company. The once great IBM was out of step with the tech market, and had no programs in place to make it an industry leader in the future.

By April, 2017 it was clear IBM was a disaster. By then we had 20 consecutive quarters of declining revenue. Amazing. How Rometty kept her job was completely unclear. Five years of shrinkage, while all investments were in buying the stock of its shrinking enterprise – intended to hide the shrink! CEO Rometty continued promising a turnaround, with vague references to the “wonderful” Watson program. But it was clear, Buffett (and everyone else) needed to get out in 2014. So Berkshire ate its losses, took the money and ran.

Have you learned your lesson? As an investor are you holding onto stocks long after leadership has shown they have no idea how to grow revenues? If so, why? Hope is not a strategy.

As a leader, are you still forecasting hockey stick turnarounds, while continuing to invest in outdated products and businesses? Are you hoping your past will somehow create your future, even though competitors and markets have moved on? Are you leading like Rometty, hoping you can hide your failures with financial machinations and Powerpoint presentations about how things will turn your way in the future – even though those assumptions are made out of hole cloth?

It’s time to get real about your investments, and your business. When revenues are challenged, something bad is happening. It’s time to do something. Fast. Before a bad quarter becomes 20, and everyone is giving up.

by Paul F | Feb 20, 2018 | Entrepreneurship, Innovation, Investing, Science, Trends

Tesla has stuck a deal to put solar panels and Powerwall batteries on 50,000 homes in Southern Australia. The homeowners will not pay for the equipment. They won’t even own it. Instead the equipment will be owned by the utility company, and the 50,000 homes will become a “virtual” power plant – operating as independent pieces of a giant grid. For everyone in the system this will lower power costs by over 30%, and improve the performance where outages are a big problem.

This is really, really smart. The old way of thinking about power generation was a big plant, usually coal, gas or oil powered. Or, a giant group of solar panels in a desert, or a giant group of windmills. Or, a nuclear-powered plant. This centralized generation is then shipped over power lines to homes and businesses.

The problem is that transmission can lose anywhere from 20% to 80% of the power. Thus, the bigger the plant in theory the lower the power cost – but that is only for generation. After factoring in the cost of transmission losses, and the cost of building and maintaining transmission lines, the cost can be quite high. And thus the resulting never-ending increases in electricity prices even as traditional feedstocks go down in cost. Decentralized power generation, in a grid of small production, nearly eliminates transmission losses and uses renewable sources in the most favorable way.

Nobody should be surprised that Tesla is a leader in this program. Back in September, 2016 when Tesla took over (or merged) with Solar City I strongly made the case that this would be a good move. The ability to make solar shingles, solar panels and store large power amounts in whole-building batteries is a game changer for how we make, and consume, electricity. As utility commissions keep realizing the problems with building ever-larger centralized plants, decentralized systems that truly utilize grid management are simply a smarter, cheaper, better way to power our homes and offices.

Most people think of Solar City as “just another home solar system.” That would be wrong. Solar City has the ability to power entire towns and regions with their system of production, storage and grid management. And that is great for Tesla shareholders. Tesla has shown it is a game changer with products like the Model 3, and the combination with Solar City actually creates a utility industry game changer, as well as auto industry game changer, that could put a hurt on companies like Exxon. Now, like when I recommended buying Tesla in January, 2015, you should be thinking long term about the opportunity for outsized returns a game-changing company like Tesla provides.

by Adam Hartung | Feb 13, 2018 | Entertainment, Innovation, Investing, Television, Web/Tech

On January 23 Netflix’ value rose to $100B. The stock is now trading north of $250/share. A year ago it was $139/share. An 80% increase in just 12 months. And long-term investors have done very well. Five years ago (January, 2013) the stock was trading at $24/share – so the valuation has increased 10-fold in 5 years! A decade ago it was trading for $3/share – so if you got in early (NFLX went public in June, 2002) you are up 83X your initial investment (meaning $1,000 would be worth $83,000.)

Back in 2004 I wrote that Blockbuster was dead meat – because by going after streaming Netflix would make Blockbuster obsolete. Netflix was using external data to project its future, and thus its strategy was not to defend & extend its DVD rental business but to spend strongly to grow the replacement. In 2010 I wrote that Netflix had projected the complete demise of DVDs by 2013, and was thus investing all its resources into streaming in order to be the market leader. At the time NFLX was $15.68. Over the next year it took off, tripling in value to $42.16. By cannibalizing DVDs it’s strategy was to leave its competition in a dying marketplace.

But, investors weren’t as sure of the Netflix strategy as I was. They feared cannibalizing DVDs would cut out the “core” of Netflix and kill the company. By October, 2011 the stock had tumbled to $12 (a drop of over 70%.) But, with the stock at new lows after a year of declines I optimistically wrote “The Case for Buying Netflix. Really.” I told readers the stock analysts were wrong, and the Netflix strategy was spot-on.

Netflix went nowhere for the next year, trading between $9 and $12. But then in December, 2012 investors started seeing the results of Netflix strategy, with fast growing streaming subscriber rates. By January, 2014 the stock was trading north of $52, so those who bought when my article published made a 400% return in just over 2 years! By March, 2015 NFLX was up another 23%, to $62 when I told readers “Netflix Valuation Was Not a House of Cards.” The Netflix strategy to dominate streaming by offering its own content may have shocked a lot of people, due to the investment size, but it was the strategy that would allow Netflix to grow subscribers globally. That has driven the last jump, to $250 in just under 3 years – another 400%+ return!

Strategy matters- to company performance, and thus long-term investor returns. Netflix has been a volatile stock, and it has had plenty of naysayers. These were people looking only short-term, and fearful of strategic pivots that have proven highly valuable. If you want your company, and your investment portfolio, to succeed it is imperative you understand external trends and use them to develop the right strategy. And heed my forecasts.

by Adam Hartung | Feb 6, 2018 | Innovation, Mobile, Software, Web/Tech

InvestorPlace.com declared Snap stock will be a big disappointment in 2018. Bad news for investors, because SNAP was an enormous disappointment in 2017. After going public at $27/share in early March, the stock dropped to $20 by mid-March, then just kept dropping until it bottomed at just under $12 in August. Since then the stock has largely gone sideways at $15.

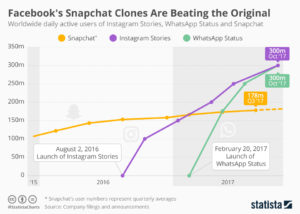

This was not unexpected. As I wrote in April, Snapchat was not without competition and was unlikely to be a long-term winner. Even though Snapchat and its Stories feature grew popular with teenagers 14 to 19, in August, 2016 Facebook launched Instagram Stories as a direct competitor. In just 7 months – just as SNAP went public – Instagram Stories had more users than Snapchat. It was clear then if you wanted to make money on the photo and video sharing trends, investors were better off to own Facebook stock and avoid the newly available SNAP shares (stock, not pix!)

Now the situation is far worse. Facebook launched WhatsApp Status as another competitive product in February, 2017 and it took less than 3 months for its user base to exceed Snapchat. As the chart below shows, by October, 2017 Stories and Status each had 300 million users, while Snapchat was mired at 180 million users. With only 30% the users of Facebook, Snapchat has little chance to succeed against the social media powerhouse.

Statista

Facebook is now a very large company. But, it has shown it is adaptable. Rather than sticking to its original market, Facebook went mobile and has launched new products as fast as competitors tried to carve out niches. The question is, are you constantly scanning the horizon for new products and adapting – fast – to keep your customers and grow? Or are you stuck trying to defending your old business while upstarts carve up your market?”

by Adam Hartung | Jan 5, 2018 | Defend & Extend, Innovation, Leadership

Fast Company just published 3 common behaviors that kill innovation. Congratulations! The editors reinforce that most management behavior and best practices are lethal to innovation.

All the way back in November, 2009, my Forbes column explained that organizations approach innovation entirely wrong- trying far too hard to build on historical company strengths, which leads to weak extensions that fail to generate sustainable growth. In November, 2011, my Forbes column identified the “killer comments” that leaders used to stop innovation. Fast Company’s list is remarkably similar to that 2011 column, though it is a shorter list. In June, 2015, my Forbes column described how HR best practices are designed to limit diversity in thinking- and always lead to killing innovation projects. Factually, as I wrote in February, 2011, almost nobody would hire the next Steve Jobs if he applied for a job!

Quite simply, we have built organizations that rigidly adhere to continuing past processes, and are hard wired to resist innovation. This phenomenon has been around for a long time, even though Fast Company just discovered it, and I’ve been writing about it for 9 years. Give my past columns a read and you’ll be forewarned of the risks to brainstorming, or throwing together innovation teams, without a system of new thinking.

Fortunately, smart leaders today see that by focusing on external data and cleverly using outside thinkers, innovation can create a high-growth future. The approach I’ve been teaching organizations for years. Only by overcoming outdated, historical management practices can a modern organization thrive. You can do it- if you smartly use trends and new approaches.

by Adam Hartung | Dec 22, 2017 | Advertising, Film, Innovation, Marketing, Trends

Here in late 2017, the biggest trends are: the 24 hour news cycle, animosity in broadcast and online media, fatigue from constant connection and interaction, international threats and our political climate. The holiday season is in the background struggling for attention.

How are people tuning out of this cacophony to get in the mood for the holidays?

The answer: Christmas movies! And which channel has 75% share of the new movies in 2017? If you have watched any TV since October, you’d know that it’s The Hallmark Channel. THC has produced over 20 original movies for the 2017 Christmas season and has seen viewership grow by 6.7% per year since 2013. THC is on track to surpass the 2016 season in viewership and its brand image is solidly wholesome.

Starting in October, THC runs seasonal programming with its successful “The Good Witch” series (no vampires!) and continues with “Countdown to Christmas” featuring original Hallmark-produced content.

Hallmark spent decades preparing to capture the benefits of these trends. It had become a source of family oriented, holiday-themed programming especially popular in recent years. Once only an ink and paper company, Hallmark expanded strategically in the 1970s with ornaments and cultural greeting cards and again in 1984 with its acquisition of Crayola drawing products. The company moved into direct retail in 1986 and ecommerce in the mid-1990s. Hallmark eCards was launched in 2005.

Hallmark capitalized on branded media content originally to support the core business and it now generates profits as a standalone business. In 2001, the Hallmark Channel was launched. The Hallmark Movie Channel was developed in 2004 which became Hallmark Movies and Mysteries in 2014. This year, the Hallmark Drama channel was launched further leveraging the brand.

Many companies sponsored radio shows in the 1920s through the war years. Serials featuring one company’s products appeared in 1928 on radio. In 1952, Proctor and Gamble sponsored the first TV soap opera featuring one company (“The Guiding Light”). But The Hallmark Hall of Fame was there first on Christmas Eve in 1951 sponsoring a made-for-TV opera, “Amahl and the Night Visitors.”

Written by Gian Carlo Menotti in less than two months and timed for a one hour TV slot, “Amahl” has become, probably, the most performed opera in history.

Hallmark wasn’t the first mover in sponsored media content, but it had learned to experiment with new media. The company was positioned to take advantage of the trend toward family friendly broadcast content and this year was ready to give the nation a place to rest and escape from the chaos. A bit like the story of Amahl and Christmas itself.

Once just a card company, Hallmark followed market trends to expand its business and become a leader in content marketing which is now one of the hottest areas in all marketing. And both the new video content and large library were ready for the current trend- streaming video!

by Adam Hartung | Aug 29, 2017 | Innovation, Leadership, Marketing, Mobile, Web/Tech

For most consumers an Android-based phone from one of the various manufacturers, most likely bought through a wireless provider if in the USA, does pretty much everything the consumer wants. Developers of most consumer apps, such as games, navigation, shopping, etc. make sure their products work on all phones. For that reason, the bulk of consumers are happy to buy their phone for $200 or less, and most don’t even care what version of Android it runs. As a stand-alone tool an Android phone does pretty much everything they want, and they can afford to replace it every year or two.

But the business community has different requirements.

And because iOS has superior features, Apple continues to dominate the enterprise environment:

- All iPhones are encrypted, giving a security advantage to iOS. Due to platform fragmentation (a fancy way of saying Android is not the same on all platforms, and some Android phones run pretty old versions) most Android phones are not encrypted. That leads to more malware on Android phones. And, Android updates are pushed out by the carrier, compared to Apple controlling all iOS updates regardless of carrier. When you’re building an enterprise app, these security issues are very important.

- iOS is seamless with Macs, and can be pretty well linked to Windows if necessary for an apps’ purpose. Android plays well with Chromebooks, but is far less easy to connect with established PC platforms. So if you want the app to integrate across platforms, such as in a corporation, it’s easier with iOS.

- iPhones come exactly the same, regardless of the carrier. Not true for Android phones. Almost all Androids come with various “junkware.” These apps can conflict with an enterprise app. For enterprise app developers to make things work on an Android phone they really need to “wipe” the phone of all apps, make sure each phone has the same version of Android and then make sure users don’t add anything which can cause a user conflict with the enterprise app. Much easier to just ask people to use an iPhone.

- iOS backs up to iCloud or via iTunes. Straightforward and simple. And if you need to restore, or change devices, it is a simple process. But in the Android world companies like Verizon and Samsung integrate their own back-up tools, which are inconsistent and can be quite hard for a developer to integrate into the app. Enterprise apps need back-ups, and making that difficult can be a huge problem for enterprise developers who have to support thousands of end users. And the fact that Android restores are not consistent, or reliable, makes this a tough issue.

- Search is built-in with iOS. Simple. But Android does not have a clean and simple search feature. And the old cross-platform inconsistencies plague the various search functions offered in the Android world. When using an enterprise app, which may well have considerable complexity, accessing an easy search function is a great benefit.

Most of these issues are no big deal for the typical smartphone consumer who just uses their phone independently of their work. But when someone wants to create an enterprise app, these become really important issues. To make sure the app works well, meeting corporate and end user needs, it is much easier, and better, to build it on iOS.

This allows Apple to price well above the market average

Today Apple charges around $800 for an iPhone 7, and expectations are for the iPhone 8 to be priced around $1,000. Because Apple’s pricing is some 4-5x higher, it allows Apple’s iOS revenue to actually exceed the revenue of all the Android phones sold! And because Android phone manufacturers compete on price, rather than features and capabilities, Apple makes almost ALL the profit in the smartphone hardware business. Even as iPhone unit volume has struggled of late, and some analysts have challenged Apple’s leadership given its under 20% market share, profits keep rolling in, and up, for the iPhone.

By taking the lead with enterprise app developers Apple assures itself of an ongoing market. Three years ago I pointed out the importance of winning the developer war when IBM made its huge commitment to build enterprise apps on iOS. This decision spelled doom for Windows phone and Blackberry — which today have inconsequential market shares of .1% and .0% (yes, Blackberry’s share is truly a rounding error in the marketplace.) Blackberry has become irrelevant. And having missed the mobile market Microsoft is now trying to slow the decline of PC sales by promoting hybrid devices like the Surface tablet as a PC replacement. But, lacking developers for enterprise mobile apps on Microsoft O/S it will be very tough for Microsoft to keep the mobile trend from eventually devastating Windows-based device sales.

As the world goes mobile, devices become smaller and more capable. The need for two devices, such as a phone and a PC, is becoming smaller with each day. Those who predicted “nobody can do real work on a smartphone” are finding out that an incredible amount of work can be done on a wirelessly connected smartphone. As the number of enterprise apps grows, and Apple remains the preferred developer platform, it bodes well for future sales of devices and software for Apple — and creates a dark cloud over those with minimal share like Blackberry and Microsoft.

by Adam Hartung | Jul 31, 2017 | In the Flats, Innovation, Investing, Leadership, Marketing

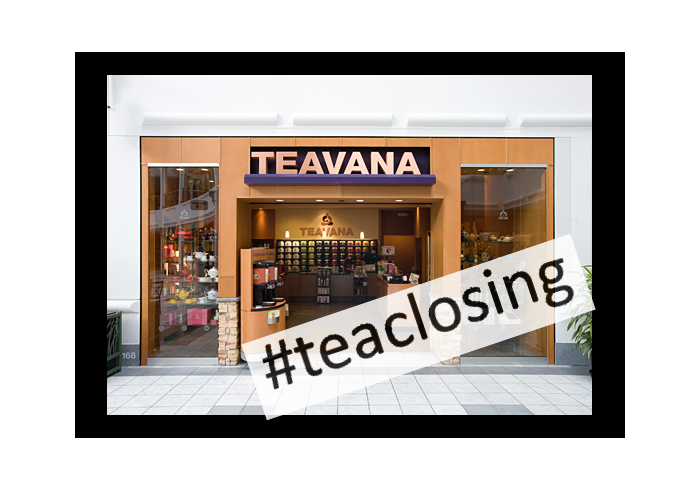

Amid all the political news last week it was easy to miss announcements in the business world. Especially one that was relatively small, like Starbucks announcement on Thursday July 27, 2017 that it was closing all 379 of its Teavana stores. While these will be missed by some product fanatics, the decision is almost immaterial given that these units represent only about 3% of Starbucks US stores, and about 1.5% of the 25,000 Starbucks globally.

Yet, closing Teavana is a telltale sign of concern for Starbucks investors.

Starbucks founding CEO Howard Schultz returned to the top job in January, 2008, promising to get out of distractions such as music production, movie production, internet sales, grocery products, liquor products and even in-store food sales in order to return the company to its “core” coffee business. Since then Starbucks valuation has risen some 5.5-6 fold, from $9.45/share to the recent range of $54 to $60 per share. A much better return than the roughly doubling of the Dow Jones Industrial Average over the same timeframe.

Yet, one should take time to evaluate what this closing means for the long-term future of Starbucks. This is the second time Starbucks made an acquisition only to shut it down. In 2015 Starbucks closed all 23 La Boulange bakery cafes, with little fanfare. Now, after paying $620M to buy Teavana in 2012, they are closing all those stores. While leadership blamed its decision on declining mall visits (undoubtedly a fact) for the closures, Teavana is not missing goals due to the Amazon Effect. There are multiple options for how to market Teavana’s fresh and packaged products far beyond mall store locations. Choosing to close all stores indicates leadership has minimal interest in the brand.

Starbucks’ focus leaves little opportunity for new growth

It increasingly appears that today’s Starbucks literally isn’t interested, or able, to do anything other than build, and operate, more Starbucks stores. And Starbucks is clearly doubling down on its plans to be Starbucks store-centric. The company opened 575 new units in the last year, and announced plans to open more stores creating 68,000 additional US jobs in the next 5 years. Further, Starbucks is paying $1.3B to buy the half of its China business previously owned by a partner. Clearly, leadership continues to tighten company focus on the “core” coffee store business for the future.

This sounds great short-term, given how well things have gone the last 8 years. But there are concerns. Sales are up 4% last quarter, but that is wholly based upon higher prices. Customer counts are flat, indicating that stores are not attracting new customers from competitors. Sales gains are due to average ticket prices increasing 5%, which is marginal and likely refers to higher priced products. Starbucks is now relying completely on new stores to create incremental growth, since bringing in new customers to existing stores is not happening.

Frequently this stagnant store sales metric indicates store saturation. A bad sign. Does the US, or international markets, really need more, new Starbucks stores? It was 2010 when comedian Lewis Black had a successful viral rant (PG version) claiming that when he observed a Starbucks across the street from another Starbucks he knew it was the end of civilization.

What happens when the market doesn’t need new Starbucks stores?

One does have to wonder when the maximum number of Starbucks will be reached. Especially given the ever growing number of competitors in all markets. Direct competitors such as Caribou Coffee, The Coffee Bean, Seattle’s Best, Gloria Jean’s, Costa, Lavazza, Tully’s, Peet’s and literally dozens of chain and independent coffee shops are competing for Starbucks’ customers. Simultaneously competition from low priced alternatives is emerging from brands like Dunkin Donuts and McDonald’s, now catering more to coffee lovers. And non-coffee fast casual shops are seeking to attract more people for congregating, such as Panera, Fuddruckers, Pei Wei, TGI Friday’s and others. All of these are competitors, either directly or indirectly, for the customer dollars sought by Starbucks. Are more Starbucks stores going to succeed?

As McDonald’s, Pizza Hut and other fast food chains learned the hard way, there comes a time when a brand has built all the market needs. Then leadership has to figure out how to do something else. McDonald’s invested heavily in Boston Market and Chipotle’s, but let those high growth operations go when it decided to refocus on its “core” hamburger business – leading to heavy valuation declines. Starbucks is closing Teavana, but should it? When will Starbucks saturate? And what will Starbucks do to grow when that happens?

Starbucks has had a great run. And that run appears not fully over. But long-term investors have reason to worry.

Is it smart to make such a huge bet on China?

Will store growth successfully continue, with all the stores that already exist?

Will direct and indirect competitors eat away at market share?

What will Starbucks do when it has reached it market maximum, and it doesn’t seem to have any emerging new store concepts to build upon?

by Adam Hartung | Jul 14, 2017 | In the Rapids, Innovation, Marketing

Amazon just had another record Prime Day, with sales up 60%. And the #1 product sold was Amazon’s Echo Dot speaker. At $34.99 it surpassed last year’s unit sales by seven-fold. And the traditional Echo speaker, marked down 50% to $90, broke all previous sales records.

Amazon just took a commanding lead in the voice assistant platform market

These Echo sales most likely sealed Amazon’s long-term leadership in the war to be the #1 voice assistant. Amazon already has 70% market share in voice activated speakers, nearly 3 times #2 provider Google. And all other vendors in total barely have 5% share.

While it may seem like digital speakers are no big deal, speaker sales are analogous to iPhone sales when evaluating the emergence of smartphones and apps. The iPhone seemed like a small segment until it became clear smartphones were the new personal technology platform. Apple’s early lead allowed iOS to dominate the growth cycle, making the company intensely profitable.

Echo and Echo Dot aren’t just speakers, but interfaces to voice activated virtual assistants. For Echo the platform is Amazon’s Alexa. Alexa is to voice activated devices and applications what iOS was to Smartphones. By talking to Alexa customers are able to do many things, such as shopping, altering their thermostats, opening and closing doors, raising and lowering blinds, recording people in their homes — the list is endless. And as that list grows customers are buying more Alexa devices to gain greater productivity and enhanced lifestyle. Echos are entering more homes, and multiplying across rooms in these homes.

Do you remember when early iPhone ads touted “there’s an app for that?” That tagline told customers if they changed from a standard mobile phone to a smartphone there were a lot of advantages, measured by the number of available apps. Just like iOS apps gave an advantage to owning an iPhone, Alexa skills give an advantage to owning Echo products. In the last year the number of skills available for Alexa has exploded, growing from 135 to 15,000. Quite obviously developers are building on Alexa much faster than any other voice assistant.

By radically cutting the price of both Echo Dot and Echo, and promoting sales, Amazon is creating an installed base of units which encourages developers to write even more skills/apps.

The more Alexa devices are installed, the more likely developers will write additional skills for Alexa. As more devices lead to more skills, skills leads to more Alexa/Echo capability, which encourages more people to buy Alexa activated devices, which further encourages even more skills development. It’s a virtuous circle of goodness, all leading to more Amazon growth.

For marketers it is important to realize that success really doesn’t correlate with how “good” Alexa works. Google’s Assistant and Microsoft’s Cortana perform better at voice recognition and providing appropriate responses than Alexa and Siri. But there are relatively few (almost no) devices in the marketplace built with Assistant or Cortana as the interface. Developers need their skills/apps to be on platforms customers use. If customers are buying speakers, thermostats and televisions that are embedded with Alexa, then developers will write for Alexa. Even if it has shortcomings. It’s not the product quality that determines the winner, but rather the ability to create a base of users.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

It is genius for Amazon to promote Echo and Echo Dot, selling both cheaper than any other voice activated speaker. Even if Amazon is making almost no profit on device sales. By using their retail clout to build an Alexa base they make the decision to create skills for Alexa easy for developers.

This is a horrible problem for Google, #2 in this market, because Google does not have the retail clout to place millions of their speakers (and other devices) in the market. Google is not a device company, nor a powerful retailer of Android devices. The Android device makers need to profit from their devices, so they cannot afford to sell devices unprofitably in order to build an installed base for Google. And because Android’s platform is not applied consistently across device manufacturers, Google Assistant skills cannot be assured of operating on every Android phone. All of which makes the decision to build Google Assistant skills problematic for developers.

Can Apple Stop the Alexa juggernaut?

The game is not over. Apple would like customers to use Siri on their iPhones to accomplish what Amazon and Alexa do with Echo. Apple has an enormous iPhone base, and all have Siri embedded. Perhaps Apple can encourage developers to create Siri-integrated apps which will beat back the Amazon onslaught?

Today, Apple customers still cannot use Siri to control their Apple TV (Though as of August, 2017, it’s been improved.), or make payments with ApplePay, for example. Nor can iPhone users tell Siri to execute commands for remote systems which are controlled by apps, like unlocking doors, turning on appliances, shooting remote security video or placing an on-line order. Apple has a lot of devices, and apps, but so far Siri is not integrated in a way that allows voice activation like can be done with Alexa.

Additionally, as big as the iPhone installed base has become, when comparing markets the actual raw number of speakers could catch up with iPhones. Echo Dot is $35. The cheapest iPhone is the SE, at $399 (on the Apple site although available from Best Buy at $160.) And an iPhone 7 starts at $650. The huge untapped Apple markets, such as China and India, will find it a lot easier to purchase low cost speakers than iPhones, especially if their focus is to use some of those 15,000 skills. And because of the low pricing ($35 to $90) it is easy to buy multiple devices for multiple locations in one’s home or office.

Will we look back and call Echo a Disruptive Innovation?

Innovator’s Dilemma

Recall the wisdom of Clayton Christensen‘s “Innovator’s Dilemma.” The incumbent keeps improving their product, hoping to maintain a capability lead over the competition. But eventually the incumbent far overshoots customer needs, developing a product that is overly enhanced. The disruptive innovator enters the market with a considerably “less good” product, but it meets customer needs at a much lower price. People buy the cheaper product to meet their limited goal, and bypass the more capable but more expensive early market leader.

Doesn’t this sound remarkably similar to the development of iPhones (now on version 8 and expected to sell at over $1,000) compared with a $35 speaker that is far less capable, but still does 15,000 interesting things?

The biggest loser in this new market is Microsoft

This week Microsoft announced another 1,500 layoffs in what has become an annual bloodletting ritual for the PC software giant. But even worse was the announcement that Microsoft would no longer support any version of Windows Phone OS version 8.1 or older – which is 80% of the Windows Phone market. Given that Microsoft has less than 2% market share, and that less than .4% of the installed smartphone base operates on Windows Phone, killing support for these phones will lead to sales declines. This action, along with gutting the internal developer team last year, clearly indicates Microsoft has given up on the phone business for good. This means that now Microsoft has no device platform for Cortana, Microsoft’s voice assistant, to use.

Microsoft ignored smartphones, allowing Apple’s iOS to become the early standard. Apple rapidly grew its installed base. Microsoft could not convince developers to write for Windows Phone because there weren’t enough devices in the market. Without a phone base, with tablet and hybrid sales flat to declining, and with PC sales in the gutter Cortana enters the market DOA (Dead On Arrival.) Even if it were the best voice assistant on the planet developers will not create skills for Cortana because there are no devices out there using Cortana as the interface.

So Microsoft completely missed yet another market. This time the market for voice activated devices in the smart phone, smart car or any other smart device in the IoT marketplace. It missed mobile, and now it has missed voice assist. As PC sales decline, Microsoft’s only hope is to somehow emerge a big winner in cloud storage and services (IaaS or Infrastructure as a Service) with Azure. But, Azure was a late-comer to the cloud market and is far behind Amazon’s AWS (Amazon Web Services.) Amazon has +40% market share, which is 40% more than the share of Microsoft, Google and IBM combined.

Build the base and developers will come…